Welsh Government, and Latterly the WRA, Through the Processes of Design and Systems Testing

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Finance Committee the Land Transaction Tax (Transitional Provisions) (Wales) Regulations 2018

Finance Committee The Land Transaction Tax (Transitional Provisions) (Wales) Regulations 2018 This Statutory Instrument is being considered by the Finance Committee under Standing Order 27.8A. Background and Purpose 01. These Regulations make transitional provisions in respect of the introduction of land transaction tax (“LTT”) in Wales by the Land Transaction Tax and Anti- avoidance of Devolved Taxes (Wales) Act 2017 (“the LTTA Act”). The provisions ensure that transactions which take place on or after 1 April 2018 receive treatment which is consistent, meaning that transactions are not taxed twice under LTT and Stamp Duty Land Tax (“SDLT”), or not taxed at all. 02. The Regulations also ensure that arrangements commenced prior to 1 April 2018 and for which certain reliefs (which exist in both regimes) were claimed will continue to be relieved under LTT (subject to certain conditions being met). Further, the Regulations will also provide for transitional rules for the purposes of determining whether a transaction completed on or before 26 November 2018 is a higher rates residential property transaction where a person‘s main residence is being replaced. Procedure 03. Affirmative resolution. Merits Scrutiny 04. No points are identified for reporting in respect of this instrument. Policy objectives 05. Statement of policy intent 06. To support the Committee’s scrutiny of the Land Transaction Tax and Anti- avoidance of Devolved Taxes (LTTA) (Wales) Bill, the Welsh Government provided information on the policy intent for the delegated powers within the Bill. Regulations 1-2 07. Provides that the regulations come into force on the day Land Transaction Tax (LTT) commences and defines terminology. -

ON the HORIZON Mining Sector's Guide to Relevant Upcoming Legal, Commercial and Regulatory Changes and Developments January 2017

ON THE HORIZON Mining sector's guide to relevant upcoming legal, commercial and regulatory changes and developments January 2017 WHAT IS "ON THE HORIZON"? ■ A legal risk management tool tailored to your business. ■ Selected future legal, regulatory and commercial developments affecting the UK. ■ A quick guide to help you decide whether you need to know more. For further information, please use the links or contact one of our lawyers below. If you have any questions about this horizon scanning service, please email [email protected]. Petra Billing Roger Collier Office Managing Partner - Real Estate Partner - Real Estate T +44 207 7966 047 T +44 121 2625 661 [email protected] [email protected] Mining Sector - On the Horizon | 1 CONTENTS Planning conditions - consultation .......................................................................................................................................... 3 Compulsory purchase consultation ......................................................................................................................................... 3 Environmental justice in Scotland consultation ....................................................................................................................... 4 Aggregates levy in Scotland ................................................................................................................................................... 4 Fracking in Scotland .............................................................................................................................................................. -

Impact Assessment

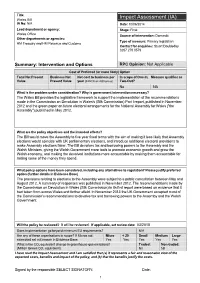

Title: Impact Assessment (IA) Wales Bill IA No: N/A Date: 10/06/2014 Lead department or agency: Stage: Final Wales Office Source of intervention: Domestic Other departments or agencies: Type of measure: Primary legislation HM Treasury and HM Revenue and Customs Contact for enquiries: Stuart Doubleday 0207 270 0579 Summary: Intervention and Options RPC Opinion: Not Applicable Cost of Preferred (or more likely) Option Total Net Present Business Net Net cost to business per In scope of One-In, Measure qualifies as Value Present Value year (EANCB on 2009 prices) Two-Out? No NA What is the problem under consideration? Why is government intervention necessary? The Wales Bill provides the legislative framework to support the implementation of the recommendations made in the Commission on Devolution in Wales's (Silk Commission) Part I report, published in November 2012 and the green paper on future electoral arrangements for the National Assembly for Wales ("the Assembly") published in May 2012. What are the policy objectives and the intended effects? The Bill would move the Assembly to five year fixed terms with the aim of making it less likely that Assembly elections would coincide with UK parliamentary elections, and introduce additional electoral provisions to make Assembly elections fairer. The Bill devolves tax and borrowing powers to the Assembly and the Welsh Ministers, giving the Welsh Government more tools to promote economic growth and grow the Welsh economy, and making the devolved institutions more accountable by making them accountable for raising some of the money they spend. What policy options have been considered, including any alternatives to regulation? Please justify preferred option (further details in Evidence Base) The provisions relating to elections to the Assembly were subject to a public consultation between May and August 2012. -

Country and Regional Public Sector Finances: Methodology Guide

Country and regional public sector finances: methodology guide A guide to the methodologies used to produce the experimental country and regional public sector finances statistics. Contact: Release date: Next release: Oliver Mann 21 May 2021 To be announced [email protected]. uk +44 (0)1633 456599 Table of contents 1. Introduction 2. Experimental Statistics 3. Public sector and public sector finances statistics 4. Devolution 5. Country and regional public sector finances apportionment methods 6. Income Tax 7. National Insurance Contributions 8. Corporation Tax (onshore) 9. Corporation Tax (offshore) and Petroleum Revenue Tax 10. Value Added Tax 11. Capital Gains Tax 12. Fuel Duties 13. Stamp Tax on shares 14. Tobacco Duties 15. Beer Duties 16. Cider Duties 17. Wine Duties Page 1 of 41 18. Spirits Duty 19. Vehicle Excise Duty 20. Air Passenger Duty 21. Insurance Premium Tax 22. Climate Change Levy 23. Environmental levies 24. Betting and gaming duties 25. Landfill Tax, Scottish Landfill Tax and Landfill Disposals Tax 26. Aggregates Levy 27. Bank Levy 28. Stamp Duty Land Tax, Land and Buildings Transaction Tax, and Land Transaction Tax 29. Inheritance Tax 30. Council Tax and Northern Ireland District Domestic Rates 31. Non-domestic Rates and Northern Ireland Regional Domestic Rates 32. Gross operating surplus 33. Interest and dividends 34. Rent and other current transfers 35. Other taxes 36. Expenditure methodology 37. Annex A : Main terms Page 2 of 41 1 . Introduction Statistics on public finances, such as public sector revenue, expenditure and debt, are used by the government, media and wider user community to monitor progress against fiscal targets. -

Your Monthly E-Bulletin

YOUR MONTHLY E-BULLETIN Issue 66; February 2019 LATEST CONSORTIUM NEWS Brexit and Working with LLG As you may know from e-mails recently sent out, the Ministry for Housing, Communities and Local Government (MHCLG) has requested LLG’s input into the impact of Brexit on Local Government providing a welcome opportunity to influence and scope the outcomes for local government once Brexit takes place. Thank you so much to those who have expressed an interest in helping LLG with this work from the NW region which should benefit all member organisations! Watch out for more news on this as the detail emerges. LGA and possible Local Authorities and Fire Service Legal Framework The Consortium is aware of correspondence from the LGA received later on last year concerning the possibility of a national framework to access external legal support. The Chair of your Management Board is in contact with the LGA about their proposals and is keeping up to date with the LGA intentions as they emerge. Information as to how such a framework would impact upon the work of the Consortium will be released as soon as more is known. Consortium FREE Training Programme 2018/2019 You can book yourselves, colleagues or clients on to our FREE courses through the website at www.nwlegalconsortium.com With this latest programme we have aligned all course start times as 10am to avoid confusion and assist all delegates in making their travel arrangements. Please note that 10am is the actual start of the training session. Coming up you’ve got: On 27th February we have our next -

The Welsh Government's Legislative Consent Memorandum on The

Welsh Parliament Finance Committee The Welsh Government’s Legislative Consent Memorandum on the United Kingdom Internal Market Bill November 2020 www.senedd.wales The Welsh Parliament is the democratically elected body that represents the interests of Wales and its people. Commonly known as the Senedd, it makes laws for Wales, agrees Welsh taxes and holds the Welsh Government to account. An electronic copy of this document can be found on the Welsh Parliament website: www.senedd.wales/SeneddFinance Copies of this document can also be obtained in accessible formats including Braille, large print, audio or hard copy from: Finance Committee Welsh Parliament Cardiff Bay CF99 1SN Tel: 0300 200 6565 Email: [email protected] Twitter: @SeneddFinance © Senedd Commission Copyright 2020 The text of this document may be reproduced free of charge in any format or medium providing that it is reproduced accurately and not used in a misleading or derogatory context. The material must be acknowledged as copyright of the Senedd Commission and the title of the document specified. Welsh Parliament Finance Committee The Welsh Government’s Legislative Consent Memorandum on the United Kingdom Internal Market Bill November 2020 www.senedd.wales About the Committee The Committee was established on 22 June 2016. Its remit can be found at: www.senedd.wales/SeneddFinance Committee Chair: Llyr Gruffydd MS Plaid Cymru Current Committee membership: Alun Davies MS Siân Gwenllian MS Welsh Labour Plaid Cymru Mike Hedges MS Rhianon Passmore MS Welsh Labour Welsh Labour Nick Ramsay MS Mark Reckless MS* Welsh Conservatives Independent *Mark Reckless was elected to the Finance Committee as a member of the Brexit Party until 16.10.2020. -

Finance Committee

------------------------ Public Document Pack ------------------------ Agenda - Finance Committee Meeting Venue: For further information contact: Committee Room 3 - Senedd Bethan Davies Meeting date: Thursday, 3 November Committee Clerk 2016 0300 200 6372 Meeting time: 09.00 [email protected] 1 Introductions, apologies, substitutions and declarations of interest 2 Paper(s) to note (09.00) (Pages 1 - 6) Additional evidence from the Law Society - Land Transaction Tax and Anti- avoidance of Devolved Taxes (Wales) Bill (Pages 7 - 10) Consultation responses: Dialogue - Land Transaction Tax and Anti-avoidance of Devolved Taxes (Wales) Bill (Pages 11 - 16) Additional evidence from the Land Registry - Land Transaction Tax and Anti- avoidance of Devolved Taxes (Wales) Bill (Pages 17 - 28) Additional evidence from CLA Cymru - Land Transaction Tax and Anti-avoidance of Devolved Taxes (Wales) Bill (Pages 29 - 30) Additional evidence from the Scottish Government - Land Transaction Tax and Anti-avoidance of Devolved Taxes (Wales) Bill (Pages 31 - 37) 3 Wales Audit Office and the Auditor General for Wales estimate of income and expenses: Evidence session (09.00-10.00) (Pages 38 - 313) Huw Vaughan Thomas – Auditor General for Wales Isobel Garner - Chair, Wales Audit Office Kevin Thomas – Director of Corporate Services Steven O’Donoghue – Director of Finance Paper 1 - Wales Audit Office - Estimate of income and expenses 2017-18 Paper 2 - The Wales Audit Office and Auditor General for Wales’ Annual Report and Accounts 2015-16 Paper 3 - Wales Audit Office- Final Audit Findings Report Year Ended 31 March 2016 Paper 4 - Wales Audit Office Annual Plan 2016-17 - Including additional information on our three-year strategy and priorities Paper 5 - Wales Audit Office - Interim Report – An assessment of progress made against our 2016-17 Annual Plan during the period 1 April to 30 September 2016 4 Motion under Standing Order 17.42 to resolve to exclude the public from the meeting for the following business: (10.00) Items 5, 9 and 10. -

Land Transaction Tax

STATES OF JERSEY Corporate Services Panel Review of Land Transaction Tax WEDNESDAY, 7th MAY 2008 Panel: Deputy PJ.D. Ryan of St. Helier (Chairman) Connétable J.L.S. Gallichan of Trinity Deputy R.G. Le Hérissier of St. Saviour Connétable D.J. Murphy of Grouville Mr. R. Teather (Adviser) Witnesses: Senator T.A. Le Sueur (The Minister for Treasury and Resources) Mr. K. Hemmings (Head of Decision Support) Deputy P.J.D. Ryan of St. Helier (Chairman): We do not want to spend too much time talking about the general principle behind the law because the States has ostensibly accepted it, except to say that there is an anomaly in that the States originally wanted you to look at commercial property and this law does not cover commercial property. It also does not cover all domestic property. Why does it not cover certain of the domestic transactions as well? Senator T.A. Le Sueur (The Minister for Treasury and Resources): You will have to identify to me which ones it does not cover before I can explain to you why it does not. Deputy P.J.D. Ryan: You have gone for where a transfer of a share, the share conveys legal right of occupation as a definition within the law whereas there are a number - not necessarily a large number - of particularly, probably, single dwellings as opposed to, say, apartments and particularly the older ones where for one reason or another the shareholder that buys the shares relies on the fact that he owns 100 per cent of the share capital of that particular company and can appoint his own directors and by so doing occupies the property rather than the shares themselves conveying that legal right. -

The Strange Reconstitution of Wales

THE STRANGE RECONSTITUTION OF WALES Richard Rawlings* Professor of Public Law, UCL; Honorary Distinguished Professor, Cardiff University; Leverhulme Major Research Fellow Wales; Devolution; Constitutional Change; Legislative Process; Brexit The emergence of determinedly forward-looking and principled approaches to the design and workings of the territorial constitution is a notable feature of public life in contemporary Wales. First Minister Carwyn Jones has adopted a ‘new Union’ mind-set in the light of devolution, so championing a looser and less hierarchical set of UK constitutional arrangements in which, grounded in popular sovereignty, the several systems of representative democracy pursue self-rule and shared rule in cooperative fashion.1 Building on, and even ranging beyond, the operational realities of quasi-federalism,2 some basic tenets of constitutional policy for the UK as a multi- (pluri-) national state3 are elaborated accordingly by the Welsh Government. Namely that the UK is best seen as a voluntary association of nations in which devolved institutions are effectively permanent features; in which the allocation of functions is based on the twin elements of subsidiarity and mutual benefit; and in which the relations of the four governments are characterised by mutual respect and parity of esteem.4 A form of ‘Greater England’ unionism, one which tolerates only limited territorial difference,5 this is not. Reference is also made in the context of Brexit to pooled and shared sovereignty within the UK,6 a challenging notion in more ways than one. For an uncodified constitution historically grounded in parliamentary sovereignty, such an advanced and even radical set of official perspectives is the more noteworthy coming as it does from the only devolved government fully committed to the UK. -

Fairness, Growth and Accountability

Fairness, Growth and Accountability Policy paper on the approach to Welsh Taxes Autumn Conference 2015 Ref: 2015/P-03 1 Table of Contents Background to Policy Document 3 Foreword 4 Introduction 5 Summary of Proposals 6 Tax Policy Principles 8 Income Tax 12 Green Taxes 17 Land Transaction Tax 23 Council Tax 28 Business Rates 33 2 Background to Policy Document This paper has been prepared as part of a project for Kirsty Williams AM, funded with the kind support of the Joseph Rowntree Reform Trust. The aim of this project is to explore the issues to ensure accountability, fairness and growth in those taxes within the remit of the National Assembly for Wales. This paper has been approved for publication by the Welsh Liberal Democrats’ Policy Committee as a policy paper for debate at the Welsh Liberal Democrat Autumn Conference in Swansea in November 2015. Within the policy-making procedure of the Liberal Democrats, the Federal Party determines the policy of the Party in those areas which might reasonably be expected to fall within the remit of the federal institutions in the context of a federal United Kingdom. The Party in England, the Scottish Liberal Democrats, the Welsh Liberal Democrats and the Northern Ireland Local Party determine the policy of the Party on all other issues, except that any or all of them may confer this power upon the Federal Party in any specified area. If approved by Conference, this paper will form the policy of the Welsh Liberal Democrats. Many of the policy papers published by the Welsh Liberal Democrats imply modifications to existing government public expenditure priorities. -

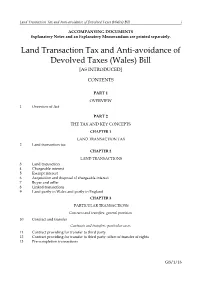

Land Transaction Tax and Anti-Avoidance of Devolved Taxes (Wales) Bill I

Land Transaction Tax and Anti-avoidance of Devolved Taxes (Wales) Bill i ACCOMPANYING DOCUMENTS Explanatory Notes and an Explanatory Memorandum are printed separately. Land Transaction Tax and Anti-avoidance of Devolved Taxes (Wales) Bill [AS INTRODUCED] CONTENTS PART 1 OVERVIEW 1 Overview of Act PART 2 THE TAX AND KEY CONCEPTS CHAPTER 1 LAND TRANSACTION TAX 2 Land transaction tax CHAPTER 2 LAND TRANSACTIONS 3 Land transaction 4 Chargeable interest 5 Exempt interest 6 Acquisition and disposal of chargeable interest 7 Buyer and seller 8 Linked transactions 9 Land partly in Wales and partly in England CHAPTER 3 PARTICULAR TRANSACTIONS Contracts and transfers: general provision 10 Contract and transfer Contracts and transfers: particular cases 11 Contract providing for transfer to third party 12 Contract providing for transfer to third party: effect of transfer of rights 13 Pre-completion transactions GB/1/16 Land Transaction Tax and Anti-avoidance of Devolved Taxes (Wales) Bill ii Substantial performance 14 Meaning of substantial performance Options etc. 15 Options and rights of pre-emption Exchanges 16 Exchanges CHAPTER 4 CHARGEABLE TRANSACTIONS AND CHARGEABLE CONSIDERATION Chargeable transactions 17 Chargeable transaction Chargeable consideration 18 Chargeable consideration 19 Contingent consideration 20 Uncertain or unascertained consideration 21 Annuities 22 Deemed market value 23 Exceptions PART 3 CALCULATION OF TAX AND RELIEFS Calculation of tax 24 Regulations specifying tax bands and tax rates 25 Procedure for regulations specifying -

Second Homes: Developing New Policies in Wales

Second homes: Developing new policies in Wales Author: Dr Simon Brooks Second homes: Developing new policies in Wales Audience Welsh Government departments; public bodies in Wales; community councils; third sector organisations in Wales; private sector companies in Wales; organisations working with communities; and other interested parties. Overview This report was initiated following the award of a small grant by the Coleg Cymraeg Cenedlaethol to Dr Simon Brooks, Associate Professor in the School of Management at Swansea University, to scrutinise policy on second homes in Wales and Cornwall. The original aim was to prepare a brief report focussing on the comparison between public policy solutions based on taxation policy (Wales) and planning policy (Cornwall). However, due to the increasing interest in this subject area, the Welsh Government’s Minister for Mental Health, Well-being and Welsh Language asked if the research could be expanded in order to scrutinise some wider issues regarding second homes and to make policy recommendations. Further information Enquiries about this document should be referred to: Welsh Language Division Welsh Government Cathays Park Cardiff CF10 3NQ e-mail: [email protected] Additional copies This document is available on the Welsh Government website at gov.wales/welsh-language Mae’r ddogfen yma hefyd ar gael yn Gymraeg. This document is also available in Welsh. © Crown copyright 2021 WG42058 Digital ISBN 978 1 80082 858 2 Contents Terms of Reference 1. Context 2. A regional and local problem – not a national problem 3. The impact of second homes on the sustainability of communities and the Welsh language 4. Brexit and Covid-19 – a reason to act 5.