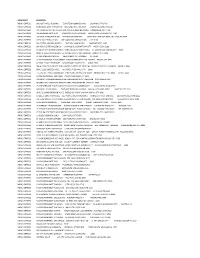

P7B Fixed-Rate Bonds Due 2027 Preliminary Prospectus

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Company Name: Ayala Land Malls Inc. Corporate Address: 5Th Floor, Glorietta 4, Ayala Center Makati City

Company Name: Ayala Land Malls Inc. Corporate Address: 5th Floor, Glorietta 4, Ayala Center Makati City Mall List Luzon Mall Name Mall Location Harbor Point Subic Bay Freeport Zone, Zambales MarQuee Mall Angeles City, Pamapanga Ayala Malls Cloverleaf A Bonifacio Ave Brgy Balingasa, Quezon City TriNoma Edsa Corner North Avenue, Quezon City Ayala Malls Vertis North North Avenue Brgy Bagong Pag-asa, Quezon City Fairview Terraces Quirino Highway cor Maligaya Drive Novaliches, Quezon City U.P. Town Center Katipunan Avenue Diliman, Quezon City Ayala Malls Feliz Amang Rodriguez Cor J.P. Rizal Brgy Dela Paz, Pasig City Ayala Malls Marikina Liwasag Kalayaan Brgy Marikina Heights, Marikina City Ayala Malls The 30th Meralco Ave. Brgy Ugong, Pasig City Market! Market! Bonifacio Global City, Taguig One Ayala Ave Ayala Avenue, Makati City Glorietta Ayala Center, Makati City Greenbelt Legazpi Street, Makati City Ayala Malls Circuit Circuit Makati, Hippodromo, Carmona, Makati City Ayala Malls Manila Bay Macapagal Blvd cor. Aseana Avenue, Paranaque City Alabang Town Center Alabang Town Center, Muntinlupa City The District Dasma Molina Road, Dasmarinas, Cavite The District Imus Aguinaldo Highway cor. Daang Hari Road Anabu II-D, Imus, Cavite Vermosa Daang Hari Road cor. Vermosa Blvd., Imus, Cavite Ayala Malls Solenad Nuvali, Brgy. Sto. Domingo, City of Santa Rosa, Laguna Ayala Malls Serin Gen. Emilio Aguinaldo Highway Tagaytay City, Cavite Ayala Malls Legazpi Rizal Street corner Quezon Ave., Barangay Capantawan, Legazpi City, Albay Mall List VisMin Mall Name Mall Location Abreeza J.P. Laurel Ave., Davao City Ayala Center Cebu Cebu Business Park, Cebu City Central Bloc I. Villa Street Cebu IT Park, Cebu City Centrio Mall CM Recto-Corrales Ave, Cagayan de Oro Ayala Malls Capitol Central Gatuslao Street, Bacolod City . -

MEMO EXPRESS.Pdf

MERCHANT BRANCHES MEMO EXPRESS SM SOUTHMALL ALABANG ZAPOTE RD ALMANZA UNO LAS PINAS CITY 1740 MEMO EXPRESS CYBERZONE SM CITY FAIRVIEW REGALADO AVE. GREATER LAGRO QUEZON CITY 1100 MEMO EXPRESS UNIT CZ24 SM CITY BF D.A.S.A COR PRES AVE BRGY BF HOMES PARANAQUE CITY 1700 MEMO EXPRESS 345 ALABANG ZAPOTE RD ROBINSON PLACE LAS PINAS BRGY TALON LAS PINAS CITY 1740 MEMO EXPRESS UNIT 303 2F ARCADIA BLDG SANTA ROSA TAGAYTAY ROAD DON JOSE STA. ROSA CITY LAGUNA 4026 MEMO EXPRESS CZ234 SM CITY BACOLOD RECLAMATION ARE BACOLOD CITY 6100 MEMO EXPRESS SM CENTER ANGONO MANILA EAST ROAD SAN ISIDRO ANGONO RIZAL 1930 MEMO EXPRESS SM MEGA CENTER MELENCIO SAN ROQUE CABANATUAN CITY NUEVA ECIJA 3100 MEMO EXPRESS CY 20 SM CITY GENSAN CORNER SANTIAGO BLVD SAN MIGUEL ST. LAGAO GEN SANTOS CITY 9500 MEMO EXPRESS SPACE 3-052 3F NEW GLORIETTA 2 AYALA CENTER SAN LORENZO MAKATI CITY 1224 MEMO EXPRESS L3-341 ROBINSONS NORTH ABUCAY BRGY 91 TACLOBAN CITY 6500 MEMO EXPRESS L2 2019 ROBINSON PLACE ORMOC CHRYSANTHEMUM SUBD. COGON ORMOC CITY 6541 MEMO EXPRESS CZ 3008 17 SM CITY LEGAZPI TAHAO ROAD LEGAZPI CITY ALBAY 4500 MEMO EXPRESS RM 814 PACIFIC LAND CTR BLDG QUITIN PAREDES ST. BRGY 289 ZONE 027 DIST 111 BINONDO MANILA 1006 MEMO EXPRESS SPACE 3111 ABREEZA MALL JP LAUREL AVE DAVAO CITY 8000 MEMO EXPRESS THE DISTRICT MALL AGUINALDO HIWAY COR. DAANG HARI ROAD ANABU II D CITY OF IMUS CAVITE 4103 MEMO EXPRESS L3 ROBINSON PLACE SANTIAGO MABINI SANTIAGO CITY 3311 MEMO EXPRESS 239 SM CITY CAUAYAN MAHARLIKA HIGHWAY DISTRICT 2 CAUAYAN CITY ISABELA 3305 MEMO EXPRESS CENTRIO MALL CM RECTO AVENUE BRGY 24 CAGAYAN DE ORO CITY 9000 MEMO EXPRESS L3-338 ROBINSON PLACE MALOLOS SUMAPANG MATANDA CITY MALOLOS BULACAN 3300 MEMO EXPRESS 3RD LEVEL SPACE 3029A FAIRVIEW TERRACES QUIRINO HIGHWAY PASONG PUTIK QUEZON CITY 1012 MEMO EXPRESS SPACE 2 02448 ROBINSON PLACE PUEBLO DE PANAY LAWAAN ROXAS CITY 5800 MEMO EXPRESS CZ 015 25 SM CITY SAN JOSE DEL MONTE BRGY TUNGKONG MANGGA CITY OF SAN JOSE DEL MONTE BULACAN 3023 MEMO EXPRESS UNIT 326 3RD FLR AYALA MALLS LEGAZPI RIZAL ST. -

METRO MANILA Alabang Town Center Glorietta 2 SM

METRO MANILA Alabang Town Center Glorietta 2 SM Fairview SM Sucat Ayala Fairview Terraces Greenhills Shopping Center SM Las Piñas SM Taytay Ayala Malls – Circuit Market Market SM Mall Of Asia SM Tunasan Ayala Malls – Cloverleaf Power Plant Mall SM Manila SM Valenzuela Ayala Malls – Feliz Robinsons Antipolo SM Marikina SMDC Light Mall Ayala Malls – Manila Bay Robinsons Magnolia SM Masinag Sta. Lucia Mall Ayala Malls – Marikina Robinsons Manila SM Megamall Starmall Alabang Ayala Malls – The 30th Shangri-La Plaza Mall SM North Edsa The Podium Ayala Malls – Vertis North SM Angono SM Novaliches Trinoma Mall Festival Mall SM Aura Premier SM San Lazaro UP Town Center Fisher Mall – Malabon SM BF Parañaque SM San Mateo Uptown Mall Fisher Mall – Quezon City SM Bicutan SM Southmall Venice Grand Canal Mall Gateway Mall SM Cubao SM Sta. Mesa Vista Mall – Taguig PROVINCIAL Abreeza Mall Megaworld Mandurriao SM Bacolod SM Naga Ayala Center Cebu Nepo Mall Dagupan SM Bacoor SM Olongapo Ayala Malls – Capitol Pacific Mall Legazpi SM Baguio SM Pampanga Ayala Malls – Legazpi Parkmall Mandaue SM Baliwag SM Puerto Princesa Balagtas Town Center Puregold Laoag SM Batangas SM Rosales BQ Mall Tagbilaran Robinsons Antique SM Cabanatuan SM Rosario Centrio Mall – CDO Robinsons Bacolod SM Calamba SM San Jose Bulacan CSI Citymall – Dagupan Robinsons Butuan SM Cauayan SM San Pablo CSI Citymall – Iba Robinsons Calasiao SM CDO SM Sangandaan CSI Citymall – San Fernando Robinsons Dumaguete SM Cebu SM Seaside Gaisano – Digos Robinsons Galleria Cebu SM Clark SM Tarlac Gaisano -

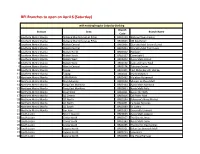

BPI Branches to Open on April 6 (Saturday)

BPI Branches to open on April 6 (Saturday) with existing/regular Saturday Banking Branch Division Area Branch Name Code 1 Southern Metro Manila Alabang Muntinlupa Las Piñas BR00159 Alabang Town Center 2 Southern Metro Manila Alabang Muntinlupa Las Piñas BR00833 SM Southmall 3 Southern Metro Manila Makati Central BR00006 Glorietta Mall Ground Level 4 Southern Metro Manila Makati Central BR00453 Glorietta Mall Third Level 5 Southern Metro Manila Makati North BR00352 Rockwell 6 Southern Metro Manila Makati South BR00157 Greenbelt 5 7 Southern Metro Manila Makati West BR00303 Ayala Malls Circuit 8 Southern Metro Manila Makati West BR00430 Cash and Carry Mall 9 Southern Metro Manila Manila Central BR00174 Tutuban Center 10 Southern Metro Manila Taguig BR01004 Fort Mckinley Hill- Venice 11 Southern Metro Manila Taguig BR00161 Market Market 12 Northern Metro Manila CAMANAVA BR00462 Malabon Fishermall 13 Northern Metro Manila Mandaluyong BR00250 Shangri-La Plaza Mall 14 Northern Metro Manila Pasig East Marikina BR00164 Ayala Malls Marikina 15 Northern Metro Manila Pasig East Marikina BR00804 Ayala Malls Feliz 16 Northern Metro Manila Pasig West BR00411 Ayala The 30th 17 Northern Metro Manila QC Central BR00446 QA Fisher Mall 18 Northern Metro Manila QC North BR00194 Robinson's Nova Market 19 Northern Metro Manila QC North BR00451 Fairview Terraces 20 Northern Metro Manila QC South BR00389 St. Luke's 21 Northern Metro Manila San Juan BR00193 Greenhills Unimart 22 South Luzon Bicol / Quezon BR00066 Ayala Malls Legazpi 23 South Luzon Cavite North BR00357 The District Imus 24 South Luzon Cavite South BR00180 Ayala Malls Serin 25 South Luzon Cavite South BR00285 The District Dasmarinas 26 South Luzon Laguna North BR00221 Biñan Southwoods Mall 27 South Luzon Laguna North BR00233 Solenad 3 28 South Luzon Laguna North BR00898 Sta. -

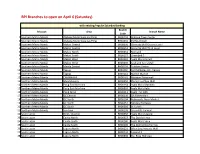

BPI Branches to Open on April 6 (Saturday)

BPI Branches to open on April 6 (Saturday) with existing/regular Saturday Banking Branch Division Area Branch Name Code 1 Southern Metro Manila Alabang Muntinlupa Las Piñas BR00159 Alabang Town Center 2 Southern Metro Manila Alabang Muntinlupa Las Piñas BR00833 SM Southmall 3 Southern Metro Manila Makati Central BR00006 Glorietta Mall Ground Level 4 Southern Metro Manila Makati Central BR00453 Glorietta Mall Third Level 5 Southern Metro Manila Makati North BR00352 Rockwell 6 Southern Metro Manila Makati South BR00157 Greenbelt 5 7 Southern Metro Manila Makati West BR00303 Ayala Malls Circuit 8 Southern Metro Manila Makati West BR00430 Cash and Carry Mall 9 Southern Metro Manila Manila Central BR00174 Tutuban Center 10 Southern Metro Manila Taguig BR01004 Fort Mckinley Hill- Venice 11 Southern Metro Manila Taguig BR00161 Market Market 12 Northern Metro Manila CAMANAVA BR00462 Malabon Fishermall 13 Northern Metro Manila Mandaluyong BR00250 Shangri-La Plaza Mall 14 Northern Metro Manila Pasig East Marikina BR00164 Ayala Malls Marikina 15 Northern Metro Manila Pasig East Marikina BR00804 Ayala Malls Feliz 16 Northern Metro Manila Pasig West BR00411 Ayala The 30th 17 Northern Metro Manila QC Central BR00446 QA Fisher Mall 18 Northern Metro Manila QC North BR00194 Robinson's Nova Market 19 Northern Metro Manila QC North BR00451 Fairview Terraces 20 Northern Metro Manila QC South BR00389 St. Luke's 21 Northern Metro Manila San Juan BR00193 Greenhills Unimart 22 South Luzon Bicol / Quezon BR00066 Ayala Malls Legazpi 23 South Luzon Cavite North BR00357 The District Imus 24 South Luzon Cavite South BR00180 Ayala Malls Serin 25 South Luzon Cavite South BR00285 The District Dasmarinas 26 South Luzon Laguna North BR00221 Biñan Southwoods Mall 27 South Luzon Laguna North BR00233 Solenad 3 28 South Luzon Laguna North BR00898 Sta. -

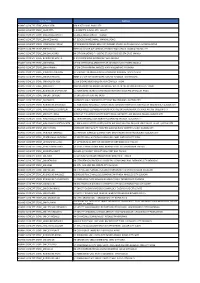

BPI Branches with Extended Banking Hours Starting December 9, 2019 up to January 3, 2020

BPI Branches with Extended Banking Hours starting December 9, 2019 up to January 3, 2020 Regular Extended (Dec 9, 2019 up to January 3, 2020) Division Area BR Name BR Code Address Banking Hours Office Hours Banking Hours Office Hours 1 Southern Metro Manila Alabang / Muntinlupa / Las Pinas Alabang South BR00346 Ground Floor South Supermarket, Filinvest, Brgy. Alabang Muntinlupa City 09:00 AM to 04:30 PM 08:30 AM to 05:30 PM 09:00 AM to 05:30 PM 08:30 AM to 06:30 PM 2 Southern Metro Manila Alabang / Muntinlupa / Las Pinas Alabang Town Center BR00159 2/F Madrigal Entrance Alabang Town Center, Brgy. Ayala Alabang Muntinlupa City 1770 10:00 AM to 05:30 PM 09:30 AM to 06:30 PM 10:00 AM to 06:30 PM 09:30 AM to 07:30 PM 3 Southern Metro Manila Alabang / Muntinlupa / Las Pinas Las Pinas BR00830 Real ST. Corner Gemini ST., Pamplona,Alabang Zapote Road, Las Pinas City 09:00 AM to 04:30 PM 08:30 AM to 05:30 PM 09:00 AM to 05:30 PM 08:30 AM to 06:30 PM 4 Southern Metro Manila Alabang / Muntinlupa / Las Pinas Muntinlupa South Park BR01003 South Park National Road Brgy. Alabang, Muntinlupa City 10:00 AM to 05:30 PM 09:30 AM to 06:30 PM 10:00 AM to 06:30 PM 09:30 AM to 07:30 PM 5 Southern Metro Manila Alabang / Muntinlupa / Las Pinas New Alabang BR00033 GF Alabang Zapote Rd. Mall Entrance ,Alabang Town Center, Alabang , Muntinlupa City 09:00 AM to 04:30 PM 08:30 AM to 05:30 PM 09:00 AM to 05:30 PM 08:30 AM to 06:30 PM Upper Ground Floor, SM Southmall, Alabang Zapote Road, Brgy Almanza Uno, Las Pinas 6 Southern Metro Manila Alabang / Muntinlupa / Las Pinas SM Southmall BR00833 10:00 AM to 05:30 PM 09:30 AM to 06:30 PM 10:00 AM to 06:30 PM 09:30 AM to 07:30 PM City 1740 7 Southern Metro Manila Makati Central Glorietta Mall Ground Level BR00006 G/F Unit 1086 Glorietta Mall, Ayala Center, Brgy. -

METRO MANILA Alabang Town Center Glorietta 2 SM Fairview SM

METRO MANILA Alabang Town Center Glorietta 2 SM Fairview SM Sucat Ayala Fairview Terraces Greenhills Shopping Center SM Las Piñas SM Taytay Ayala Malls – Circuit Market Market SM Mall Of Asia SM Tunasan Ayala Malls – Cloverleaf Power Plant Mall SM Manila SM Valenzuela Ayala Malls – Feliz Robinsons Antipolo SM Marikina SMDC Light Mall Ayala Malls – Manila Bay Robinsons Magnolia SM Masinag Sta. Lucia Mall Ayala Malls – Marikina Robinsons Manila SM Megamall Starmall Alabang Ayala Malls – The 30th Shangri-La Plaza Mall SM North Edsa The Podium Ayala Malls – Vertis North SM Angono SM Novaliches Trinoma Mall Festival Mall SM Aura Premier SM San Lazaro UP Town Center Fisher Mall – Malabon SM BF Parañaque SM San Mateo Uptown Mall Fisher Mall – Quezon City SM Bicutan SM Southmall Venice Grand Canal Mall Gateway Mall SM Cubao SM Sta. Mesa Vista Mall – Taguig PROVINCIAL Abreeza Mall Megaworld Mandurriao SM Bacolod SM Naga Ayala Center Cebu Nepo Mall Dagupan SM Bacoor SM Olongapo Ayala Malls – Capitol Pacific Mall Legazpi SM Baguio SM Pampanga Ayala Malls – Legazpi Parkmall Mandaue SM Baliwag SM Puerto Princesa Balagtas Town Center Puregold Laoag SM Batangas SM Rosales BQ Mall Tagbilaran Robinsons Antique SM Cabanatuan SM Rosario Centrio Mall – CDO Robinsons Bacolod SM Calamba SM San Jose Bulacan CSI Citymall – Dagupan Robinsons Butuan SM Cauayan SM San Pablo CSI Citymall – Iba Robinsons Calasiao SM CDO SM Sangandaan CSI Citymall – San Fernando Robinsons Dumaguete SM Cebu SM Seaside Gaisano – Digos Robinsons Galleria Cebu SM Clark SM Tarlac Gaisano -

List of Fitflop and Res|Toe|Run Stores Nationwide

List of FitFlop and Res|Toe|Run Stores Nationwide FITFLOP FREESTANDING STORES RES|TOE|RUN STORES 1 FITFLOP AYALA ABREEZA 1 RES|TOE|RUN ARANETA CENTER GATEWAY 2 FITFLOP AYALA ALABANG TOWN CENTER 2 RES|TOE|RUN AVENUE SQUARE 3 FITFLOP AYALA CEBU 3 RES|TOE|RUN AYALA ABREEZA 4 FITFLOP AYALA CENTRIO 4 RES|TOE|RUN AYALA ALABANG TOWN CENTER 5 FITFLOP AYALA MARQUEE 5 RES|TOE|RUN AYALA CAMP JOHN HAY 6 FITFLOP AYALA TRINOMA 6 RES|TOE|RUN AYALA CENTER CEBU 7 FITFLOP ROBINSONS ERMITA 7 RES|TOE|RUN AYALA CENTRIO 8 FITFLOP SHANGRILA PLAZA 8 RES|TOE|RUN AYALA GLORIETTA 4 9 FITFLOP SM AURA 9 RES|TOE|RUN AYALA HARBOR POINT 10 FITFLOP SM BACOLOD 10 RES|TOE|RUN AYALA MALLS CLOVERLEAF (KIOSK) 11 FITFLOP SM BAGUIO 11 RES|TOE|RUN AYALA MALLS LEGAZPI 12 FITFLOP SM BATANGAS 12 RES|TOE|RUN AYALA MARKET MARKET 13 FITFLOP SM CABANATUAN 13 RES|TOE|RUN AYALA MARQUEE 14 FITFLOP SM CEBU 14 RES|TOE|RUN AYALA SOLENAD NUVALI 15 FITFLOP SM ILOILO 15 RES|TOE|RUN AYALA THE DISTRICT IMUS 16 FITFLOP SM MALL OF ASIA 16 RES|TOE|RUN AYALA TRINOMA 17 FITFLOP SM MEGAMALL 17 RES|TOE|RUN BANILAD TOWN CENTRE 18 FITFLOP SM NORTH EDSA ANNEX 18 RES|TOE|RUN CENTURY CITY MALL 19 FITFLOP SM PAMPANGA 19 RES|TOE|RUN EVIA PONTERIA NORTH 20 FITFLOP SM SOUTHMALL 20 RES|TOE|RUN FAIRVIEW TERRACES 21 FITFLOP SM TARLAC 21 RES|TOE|RUN FESTIVAL 22 RES|TOE|RUN FISHER MALL 23 RES|TOE|RUN JARO ILOILO 24 RES|TOE|RUN KCC GENERAL SANTOS 25 RES|TOE|RUN KCC ZAMBOANGA 26 RES|TOE|RUN LIMKETKAI 27 RES|TOE|RUN MEGAWORLD EASTWOOD NEW 28 RES|TOE|RUN MEGAWORLD LUCKY CHINATOWN 29 RES|TOE|RUN MEGAWORLD NEWPORT 30 RES|TOE|RUN -

Metropolitan Bank & Trust Company

LIST OF PARTICIPATING SAMSUNG EXPERIENCE STORES SM LANANG PREMIERE AYALA MALLS MARIKINA NCCC MALL VICTORIA PLAZA AYALA HARBOR POINT SM CITY CONSOLACION SM CITY CLARK SM SEASIDE CITY CEBU VISTA MALL BATAAN ROBINSONS GALLERIA CEBU SM CENTER LAS PIÑAS PARKMALL CEBU CITY STARMALL ALABANG SM CITY NOVALICHES AYALA MALLS THE 30TH SM CITY BACOOR SM CENTER MUNTINLUPA SM CITY FAIRVIEW ROBINSONS PLACE CALASIAO SM CITY MANILA SM CITY TARLAC SM MALL OF ASIA SM CITY ROSALES SM SOUTHMALL ROBINSONS PLACE ANTIPOLO SM CITY TAYTAY SM CITY CABANATUAN SM CITY BF PARAÑAQUE NEPO MALL DAGUPAN SM CITY MOLINO SM CITY SAN JOSE DEL MONTE AYALA MALLS TRINOMA SM CITY URDANETA CENTRAL SM CITY TRECE MARTIRES SM CITY TELABASTAGAN THE PODIUM ROBINSONS PLACE TUGUEGARAO SM CITY LEGAZPI SM CENTER DAGUPAN ROBINSONS PLACE ABUCAY AYALA MALLS FELIZ ROBINSONS PLACE ORMOC AYALA MALLS VERTIS NORTH SM CITY BATANGAS FESTIVAL MALL ALABANG SM CITY CALAMBA ROBINSONS PLACE MANILA (ERMITA) SM CITY NAGA SM MEGAMALL FISHER MALL AYALA MALLS CIRCUIT SM CENTER SANGANDAAN SM CITY CEBU AYALA MALLS LEGAZPI SM CITY SAN LAZARO GREENHILLS MALL SM LIGHT MALL GATEWAY MALL SM CITY BALIWAG TUTUBAN COMMERCIAL CENTER SM CITY MARIKINA SM CITY STA. ROSA SM CITY NORTH EDSA SM CITY SAN MATEO SM CITY PAMPANGA ALABANG TOWN CENTER STA. LUCIA EAST GRAND MALL SM CITY MASINAG SM CITY OLONGAPO DOWNTOWN AYALA FAIRVIEW TERRACES GLORIETTA 2 METROPOLITAN BANK & TRUST COMPANY The MCC Center, 6778 Ayala Avenue, Makati City, Philippines 1226 | Tel. No. (632) 88-700-900 PUREGOLD LAOAG SM CUBAO AYALA CENTRIO MALL MARKET! -

Merchant Branch List

Merchant Branch List Anson’s at Landmark SM North Edsa Ayala Fairview Terraces Sta. Lucia East Grand Mall Makati SM Pasig Bonifacio High Street Sta. Lucia East Grand Mall - 2/F Trinoma SM Southmall Centrio Mall Tarlac SM Sucat Eastwood City Walk 1 Waltermart - Pampanga Sta. Lucia East Grand Mall Evia Applebee’s The 30th Mall Fairview Terraces Bonifacio Global City The District Imus Glorietta 3 Bizu Patisserie and Bistro Eastwood City Waltermart Greenbelt 3 Alabang Town Center Harbor Point Eastwood Mall Las Piñas Greenbelt 2 Arena The Bistro Group Marquee Mall Greenhills Promenade Alabang Town Center Baker and Cook Mckinley Hill Robinsons Magnolia SM City North EDSA Conrad Hotel Manila Robinsons Galleria St. Luke’s Global City UP Town Center Robinsons Place Manila Buffalo Wild Wings San Fernando Conrad SM Mall of Asia Black Canyon Coffee The Athlete’s Foot Estancia Mall Solenad Circuit Mall Abreeza Mall, Davao City Glorietta 2 Tomas Morato McKinley Hill Alabang Town Center Uptown Mall Trinoma Ayala Center Cebu Vista Mall Robinsons Place Manila Ayala Two Parkade, BGC Bruno’s Barbers Glorietta 2 Bulgogi Brothers Texas Roadhouse 30th Mall Glorietta 3 Alabang Town Center Uptown Mall Alabang Town Center Limketkai Mall, CDO Greenbelt 5 Conrad Ayala Center Cebu Marquee Mall, Angeles City Newport Mall Ayala Fairview Terraces Robinsons Bacolod SM Lanang Premier Tonkatsu by Terazawa Banawe Robinsons Dumaguete SM Mall of Asia Ayala Center Cebu Centrio Mall Robinsons Ermita Commonwealth Robinsons Galleria Denny’s Village Tavern Eastwood Robinsons Magnolia Trinoma Bonifacio High Street Central Festival Mall Robinsons Palawan Uptown Parade Fort Bonifacio Robinsons Pangasinan Vista Mall Watami Gateway Mall Robinsons Tacloban Greenbelt 2 Glorietta 3 Sta. -

METROPOLITAN BANK & TRUST COMPANY Promo Mechanics

Promo Mechanics 1. Fri-dates with Visa at the Cinemas is open to all who purchase at least two (2) movie tickets from January 17 to March 27, 2020 (all Friday screenings only) at the participating Ayala Malls Cinemas – Glorietta 4, Greenbelt 3, Greenbelt 1, Ayala Malls Circuit, Alabang Town Center, Market! Market!, TriNoma, Fairview Terraces, U.P. Town Center, Ayala Malls Cloverleaf, Ayala Malls The 30th, Ayala Malls Feliz, Ayala Malls Manila Bay, Ayala Malls South Park, Ayala Malls Legazpi, MarQuee, Harbor Point, Ayala Center Cebu and Abreeza. 2. Cinema-goers will get a complimentary popcorn for every 2 movie tickets purchased via tapping to pay (contactless) using their Metrobank Visa contactless credit cards. 3. Once qualified, customer will receive a stub, which will be presented to The Movie Snackbar. A stub is valid only on the day it is issued. 4. A maximum of 1 redemption per Metrobank Visa contactless credit card per day. 5. Movie tickets and stubs are valid only in the cinema branch where it is purchased. 6. Movie tickets are non-refundable. 7. Offer is not applicable in specialty cinemas (A-Luxe Seats, A-Giant Screen, 4DX). 8. Offer is not exchangeable for or convertible to cash and other goods. 9. Offer may not be availed of in conjunction with other existing discounts and promotions. List of Participating Outlets/ Branches: 1. Abreeza 12. Ayala Malls Vertis North 2. Alabang Town Center 13. Fairview 3. Ayala Center Cebu 14. Glorietta 4 4. Ayala Malls Circuit 15. Greenbelt 1 5. Ayala Malls Cloverleaf 16. Greenbelt 3 6. -

Updated Huawei Branches

Store Name Address HUAWEI CONCEPT STORE_AYALA 30TH AYALA 3OTH MALL PASIG CITY HUAWEI CONCEPT STORE_GLORIETTA 3L GLORIETTA 2 AYALA CTR MAKATI HUAWEI CONCEPT STORE_AYALA MALL CIRCUIT 3/L AYALA MALLS CIRCUIT MAKATI HUAWEI CONCEPT STORE_SM MEGAMALL 4/F BLDG B SM MEGAMALL MANDALUYONG HUAWEI CONCEPT STORE_ ROBINSONS FORUM G/F ROBINSONS FORUM EDSA COR PIONEER ST BRGY BARANGKA ILAYA MANDALUYONG HUAWEI CONCEPT STORE_THE PODIUM THE PODIUM ADB AVE ORTIGAS CTR BRGY WACK WACK MANDALUYONG CITY HUAWEI CONCEPT STORE_SM SAN LAZARO SM CITY SAN LAZARO F HUERTAS ST BRGY 350 Z 035 STA CRUZ MANILA HUAWEI CONCEPT STORE_ROBINSONS ERMITA L3 MIDTOWN WING ROBINSONS PLACE MANILA HUAWEI CONCEPT STORE_SM MANILA G/F SM CITY MANILA ARROCEROS ST SAN MARCELINO ERMITA MANILA HUAWEI CONCEPT STORE_SM MARIKINA G/F SM CITY MARIKINA MARCOS HWAY KALUMPANG MARIKINA HUAWEI CONCEPT STORE_STARMALL ALABANG 3/F STARMALL ALABANG SOUTH SUPERHWAY ALABANG MUNTINLUPA HUAWEI CONCEPT STORE_SM MUNTINLUPA SMMT 212-2/F SM MUNTINLUPA NATL RD TUNASAN MUNTINLUPA HUAWEI CONCEPT STORE_SM MALL OF ASIA CZ J W DIOKNO BLVD MALL OF ASIA COMPLEX PASAY HUAWEI CONCEPT STORE_AYALA FELIZ MARCOS HWAY COR AMANG RODRIGUEZ AVE DELA PAZ 4/L AYALA MALL FELIZ PASIG HUAWEI CONCEPT STORE_ROBINSONS METRO EAST 3/L ROBINSONS METRO EAST MARCOS HWAY BRGY DELA PAZ SANTOLAN PASIG HUAWEI CONCEPT STORE_SM EAST ORTIGAS 2/F SM EAST ORTIGAS AVE PASIG HUAWEI CONCEPT STORE_EASTWOOD EASTWOOD MALL EASTWOOD CITY BRGY BAGUMBAYAN QUEZON CITY HUAWEI CONCEPT STORE_ROBINSONS MAGNOLIA 3/L ROBINSONS MAGNOLIA AURORA BLVD COR DONA HEMADY N