E-Commerce Mobile Banking Security: a Comparative Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ang Higante Sa Gubat

Isabela School of Arts and Trades, Ilagan Quirino Isabela College of Arts and Technology, Cauayan Cagayan Valley College of Quirino, Cabarroguis ISABELA COLLEGES, ▼ Cauayan Maddela Institute of Technology, Maddela ISABELA STATE UNIVERSITY, ▼ Angadanan Quirino Polytechnic College, Diffun ISABELA STATE UNIVERSITY, ▼Cabagan QUIRINO STATE COLLEGE ▼ Diffun, Quirino ISABELA STATE UNIVERSITY, Cauayan Polytechnic College, ▼Cauayan ISABELA STATE UNIVERSITY, ▼Echague Region III (Central Luzon ) ISABELA STATE UNIVERSITY, ▼Ilagan ISABELA STATE UNIVERSITY, ▼Jones ISABELA STATE UNIVERSITY, ▼Roxas Aurora ISABELA STATE UNIVERSITY, ▼San Mariano AURORA STATE COLLEGE OF TECHNOLOGY, ▼ Baler ISABELA STATE UNIVERSITY, ▼San Mateo Mount Carmel College, Baler Mallig Plains College, Mallig Mount Carmel College of Casiguran, Casiguran Metropolitan College of Science and Technology, Santiago Wesleyan University Philippines – Aurora Northeast Luzon Adventist School of Technology, Alicia Northeastern College, Santiago City Our Lady of the Pillar College of Cauayan, Inc., Cauayan Bataan Patria Sable Corpus College, Santiago City AMA Computer Learning Center, Balanga Philippine Normal University, Alicia Asian Pacific College of Advanced Studies, Inc., Balanga Southern Isabela College of Arts and Trade, Santiago City Bataan (Community) College, Bataan Central Colleges, Orani S ISABELA STATE UNIVERSITY ▼ Echague, Isabela Bataan Heroes Memorial College, Balanga City Saint Ferdinand College-Cabagan, Cabagan BATAAN POLYTECHNIC STATE COLLEGE, ▼Balanga City Saint Ferdinand -

The Successful Examinees Who Garnered the Ten (10) Highest Places in the November 2014 Nurse Licensure Examination Are the Following

The successful examinees who garnered the ten (10) highest places in the November 2014 Nurse Licensure Examination are the following: RANK NAME SCHOOL RATING (%) PAMANTASAN NG LUNGSOD NG 1 ELIJAH CATACUTAN LEGASPI 86.80 MAYNILA WESLEYAN UNIVERSITY- 2 GEASTYNE LAUREN GALANG NOLIDO 86.60 PHILIPPINES-CABANATUAN CITY ST. SCHOLASTICA'S COLLEGE- JANELLE JOY FERNANDEZ PONFERRADA 86.60 TACLOBAN MARIANO MARCOS STATE RALF JAY VILLANUEVA RETOTAL 86.60 UNIVERSITY-BATAC 3 JOBELLE KASPER BATANGAN AGMATA NORTHWESTERN UNIVERSITY 86.20 ELLAINE MARIE TIBURCIO LAURETA SAINT MARY'S UNIVERSITY 86.20 SAN LORENZO RUIZ COLLEGE OF CHERYL CUBI YMAS 86.20 ORMOC 4 NORHANA ABDULKARIM ALI ARELLANO UNIVERSITY-MANILA 86.00 JOSE RIZAL MEMORIAL STATE RONNIE VINCENT BOLASCO ANTIVO 86.00 UNIVERSITY-DAPITAN COLEGIO SAN AGUSTIN-BACOLOD CORLENE JOIE LINAUGO CORTEZ 86.00 CITY MICHELLE LAUREN NEPOMUCENO XAVIER UNIVERSITY 86.00 ESTRELLA UNIVERSITY OF EASTERN KELVIN KENN BRILLANTE MAGDARAOG 86.00 PHILIPPINES-CATARMAN UNIVERSITY OF THE PHILIPPINES- ANATOLE GAIL PARIAN VALLEJOS 86.00 MANILA 5 ROGER JOHN NECESITO ASTROLABIO SAN PEDRO COLLEGE-DAVAO CITY 85.80 ILIGAN MEDICAL CENTER COLLEGE, IVAN GARDE REDUBLADO 85.80 INC. UNIVERSIDAD DE MANILA (CITY JOSHUA CALEB SANCHEZ UGTO 85.80 COLL. OF MANILA) 6 JEWELL MARI ELAINE ADVINCULA DAVID ARELLANO UNIVERSITY-MANILA 85.60 MARY DOMINICA RAYMUNDO FUENTES SAINT JUDE COLLEGE-MANILA 85.60 JG MARIE PLANA NAVIGAR CENTRAL PHILIPPINE UNIVERSITY 85.60 ARGIE HUERVAS SILUBRICO SAINT PAUL UNIVERSITY-ILOILO 85.60 EMMANUEL LAMIS ZALDIVIA RIVERSIDE COLLEGE -

The Performance of Schools in the June 2018 Nurse Licensure Examination in Alphabetical Order As Per R.A

The performance of schools in the June 2018 Nurse Licensure Examination in alphabetical order as per R.A. 8981 otherwise known as PRC Modernization Act of 2000 Section 7(m) "To monitor the performance of schools in licensure examinations and publish the results thereof in a newspaper of national circulation" is as follows: JUNE 2018 NURSE LICENSURE EXAMINATION PERFORMANCE OF SCHOOLS IN ALPHABETICAL ORDER SEQ. FIRST TIMERS REPEATERS OVERALL PERFORMANCE NO. SCHOOL PASSED FAILED COND TOTAL % PASSED PASSED FAILED COND TOTAL % PASSED PASSED FAILED COND TOTAL % PASSED ABE INTERNATIONAL COLLEGE 1 OF BUSINESS & ECONOMICS- 0 0 0 0 0.00% 0 1 0 1 0.00% 0 1 0 1 0.00% BACOLOD ABELLANA COLLEGE OF ARTS & 2 TRADE 0 0 0 0 0.00% 0 1 0 1 0.00% 0 1 0 1 0.00% ABRA VALLEY COLLEGE 3 0 3 0 3 0.00% 4 13 0 17 23.53% 4 16 0 20 20.00% ABUBAKAR COMPUTER 4 LEARNING CENTER 1 1 0 2 50.00% 0 13 0 13 0.00% 1 14 0 15 6.67% ADAMSON UNIVERSITY 5 0 0 0 0 0.00% 1 2 0 3 33.33% 1 2 0 3 33.33% ADVENTIST MED. CENTER COLL.- 6 ILIGAN CITY,INC(MSHC, INC) 5 0 0 5 100.00% 4 6 0 10 40.00% 9 6 0 15 60.00% ADVENTIST UNIVERSITY OF THE 7 PHILIPPINES 33 3 0 36 91.67% 12 5 0 17 70.59% 45 8 0 53 84.91% AGO FOUNDATION COLLEGE 8 0 1 0 1 0.00% 2 8 0 10 20.00% 2 9 0 11 18.18% AGO MEDICAL & EDUCATIONAL 9 CENTER-BICOL CHRISTIAN 0 2 0 2 0.00% 6 14 0 20 30.00% 6 16 0 22 27.27% COLL.OF MED AKLAN CATHOLIC COLLEGE-(FOR 10 AKLAN COLLEGE)-KALIBO 0 0 0 0 0.00% 0 3 0 3 0.00% 0 3 0 3 0.00% AKLAN POLYTECHNIC INSTITUTE 11 0 0 0 0 0.00% 1 1 0 2 50.00% 1 1 0 2 50.00% AKLAN STATE UNIVERSITY(AKLAN 12 S.C.A.)-BANGA -

Performance of Schools in the January 2016 Pharmacist Licensure Examination in Alphabetical Order As Per R.A

The performance of schools in the January 2016 Pharmacist Licensure Examination in alphabetical order as per R.A. 8981 otherwise known as PRC Modernization Act of 2000 Section 7(m) "To monitor the performance of schools in licensure examinations and publish the results thereof in a newspaper of national circulation" is as follows: JANUARY 2016 PHARMACIST LICENSURE EXAMINATION PERFORMANCE OF SCHOOLS IN ALPHABETICAL ORDER SEQ. FIRST TIMERS REPEATERS OVERALL PERFORMANCE NO. SCHOOL PASSED FAILED TOTAL % PASSED PASSED FAILED TOTAL % PASSED PASSED FAILED TOTAL % PASSED ADAMSON UNIVERSITY 1 23 5 28 82.14% 1 3 4 25.00% 24 8 32 75.00% ANGELES UNIVERSITY 2 FOUNDATION 6 2 8 75.00% 9 7 16 56.25% 15 9 24 62.50% CEBU DOCTORS UNIVERSITY 3 19 1 20 95.00% 1 6 7 14.29% 20 7 27 74.07% CENTRAL ILOCANDIA COLLEGE 4 OF SCIENCE & TECHNOLOGY 0 1 1 0.00% 0 0 0 0.00% 0 1 1 0.00% CENTRAL LUZON DOCTOR'S 5 HOSPITAL EDUCATIONAL 7 20 27 25.93% 3 3 6 50.00% 10 23 33 30.30% INSTITUTION CENTRO ESCOLAR UNIVERSITY- 6 MAKATI 4 8 12 33.33% 8 12 20 40.00% 12 20 32 37.50% CENTRO ESCOLAR UNIVERSITY- 7 MALOLOS 4 10 14 28.57% 6 10 16 37.50% 10 20 30 33.33% CENTRO ESCOLAR UNIVERSITY- 8 MANILA 76 46 122 62.30% 32 40 72 44.44% 108 86 194 55.67% EMILIO AGUINALDO COLLEGE- 9 MANILA 3 0 3 100.00% 0 4 4 0.00% 3 4 7 42.86% GENERAL SANTOS DOCTORS' 10 MEDICAL SCHOOL FOUNDATION 22 12 34 64.71% 0 0 0 0.00% 22 12 34 64.71% LICEO DE CAGAYAN UNIVERSITY 11 23 15 38 60.53% 5 15 20 25.00% 28 30 58 48.28% LORMA COLLEGE 12 27 10 37 72.97% 2 0 2 100.00% 29 10 39 74.36% LYCEUM NORTHWESTERN UNIV- 13 DAGUPAN -

2015Suspension 2008Registere

LIST OF SEC REGISTERED CORPORATIONS FY 2008 WHICH FAILED TO SUBMIT FS AND GIS FOR PERIOD 2009 TO 2013 Date SEC Number Company Name Registered 1 CN200808877 "CASTLESPRING ELDERLY & SENIOR CITIZEN ASSOCIATION (CESCA)," INC. 06/11/2008 2 CS200719335 "GO" GENERICS SUPERDRUG INC. 01/30/2008 3 CS200802980 "JUST US" INDUSTRIAL & CONSTRUCTION SERVICES INC. 02/28/2008 4 CN200812088 "KABAGANG" NI DOC LOUIE CHUA INC. 08/05/2008 5 CN200803880 #1-PROBINSYANG MAUNLAD SANDIGAN NG BAYAN (#1-PRO-MASA NG 03/12/2008 6 CN200831927 (CEAG) CARCAR EMERGENCY ASSISTANCE GROUP RESCUE UNIT, INC. 12/10/2008 CN200830435 (D'EXTRA TOURS) DO EXCEL XENOS TEAM RIDERS ASSOCIATION AND TRACK 11/11/2008 7 OVER UNITED ROADS OR SEAS INC. 8 CN200804630 (MAZBDA) MARAGONDONZAPOTE BUS DRIVERS ASSN. INC. 03/28/2008 9 CN200813013 *CASTULE URBAN POOR ASSOCIATION INC. 08/28/2008 10 CS200830445 1 MORE ENTERTAINMENT INC. 11/12/2008 11 CN200811216 1 TULONG AT AGAPAY SA KABATAAN INC. 07/17/2008 12 CN200815933 1004 SHALOM METHODIST CHURCH, INC. 10/10/2008 13 CS200804199 1129 GOLDEN BRIDGE INTL INC. 03/19/2008 14 CS200809641 12-STAR REALTY DEVELOPMENT CORP. 06/24/2008 15 CS200828395 138 YE SEN FA INC. 07/07/2008 16 CN200801915 13TH CLUB OF ANTIPOLO INC. 02/11/2008 17 CS200818390 1415 GROUP, INC. 11/25/2008 18 CN200805092 15 LUCKY STARS OFW ASSOCIATION INC. 04/04/2008 19 CS200807505 153 METALS & MINING CORP. 05/19/2008 20 CS200828236 168 CREDIT CORPORATION 06/05/2008 21 CS200812630 168 MEGASAVE TRADING CORP. 08/14/2008 22 CS200819056 168 TAXI CORP. -

Download Download

Ryan Michael, F., Cyruz P, Homelo V., Jonaid, M., Dary, L., Don Vicente C., Mary Nellie T., Xerxes G., Jejomar D., Maria Teresa R., & Ronnell D. Dela Rosa. Uso de Internet y la alfabetización en eSalud con temor al COVID-19 entre estudiantes de enfermería en Filipinas Uso de Internet y la alfabetización en eSalud con temor al COVID-19 entre estudiantes de enfermería en Filipinas Internet use, eHealth literacy and fear of COVID-19 among nursing students in the Philippines Ryan Michael F. Cyruz P. Tuppal. Homelo V. Estoque. Jonaid M. Sadang. Daryl L. Superio. Oducado. St. Dominic College Far Eastern University Mindanao State Aquaculture Department, West Visayas State of Asia [email protected] University-Marawi Southeast Asian Fisheries University [email protected] [email protected] Development Center [email protected] [email protected] Don Vicente C. Mary Nellie T. Roa. Xerxes G. Malaga. Jejomar D. Quiros. Maria Teresa R. Fajardo. Real. St. Dominic College Negros Occidental Saint Jude College- University of Pangasinan- St. Dominic College of Asia Comprehensive Health PHINMA PHINMA of Asia [email protected] Program [email protected] [email protected] [email protected] [email protected] Ronnell D. Dela Rosa. Bataan Peninsula State University [email protected] RESUMEN. El brote de COVID-19 puso de relieve no solo la seguridad sino también el bienestar mental de los estudiantes de enfermería. En la actualidad, no se comprende bien el nivel de miedo al COVID-19 y los factores asociados entre los estudiantes de enfermería en Filipinas. Esta encuesta transversal en línea determinó la relación entre el uso de Internet y la alfabetización en eSalud con el miedo al COVID-19. -

AWS Educate Instituion List

Educate Institution City Country 3aaa Apprenticeships Derby United Kingdom 3W Academy Paris France A P Shah Institute of Technology Thane West India A.V.C. College of Engineering Mayiladuthurai India AARHUS TECH Aarhus N Denmark Aarupadai Veedu Institute of Technology Kanchipuram(Dt) India Abb Industrigymansium Västerås Sweden Abertay University Dundee United Kingdom ABES Engineering College Ghaziabad India Abilene Christian University Abilene United States ABMSP's Anantrao Pawar College of Engineering and Pune India Research Pune Abo Akademi University Turku Finland Academia de Bellas Artes Semillas Ltda Bogota Colombia Academia Desafio Latam Santiago Chile Academie Informatique Quebec-Canada Lévis Canada Academy College Bloomington United States Academy for Urban Scholars Columbus United States ACAMICA Palermo Argentina Accademia di Belle Arti di Cuneo Cuneo Italy Achariya College of Engineering Technology Puducherry India Acharya Institute of Technology Bangalore India Acharya Narendra Dev College New Delhi India Achievement House Cyber Charter School Exton United States Acropolis Institute of Technology & Research, Indore Indore India Educate Institution City Country Ada Developers Academy Seattle United States Ada. National College for Digital Skills London United Kingdom Additional Skill Acquisition Programme (ASAP) Thiruvananthapuram India Adhi college of Engineering and Technology KAncheepuram India Adhiyamaan College of Engineering Hosur India Adithya Institute of Technology coimbatore India Aditya Engineering College Kakinada -

Republic of the Philippines Professional Regulation Commission Lucena Regional Office

Republic of the Philippines Professional Regulation Commission Lucena Regional Office PLEASE CHECK: - If your name is included in the LIST. - If there are discrepancies in the spelling of your NAME and your DATE of BIRTH. - If your LEVEL (Elementary or Secondary) and your MAJOR / FIELD OF SPECIALIZATION to be taken is correct. - If the Name of the College / University you graduated from is correct. FOR CORRECTIONS: Please call ARNEL or CHESTER at (042) 373-7316 or email PRC LUCENA at [email protected] VERIFY YOUR APPLICATION NUMBER FROM THE ROOM WATCHERS / PROCTORS ASSIGNED IN YOU ROOM. FINAL LIST OF ROOM ASSIGNMENTS WILL BE POSTED STARTING MARCH 9, 2015 Seq. No Last Name First Name Middle Name Date of Birth School Graduated Level Major 1 AALA NANCY PORNEA 021681 TANAUAN INSTITUTE Elementary 2 ABADIER MARICAR MACATANGGA 110580 CENTRO ESCOLAR UNIVERSITY-MANILA Secondary TLE 3 ABADIER RHODALLIA CACALDA 102985 LAGUNA STATE POLYTECHNIC UNIVERSITY-STA. CRUZ Secondary TLE 4 ABADIER RUBY PUHAWAN 032371 UNION COLLEGE Elementary 5 ABAN NEZIEL PALOSA 040881 CAMARINES NORTE STATE COLLEGE-DAET Elementary 6 ABANADOR SHEIRYLAINE MORALES 071278 ABADA COLLEGE Secondary TLE 7 ABANES ANNA LIZA AVILA 091282 LA CONSOLACION COLLEGE-DAET Secondary TLE 8 ABANES MARIA MAGDALENA SANCHO 052777 CAMARINES NORTE STATE COLLEGE-DAET Secondary Physical Sciences 9 ABANILLA NIMROD RODIL 051692 POLYTECHNIC UNIVERSITY OF THE PHILIPPINES-UNISAN Elementary 10 ABANTO KAYE CHRISTINE ELEP 032991 CALAUAG CENTRAL COLLEGE Secondary TLE 11 ABANTO MENCHIE CASIANO 020778 MABINI -

PT FGBM May 3-4 2012 Minutes Draft 2

(DRAFT) DEPARTMENT OF HEALTH MEDICAL QUALITY ASSURANCE BOARD OF PHYSICAL THERAPY GENERAL BUSINESS MEETING GENERAL RULES REVIEW MAY 3-4, 2012 MINUTES Wyndham Jacksonville Riverwalk 1515 Prudential Dr. Jacksonville, FL 32207 (904) 396-5100 Participants in this public meeting should be aware that these proceedings are being recorded and that an audio file of the meeting will be posted to the Board’s website. May 3, 2012 – 6:30 p.m. The minutes reflect the actual sequence of events rather than the original agenda order. Call the Meeting to Order and Roll Call: Clint Lohr, Chair, called the general business meeting to order at approximately 6:30 p.m. Those present for all or part of the meeting, included the following: MEMBERS PRESENT BOARD COUNSEL Clint Lohr, Chair, PT, Cert. MDT Ed Tellechea, Board Counsel, Violeta Acuna-Parker, PT Assistant Attorney General Office Dr. Madeleine Hellman PT, MHM, Ed.D Jack Rust, PT STAFF PRESENT Allen Hall, Executive Board Director MEMBERS ABSENT Jessica Sapp, Program Administrator Dr. Gina Petraglia, PT PROSECUTING ATTORNEY Manshi Shah, Prosecuting Attorney, DOH Prosecution Services The board excused Dr. Petraglia from this meeting. Also in attendance was Dr. Shelia Nicholson, President of the Florida Physical Therapy Association. RULES REVIEW AND/OR DEVELOPMENT Tab 1 Rule Discussion • Rule 64B17-9.001(6)(f), Continuing Education The Board discussed Rule 64B17-9.001(6)(f) in regards to the possiblity of increasing the amount of continuing education hours awarded for licensees who take and pass the Florida laws and rules examination. Board of Physical Therapy Practice Minutes General Board Meeting and Rules Review May 3-4, 2012 Page 1 of 25 Mr. -

PHINMA Corporation 2017 Annual Report PHINMA GROUP's MISSION STATEMENT

MOVING FORWARDPHINMA Corporation 2017 Annual Report PHINMA GROUP'S MISSION STATEMENT The PHINMA Group’s Mission is to help build our Nation through competitive and well- managed business enterprises that enable FIlipinos to attain a better quality of life. With WHO WE ARE professional and effective management as our distinctive edge, we aim to give communities, PHINMA is a proudly Filipino conglomerate not only in the Philippines but wherever else that seeks to make lives better and build the we might find the need, improved access to the nation through successfully run and profitable essentials of a dignified life. businesses while remaining consistent with our core values of Integrity, Patriotism, Competence In the pursuit of our Mission, we look to our and Professionalism. tradition, our experience, our reputation, and above all, our people, as the principal factors that will enable us to achieve our lofty goals. The PHINMA Group will demonstrate that private business can mutually serve the needs of society and the aspirations of shareholders. TABLE OF CONTENTS Financial Highlights 1 Message to Shareholders 2 Business Review Education 6 Construction Materials 12 Energy 16 Housing 20 Hotels 24 Strategic Consulting 26 Corporate Social Responsibility 28 Board of Directors 32 Executive Committee 38 Corporate Governance Report 40 Financial Statements 45 Corporate Directory 128 Corporate Information IBC FINANCIAL HIGHLIGHTS 2017 2016 2015 (as restated) INCOME AND DIVIDENDS (In Thousand Pesos) Revenues 6,419,212 6,302,141 5,710,308 Net Income -

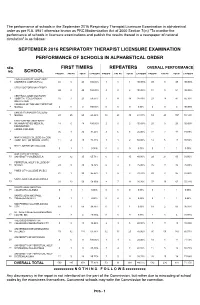

Repeaters First Timers School Performance Of

The performance of schools in the September 2016 Respiratory Therapist Licensure Examination in alphabetical order as per R.A. 8981 otherwise known as PRC Modernization Act of 2000 Section 7(m) "To monitor the performance of schools in licensure examinations and publish the results thereof in a newspaper of national circulation" is as follows: SEPTEMBER 2016 RESPIRATORY THERAPIST LICENSURE EXAMINATION PERFORMANCE OF SCHOOLS IN ALPHABETICAL ORDER SEQ. FIRST TIMERS REPEATERS OVERALL PERFORMANCE NO. SCHOOL PASSED FAILED TOTAL % PASSED PASSED FAILED TOTAL % PASSED PASSED FAILED TOTAL % PASSED CAGAYAN STATE UNIVERSITY- 1 ANDREWS CAMPUS(TUG) 48 0 48 100.00% 1 0 1 100.00% 49 0 49 100.00% CEBU DOCTORS UNIVERSITY 2 49 0 49 100.00% 2 0 2 100.00% 51 0 51 100.00% CENTRAL LUZON DOCTOR'S 3 HOSPITAL EDUCATIONAL 16 7 23 69.57% 7 11 18 38.89% 23 18 41 56.10% INSTITUTION COLLEGE OF THE HOLY SPIRIT OF 4 MANILA 2 0 2 100.00% 0 0 0 0.00% 2 0 2 100.00% EMILIO AGUINALDO COLLEGE- 5 MANILA 43 25 68 63.24% 16 23 39 41.03% 59 48 107 55.14% FAR EASTERN UNIVERSITY- 6 NICANOR REYES MEDICAL 18 0 18 100.00% 2 0 2 100.00% 20 0 20 100.00% FOUNDATION LORMA COLLEGE 7 35 1 36 97.22% 2 6 8 25.00% 37 7 44 84.09% MARY CHILES COLLEGE (for.GEN. 8 HOSP. SCH. OF NRSNG. & MID.) 11 4 15 73.33% 1 1 2 50.00% 12 5 17 70.59% MARY JOHNSTON COLLEGE 9 0 1 1 0.00% 0 0 0 0.00% 0 1 1 0.00% OUR LADY OF FATIMA 10 UNIVERSITY-VALENZUELA 23 12 35 65.71% 6 9 15 40.00% 29 21 50 58.00% PERPETUAL HELP COLLEGE OF 11 MANILA 29 9 38 76.32% 6 2 8 75.00% 35 11 46 76.09% PINES CITY COLLEGE (PCEC) 12 21 1 22 95.45% 1 2 3 33.33% 22 3 25 88.00% SAINT JUDE COLLEGE-MANILA 13 33 23 56 58.93% 4 7 11 36.36% 37 30 67 55.22% SAINTS JOHN AND PAUL 14 COLLEGES-CALAMBA 0 1 1 0.00% 0 0 0 0.00% 0 1 1 0.00% SAINTS JOHN AND PAUL 15 COLLEGES-MAKATI 0 1 1 0.00% 0 0 0 0.00% 0 1 1 0.00% SAN PEDRO COLLEGE-DAVAO 16 CITY 64 1 65 98.46% 0 1 1 0.00% 64 2 66 96.97% ST. -

List AWS Educate Institutions

Educate Institution City Country 1337 KHOURIBGA Morocco 1daoyun 无锡 China 3aaa Apprenticeships Derby United Kingdom 3W Academy Paris France 42 São Paulo sao paulo Brazil 42 seoul seoul Korea, Republic of 42 Tokyo Minato-ku Tokyo Japan 42Quebec QUEBEC Canada A P Shah Institute of Technology Thane West India A. D. Patel Institute of Technology Ahmedabad India A.V.C. College of Engineering Mayiladuthurai India Aalim Muhammed Salegh College of Engineering Avadi-IAF India Aaniiih Nakoda College Harlem United States AARHUS TECH Aarhus N Denmark Aarhus University Aarhus Denmark Aarupadai Veedu Institute of Technology Kanchipuram(Dt) India Abb Industrigymansium Västerås Sweden Abertay University Dundee United Kingdom ABES Engineering College Ghaziabad India Abilene Christian University Abilene United States Research Pune Pune India Abo Akademi University Turku Finland Academia de Bellas Artes Semillas Ltda Bogota Colombia Academia Desafio Latam Santiago Chile Academia Sinica Taipei Taiwan Academie Informatique Quebec-Canada Lévis Canada Academy College Bloomington United States Academy for Career Exploration PROVIDENCE United States Academy for Urban Scholars Columbus United States ACAMICA Palermo Argentina Accademia di Belle Arti di Cuneo Cuneo Italy Achariya College of Engineering Technology Puducherry India Acharya Institute of Technology Bangalore India Acharya Narendra Dev College New Delhi India Achievement House Cyber Charter School Exton United States Acropolis Institute of Technology & Research, Indore Indore India ACT AMERICAN COLLEGE