BOSTON UNIVERSITY Independent Auditors' Reports As Required By

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Eminent Philosopher a Passion for Languages Physicist and Philosopher

tics from the University of Wisconsin, teaches his class, Linguistic Problems Eminent Philosopher Madison, in 1955. in the Teaching of English as a Foreign With his passion for languages, Saitz Language. “I cannot fi ll his shoes, of !""##$ %&'(&##", 86, a College of was an expert in applied linguistics and course, but for one night a week I can Arts & Sciences professor emeritus of kinesics, or gestures, who “found humor try.” ()&&*+)# ,"-)$ (.%!’16) philosophy, on August 12, 2015. in the way people would say things and One of the world’s eminent philosoph- even in the crazy rules of English,” says Physicist and Philosopher ers and logicians, Hintikka was born in his son, Richard Saitz (CAS’87, MED’87), Vantaa, Finland, in 1929, a BU School of Public Health "*'+) -%&0$'1, 87, a College of and educated at the Uni- professor and chair of com- Arts & Sciences professor emeritus versity of Helsinki, where munity health sciences and a of philosophy and of physics, on Aug- he earned a PhD in phi- School of Medicine profes- ust 8, 2015. losophy in 1956. sor of medicine. “He married Shimony’s research transcended dis- In 1990, he joined the BU my mom, who was primarily ciplinary boundaries and literary genres. philosophy faculty, where Hintikka a Spanish speaker, and he He made lasting contributions to the ar- his expertise in game- seemed to really enjoy people eas of inductive logic, the philosophy of theoretical semantics and epistemic who spoke other languages.” C. S. Peirce, the quantum measurement logic (the logic of knowledge and belief) Saitz was dedicated to teaching problem, and Bell’s theorem. -

The University of Iowa 2021-22 General Catalog 1

The University of Iowa 2021-22 General Catalog 1 The University of Iowa 2021-22 General Catalog The General Catalog provides information about academic programs at the University of Iowa, one of three universities governed by the Board of Regents, State of Iowa. The Catalog also provides links to supporting offices at the University, a list of administrative officers, an A-Z list of University of Iowa faculty members, a University calendar, and a link to the Code of Iowa for information regarding admission requirements and Iowa resident/nonresident standing. The General Catalog is published for informational purposes and should not be construed as the basis of a contract between a student and the University of Iowa. Every effort is made to provide information that is accurate at the time of publication. However, information on courses, curricula, fees, policies, regulations, and other matters is subject to change any time during the period for which the Catalog is in effect. For PDF versions of archived back editions, visit Archive on the Catalog website. The General Catalog is produced by the Office of the Registrar. Your comments and suggestions are welcome. Questions concerning the Catalog may be directed to the Office of the Registrar at [email protected]. The University of Iowa is accredited by the Higher Learning Commission. The University is a member of the Association of American Universities and is associated with Indiana, Michigan State, Northwestern, Ohio State, Pennsylvania State, Purdue, and Rutgers Universities and the Universities of Illinois, Maryland, Michigan, Minnesota, Nebraska-Lincoln, and Wisconsin-Madison in the Big Ten Conference. -

Teh-Yuan Ho, Ph.D

CURRICULUM VITAE Teh-Yuan Ho, Ph.D. Department of Animal Sciences Tel: 848-932-6328 School of Environmental and Biological Sciences Fax: 732-932-6996 Rutgers, The State University of New Jersey Foran Hall, 59 Dudley Road, Rm 126 [email protected] New Brunswick, NJ 08901-8525 animalsciences.rutgers.edu EDUCATION 1991 Ph.D., Plant Biology Rutgers University 1986 M.S., Biology University of Iowa 1979 B.S., Agronomy National Taiwan University PROFESSIONAL POSITIONS 2013-Present Research Associate Department of Animal Sciences, Rutgers University 2012 Visiting Scholar Institute of Molecular Biology, National Chung-Hsing University, Taichung, Taiwan 2011 Plant Biologist USDA, Center for Plant Health Science and Technology (CPHST) 2003-2011 Research Associate Department of Animal Sciences, Rutgers University 2002-2003 Research/Teaching Specialist School of Public Health, University of Medicine and Dentistry of New Jersey (UMDNJ) 1995-2000 Research/Teaching Specialist Department of Environmental and Community Medicine, UMDNJ 1994-1995 Research Scientist Department of Developmental Chemotherapy, Memorial Sloan-Kettering 1 CURRICULUM VITAE Cancer Center 1991-1993 Postdoctoral Research Fellow Department of Pathology, Fox Chase Cancer Center 1986-1991 Teaching Assistant Department of Biochemistry and Microbiology, Rutgers University 1983-1986 Teaching Assistant Department of Biology, The University of Iowa PUBLICATIONS 1. Bagnell, C., Ho, TY., George, A., Wiley, A.A., Miller, D., Bartol, F. (2017) Maternal Lactocrine Programming of Porcine Reproductive Tract Development. Mol Reprod Dev. 84:957-968. 2. Ho, TY., Rahman, K M., Camp M E., Wiley, A A., Bartol, F F., Bagnell C. (2016) Timing and duration of nursing from birth affect neonatal porcine uterine matrix metalloproteinase 9 and tissue inhibitor of metalloproteinase 1. -

Division of Endodontics Director, Graduate Endodontics

Faculty Profiles Scott B. McClanahan Professor Director, Division of Endodontics Director, Graduate Endodontics Diplomate, American Board of Endodontics Dr. McClanahan received a B.A. in 1974 and D.D.S. in 1981 both from the University of North Carolina at Chapel Hill. In 1981, he entered the U.S. Navy as a dental officer. Dr. McClanahan was selected by the Navy for civilian specialty training and completed his certificate of residency in endodontics at Northwestern University Dental School as well as a M.S. from Northwestern University in 1989. After three assignments as a clinical endodontist, Dr. McClanahan joined the faculty of the Endodontics Department at the Naval Postgraduate Dental School, Bethesda, MD in 1998 and in 2001, assumed the responsibilities of Chairman of the Endodontics Department and Director of the Advanced Specialty Education Program in Endodontics. Dr. McClanahan retired from active duty in September 2005 and joined the faculty at the University of Minnesota, School of Dentistry in November of 2005. He is a Fellow of the International College of Dentists. Dr. McClanahan is a standing Director of the American Board of Endodontics 2013-9 and the 2018-9 President of the board. 1/10 Carolina Rodriguez-Figueroa Clinical Assistant Professor Director, Undergraduate Endodontics Director, Pre-Clinical Endodontics Course Dr. Carolina Rodriguez-Figueroa was born and raised in Caracas, Venezuela. In 2002, she received her dental degree from the Universidad Central de Venezuela School of Dentistry. In 2003, she was accepted into the Gerondontology Program at the “Universidad Complutense de Madrid”, Spain and upon completion of the program in 2004, worked in private practice in Venezuela. -

Download 2021 Report

2020-2021 Report NCAA DI, DII, DIII 2020-2021 130,9HO2UR7S Report The 2020-2021 school year brought challenges to every aspect of the student-athlete experience. From postponed seasons and canceled games to team quarantines and virtual classes, these changes included the ways in which student-athletes were able to engage with their communities. New and creative ways to reach people were rolled out as elementary school visits turned into zoom calls, visits to animal shelters changed to students creating dog toys out of old t-shirts. Letters were written, videos were made, food was donated as these student-athletes found safe ways to support those in need. While participation and hours may be lower than some of the past years, the spirit of giving back and helping others is as high as ever! 2.29million economic impact 1. Georgia Southern University MEN'S soccer P 2020-2021 NCAA DI O 2. Georgia Southern University T MEN'S Tennis S TOP 50 SCHOOLS ' 3. Tulane University 1.Tulane University 26.Towson University N MEN'S Basketball 2.University of Louisiana at Lafayette 27.North Carolina Central University E 3.University of Pittsburgh 28.Texas Christian University 4. U of Louisiana at Lafayette 4.University of Louisville 29.Texas A&M University M MEN'S GOlf 5.University of South Alabama 30.Florida State University 6.University of North Dakota 31.Kansas State University 5. UTRGV 7.University of Michigan 32.Quinnipiac University MEN'S GOlf 8.Boston College 33.University of Louisiana at Monroe 9.University of Miami 34.Northern Illinois University 10.University of Alabama at Birmingham 35.Washington State University 11.Bucknell University 36.Clemson University 12.James Madison University 37.University of Montana P 1. -

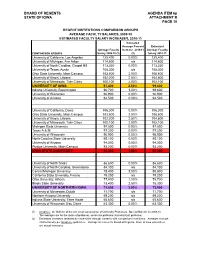

BOARD of REGENTS AGENDA ITEM 6P STATE of IOWA ATTACHMENT B PAGE 10

BOARD OF REGENTS AGENDA ITEM 6p STATE OF IOWA ATTACHMENT B PAGE 10 REGENT INSTITUTIONS COMPARISON GROUPS AVERAGE FACULTY SALARIES, 2009-10 ESTIMATED FACULTY SALARY INCREASES, 2010-11 Estimated Average Percent Estimated Average Faculty Increase 2010-11 Average Faculty COMPARISON GROUPS Salary 2009-10 (1) (2) Salary 2010-11 University of California, Los Angeles 125,400 0.00% 125,400 University of Michigan, Ann Arbor 114,600 n/a 114,600 University of North Carolina, Chapel Hill 113,330 0.00% 113,330 University of Texas, Austin 108,300 n/a 108,300 Ohio State University, Main Campus 103,500 2.00% 105,600 University of Illinois, Urbana 102,200 2.50% 104,800 University of Minnesota, Twin Cities 100,100 2.00% 102,100 UNIVERSITY OF IOWA 97,400 2.50% 99,800 Indiana University, Bloomington 96,700 3.00% 99,600 University of Wisconsin 96,900 0.00% 96,900 University of Arizona 94,500 0.00% 94,500 University of California, Davis 106,000 0.00% 106,000 Ohio State University, Main Campus 103,500 2.00% 105,600 University of Illinois, Urbana 102,200 2.50% 104,800 University of Minnesota, Twin Cities 100,100 2.00% 102,100 Michigan State University 97,500 0.00% 97,500 Texas A & M 97,200 0.00% 97,200 University of Wisconsin 96,900 0.00% 96,900 North Carolina State University 95,100 0.00% 95,100 University of Arizona 94,500 0.00% 94,500 Purdue University, Main Campus 93,200 0.00% 93,200 IOWA STATE UNIVERSITY 91,300 1.90% 93,000 University of North Texas 86,600 0.00% 86,600 University of North Carolina, Greensboro 84,100 n/a 84,100 Central Michigan University 78,400 3.00% 80,800 California State University, Fresno 79,200 n/a 79,200 Ohio University, Athens 77,900 1.00% 78,700 Illinois State University 73,400 2.50% 75,300 UNIVERSITY OF NORTHERN IOWA 71,800 3.00% 73,900 University of Minnesota, Duluth 71,700 n/a 71,700 Northern Arizona University 69,200 n/a 69,200 Indiana State University, Terre Haute 65,600 n/a 65,600 University of Wisconsin, Eau Claire 63,300 0.00% 63,300 (1) Academe, the Bulletin of the American Association of University Professors, Special Bulletin for 2009-10. -

List of Registered Participants As of 28

31st ANNUAL MIDWEST THEORY GET-TOGETHER 1:00 pm Friday - Noon Saturday September 28-29, 2018 Physics Division, Argonne National Laboratory Building 203 Auditorium PARTICIPANTS Dekrayat ALMAALOL Kent State University Xin AN University of Illinois at Chicago Kemal BASAR University of Illinois at Chicago Robert BASILI Iowa State University Joseph BONITATI Michigan State University Mark CAPRIO University of Notre Dame John CLARK Washington University in St. Louis Chrysovalantis CONSTANTINOU Monmouth College Pawel DANIELEWICZ Michigan State University Xiangai DENG Michigan State University Zhouyou FAN Michigan State University Christopher FASANO Monmouth College Patrick FASANO University of Notre Dame Dillon FRAME Michigan State University Gabriel GIVEN Michigan State University Alexander HABER Washington University in St. Louis Steven HARRIS Washington University in St. Louis Rongzheng HE Michigan State University Caleb HICKS Michigan State University Sirajudheen KUTHINI KUNHAMMED University of Iowa Dean LEE Michigan State University Ning LI Michigan State University Ruizi LI Michigan State University Shiyong LI University of Illinois at Chicago Hao LIN Michigan State University Huey-Wen LIN Michigan State University Bingnan LU Michigan State University Pierre NZABAHIMANA Michigan State University Soham PAL Iowa State University Maria PIARULLI Washington University in St. Louis Dragana PILIPOVIC University of Illinois at Chicago Wayne POLYZOU University of Iowa Maneesha PRADEEP University of Illinois at Chicago Avik SARKAR Michigan State University Shiplu SARKER Iowa State University James VARY Iowa State University Jacob WATKINS Michigan State University Andreas WINDISCH Washington University in St. Louis (cont’d) Daniel WINNEY Indiana University Ho-Ung YEE University of Illinois at Chicago Peng YIN Iowa State University Rui ZHANG Michigan State University Participating Members of the Argonne Theory Group: Kyle BEDNAR Noemi ROCCO Ian CLOËT Pedro RIVERO RAMIREZ Henning ESBENSEN Chao SHI Adam FREESE Andrea SIGNORI Alessandro LOVATO Robert WIRINGA 9/28/18 . -

Description of Omnipop for Proposals

Description of OmniPoP for Proposals Summary The OmniPoP is a collaborative effort between 12 of the member universities of the Big Ten Academic Alliance. Together, these institutions have pooled their efforts to create a high performance shared infrastructure based in the Chicago area. This infrastructure was designed to complement and augment the shared fiber infrastructure that the Big Ten Academic Alliance members had previously purchased. The OmniPoP operates a high capacity switching infrastructure that supports 10 gigabit and 100 gigabit connections to its member institutions and equivalent high capacity links to national research and education networks such as Internet2, ESnet, and Starlight. This allows OmniPoP connections to be leveraged to provide services to large data flows in support of multi-institutional cooperative research efforts. Efforts supported today include interconnections between the Large Hadron Collider (LHC) Tier 2 efforts at the member institutions and the Midwest Openflow Crossroads Initiative (MOXI) project which links several midwest regional networks to the GENI backbone. OmniPoP Infrastructure and Peerings The Omnipop infrastructure consists of a redundant pair of 100 gigabit capable switches. These switches operate from geographically diverse co-location facilities within the Chicago metropolitan areas. These facilities also serve as Points of Presence (PoPs) for other major networks such as Internet2, ESnet (Department of Energy’s Energy Sciences Network), and Starlight (the international peering exchange), enabling seamless cross connections to the major national and international research and education networks that support much of the academic research community. An additional benefit to these facilities is that they offer the opportunity for Big Ten Academic Alliance members to co-locate additional network related equipment in support of their own projects independent of the OmniPoP core infrastructure. -

Iowa State University, the University of Iowa and the University of Northern Iowa

Application Fee Waiver/Deferment Information for Iowa State University, the University of Iowa and the University of Northern Iowa Iowa State University 1. Apply Students should complete the online application for admission up to the payment screen at https://www.admissions.iastate.edu/apply/online/index.php. 2. Fee Waiver/Deferment Documentation • If the student is in a GEAR UP, TRIO Program or other similar program, their advisor should e-mail the Iowa State University Admissions Office stating the student’s participation. • If the student is not included in one of the above programs, an educator or parent may e-mail the Iowa State University Admissions Office explaining the student’s need for an application fee deferral. • If neither of the above is available, the student can e-mail the ISU Admissions Office to explain their situation. • ISU will always defer fees for students who receive free or reduced lunch, or qualify for the SAT/ACT fee waiver. Fee waiver documentation can be emailed to: [email protected] 3. Complete Application When the application and deferment request email are complete, the ISU Admissions Office will defer the fee and submit the application. When the student receives an admission decision, he or she can contact the ISU Admissions Office with their decision and receive assistance with deferring the $330 admissions acceptance fee as well. University of Iowa 1. Apply Students should complete the online application at https://apply.admissions.uiowa.edu/ admissions/login.page up to the payment section, and select Fee Waiver Option. 2. Fee Waiver/Deferment Documentation The University of Iowa Office of Admissions will accept any of the following forms of fee waiver documentation: • an ACT or SAT fee waiver; • a letter from a high school or college official on school letterhead confirming that payment of the fee would represent a significant financial hardship to the student and/or family; or • a letter from a TRIO program official verifying participation in a federal program for low- income students. -

Fact Book Office of Institutional Research Fact Book 2009-2010 Quick Facts

2009-2010 Fact Book Office of Institutional Research Fact Book 2009-2010 Quick Facts Location Ames, Iowa 50011 2008-2009 Degrees Awarded University President Gregory L. Geoffroy Bachelor’s 4,129 Board of Regents, State of Iowa, President David W. Miles 1st Professional 113 Homepage Address www.iastate.edu Master’s and Specialist 810 Office of Admissions Phone Number 800 262-3810 Ph.D. 316 University Accreditation The Higher Learning Commission Honorary Doctorate 3 and a Member of the North Total Living Alumni 214,225 Central Association Fiscal Year 2008-2009 Student Credit Hours 729,412 Fall 2009 Employee Headcount Organizational Structure Faculty 1,746 Colleges 8 Other Permanent Staff 4,375 Schools 1 Students and Hourly 8,318 Academic Departments 55 Total 14,439 Extension Areas 5 2008-2009 Revenues $991,568,000 Fall 2009 Headcount Enrollment State Appropriations 29.0% Undergraduate 22,521 Federal Appropriations 1.3% 1st Professional 564 Tuition and Fees 24.5% Graduate 4,860 Contracts and Grants 23.0% Total 27,945 Auxiliary Enterprises 13.7% Academic Year 2009-2010 Tuition and Fees Independent Operations 3.2% Undergraduate Resident $6,651 Other 5.3% Undergraduate Nonresident $17,871 Graduate Resident $7,565 2008-2009 Sponsored Funding Awarded $305,229,000 Graduate Nonresident $18,665 2008-2009 Gift Receipts and Commitments $127,749,000 1st Professional Resident $16,577 Inventory of Land Acres 11,373 1st Professional Nonresident $38,155 Academic Year 2009-2010 Room and Board $7,277 Fact Book 2009-2010 Office of Institutional Research 3410 Beardshear Hall Gebre H. Tesfagiorgis Director Iowa State University Sandra W. -

Gabriele Camera – Academic CV CONTACT INFORMATION

Gabriele Camera – Academic CV CONTACT INFORMATION Economic Science Institute, Chapman University, One University Drive, Orange, CA 92866. Tel: 714-628-2806. E-mail: RESEARCH INTERESTS Monetary Theory, Macroeconomics, Experimental Economics, Applied Theory, Search Theory, Labor. TEACHING Macroeconomics, Monetary Economics, Money and Banking (undergraduate, MBA, PhD) EDUCATION Degree Field Institution Year Ph.D. Economics University of Iowa 1997 MA Economics Miami University 1992 B.S. (Laurea) Business and Economics Universita’ di Urbino (Italy) 1991 Diploma Music (Clarinet) Conservatorio “Rossini” (Italy) 1985 ACADEMIC PROFESSIONAL EXPERIENCE 2012 - : Economic Science Institute, Chapman University. Research Professor of Economics and Finance. 2012 - 2103: University of Basel. Professor of Macroeconomics. 2009 - 2012 : Krannert School of Management, Purdue University. Professor of Economics. 2010 (Spring): University of Siena. Fulbright Siena Chair in Economics. 2009 (Spring): Institute for Advanced Studies, University of Bologna. Senior Visiting Fellow. 2007-2009: University of Iowa, Henry B. Tippie Research Professor of Economics 2003-2007: Krannert School of Management, Purdue University. Associate Professor. Promotion to Full Professor, August 2007. 2003: Dept. of Mathematics & Statistics, Universita’ di Napoli “Federico II”, Italy. Research Fellow. 2003 (Spring): Department of Economics, University of Texas at Austin. Visiting Professor. 1997-2003: Krannert School of Management, Purdue University. Assistant Professor. HONORS & AWARDS Excellence in Teaching. Krannert Executive Education Programs, Purdue University, 2010. Fulbright Distinguished Teaching Award, Siena Chair in Economics, 2009/2010 2nd Year Core Faculty of the Year Award, Tippie MBA program, University of Iowa, 2008 Dean’s Teaching Award, Tippie College of Business, University of Iowa, 2008 Honeywell research award, Krannert School of Management, Purdue University, 2006 Krannert Distinguished Teacher, MBA program, Purdue University, 2005. -

Nancy's Promise

PHOTOS 2014 Sarcoma Symposium Nancy’s Promise Newsletter of the University af Iowa Holden Cancer Center Melanoma and Sarcoma Tissue Bank Since 2008, the melanoma IN THIS ISSUE and sarcoma programs at the University of Iowa have been rapidly growing. We have two strong teams in Foreword both programs with highly page 2 specialized scientists Michael Henry, Ben Miller and Mo Milhem and physicians who are Patient Profiles dedicated to these fields. Melanoma Symposium pages 3-5 These teams have led and opened numerous clinical trials which have enhanced Patient Advocates research in both diseases. page 5 One of the most important resources to transpire is the MAST (Melanoma And Sarcoma Tissue bank). The MAST is a repository of new or Mast Poster previously diagnosed patients with proliferative disorders of the skin, ocular or pages 6-7 connective tissue disorders. The purpose of the MAST is to generate a comprehensive bank with biospecimen and clinical information that will contribute to the success of many multidisciplinary and translational research projects at the University of Iowa. Social Media By the Numbers pages 8-9 This is our first publication for you to meet the team at the University of Iowa for both (Follow us!) disease types, learn about initiatives, collaborations, new research ideas and patient stories. Research Groups page 10 The MAST is possible thanks to the generosity of grateful donors who support our 2013 Facebook: work and trust in our expertise to further research in these two diseases. Sarcoma Iowa Grant Recipients Melanoma Iowa pages 11-12 Mohammed M. Milhem, MD Twitter: Photos Deputy Director for Clinical Cancer Services pages 13-16 Holden Comprehensive Cancer Center @SarcomaIowa University of Iowa @MelanomaIowa Blog: ISSUE NUMBER 1 www.doctormoiowa.com 2014 Fall/Winter 2014 16 MAST Newsletter their way to do things for me much more than they needed to.