Designing and Adjusting an Investment Strategy: Real Life Example

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Are Covered in Fgratt-The Importance of Financial Management

DOCUMENT RESUME ED 228 494, CE 035 688 AUTHOk Ashmore, M.. Catherine;,Pritz, Sandra G.. Managing the Finances. PACE Revised..Level 1.-Unit 16. Research & Development Series No. 240AB16. INSTITUTION Ohlio State Univ:, Columbus. National Center for Research in Vocational Education. .SPONS AGENCY Office of Vocational and Adult Education (ED), Washington, DC. PUB DATE 83 CONTRACT 300-78-0032 'NOTE 23p.; For related dOcuMents, see CE 035' 672,-729.. AVAILABLE FROM 'National Center Publications, Box.F, The Ohib State University, 1960 Kenny Road, Columbus, OH 43210 (Complete set--$120.00; individual levels--$45.00 each; instructors' guides--$14.50 each; resource guide--$7.95; module sets--$35.06 each level; individual modules--$2.50 each). PUB TYPE' Guides.- Classroom Use.- Materials '(For Learner) (051) EDRS PRICE MF01/PC01 Plus Postage. DESCRIPTORS Behavioral Objectives; Business Administration; *Business Education; Career Choice; Data ProceSsing; Definitions; *Entrepreneurship; Learning Activities; *Money Managemeht; *ReCordkeeping; Records (Forms.); Secondary Education; *Small Businesses;. Units of Study IDENTIFIERS *Business Finance; *Ptogram for Acquiring Competehce Entrepreneurship ABSTRACT This lesson on competent financial management, the 16th in a series of 18 units, is part of the first level of a comprehensive entrepreneurship curriculum entitled: A Pro§ram for Acquiring Competence in Entrepreneurship (PACE),:(Designed for use with secondary students; the first level of PACE introduces students to the concepts involved in entrepreneurship and helps them become aware of entrepreneurship as a career option.) The following topics . are covered in fgraTt-the importance of financial management, the' components of a balance sheet the differences between current and fixed assets and current and fjixe labilitie, the components of a profit and loss statement, meehods 4or-calculating selected financial ratios, sources of financial ratio d'ata,'and the activittes associated with electronic data processing and,financial analysis. -

Tax Accounting

CORPORATE BUSINESS TAXATION MONTHLY Tax Accounting BY JAMES E. SALLES n this month’s column: you have an intangible asset, what kinds of expenditures are includable in its basis? Any self-constructed asset, of I course, presents the potential issue of how to determine • In Wells Fargo & Co. v. Commissioner,1 the Eighth its cost. In contrast to the situation as to real and tangible Circuit overturns a Tax Court holding that required personal property, however, there is little guidance as to the taxpayer to capitalize a portion of executives’ how to determine the “cost” of intangible assets, particu- salaries in a corporate acquisition. larly the somewhat amorphous intangibles frequently • The Tax Court holds in Chrysler Corporation v. involved in post-INDOPCO capitalization cases. 2 Commissioner that estimated warranty costs can- The Facts of Wells Fargo not be deducted when a car is sold. The expenditures at issue in Wells Fargo were incurred TAX COURT REVERSED IN by a target bank that was eventually absorbed into ANOTHER CAPITALIZATION CASE Norwest. The parties agreed that INDOPCO required the target to capitalize expenditures attributable to the In Norwest Corporation v. Commissioner,3 discussed in acquisition, but disagreed as to which those were. this column in CBTM’s inaugural issue,4 the Tax Court held The first controversy concerned fees paid lawyers and investment bankers during the run-up to the transaction. • that the taxpayer had to capitalize “preparatory The taxpayer argued these were generic “investigatory expenditures” -

Fair Value Hedge Accounting Z Cash Flow Hedge Accounting

Dao (道) Meets Mo (魔) Accounting Challenged by Modern Banking Pierre Jinghong Liang (梁景宏) Carnegie Mellon University For presentation at Southwest University of Finance and Economics (西南财经大学) 2011.7.7 Accounting: a Brief History 2011.7 SWUFE Accounting Challenged by Modern Banking 2 Accounting: a Brief History z 8500 B.C. ClaClay tokens made in shapes to represent variou s commodities constitute first record keeping system z 200 B.C. Symbols for all Arabic numerals except zero devised by Hindus in India z 600 A.D. Zero was developed . The 10-numeral system spread by traders throughout Europe in the 800s 2011.7 SWUFE Accounting Challenged by Modern Banking 3 Accounting: a Brief History 2011.7 SWUFE Accounting Challenged by Modern Banking 4 Accounting: a Brief History z 1400s: Double-entry bookkeeping used in Italy z 1494: Italian monk and scholar Luca Pacioli published the first known tttext (Summa) on the practice of dbldouble-entry bkkibookkeeping z 1845: Business corporation law passed in England z 1887: The predecessor of AICPA founded z 1904: Association of Chartered Certified Accountants founded z 1934: Securities Exchange Act establishes the SEC and mandates audits for all listed companies z 1940: the landmark Paton-Littleton Monograph published 2011.7 SWUFE Accounting Challenged by Modern Banking 5 High Praises for Bookkeeping Bookkeeping is “one of the “Bookkeeping is one of two fairest inventions of perfect sciences.” human mind.” 2011.7 SWUFE Accounting Challenged by Modern Banking 6 Accounting: a Brief History z 1973: Current -

Page 1 Iind SEMESTER B COM (2017 ADMISSION) FINANCIAL ACCCOUNTING – QUESTION BANK 1. out of the Following, Direct Expense Is A

School of Distance Education IInd SEMESTER B COM (2017 ADMISSION) FINANCIAL ACCCOUNTING – QUESTION BANK 1. Out Of The following, Direct Expense Is A) Salaries b) carriage outward c) rent of office building d) carriage inward 2. Goodwill is a a) Fixed asset b) current asset c) intangible asset d) fictitious asset 3. Income received in advance is a) An income b) a liability c) an asset d) a loss 4. Sales are equal to a) Cost of goods sold plus profit b) cost of goods sold minus gross profit c) gross profit minus cost of goods sold d) none of these 5. Interest on drawings is a) An expenditure for the business b) an expense for the business c) a gain for the business d) a loss for the business 6. Which of the following is not a fixed asset a) Motor cycles b) furniture c) inventory d) free hold property 7. Which of the following is a current liability a) A five year bank loan b) workmen compensation fund c) bank overdraft d) dividend equalization 8. Which of the following is not an intangible asset a) Stock b) goodwill c) trade mark d) patents. 9. In the case of net worth method of single entry system, the net profit is ascertained by a) Preparing trading and profit and loss account b) comparing opening and closing capital c) preparing d) none of these 10. Capital at the beginning of the year is ascertained by preparing a) Cash account b) opening statement of affairs c) total creditors account d) total debtors account. -

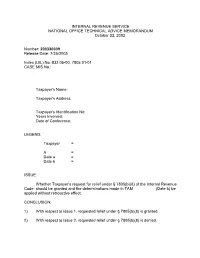

200330009 Release Date: 7/25/2003

INTERNAL REVENUE SERVICE NATIONAL OFFICE TECHNICAL ADVICE MEMORANDUM October 22, 2002 Number: 200330009 Release Date: 7/25/2003 Index (UIL) No.:832.05-00, 7805.01-01 CASE MIS No.: Taxpayer's Name: Taxpayer's Address: Taxpayer's Identification No: Years Involved: Date of Conference: LEGEND: Taxpayer = A = Date a = Date b = ISSUE: Whether Taxpayer’s request for relief under § 7805(b)(8) of the Internal Revenue Code should be granted and the determinations made in TAM (Date b) be applied without retroactive effect. CONCLUSION: 1) With respect to issue 1, requested relief under § 7805(b)(8) is granted. 2) With respect to issue 2, requested relief under § 7805(b)(8) is denied. 2 FACTS: Taxpayer, a property and casualty insurance company, is taxed under the provisions of Part II of Subchapter L of the Internal Revenue Code. Taxpayer issues retrospectively rated insurance policies. These policies provide for retrospective premium adjustments generally referred to as “retro debits” and “retro credits.” A retro debit represents an additional premium amount due from a policyholder if the actual premium, calculated based on a retrospective rating formula which takes into account the amount of losses and loss expenses incurred, exceeds the amount previously collected from the policyholder. A retro credit represents a premium refund owed to a policyholder where the amount collected from the policyholder exceeds the actual policy premium determined under the retrospective rating formula. On Date a, the Service issued a technical advice memorandum (1967 TAM), to A addressing the recognition of retro credits from retrospectively rated insurance policies in the computation of income. -

52900646.Pdf

WORKING CAPITAL AT A GLANCE INTRODUCTION TYPES FEATURES DETERMINANTS COMPONENTS WORKING CAPITAL CYCLE INTRODUCTION A successful sales program is necessary for earning profits by any business enterprise. Sales don’t convert into cash instantly. There is a time lag between the sale of goods and receipt of cash. Therefore, there is a need for working capital in the form of current assets to deal with the problem arising out of the lack of immediate realization of cash against goods sold. Therefore sufficient working capital is necessary to sustain sales activity. Defination of Working Capital:- According to C.W. Gestenbergh- “Working capital is ordinarily defined as the excess of the current assets over current liabilities”. According to Lawrence. J. Gitmen “The most common defination of working capital is the difference of the firm’s current assets and current liabilities.” Defination of working capital management:- “Working capital management involves the relationship between a firm's short-term assets and its short-term liabilities. The goal of working capital management is to ensure that a firm is able to continue its operations and that it has sufficient ability to satisfy both maturing short-term debt and upcoming operational expenses. The management of working capital involves managing inventories, accounts receivable and payable, and cash.” -From WWW.STUDYFINANCE.COM Management of working capital Guided by the above criteria, management will use a combination of policies and techniques for the management of working capital. These require managing the current assets - generally cash and cash equivalents, inventories and debtors. There are also a variety of short term financing options which are considered. -

Pension Fund Asset Allocation and Liability Discount Rates: Camouflage and Reckless Risk Taking by U.S

Pension Fund Asset Allocation and Liability Discount Rates: Camouflage and Reckless Risk Taking by U.S. Public Plans?∗ Aleksandar Andonov Maastricht University Rob Bauer Maastricht University Martijn Cremers University of Notre Dame May 2013 Abstract Using an international pension fund database, we compare the asset allocations, liability discount rates, and performance across six groups: public and private pension funds in three regions (United States, Canada, and Europe). U.S. public funds face distinct regulations that link the liability discount rate to their expected return on assets rather than to the riskiness of their promised pension benefits. Accordingly, they behave differently from all other pension funds. In the past two decades, U.S. public pension funds uniquely increased allocations to riskier investments to maintain high discount rates (especially as more members retired), thereby camouflaging the degree of underfunding. This increased risk-taking is associated with an annual underperformance of more than 60 basis points and seems to be driven by the conflict of interest between current and future stakeholders, and could result in significant costs to future workers and taxpayers. JEL classification: G11, G18, G23, H55. Keywords: pension funds, public policy, defined benefit, risk-taking, asset-liability management, asset allocation, liability discount rates, retirement, mature, regulation. ∗Contact authors via email at [email protected], [email protected] and mcre- [email protected]. We thank CEM Benchmarking -

Actuarial Research Clearing House 1993 VOL. 1 a Market

ACTUARIAL RESEARCH CLEARING HOUSE 1993 VOL. 1 A Market Value Balance Sheet: Why and How M. C. Modisett During the next few years, a revolution may hit the financial and insurance industries as financial reporters overhaul the methods currently employed to evaluate companies' financial starements. While the insurance community" has reported the position of companies using book value accounting for a major portion of this century, recent events (see Griffin in [I]) have motivated professionals to revisit their methods of accounting in order to more accurately reflect the market value of each company's holdings. To report marketable insu'uments at a close approximanon of their market value while treating nonmaskemble |nslruments in a consistent manner presents a theoretical challenge. The following paper presents a theoretical framework to approach this challenge. History Grif~fin in [1] describes the current trends towards market value accounting, demonstrating that, with good management, stable surplus readily arises with market valuing of assets and liabili~es, sod i]lustranng how market value accounting could *tert management to asset- liability mismatch risks. We illustrate the concerns with market value repor~g by presenting a brief history of book valae accounting. The following history consututes a brief summary from which we can observe salient wends. Early in this century, assets were carried on financial statements at their observed market values. Insurance liabilities were valued as expected cash flows discounted at regulatorily specified discount rares.a In this early period marke~s varied little, rising at a moderate rate on a total return basis. A company assuming no new premiums could look forward to a smooth growth pattern of assets, liabililies and surplus. -

Funds Flow Statement Introduction

FUNDS FLOW STATEMENT INTRODUCTION The basic financial statements i.e., the Balance Sheet and Profit & Loss A/c or Income Statement of business reveals the net effect of various transactions on operational and financial position of the company. The balance sheet gives a summary of the assets & liabilities of an undertaking at a particular point of time. There are many transactions that take place in an undertaking and which do not operate Profit & Loss A/c. Thus another statement has to be prepared to show the change in Assets & Liabilities from the end of one period of time to the end of another period of time. The statement is called a statement of changes in financial position or a Funds Flow Statement. The Funds Flow Statement is a statement which shown the movement of funds and is a report of financial operations of business undertaking. In simple words it is a statement of source and application of funds. In any business we can not under estimate the flow of funds from two operations. The business runs with funds but the organization knows how to flow of funds. The Funds Flow Statement is concerned with sources and applications of organization. Statement of changes in working capital shows the increase or decrease in the working capital. “Funds from Operations” statement shows how much funds from operations. MEANING & CONCEPT OF FUNDS The term “Fund” has been defined and interpreted differing by different experts. Broadly the term fund refers to all the financial resource of the company on the other extreme fund has been understood as cash only. -

The Fact of the Liability Requirement in the All Events Test—Flying Lessons Over the Dark Clouds of General Dynamics from a Giant Eagle

THE FACT OF THE LIABILITY REQUIREMENT 635 The Fact of the Liability Requirement in the All Events Test—Flying Lessons over the Dark Clouds of General Dynamics from a Giant Eagle PHILIP G. COHEN* Abstract For taxpayers employing the accrual method of accounting, a liability is generally deductible for federal income tax purposes “in the taxable year in which all the events have occurred that establish the fact of the liability, the amount of the liability can be determined with reasonable accuracy, and economic performance has occurred with respect to the liability.” The first requirement of the all events test, establishing the fact of the liability, was the subject of a thought-provoking Third Circuit decision, Giant Eagle, Inc. v. Commissioner, a case in which the taxpayer prevailed. In Giant Eagle, the dissenting judge, Thomas M. Hardiman, determined that the majority’s rea- soning contained a fatal flaw: it did not adequately address the fact that the rebate program established by the taxpayer included an expiration provision on claims not filed within a prescribed time frame. This Article utilizes Giant Eagle to analyze conditions precedent that are real versus those that are mere technicalities, the differences between conditions precedent and conditions subsequent, and the effect of waivers upon establishing the fact of the liability. Other important lessons are garnered from the examination of Giant Eagle, including overcoming the questionable decision of the Supreme Court in United States v. General Dynamics Corp. * Associate Professor of Taxation, Pace University Lubin School of Business; Retired Vice President-Tax & General Tax Counsel, Unilever United States, Inc.; B.A. -

Audited Financial Statements for Fiscal Year

LAWRENCE UNIVERSITY OF WISCONSIN Appleton, Wisconsin FINANCIAL STATEMENTS Including Independent Auditors' Report As of and for the Years Ended June 30, 2014 and 2013 LAWRENCE UNIVERSITY OF WISCONSIN TABLE OF CONTENTS Independent Auditors' Report 1 Financial Statements Statements of Financial Position 2 Statements of Activities 3-4 Statements of Cash Flows 5 Notes to Financial Statements 6-34 ~AKER TILLY Baker T ill) Vtrchow Krause, LLP 777 E Wisconsin Ave, 32nd Floor M ilwaukee, WI 53202-5313 rel414 777 5500 fa" 414 777 5555 bakerrilh com INDEPENDENT AUDITORS' REPORT To the Board of Trustees Lawrence University of Wisconsin Appleton, Wisconsin We have audited the accompanying financial statements of Lawrence University of Wisconsin (the "University"), which comprise the statements of financial position as of June 30, 2014 and 2013, and the related statements of activities and cash flows for the years then ended, and the related notes to the financial statements. Management's Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors' Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free from material misstatement. -

Earnings Focused Asset-Liability Management by Barry Freedman

Article from: Risks and Rewards Newsletter August 2005 – Issue No. 47 Earnings Focused Asset-Liability Management by Barry Freedman Introduction This article is based on research by the author for the purpose of completing his professional development project as a partial fulfillment of his FSA requirements. The views here are two main techniques for evaluat- expressed in this article are those of the author alone and ing the financial impact of interest rate do not reflect the asset-liability management strategies of movements on insurance companies: his employer. duration measures and computer simula- tions. In many ways these approaches provide complementary viewpoints. The duration approach to evaluating interest rate risk is based on a relatively simple theoretical model.1 The basic goal of the duration approach is to evaluate Tthe impact of interest rate movements on the market values of assets and liabilities. Although the model has evolved since its description by Redington, its fundamental properties have remained unchanged— this model is essentially based on market value meas- ures. On the other hand, earnings (GAAP, statutory and tax) are based on book value measures, such as net investment income and change in reserves. The duration approach, even at its most complicated, can therefore only approximate the impact of interest rate movements on earnings. In contrast to the duration approach, computer simulation based asset-liability management (ALM) models typically take a large amount of asset and liability data and apply borrowing and reinvestment strategies to project financial experience. Although these simulation models will often produce market value outputs, their focus tends to be on a balance sheet and income statement presentation.