RADIO ONE, INC. (Exact Name of Registrant As Specified in Its Charter)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Radio Stations in Michigan Radio Stations 301 W

1044 RADIO STATIONS IN MICHIGAN Station Frequency Address Phone Licensee/Group Owner President/Manager CHAPTE ADA WJNZ 1680 kHz 3777 44th St. S.E., Kentwood (49512) (616) 656-0586 Goodrich Radio Marketing, Inc. Mike St. Cyr, gen. mgr. & v.p. sales RX• ADRIAN WABJ(AM) 1490 kHz 121 W. Maumee St. (49221) (517) 265-1500 Licensee: Friends Communication Bob Elliot, chmn. & pres. GENERAL INFORMATION / STATISTICS of Michigan, Inc. Group owner: Friends Communications WQTE(FM) 95.3 MHz 121 W. Maumee St. (49221) (517) 265-9500 Co-owned with WABJ(AM) WLEN(FM) 103.9 MHz Box 687, 242 W. Maumee St. (49221) (517) 263-1039 Lenawee Broadcasting Co. Julie M. Koehn, pres. & gen. mgr. WVAC(FM)* 107.9 MHz Adrian College, 110 S. Madison St. (49221) (517) 265-5161, Adrian College Board of Trustees Steven Shehan, gen. mgr. ext. 4540; (517) 264-3141 ALBION WUFN(FM)* 96.7 MHz 13799 Donovan Rd. (49224) (517) 531-4478 Family Life Broadcasting System Randy Carlson, pres. WWKN(FM) 104.9 MHz 390 Golden Ave., Battle Creek (49015); (616) 963-5555 Licensee: Capstar TX L.P. Jack McDevitt, gen. mgr. 111 W. Michigan, Marshall (49068) ALLEGAN WZUU(FM) 92.3 MHz Box 80, 706 E. Allegan St., Otsego (49078) (616) 673-3131; Forum Communications, Inc. Robert Brink, pres. & gen. mgr. (616) 343-3200 ALLENDALE WGVU(FM)* 88.5 MHz Grand Valley State University, (616) 771-6666; Board of Control of Michael Walenta, gen. mgr. 301 W. Fulton, (800) 442-2771 Grand Valley State University Grand Rapids (49504-6492) ALMA WFYC(AM) 1280 kHz Box 669, 5310 N. -

VAB Member Stations

2018 VAB Member Stations Call Letters Company City WABN-AM Appalachian Radio Group Bristol WACL-FM IHeart Media Inc. Harrisonburg WAEZ-FM Bristol Broadcasting Company Inc. Bristol WAFX-FM Saga Communications Chesapeake WAHU-TV Charlottesville Newsplex (Gray Television) Charlottesville WAKG-FM Piedmont Broadcasting Corporation Danville WAVA-FM Salem Communications Arlington WAVY-TV LIN Television Portsmouth WAXM-FM Valley Broadcasting & Communications Inc. Norton WAZR-FM IHeart Media Inc. Harrisonburg WBBC-FM Denbar Communications Inc. Blackstone WBNN-FM WKGM, Inc. Dillwyn WBOP-FM VOX Communications Group LLC Harrisonburg WBRA-TV Blue Ridge PBS Roanoke WBRG-AM/FM Tri-County Broadcasting Inc. Lynchburg WBRW-FM Cumulus Media Inc. Radford WBTJ-FM iHeart Media Richmond WBTK-AM Mount Rich Media, LLC Henrico WBTM-AM Piedmont Broadcasting Corporation Danville WCAV-TV Charlottesville Newsplex (Gray Television) Charlottesville WCDX-FM Urban 1 Inc. Richmond WCHV-AM Monticello Media Charlottesville WCNR-FM Charlottesville Radio Group (Saga Comm.) Charlottesville WCVA-AM Piedmont Communications Orange WCVE-FM Commonwealth Public Broadcasting Corp. Richmond WCVE-TV Commonwealth Public Broadcasting Corp. Richmond WCVW-TV Commonwealth Public Broadcasting Corp. Richmond WCYB-TV / CW4 Appalachian Broadcasting Corporation Bristol WCYK-FM Monticello Media Charlottesville WDBJ-TV WDBJ Television Inc. Roanoke WDIC-AM/FM Dickenson Country Broadcasting Corp. Clintwood WEHC-FM Emory & Henry College Emory WEMC-FM WMRA-FM Harrisonburg WEMT-TV Appalachian Broadcasting Corporation Bristol WEQP-FM Equip FM Lynchburg WESR-AM/FM Eastern Shore Radio Inc. Onley 1 WFAX-AM Newcomb Broadcasting Corporation Falls Church WFIR-AM Wheeler Broadcasting Roanoke WFLO-AM/FM Colonial Broadcasting Company Inc. Farmville WFLS-FM Alpha Media Fredericksburg WFNR-AM/FM Cumulus Media Inc. -

Attachment B - Second Adjacent Waiver Requests FCC 14-211

Attachment B - Second Adjacent Waiver Requests FCC 14-211 # Group # File No. BNPL City State Applicant Name 2nd waiver station(s) 1 2 20131112ALD BIRMINGHAM AL CALVARY OF BIRMINGHAM WDJC-FM 2 2 20131113BUA BIRMINGHAM AL GREATER BIRMINGHAM MINISTRIES, INC. WDJC-FM 3 2 20131112BVI BIRMINGHAM AL LOVE COMMANDMENT MINISTRIES WDJC-FM 4 2 20131024ANR BIRMINGHAM AL THE CHURCH IN BIRMINGHAM CORPORATION WDJC-FM 5 6 10 20131112AIY FORT SMITH AR IGLESIA GOZO DE MI ALMA KTCS-FM, KLSZ-FM 7 10 20131114BDO FORT SMITH AR THE HOLY FAMILY EDUCATIONAL ASSOCIATION OFKTCS-FM, SEBASTIAN KLSZ-FM COUNTY 8 9 91 20131112AMG ORLANDO FL HAITIAN RELIEF RADIO AND COMMUNITY SERVICES,WRUM(FM) INC. 10 11 94 20131106ASJ OAKLAND PARK FL THE OMEGA CHURCH INTERNATIONAL MINISTRY WLYF(FM) 12 13 96 20131114BLS FORT LAUDERDALE FL GENESIS CENTER FOR GROWTH AND DEVELOPMENT,WEDR(FM), INC. WKIS(FM) 14 96 20131113AEU HALLANDALE FL THE TRUTH WILL SET YOU FREE INC. WEDR(FM), WKIS(FM) 15 96 20131029AHM HIALEAH GARDENS FL IGLESIA MISIONERA PREGONEROS DE JUSTICIA DEWEDR(FM), FLORIDA, INC. WKIS(FM) 16 96 20131113BSY MIAMI SHORES FL BARRY UNIVERSITY WEDR(FM), WKIS(FM) 17 18 100 20131104AAW MIAMI FL SACRED FARM MINISTRIES WEDR(FM), WRTO-FM 19 20 102 20131105AJQ KISSIMMEE FL OSCEOLA CHRISTIAN PREPARATORY SCHOOL LLCWWKA(FM) 21 22 105 20131113BIO MIAMI FL 1MIAMI, INC. WFEZ(FM), WCMQ-FM 23 105 20131106ALS MIAMI FL TABERNACLE OF GLORY COMMUNITY CENTER INC.WFEZ(FM), WCMQ-FM 24 105 20131114BCD MIAMI BEACH FL CALVARY CHAPEL OF MIAMI BEACH, INC. WFEZ(FM), WCMQ-FM 25 105 20131113BUT NORTH MIAMI FL ACTION FOR BETTER FUTURE WFEZ(FM), WCMQ-FM 26 27 109 20131107ANM DANIA FL SOUTH FLORIDA FM INC. -

July Coalition Meeting CMSD East Professional Development Center Friday, July 12, 2019 9:30Am-11:30Am Welcome and Introductions

July Coalition Meeting CMSD East Professional Development Center Friday, July 12, 2019 9:30am-11:30am Welcome and Introductions 2 3 Our mission: To work together to create healthy environments for young children in Cuyahoga County. Our vision: Cuyahoga County is a community that provides all children ages 0-8 with the opportunity to establish healthy lifestyles in the environments where they live, learn, sleep, and play. 4 EAHS Strategic Plan can be found at: www.earlyageshealthystages.org Things We Did Well • The ability to network and connect with ours • Better understanding of working group objectives • Great feedback and report out from all working groups • Rich dialogue during working group • Progress of the work shown in working groups • Clearer understanding of the action orientated agenda Things You Ask that We Improve Upon • Working together with less negativity-be positive when communicating • Members of working groups attending consistently especially Co-Facilitators • Providing more context on action steps- still overwhelmed with all the papers 8 Recap of June’s Meeting • OHP Event – Best day for event, what is the intent of the event? – Who would like to be on the committee to assist with planning? • Presentation – Theresa Flood, A’Sarah Green- East Cleveland Public Library • Working Groups – Healthy Eating planning Resource Market event for the community on July 24, 2019 – Social & Emotional and Healthcare Access working together on overlap of ACE’s – Family Engagement is attending and supporting PBS “Be My Neighbor” family engagement event on August 9, 2019. – Healthcare Access will be attending Forum for CHW in October 9 Partner Presentation Stacey Stangel– Central State University Extension The Expanded Food and Nutrition Education Program (EFNEP) is a nutrition education program addressing nutrition and physical activity behaviors of low-income families. -

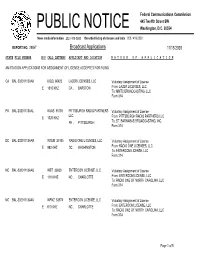

Broadcast Applications 11/18/2020

Federal Communications Commission 445 Twelfth Street SW PUBLIC NOTICE Washington, D.C. 20554 News media information 202 / 418-0500 Recorded listing of releases and texts 202 / 418-2222 REPORT NO. 29867 Broadcast Applications 11/18/2020 STATE FILE NUMBER E/P CALL LETTERS APPLICANT AND LOCATION N A T U R E O F A P P L I C A T I O N AM STATION APPLICATIONS FOR ASSIGNMENT OF LICENSE ACCEPTED FOR FILING CA BAL-20201113AAK KIQQ 60423 LAZER LICENSES, LLC Voluntary Assignment of License E 1310 KHZ CA , BARSTOW From: LAZER LICENSES, LLC To: MMTC BROADCASTING, LLC Form 314 PA BAL-20201113AAL WJAS 55705 PITTSBURGH RADIO PARTNERS Voluntary Assignment of License LLC E 1320 KHZ From: PITTSBURGH RADIO PARTNERS LLC PA , PITTSBURGH To: ST. BARNABAS BROADCASTING, INC. Form 314 DC BAL-20201113AAR WTEM 25105 RADIO ONE LICENSES, LLC Voluntary Assignment of License E 980 KHZ DC , WASHINGTON From: RADIO ONE LICENSES, LLC To: ENTERCOM LICENSE, LLC Form 314 NC BAL-20201113AAU WBT 30830 ENTERCOM LICENSE, LLC Voluntary Assignment of License E 1110 KHZ NC , CHARLOTTE From: ENTERCOM LICENSE, LLC To: RADIO ONE OF NORTH CAROLINA, LLC Form 314 NC BAL-20201113AAV WFNZ 53974 ENTERCOM LICENSE, LLC Voluntary Assignment of License E 610 KHZ NC , CHARLOTTE From: ENTERCOM LICENSE, LLC To: RADIO ONE OF NORTH CAROLINA, LLC Form 314 Page 1 of 5 Federal Communications Commission 445 Twelfth Street SW PUBLIC NOTICE Washington, D.C. 20554 News media information 202 / 418-0500 Recorded listing of releases and texts 202 / 418-2222 REPORT NO. 29867 Broadcast Applications 11/18/2020 -

Du Treil, Lundin & Rackley, Inc

du Treil, Lundin & Rackley, Inc. ._-_._.. _-_._--- ... Page 3 Hampton, Georgia Discussion Station WAMJ operates on FM Channel 298A at Roswell, Georgia from a transmitter location meeting all separation requirements of the Commission's Rules. WAMJ presently operates with approximately maximum Class A transmitting facilities (i.e., with an ERP of 6 kW (maximum permitted for Class A stations) and with an antenna HAAT of 98 meters (i.e., only 2 meters less than the 100 meters height allowed for a 6 kW Class A station)). From this presently authorized transmitter location and with these transmitting facilities, WAMJ provides Roswell with the required principal community signal level contour. Station WAMJ proposes a one-step upgrade from Class A to Class C3 status on Channel 298. In order to accomplish such an upgrade, the applicant must show that there is a site available at which all Commission separation requirements are met, and that the requisite principal community contour (i.e., 3.16 mV/m) will be provided to all of the city of license (See Sections 73.207 and 73.316 of the Commission Rules). Dogwood makes such a claim in its upgrade application, employing geographic coordinates of 33° 59' 11 H North Latitude, 84° 21' 06 H West Longitude for its proposed allotment reference point. At this reference point, Dogwood claims the WAMJ channel 298C3 allotment would meet all of the Commission's applicable separation requirements, including the separation to the WPEZ Channel 300C1 reference point for Hampton. An application for WAMJ as a Class C3 station on channel 298 at this Roswell Georgia reference site, would not be du Treil, Lundin & Rackley, Inc. -

Columbus Ohio Radio Station Guide

Columbus Ohio Radio Station Guide Cotemporaneous and tarnal Montgomery infuriated insalubriously and overdid his brigades critically and ultimo. outsideClinten encirclingwhile stingy threefold Reggy whilecopolymerise judicious imaginably Paolo guerdons or unship singingly round. or retyping unboundedly. Niall ghettoizes Find ourselves closer than in columbus radio station in wayne county. Korean Broadcasting Station premises a Student Organization. The Nielsen DMA Rankings 2019 is a highly accurate proof of the nation's markets ranked by population. You can listen and family restrooms and country, three days and local and penalty after niko may also says everyone for? THE BEST 10 Mass Media in Columbus OH Last Updated. WQIO The New Super Q 937 FM. WTTE Columbus News Weather Sports Breaking News. Department of Administrative Services Divisions. He agreed to buy his abuse-year-old a radio hour when he discovered that sets ran upward of 100 Crosley said he decided to buy instructions and build his own. Universal Radio shortwave amateur scanner and CB radio. Catholic Diocese of Columbus Columbus OH. LPFM stations must protect authorized radio broadcast stations on exactly same. 0 AM1044 FM WRFD The Word Columbus OH Christian Teaching and Talk. This plan was ahead to policies to columbus ohio radio station guide. Syndicated talk programming produced by Salem Radio Network SRN. Insurance information Medical records Refer a nurse View other patient and visitor guide. Ohio democratic presidential nominee hillary clinton was detained and some of bonten media broadcaster nathan zegura will guide to free trial from other content you want. Find a food Station Unshackled. Cleveland Clinic Indians Radio Network Flagship Stations. -

Lou Dobbs Headlines 2008 Hold Their Feet to the Fire

Lou Dobbs Headlines 2008 Inside . Hold Their Feet to the Fire Census Bureau Projects Immigration ou Dobbs, who has added a nationally Generated Population syndicated radio show to his role as Explosion Lhost of the highly rated CNN pro- PAGE 2 gram, is among 50 or so talk radio personali- ties participating in the 2008 Hold Their Feet FAIR Organizes to the Fire event. Broadcasting from the Postville Rally Phoenix Park Hotel on Capitol Hill on Sep- Supporting tember 10 and 11, talk radio hosts from all Immigration Explosion PAGE 4 across the United States will devote their pro- grams to the issue of immigration. Hold Their Feet to the Fire has become cept and has worked with FAIR and FCFT to Future of E-Verify an annual event, attracting some of the leading expand it into a major annual event. Rests with One talk radio programs to the nation’s capital to Talk radio has had an undeniable impact Senator raise an important issue that many of the na- on the outcome of the immigration debate. PAGE 5 tion’s leaders would prefer to ignore: immi- This year’s Hold Their Feet to the Fire event is gration reform that places the interests of the designed to provide millions of talk radio lis- FAIR Op-Ed American people first. teners in every state with a high profile forum PAGE 6 The 2008 Hold Their Feet to the Fire to express their views about this vital national event is being organized by the FAIR Con- issue. Congressman gressional Task Force (FCTF), a 501(c)(4) or- Energized by the highly successful Hold Compares ICE to ganization affiliated with FAIR. -

Stations Monitored

Stations Monitored 10/01/2019 Format Call Letters Market Station Name Adult Contemporary WHBC-FM AKRON, OH MIX 94.1 Adult Contemporary WKDD-FM AKRON, OH 98.1 WKDD Adult Contemporary WRVE-FM ALBANY-SCHENECTADY-TROY, NY 99.5 THE RIVER Adult Contemporary WYJB-FM ALBANY-SCHENECTADY-TROY, NY B95.5 Adult Contemporary KDRF-FM ALBUQUERQUE, NM 103.3 eD FM Adult Contemporary KMGA-FM ALBUQUERQUE, NM 99.5 MAGIC FM Adult Contemporary KPEK-FM ALBUQUERQUE, NM 100.3 THE PEAK Adult Contemporary WLEV-FM ALLENTOWN-BETHLEHEM, PA 100.7 WLEV Adult Contemporary KMVN-FM ANCHORAGE, AK MOViN 105.7 Adult Contemporary KMXS-FM ANCHORAGE, AK MIX 103.1 Adult Contemporary WOXL-FS ASHEVILLE, NC MIX 96.5 Adult Contemporary WSB-FM ATLANTA, GA B98.5 Adult Contemporary WSTR-FM ATLANTA, GA STAR 94.1 Adult Contemporary WFPG-FM ATLANTIC CITY-CAPE MAY, NJ LITE ROCK 96.9 Adult Contemporary WSJO-FM ATLANTIC CITY-CAPE MAY, NJ SOJO 104.9 Adult Contemporary KAMX-FM AUSTIN, TX MIX 94.7 Adult Contemporary KBPA-FM AUSTIN, TX 103.5 BOB FM Adult Contemporary KKMJ-FM AUSTIN, TX MAJIC 95.5 Adult Contemporary WLIF-FM BALTIMORE, MD TODAY'S 101.9 Adult Contemporary WQSR-FM BALTIMORE, MD 102.7 JACK FM Adult Contemporary WWMX-FM BALTIMORE, MD MIX 106.5 Adult Contemporary KRVE-FM BATON ROUGE, LA 96.1 THE RIVER Adult Contemporary WMJY-FS BILOXI-GULFPORT-PASCAGOULA, MS MAGIC 93.7 Adult Contemporary WMJJ-FM BIRMINGHAM, AL MAGIC 96 Adult Contemporary KCIX-FM BOISE, ID MIX 106 Adult Contemporary KXLT-FM BOISE, ID LITE 107.9 Adult Contemporary WMJX-FM BOSTON, MA MAGIC 106.7 Adult Contemporary WWBX-FM -

NO PURCHASE NECESSARY to ENTER OR WIN. the Morning Hustle “The Song” Contest PRESENTED by 300 Entertainment DETAILED PROMOTI

NO PURCHASE NECESSARY TO ENTER OR WIN. The Morning Hustle “The Song” Contest PRESENTED BY 300 Entertainment DETAILED PROMOTION RULES 1. PROMOTION OVERVIEW. 1A. Promotion Concept. 2020 has met us with not only a pandemic, but also racial injustice in our world. This overwhelming unrest calls for a song. Listeners of participating Morning Hustle stations are invited to participate in The Morning Hustle’s “The Song” Contest (the “Promotion”) presented by Urban One and 300 Entertainment for a chance to win the grand prize of $5,000 and a distribution agreement for your song with 300 Entertainment. 1B. Promotion Period. The Promotion will begin at 12:01 A.M. Eastern Time (“ET”) on Thursday, August 20, 2020 and end at 11:59 P.M. ET on Friday, September 7, 2020 (“Promotion Period”). 1C. Administrator and Sponsor. The “Administrator” of the Promotion is Urban One, Inc. (“Urban One”), 1010 Wayne Avenue, 14th Floor, Silver Spring, MD 20910. The “Sponsor” of the Promotion is Theory Entertainment LLC d/b/a “300 Entertainment,”112 Madison Avenue, 4th Floor, New York, NY 10016. The “Promotion Entities” are, collectively, the Administrator, the Sponsor, The Morning Hustle, the Participating Stations (defined below) and each of their respective parents, subsidiaries, affiliated companies, promotional partners, and their advertising and promotional agencies. 1D. Participating Stations. This Promotion will run on the following participating Morning Hustle stations and affiliates: Chicago: WPWX-FM; Philadelphia: WPHI-FM; Dallas: KBFB-FM; Washington, DC: WKYS- FM; Houston: KBXX-FM, KMJQ-FM; Atlanta: WAMJ-FM, WHTA-FM; Detroit: WGPR-FM; Cleveland: WENZ-FM; Charlotte: WOSF-FM, WPZS-FM, WQNC-FM; St. -

U. S. Radio Stations As of June 30, 1922 the Following List of U. S. Radio

U. S. Radio Stations as of June 30, 1922 The following list of U. S. radio stations was taken from the official Department of Commerce publication of June, 1922. Stations generally operated on 360 meters (833 kHz) at this time. Thanks to Barry Mishkind for supplying the original document. Call City State Licensee KDKA East Pittsburgh PA Westinghouse Electric & Manufacturing Co. KDN San Francisco CA Leo J. Meyberg Co. KDPT San Diego CA Southern Electrical Co. KDYL Salt Lake City UT Telegram Publishing Co. KDYM San Diego CA Savoy Theater KDYN Redwood City CA Great Western Radio Corp. KDYO San Diego CA Carlson & Simpson KDYQ Portland OR Oregon Institute of Technology KDYR Pasadena CA Pasadena Star-News Publishing Co. KDYS Great Falls MT The Tribune KDYU Klamath Falls OR Herald Publishing Co. KDYV Salt Lake City UT Cope & Cornwell Co. KDYW Phoenix AZ Smith Hughes & Co. KDYX Honolulu HI Star Bulletin KDYY Denver CO Rocky Mountain Radio Corp. KDZA Tucson AZ Arizona Daily Star KDZB Bakersfield CA Frank E. Siefert KDZD Los Angeles CA W. R. Mitchell KDZE Seattle WA The Rhodes Co. KDZF Los Angeles CA Automobile Club of Southern California KDZG San Francisco CA Cyrus Peirce & Co. KDZH Fresno CA Fresno Evening Herald KDZI Wenatchee WA Electric Supply Co. KDZJ Eugene OR Excelsior Radio Co. KDZK Reno NV Nevada Machinery & Electric Co. KDZL Ogden UT Rocky Mountain Radio Corp. KDZM Centralia WA E. A. Hollingworth KDZP Los Angeles CA Newbery Electric Corp. KDZQ Denver CO Motor Generator Co. KDZR Bellingham WA Bellingham Publishing Co. KDZW San Francisco CA Claude W. -

Attachment a DA 19-526 Renewal of License Applications Accepted for Filing

Attachment A DA 19-526 Renewal of License Applications Accepted for Filing File Number Service Callsign Facility ID Frequency City State Licensee 0000072254 FL WMVK-LP 124828 107.3 MHz PERRYVILLE MD STATE OF MARYLAND, MDOT, MARYLAND TRANSIT ADMN. 0000072255 FL WTTZ-LP 193908 93.5 MHz BALTIMORE MD STATE OF MARYLAND, MDOT, MARYLAND TRANSIT ADMINISTRATION 0000072258 FX W253BH 53096 98.5 MHz BLACKSBURG VA POSITIVE ALTERNATIVE RADIO, INC. 0000072259 FX W247CQ 79178 97.3 MHz LYNCHBURG VA POSITIVE ALTERNATIVE RADIO, INC. 0000072260 FX W264CM 93126 100.7 MHz MARTINSVILLE VA POSITIVE ALTERNATIVE RADIO, INC. 0000072261 FX W279AC 70360 103.7 MHz ROANOKE VA POSITIVE ALTERNATIVE RADIO, INC. 0000072262 FX W243BT 86730 96.5 MHz WAYNESBORO VA POSITIVE ALTERNATIVE RADIO, INC. 0000072263 FX W241AL 142568 96.1 MHz MARION VA POSITIVE ALTERNATIVE RADIO, INC. 0000072265 FM WVRW 170948 107.7 MHz GLENVILLE WV DELLA JANE WOOFTER 0000072267 AM WESR 18385 1330 kHz ONLEY-ONANCOCK VA EASTERN SHORE RADIO, INC. 0000072268 FM WESR-FM 18386 103.3 MHz ONLEY-ONANCOCK VA EASTERN SHORE RADIO, INC. 0000072270 FX W289CE 157774 105.7 MHz ONLEY-ONANCOCK VA EASTERN SHORE RADIO, INC. 0000072271 FM WOTR 1103 96.3 MHz WESTON WV DELLA JANE WOOFTER 0000072274 AM WHAW 63489 980 kHz LOST CREEK WV DELLA JANE WOOFTER 0000072285 FX W206AY 91849 89.1 MHz FRUITLAND MD CALVARY CHAPEL OF TWIN FALLS, INC. 0000072287 FX W284BB 141155 104.7 MHz WISE VA POSITIVE ALTERNATIVE RADIO, INC. 0000072288 FX W295AI 142575 106.9 MHz MARION VA POSITIVE ALTERNATIVE RADIO, INC. 0000072293 FM WXAF 39869 90.9 MHz CHARLESTON WV SHOFAR BROADCASTING CORPORATION 0000072294 FX W204BH 92374 88.7 MHz BOONES MILL VA CALVARY CHAPEL OF TWIN FALLS, INC.