CPY Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rats Chats N E W S L E T T E R

HEASB WATER SKI CLUB P. O. Box 3080, El Segundo, CA 90245 Rats Chats n e w s l e t t e r www.RadarRiverRats.org Summer Kick-Off June | 2012 Inside this Contact Important Issue Information Dates I 2012 River Flyer 2 Catherine Ohl, President & Communications June 8, 2012, Friday, 6:30 -10:30 pm Far West Ski Convention Silent Auction I [email protected] Sounding Bored 3 Ogden, Utah See page 10 for details 858.467.9469 I Boat Driver Update 3 June 22–24, 2012 I Wine Maker Dinner 3 Linda Newcomb-Mathis, Secretary Rat’s Water Ski / Wake Board Weekend Park Moabi, Needles, CA I It’s a Wrap 4 [email protected] July 13–15, 2012 & July 27–29, 2012 310.540.6244 I Ski Industry Update 5-7 Rat’s Water Ski / Wake Board Weekends Park Moabi, Needles, CA I Boat Safety 7 Paul Jackson, Treasurer & Membership August 10–11, 2012 & August 24–26, 2012 I [email protected] Getting Fit to Ski 8 Rat’s Water Ski / Wake Board Weekends I Kid’s Korner 9 310.320.0928 Park Moabi, Needles, CA I Aspen 10 Patricia Ortiz, Trips Coordinator Sept 7–9, 2012 & Sept 21–23, 2012 Rat’s Water Ski / Wake Board Weekend I FWSA Convention 11 [email protected] Park Moabi, Needles, CA I About Our Trips 12-14 323.651.0686 September 29, 2012 Wine Maker Dinner for MS I Ski, Board, Boat Etiquette 15 Simone Beaudoin, Reservations San Diego, CA See page 3 for details I Rats Membership Form 16 [email protected] Oct 5–7, 2012 & Oct 19–21, 2012 I River Sign-Up Form 17 714-841-5562 Rat’s Water Ski / Wake Board Weekend I Park Moabi, Needles, CA Community Center 18 Gene -

2017/18 Steamboat Press Kit

2017/18 Steamboat Press Kit TABLE OF CONTENTS What’s new this winter at Steamboat ............................................................... Pages 2-3 New ownership, additional nonstop flights, mountain coaster, gondola upgrades Expanded winter air program ........................................................................... Pages 4-5 Fly nonstop into Steamboat from 14 major U.S. airports. New this year: Austin, Kansas City Winter Olympic tradition ................................................................................ Pages 6-10 Steamboat has produced 89 winter Olympians, more than any other town in North America. Champagne Powder® snow ............................................................................ Pages 11-14 Family programs ............................................................................................. Pages 15-17 Mountain facts and statistics ......................................................................... Pages 18-21 History of Steamboat ...................................................................................... Pages 22-30 Events calendar .............................................................................................. Pages 31-34 Cowboy Downhill ............................................................................................ Pages 35-38 Night skiing and snowboarding ..................................................................... Pages 39-40 On-mountain dining and Steamboat’s top restaurants ............................... Pages 41-48 -

The Chateaux Deer Valley Media Kit

The Chateaux Deer Valley Media Kit The Chateaux Deer Valley 7815 Royal Street East | Park City, UT 84060 Introduction The Chateaux Deer Valley pg 2 Media Kit Located mid-mountain at Deer Valley Resort, the AAA Four Diamond hotel offers flexible accommodations including studios and multi-bedroom suites. Studios and suites feature full kitchens, living rooms and decks. Room ame- nities include gas fireplaces, free Wi-Fi, and flat screen televisions. Hotel amenities include family-friendly Italian restaurant serving lunch and dinner (seasonal hours), spa, fitness center, outdoor pool, complimentary parking, guest shuttle to Main Street, and function space. Just steps from the hiking and biking trails of Deer Valley Resort. Table of Contents Hotel Overview 2 Guest rooms and amenities 3 Dining 4 Spa 6 Destination and Recreation 9 Location: Nestled mid- mountain in the heart of Sil- Hotel Amenities: ver Lake Village at Deer Val- • On-site Check-In ley Resort in the picturesque • 24 Hour Front Desk town of Park City, Utah, The • Concierge (winter only) Chateaux is an easy 45 min- • On-Site Restaurant (seasonal operations) ute drive (38 miles/61km) • Spa / Salon (seasonal operations) from Salt Lake International • Outdoor Pool and Hot Tub Airport and 5 minutes from • Fitness Center Historic Main Street in Park • Sports Equipment Rental (seasonal operations) City. • Daily Housekeeping • Complimentary Local Shuttle • Nightly Turndown Service • Business Center • Complimentary WiFi • Conference Facility • Complimentary Underground Heated Parking • Deer Valley Resort Lift Tickets Sold at Front Desk • Complimentary Newspapers Guest rooms and amenities The Chateaux Deer Valley pg 3 Media Kit A range of accommodations are available including studios and one - to four- bedroom suites. -

Vail Resorts to Operate Canyons Resort in Park City, Utah

May 29, 2013 Vail Resorts to Operate Canyons Resort in Park City, Utah - Vail Resorts enters into a long-term lease with Talisker for first mountain resort in Utah. - Canyons will be included in the Epic Season Pass for the 2013-2014 winter season. BROOMFIELD, Colo., May 29, 2013 /PRNewswire/ -- Vail Resorts today announced that the Company has entered into a long- term lease with affiliate companies of Talisker Corporation for Canyons Resort in Park City, Utah. Under the lease, Vail Resorts has assumed all of the resort operations of Canyons while Talisker has retained its development rights for four million square feet of real estate at the resort. "With 4,000 skiable acres, easy access to the town of Park City and $75 million in recent resort improvements, Canyons is a perfect complement to our collection of world-class mountain resorts," said Rob Katz, chairman and chief executive officer of Vail Resorts. "I commend the Talisker and Canyons team for the outstanding work they have done to redevelop the resort, which is reflected in a top 10 ranking by SKI Magazine and #4 ranking by Outside Magazine. We look forward to building on that momentum and including Canyons in our industry-leading season pass products, which next season will offer guests access to Colorado, Tahoe and Utah on one season pass, a first in ski industry history. We will also leverage our guest database and domestic and international sales and marketing efforts to continue to drive Canyons' growth. Talisker has an outstanding track record of high-end resort development and we look forward to working together to create something truly extraordinary with Talisker's four million square feet of remaining approved residential and commercial density at Canyons." The transaction also incorporates the potential for the lease, without additional consideration, to include the land under the ski terrain of Park City Mountain Resort that is adjacent to Canyons and is currently owned by Talisker and is subject to pending litigation. -

Ski Resorts in the Western United States Ranked by Elevation (In Feet)

Ski Resorts in the Western United States Ranked by Elevation (in feet) Beginner(B) or Groomed Alternate Driving Time Driving Time Intermediate(I) Age Kids Top Cruising Base Lodging City Lodging (airport to (airport to Ski Resort Website State Location Lift Ticket Ski Free Elevation Rating** Elevation Elevation Lodging City Elevation Alternate Lodging City Closest Airport resort)*** Major airport resort)*** Arapahoe Basin http://www.arapahoebasin.com/ABasin/Default.aspx Colorado Dillon, CO 5- 13050 3 10780 9112 / 9035 Dillon/Silverthorne DEN-Denver 1:33 Loveland Ski Area http://www.skiloveland.com/ Colorado Georgetown, CO B 5- 13010 3 10800 9112 / 9035 Dillon/Silverthorne 5322 Denver DEN-Denver 1:19 Breckenridge http://www.breckenridge.com/ Colorado Breckenridge, CO 4- 12998 4 9600 9600 Breckenridge 9075 Frisco DEN-Denver 1:53 Telluride http://tellurideskiresort.com/TellSki/index.aspx Colorado Telluride, CO 12570 2 8725 8750 Telluride TEX-Telluride :14 MTJ-Montrose 1:29 Snowmass http://www.aspensnowmass.com/ Colorado Aspen, CO 12510 5 8104 9100 Snowmass Village 6171 Carbondale ASE-Aspen :18 DEN-Denver 3:43 Keystone http://www.keystoneresort.com/ Colorado Keystone, CO 4- 12408 4 9280 9173 Keystone Village 9075/9035/9112 Frisco/Silverthorne/Dillon EGE-Vail 1:18 DEN-Denver 1:42 Copper Mountain http://www.coppercolorado.com/winter/index.html Colorado Copper Mtn, CO 5- 12313 5 9712 9700 Copper Mountain 9075/9035/9112 Frisco/Silverthorne/Dillon EGE-Vail :49 DEN-Denver 1:39 Crested Butte http://www.skicb.com/cbmr/index.aspx Colorado Crested Butte, -

Ski & Snowboarding December 4,1997

Ski & Snowboarding December 4,1997 AMERICA HAS mmm^ STOWE WINTER PARK CRESTED BUTTE SUGARBUSH WHITEFACE MOUNTAIN LOON MOUNTAIN BOLTON VALLEY PARK CITY JAY PEAK VAIL ip^f/^J) —r;;1'" .- SKI WINDHAM BRETON WOODS OKEMO BLUE KNOB CANAAN VALLEY BELLEAYRE LABRADOR MOUNTAIN SEVEN SPRINGS ASCUTNEY MOUNTAIN BLUE MOUNTAIN 8TRATTON MOUNTAIN JACK FROST MOUNTAIN BIG BOULDER KILLINGTON V" tT • ' f • fc •* "fc L fr. -ft 'fc f k J" December 4,1987 Ski & Snowboardlng WONDERFUL SKI & BOARDING FUN! :'•§. GORE MOUNTAIN ALPINE MOUNTAIN POCONOS HIDDEN VALLEY SUGARLOAFUSA GREEK PEAK JIMINY PEAK WOODSTOCK INN SMUGGLERS NOTCH THE CANYONS SUNDAY RIVER SNOWSHOE SONG MOUNTAIN TOGGENBURG NEMACOLIN WOODLANDS MONTAGE ATTITASH SONG MOUNTAIN MOUNT SNOW BRQDIE MOUNTAIN jfiy HUNTER MOUNTAIN ELK MOUNTAIN NORTH9TAR BROMLEY i'-\:-> \Y i .• .'• **• - '•: .'••;? •'.' trailsinNewYoryiatcl i lOMNHIB *l ntsto '••:''.'•• .';: *'*•.'': hwtosHey (OTKIIXS Bobcat 5)14-676-3143 Catamount 518-325^200 , Holiday Mtn. 914-796^161 Mt, Peter 9M-98MW0 Scotch \Wte>1607-652-2470- • • Ski I'lsittcktll 6OT-326-350O JikiWindlwnifiOO-SMWLNDHAM Sterling Forc»( 911-35I-2I63 NOR11I COUNTRY Ihrnnhtthkifng/ridlttg Dr)'Hill 800-3/9-8584 : r Gore Mtn, 51^51-MU ; RojiilMtn. 518-S35-6445 SnuwRidgc 800-962-8419 Titus Mtn. 800-8*8766 •Test Mtn, 518-793-6606' Whilefacc Mtn. 518-946-2223 WillardMln. 518-te337 Cross-country skiing BaritEakt 518-576.22Z1 Cascade U Center 518-523-96O5 Cuwiingdani's 800-888-iiAni Friends lake Inn 518-494-4751 GwnetlllUX-C 518*251-2821 G'mon! Skiing is something you always wanted to try GweMln,5i8-251'2411 Lapland Lake but couldn't find die timc-didiu know how to start- Mt. -

St. Louis Ski Club 2020 Ski Trips

St. Louis Ski Club 2020 Ski Trips Ski Resort & Trip Captain Dates Lodging What’s Included Price In- Ice 1/19/20 “Ski Town USA With Lodging/Airfare Steamboat, CO Trip Price the FSA” (FSA Trip) $1,300 Thursday thru Transfers to/from www.steamboat.com 1/26/20 Phoenix Hayden Airport Jan 9th Deposit $700 6 PM 26 skiers 2BR/2B condo for four FSA Welcome Paul Snyder people Reception Balance [email protected] 6 ski days $600 Walking distance to FSA Banquet, 314-761-4797 the slopes! Parties & Races Due* Trip Full! (Racing is optional) 11/15/19 Wait List Only Flatland Race Info www.flatlandski.org Club Party Telluride, CO 2/8/20 “Unmatched in North Lodging/Airfare Trip Price www.tellurideskiresort.com America” thru $1,780 Wednesday Transfers to/from Dan McGurk 2/14/20 Peaks Hotel Montrose Airport Jan 29th Deposit [email protected] $900 6 PM 18 32 2 people per hotel Club Party 660-216-3623 skiers room Balance $880 5 ski days Trip Full! Hot Buffet Breakfast Included Due* 12/1/19 Wait List Only Park City, UT 3/11/20 “Elevated. Enhanced. Lodging/Airfare Trip Price Reimagined” $1,109 www.parkcitymountain.com/ thru Wednesday Transfers to/from 3/16/20 Peaks Hotel Salt Lake City Deposit March 4th Airport $550 Lou Boyer 6 PM 16 36 2 people per hotel [email protected] skiers room Club Party Balance . 618-610-2297 $500 4 ski days Hot Buffet Breakfast Welcome Trip Full! Due* Included Reception 1/7/20 Wait List Only Icebreakers to be held at Llywelyn’s Pub — 17 W. -

Resort Overview

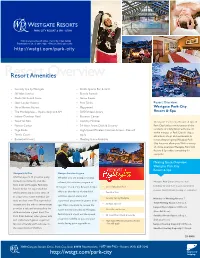

3000 Canyons Resort Drive, Park City, Utah 84098 Reservations: (877) 288-7422 • Resort: (435) 655-2240 http://wstgt.com/park-city ResortResort Amenities Overview • Serenity Spa by Westgate • Drafts Sports Bar & Grill • Ski Valet Service • Bicycle Rentals • Aloha Ski Rental Store • Game Room • Skier Locker Rooms • Pool Tables Resort Overview: • Ski-in/Ski-out Resort • Playground Westgate Park City • The Marketplace – Opens daily at 8 AM • DVD/Video Library Resort & Spa • Indoor/Outdoor Pool • Business Center • Two Hot Tubs • Laundry Facilities Westgate Park City Resort & Spa in • Fitness Center • 24-Hour Front Desk & Security Park City, Utah, provides guests all the comforts of a fully furnished home, all • Yoga Studo • High-Speed Wireless Internet Access - Fee will within minutes of Park City ski slopes, • Tennis Court apply attractions, shops and restaurants. A • Basketball Court • Meeting Space Available nonsmoking property, Westgate Park City does not allow pets. With a variety of onsite amenities, Westgate Park City Resort & Spa offers something for everyone! Meeting Space Overview: Westgate Park City Resort & Spa Westgate Kid’s Club Westgate Activities Program Children ages 3-12 (must be potty Whether you are young, or young trained) are invited to visit the at heart, the activities program at Westgate Park City provides the ideal Kid’s Club at Westgate Park City Westgate Park City Resort & Spa • Indoor/Outdoor Pool backdrop for your next special event, family Resort & Spa for supervised fun reunion, church retreat, meeting or convention. while parents enjoy some time off offers an abundance of scheduled • TwoRESORT Hot Tubs to experience resort activities (or activities, special events and • Serenity Spa by Westgate Number of Meeting Rooms: 7 rest) on their own! The approach is supervised programs for guests of all Highlights • Ski Valet Service Total Meeting Space: 6,750 sq. -

Osguthorpe V. ASC Utah, Inc

2010 UT 29 232 P.3d 999 This opinion is subject to revision before final publication in the Pacific Reporter. IN THE SUPREME COURT OF THE STATE OF UTAH ----oo0oo---- D.A. Osguthorpe, in his Nos. 20080770 capacity as Trustee of the 20090042 Dr. D.A. Osguthorpe Trust; 20090043 and D.A. Osguthorpe Family Partnership, Petitioners and Appellants, v. Wolf Mountain Resorts, L.C.; Petitioner and Appellant, v. ASC Utah, Inc., in its own stead; ASC Utah, Inc., as the representative of a defendant class consisting of ASC Utah, Inc., skiers, contractors, all other invitees and successors trespassing on plaintiffs’ real property under color of both ASC Utah, Inc.’s claim of right as a lessee from Wolf Mountain Resorts, L.C., and ASC Utah, Inc.’s claim of right as a lessee directly from F I L E D plaintiffs, Respondents and Appellees. May 7, 2010 --- Third District, Silver Summit The Honorable Bruce L. Lubeck No. 070500622 Attorneys: David W. Scofield, R. Reed Pruyn Goldstein, Thomas W. Peters, Salt Lake City, for petitioners D.A. Osguthorpe and D.A. Osguthorpe Family Partnership Victoria C. Fitlow, Park City, for petitioner Wolf Mountain Resorts, L.C. John R. Lund, Kara L. Pettit, Julianne P. Blanch, Rodney R. Parker, Michael M. Homer, Brian D. Bolinder, Jesse C. Trentadue, Salt Lake City, for respondents --- PARRISH, Justice: INTRODUCTION ¶1 This case presents questions regarding the purpose and applicability of Utah’s unlawful detainer statute. Appellants D.A. Osguthorpe and the D.A. Osguthorpe Family Partnership (collectively the “Osguthorpes”) appeal the district court’s dismissal of their unlawful detainer claims against American Skiing Company (“American Skiing”) and Wolf Mountain Resorts (“Wolf Mountain”). -

Wolf Mountain Resorts, LC, a Utah Limited

Brigham Young University Law School BYU Law Digital Commons Utah Court of Appeals Briefs 2010 Wolf Mountain Resorts, L.C., a Utah limited liability company v. ASC Utah, Inc., a Delaware corporation : Brief of Appellant Utah Court of Appeals Follow this and additional works at: https://digitalcommons.law.byu.edu/byu_ca3 Part of the Law Commons Original Brief Submitted to the Utah Court of Appeals; digitized by the Howard W. Hunter Law Library, J. Reuben Clark Law School, Brigham Young University, Provo, Utah; machine-generated OCR, may contain errors. David M. Wahlquist; Rod N. Andreason; Ryan B. Frazier; Kirton & McConkie; Attorneys for Appellant. John R. Lund; Kara L. Pettit; Snow, Christensen, and Martineau; John P. Ashton; Clark K. Taylor; Van Cott, Bagley, Cornwall & McCarthy; Attorneys for Appellee. Recommended Citation Brief of Appellant, Wolf Mountain Resorts v. ASC Utah, No. 20100342 (Utah Court of Appeals, 2010). https://digitalcommons.law.byu.edu/byu_ca3/2314 This Brief of Appellant is brought to you for free and open access by BYU Law Digital Commons. It has been accepted for inclusion in Utah Court of Appeals Briefs by an authorized administrator of BYU Law Digital Commons. Policies regarding these Utah briefs are available at http://digitalcommons.law.byu.edu/utah_court_briefs/policies.html. Please contact the Repository Manager at [email protected] with questions or feedback. IN THE UTAH COURT OF APPEALS WOLF MOUNTAIN RESORTS, L.C., a Utah limited liability company, Plaintiff/Appellant, Appellate Case No. 20100342-CA Trial Court Case No. 070500485 ASC UTAH, INC., a Delaware corporation, (ORAL ARGUMENT REQUESTED) Defendant/Appellee On Appeal from an Order Denying Wolf Mountain Resorts, L.C.'s Motion for Partial Summary Judgment and Granting ASC Utah, Inc.'s Cross-Motion for Summary Judgment by the Third Judicial District Court, Silver Summit District, The Honorable Bruce C. -

Hyatt Expands Presence in Mountain West with Hyatt Escala Lodge at Park City

Hyatt Expands Presence in Mountain West with Hyatt Escala Lodge at Park City 11/9/2010 Ski-in, ski-out 178-suite hotel in the Canyons Resort of Park City, Utah CHICAGO (November 9, 2010) – Hyatt Hotels & Resorts announced today its plans to introduce Hyatt Escala Lodge at Park City in late November 2010. The ski-in, ski-out condominium hotel property is located at the base of the Sunrise Chairlift in the Canyons Resort in Park City, Utah – the largest ski and snowboard area in Utah with 4,000 skiable acres. Hyatt Escala Lodge will also be an ideal base for exploring Park City and enjoying its many outdoor summer activities such as golf, fly fishing, and mountain biking. This mountain retreat at the Canyons is reminiscent of the grand European lodges with native mountain stonework and timber frame construction. Hyatt Escala Lodge at Park City consists of 85 spacious condominiums, which can be divided into 178 residential-style, hotel suites ranging in size from one-bedroom units at 680 square feet to four- bedroom units with 2,810 square feet. The suites feature mountain view balconies, living and dining rooms, fully equipped gourmet kitchens with stainless steel appliances, alder cabinets, extensive millwork, and hardwood flooring, as well as in-suite washers and dryers. With stone fireplaces in all living rooms and in most master bedrooms, and custom stone flooring, jetted tubs, and European frameless showers in the bathrooms, guests will experience a sophisticated escape. At Park City’s Hyatt Escala Lodge, guests will be able to enjoy a fitness center, a steam room, year-round heated swimming pools, two oversized spa tubs, and a ski valet. -

Squaw Valley |Alpine Meadows Base-To-Base Gondola Project Final EIS/EIR Apdx C

Appendix C Squaw Valley | Alpine Meadows Base-to-Base Gondola Final Visitation and Use Assessment SQUAW VALLEY | ALPINE MEADOWS BASE-TO-BASE GONDOLA FINAL VISITATION AND USE ASSESSMENT February 2018 Prepared by: SE Group and RRC Associates Squaw Valley | Alpine Meadows Gondola Visitation and Use Assessment BACKGROUND Squaw Valley Ski Holdings, LLC (SVSH) has applied to the U.S. Forest Service and Placer County, California for permission to construct a gondola connecting the Squaw Valley and Alpine Meadows ski areas.1 The U.S. Forest Service and Placer County are analyzing the potential environmental impacts of this project through a joint Environmental Impact Statement (EIS)/Environmental Impact Report (EIR). The EIS/EIR will analyze direct and indirect effects of the Proposed Action and alternatives to the Proposed Action that would occur on both National Forest System (NFS) lands as well as private lands within Placer County, California. Past, present, and reasonably foreseeable future activities that could affect, or could be affected by, implementation of the Proposed Action and alternatives will be analyzed cumulatively. This assessment is designed to inform the analysis of potential direct impacts of the proposed Base-to- Base Gondola by evaluating the anticipated changes to annual snowsports visitation at Squaw Valley | Alpine Meadows as a result of the proposed project. This analysis evaluates the anticipated impact on total snowsports visits (i.e., skier visits) and potential changes in the Squaw Valley | Alpine Meadows market share expected to specifically result from the installation and operation of the proposed Base-to-Base Gondola. METHODOLOGIES AND DATA Amenities and Attractions At the root of this assessment is the consideration of whether the proposed Base-to-Base Gondola would principally provide an added amenity at Squaw Valley | Alpine Meadows or if the added resort connectivity that it would provide would be sufficiently unique to act as an attractant to increased visitation.