John Hancock Preferred Income Fund III

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Metlife, Inc. 200 Park Avenue, New York, NY 10166

MetLife, Inc. 200 Park Avenue, New York, NY 10166 April 26, 2018 Fellow Shareholders: I am writing to you for the first time in my role as MetLife’s Lead Director to share the Board’s perspective on MetLife’s performance in 2017 and how the Company is progressing with its ongoing transformation. As Directors, we are responsible for ensuring the Company’s business strategy is sound and management is executing it effectively. We plan for the Company’s future by evaluating management talent against anticipated needs and we play the unique role of acting as advocates for shareholders to ensure your interests are represented in all major decisions affecting MetLife. The feedback the Board received from shareholders during 2017 has proven invaluable as we continue to focus on creating value for shareholders. MetLife made important progress last year in several areas. The Brighthouse Financial separation opened a new chapter in MetLife’s history. As the Company focuses on less capital-intensive businesses with greater cash-generating potential, it has the opportunity to change how it is viewed and valued by investors. MetLife achieved a ratio of Core Free Cash Flow to Core Adjusted Earnings of 75 percent last year, hitting the top end of the Company’s projected range. This made it possible to return a record $4.6 billion to shareholders through share repurchases and dividends. In January, MetLife won its long-running legal battle to remove the Company’s Systemically Important Financial Institution (SIFI) designation when the federal government dropped its appeal of the court ruling in our favor. -

Brighthouse Financial, Inc. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q ☑ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended June 30, 2019 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ___ to ___ Commission File Number: 001-37905 Brighthouse Financial, Inc. (Exact name of registrant as specified in its charter) Delaware 81-3846992 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 11225 North Community House Road, Charlotte, North Carolina 28277 (Address of principal executive offices) (Zip Code) (980) 365-7100 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading symbol(s) Name of each exchange on which registered Common Stock, par value $0.01 per share BHF The Nasdaq Stock Market LLC Depositary Shares, each representing a 1/1,000th interest in a share BHFAP The Nasdaq Stock Market LLC of 6.600% Non-Cumulative Preferred Stock, Series A 6.250% Junior Subordinated Debentures due 2058 BHFAL The Nasdaq Stock Market LLC Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

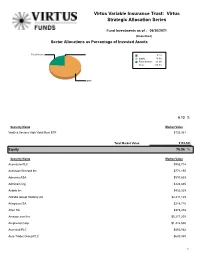

Virtus Variable Insurance Trust: Virtus Strategic Allocation Series

Virtus Variable Insurance Trust: Virtus Strategic Allocation Series Fund Investments as of : 06/30/2021 (Unaudited) Sector Allocations as Percentage of Invested Assets Fixed Income 0.1% Equity 76.0% Fixed Income 23.9% Total: 100.0% Equity 0.13 % Security Name Market Value VanEck Vectors High Yield Muni ETF $133,581 Total Market Value: $133,581 Equity 75.96 % Security Name Market Value Accenture PLC $983,714 Activision Blizzard Inc $771,155 Adevinta ASA $591,633 Admicom Oyj $123,695 Airbnb Inc $452,529 Alibaba Group Holding Ltd $2,411,125 Allegro.eu SA $218,716 Alten SA $378,478 Amazon.com Inc $5,277,205 Amphenol Corp $1,412,530 Ascential PLC $450,562 Auto Trader Group PLC $639,885 1 Autohome Inc $190,921 Avalara Inc $1,929,141 Bank of America Corp $1,237,477 Bill.com Holdings Inc $4,665,595 Boa Vista Servicos SA $227,428 Bouvet ASA $304,957 Brockhaus Capital Management AG $137,235 BTS Group AB $418,294 CAE Inc $506,141 Cerved Group SpA $153,342 CME Group Inc $550,841 Corp Moctezuma SAB de CV $192,124 CoStar Group Inc $1,162,793 CTS Eventim AG & Co KGaA $159,410 CTT Systems AB $266,966 Danaher Corp $1,307,182 DocuSign Inc $658,946 Duck Creek Technologies Inc $1,267,664 Ecolab Inc $700,710 Enento Group Oyj $373,228 Equifax Inc $624,882 Estee Lauder Cos Inc/The $743,671 Facebook Inc $3,836,284 Fair Isaac Corp $741,956 FDM Group Holdings PLC $207,920 Fineos Corp Ltd $70,397 Fintel Plc $473,852 Frontera Energy Corp $6,746 Gruppo MutuiOnline SpA $385,818 Haitian International Holdings Ltd $147,624 Haw Par Corp Ltd $416,695 HeadHunter Group -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

Wilmington Funds Holdings Template DRAFT

Wilmington Large-Cap Strategy Fund as of 5/31/2021 (Portfolio composition is subject to change) ISSUER NAME % OF ASSETS APPLE INC 4.97% MICROSOFT CORP 4.69% AMAZON.COM INC 3.45% FACEBOOK INC 1.99% ALPHABET INC 1.80% ALPHABET INC 1.77% BERKSHIRE HATHAWAY INC 1.48% JPMORGAN CHASE & CO 1.35% TESLA INC 1.20% JOHNSON & JOHNSON 1.12% UNITEDHEALTH GROUP INC 0.98% VISA INC 0.96% NVIDIA CORP 0.96% BANK OF AMERICA CORP 0.89% HOME DEPOT INC/THE 0.87% WALT DISNEY CO/THE 0.82% MASTERCARD INC 0.80% PAYPAL HOLDINGS INC 0.77% EXXON MOBIL CORP 0.68% PROCTER & GAMBLE CO/THE 0.67% COMCAST CORP 0.66% ADOBE INC 0.62% INTEL CORP 0.59% VERIZON COMMUNICATIONS INC 0.59% CISCO SYSTEMS INC 0.57% CHEVRON CORP 0.55% PFIZER INC 0.54% NETFLIX INC 0.54% AT&T INC 0.53% SALESFORCE.COM INC 0.53% ABBOTT LABORATORIES 0.51% ABBVIE INC 0.50% MERCK & CO INC 0.48% WELLS FARGO & CO 0.48% BROADCOM INC 0.47% THERMO FISHER SCIENTIFIC INC 0.47% ACCENTURE PLC 0.46% CITIGROUP INC 0.45% MCDONALD'S CORP 0.44% TEXAS INSTRUMENTS INC 0.44% COCA-COLA CO/THE 0.44% HONEYWELL INTERNATIONAL INC 0.44% LINDE PLC 0.43% MEDTRONIC PLC 0.43% NIKE INC 0.43% ELI LILLY & CO 0.42% PEPSICO INC 0.42% UNITED PARCEL SERVICE INC 0.41% WALMART INC 0.40% DANAHER CORP 0.40% UNION PACIFIC CORP 0.40% QUALCOMM INC 0.38% BRISTOL-MYERS SQUIBB CO 0.37% ORACLE CORP 0.37% LOWE'S COS INC 0.36% BLACKROCK INC 0.35% CATERPILLAR INC 0.35% AMGEN INC 0.35% BOEING CO/THE 0.35% MORGAN STANLEY 0.35% COSTCO WHOLESALE CORP 0.35% RAYTHEON TECHNOLOGIES CORP 0.34% STARBUCKS CORP 0.34% GOLDMAN SACHS GROUP INC/THE 0.34% GENERAL ELECTRIC -

Financial Services Fund

SCHEDULE OF INVESTMENTS (Unaudited) June 30, 2020 FINANCIAL SERVICES FUND SHARES VALUE SHARES VALUE COMMON STOCKS† - 99.9% Taubman Centers, Inc. 450 $ 16,992 Park Hotels & Resorts, Inc. 1,650 16,318 REITs - 30.1% Macerich Co.1 1,374 12,325 American Tower Corp. — Class A 474 $ 122,548 Crown Castle International Corp. 566 94,720 Total REITs 2,230,982 Prologis, Inc. 998 93,143 BANKS - 25.4% Equinix, Inc. 126 88,490 JPMorgan Chase & Co. 1,968 185,110 Digital Realty Trust, Inc. 496 70,487 Bank of America Corp. 6,585 156,394 SBA Communications Corp. 225 67,032 Citigroup, Inc. 2,218 113,340 Public Storage 339 65,051 Wells Fargo & Co. 4,313 110,413 AvalonBay Communities, Inc. 334 51,650 Morgan Stanley 2,038 98,435 Equity Residential 875 51,468 Goldman Sachs Group, Inc. 477 94,265 Simon Property Group, Inc. 743 50,806 U.S. Bancorp 2,210 81,372 Welltower, Inc. 975 50,456 Truist Financial Corp. 2,040 76,602 Alexandria Real Estate Equities, Inc. 307 49,811 PNC Financial Services Group, Inc. 695 73,121 Realty Income Corp. 823 48,968 Bank of New York Mellon Corp. 1,695 65,512 Weyerhaeuser Co. 2,045 45,931 State Street Corp. 833 52,937 Invitation Homes, Inc. 1,574 43,332 First Republic Bank 440 46,636 Essex Property Trust, Inc. 187 42,855 Northern Trust Corp. 564 44,748 Healthpeak Properties, Inc. 1,547 42,635 HDFC Bank Ltd. ADR 931 42,323 Boston Properties, Inc. 464 41,936 M&T Bank Corp. -

Quarterly Statement

QUARTERLY STATEMENT OF THE NEW ENGLAND LIFE INSURANCE COMPANY OF THE STATE OF MASSACHUSETTS TO THE INSURANCE DEPARTMENT OF THE STATE OF FOR THE QUARTER ENDED SEPTEMBER 30, 2020 LIFE AND ACCIDENT AND HEALTH 2020 91626202020100103 LIFE AND ACCIDENT AND HEALTH COMPANIES – ASSOCIATION EDITION QUARTERLY STATEMENT AS OF SEPTEMBER 30, 2020 OF THE CONDITION AND AFFAIRS OF THE NEW ENGLAND LIFE INSURANCE COMPANY NAIC Group Code 4932 4932 NAIC Company Code 91626 Employer’s ID Number 04-2708937 (Current) (Prior) Organized under the Laws of Massachusetts State of Domicile or Port of Entry Massachusetts Country of Domicile United States of America Incorporated/Organized 09/12/1980 Commenced Business 12/30/1980 Statutory Home Office One Financial Center Boston, MA 02111 (Street and Number) (City or Town, State and Zip Code) Main Administrative Office One Financial Center (Street and Number) Boston, MA 02111 617-578-2000 (City or Town, State and Zip Code) (Area Code) (Telephone Number) Mail Address 12802 Tampa Oaks Boulevard, Suite 447 Temple Terrace, FL 33637 (Street and Number or P.O. Box) (City or Town, State and Zip Code) Primary Location of Books and Records 12802 Tampa Oaks Boulevard, Suite 447 (Street and Number) Temple Terrace, FL 33637 980-949-4100 (City or Town, State and Zip Code) (Area Code) (Telephone Number) Internet Web Site Address www.brighthousefinancial.com Statutory Statement Contact Timothy Lashoan Shaw 980-949-4100 (Name) (Area Code) (Telephone Number) [email protected] 813-615-9468 (Email Address) (Fax Number) OFFICERS -

Full Portfolio Holdings* As of August 31, 2021 % of Security Coupon Maturity Shares/Par Market Value Net Assets Fixed Income Clearing Corp

Hartford Short Duration Fund Full Portfolio Holdings* as of August 31, 2021 % of Security Coupon Maturity Shares/Par Market Value Net Assets Fixed Income Clearing Corp. Repurchase 0.020 9/1/2021 17,536,939 17,536,939 0.830 Agreement dated 01/29/2021 at 0.020%, due on 02/01/2021 with a maturity value of $20,065,950; collateralized by U.S. Treasury Bond at 3.000%, maturing 05/15/2047, with a market value of $20,467,316 U.S. Treasury Notes 1.375 2/15/2023 9,950,000 10,129,566 0.479 U.S. Treasury Notes 0.125 5/15/2023 10,000,000 9,993,359 0.473 U.S. Treasury Notes 0.250 6/15/2024 10,000,000 9,969,531 0.472 SG Commercial Mortgage Securities Trust 2.632 3/15/2037 9,500,000 9,887,768 0.468 Global Payments, Inc. 1.200 3/1/2026 9,000,000 8,944,295 0.423 Morgan Stanley 0.864 10/21/2025 8,615,000 8,613,689 0.408 Telecom Italia S.p.A. 5.303 5/30/2024 7,450,000 8,088,465 0.383 Wells Fargo & Co. 2.164 2/11/2026 7,500,000 7,785,864 0.368 Gray Oak Pipeline LLC 2.000 9/15/2023 7,500,000 7,644,142 0.362 SG Residential Mortgage Trust 1.160 7/25/2061 7,627,916 7,623,759 0.361 Angel Oak Mortgage Trust 1.019 7/25/2066 7,590,000 7,589,895 0.359 HSBC Holdings plc 1.589 5/24/2027 7,455,000 7,480,885 0.354 Steel Dynamics, Inc. -

2020 Metlife Proxy

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 SCHEDULE 14A PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE SECURITIES EXCHANGE ACT OF 1934 Filed by the Registrant Filed by a Party other than the Registrant Check the appropriate box: Preliminary Proxy Statement Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) Definitive Proxy Statement Definitive Additional Materials Soliciting Material under § 240.14a-12 METLIFE, INC. (Name of Registrant as Specified in Its Charter) Payment of Filing Fee (Check the appropriate box): No fee required Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11 (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transactions applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: Fee paid previously with preliminary materials. Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: MetLife, Inc. 200 Park Avenue, New York, NY 10166 April 28, 2020 Fellow Shareholders: I write this letter while working from home, as the country and the world struggle to turn back a global pandemic whose social and economic effects, in the United States and the other countries where MetLife operates, are still largely ahead of us. -

Investment Stewardship 2019 Annual Report Investment Stewardship 2019 Annual Report

Investment Stewardship 2019 Annual Report Investment Stewardship 2019 Annual Report An introduction from our chairman and CEO 1 A letter to our fund shareholders 3 Our four principles 4 Our structure and approach 5 Investment Stewardship at a glance 6 Regional roundup 10 Sustainability is synonymous with long-termism 12 Engagement case studies Board composition 14 Vanguard’s perspective on board diversity 18 Oversight of strategy and risk 20 A growing focus on climate risk 22 Why disclosure frameworks are important 23 Executive compensation 24 Governance structures 26 Proxy voting history 28 Company engagements 36 b An introduction from our chairman and CEO Tim Buckley Vanguard Chairman and Chief Executive Officer When you invest with Vanguard, you can count on us to treat your investment with the care and responsibility it deserves. You’ve entrusted us with your financial future, and we work hard to protect the long-term value of your investments. Not all companies define “long-term” the same way. To be clear, at Vanguard, we know investors are saving for a future that is measured in years and decades. Our investment philosophy reflects the needs of these investors and has been at the core of Vanguard’s identity since we began more than 40 years ago. The index funds we manage on your behalf are practically permanent—structurally long-term—owners of the companies in which they invest. Even our active fund managers are behaviorally long-term. Given this extended time horizon, it’s critical that the companies our funds invest in share this long-term mindset. -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners Small Cap Value Fund, March 31, 2021 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 96.7% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Communication Services 1.0% Automobiles 1.4% Diversified Telecommunication Services 0.3% Harley-Davidson, Inc. 162,974 6,535,257 (a) Vonage Holdings Corp. 234,766 2,774,934 Thor Industries, Inc. 37,439 5,044,531 Entertainment 0.0% Total 11,579,788 (a) Madison Square Garden Sports Corp., Class A 497 89,192 Diversified Consumer Services 0.0% Interactive Media & Services 0.1% Universal Technical Institute, Inc.(a) 17,528 102,363 (a) TrueCar, Inc. 52,852 252,897 Hotels, Restaurants & Leisure 3.4% (a) Yelp, Inc. 23,277 907,803 Del Taco Restaurants, Inc. 82,093 786,451 Total 1,160,700 Dine Brands Global, Inc.(a) 58,265 5,245,598 Media 0.5% Everi Holdings, Inc.(a) 33,130 467,464 comScore, Inc.(a) 34,027 124,539 International Game Technology PLC(a) 59,831 960,287 Cumulus Media, Inc., Class A(a) 4,137 37,688 Jack in the Box, Inc. 25,887 2,841,875 Entravision Communications Corp., Class A 7,595 30,684 Marriott Vacations Worldwide Corp.(a) 32,291 5,624,446 Gray Television, Inc. 33,631 618,810 Papa John’s International, Inc. 12,345 1,094,261 iHeartMedia, Inc., Class A(a) 35,169 638,317 PlayAGS, Inc.(a) 19,414 156,865 Marchex, Inc.(a) 6,280 17,647 Six Flags Entertainment Corp.(a) 241,229 11,209,912 TEGNA, Inc. -

PORTFOLIO of INVESTMENTS – As of April 30, 2021 (Unaudited)

PORTFOLIO OF INVESTMENTS – as of April 30, 2021 (Unaudited) Natixis Sustainable Future 2015 Fund ________________________________Shares Description ____________________________________________________________ Value (†) Common Stocks – 29.1% of Net Assets Aerospace & Defense – 0.5% 7 Axon Enterprise, Inc.(a) $ 1,061 53 Boeing Co. (The)(a) 12,418 21 General Dynamics Corp. 3,995 2 L3Harris Technologies, Inc. 418 11 Moog, Inc., Class A 952 27 Raytheon Technologies Corp. ______________2,248 ______________21,092 Air Freight & Logistics – 0.3% 90 Expeditors International of Washington, Inc. 9,887 14 United Parcel Service, Inc., Class B ______________2,854 ______________12,741 Airlines – 0.1% 5 Alaska Air Group, Inc.(a) 346 29 Delta Air Lines, Inc.(a) 1,360 122 JetBlue Airways Corp.(a) ______________2,484 ______________4,190 Auto Components – 0.1% 3 Aptiv PLC(a) 432 6 BorgWarner, Inc. 291 82 Dana, Inc. 2,075 10 Visteon Corp.(a) ______________1,218 ______________4,016 Automobiles – 0.2% 133 General Motors Co.(a) 7,610 11 Thor Industries, Inc. ______________1,558 ______________9,168 Banks – 1.6% 31 Ameris Bancorp 1,677 57 BancorpSouth Bank 1,687 271 Bank of America Corp. 10,984 134 Citigroup, Inc. 9,546 49 Citizens Financial Group, Inc. 2,268 3 Comerica, Inc. 225 27 Cullen/Frost Bankers, Inc. 3,242 20 Fifth Third Bancorp 811 100 Fulton Financial Corp. 1,705 32 Huntington Bancshares, Inc. 490 50 International Bancshares Corp. 2,369 70 KeyCorp 1,523 12 M&T Bank Corp. 1,892 78 People's United Financial, Inc. 1,414 27 PNC Financial Services Group, Inc. (The) 5,048 82 Regions Financial Corp.