Exim Bank EXIM JOURNEY – Key Milestones

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

China Export and Import Bank (China EXIM Bank) Issuance Notice Of

UNOFFICIAL TRANSLATION (OFFICIAL CHINESE GUIDELINES BELOW) China Export and Import Bank (China EXIM Bank) Issuance Notice of the “Guidelines for Environmental and Social Impact Assessments of the China Export and Import Bank’s (China EXIM Bank) Loan Projects" Guidelines for Environmental and Social Impact Assessments of the China Export and Import Bank’s (China EXIM Bank) Loan Projects General Principles Article 1. In order to implement the national strategies for sustainable development, promote economic, social and environmental development, and effectively control credit risks, the Guidelines were developed according to the "People's Republic of China’s Environmental Impact Assessment (EIA) Act," "People's Republic of China’s Environmental Protection Law", "Environmental Management for Construction Project Ordinance" and other relevant state laws and regulations, and with reference to the relevant regulations and procedures for the environmental and social assessments of international financial organizations. Article 2. These Guidelines apply to the loan procedure of China EXIM Bank. Article 3. The China EXIM Bank’s loan projects are classified as domestic or offshore projects, according to the area in which the projects are implemented. Domestic projects mean that the projects are implemented inside China with China EXIM Bank’s loan support. Offshore projects refer to the projects that are implemented outside China with China EXIM Bank’s loan support. Article 4. When China EXIM Bank reviews its loan projects, not only economic benefits, but also social benefits and environmental demands are considered. Article 5. Environmental assessment refers to the systematic analysis and evaluation of the environmental impacts and its related impacts on human health and safety due to the implementation of the projects. -

Case Study Exim Bank

CASE STUDY Exim Bank, Comoros deploys Eximnet, i-exceed’s Appzillon based Internet banking solution. About Exim Bank Exim Bank (Tanzania) Ltd, is the 6th largest bank in Tanzania in terms of total assets and deposits (December 2012) with total assets of over a trillion shilling (June 2013). The bank is known as one of the most innovative & fastest growing banks in the country and is reckoned for its professionalism and business ethics. Having remained at the forefront of providing quality banking services in Tanzania since its inception in Aug' 97, Exim Bank wanted to introduce mobile and internet banking at its subsidiary Exim Bank Comoros Exim Bank’s Requirement Exim Bank wanted to improve sales effectiveness and increase customer base by offering their existing banking services in the mobile and internet space. The solution was expected to possess: High levels of data Multilingual A unified integrity and support design theme security and integrated environment Platform The ability to independence seamless work with existing backend systems i-exceed’s Solution Using Appzillon, i-exceed’s flagship Mobile Application Development Platform (MADP), Eximnet was built and deployed in just 50 days. The salient features of the Eximnet application are: 1 2 3 Multilingual Seamless integration with support the core banking backend Unified user experience system using a new web across mobile and services tier Internet platforms 4 5 Interfaces with the Inclusion of all key technical support to consumer transactions and monitor user actions request facilities on mobile and handle service and Internet platforms requests in real time Result Business benefits of Eximnet: CUSTOMERS BANK Access to best in class mobile and Reduced branch workload and branch internet banking facilities with operation costs as customers can international standards and security. -

African Markets Revealed

AFRICAN MARKETS REVEALED SEPTEMBER 2020 • Steven Barrow • Ferishka Bharuth • Mulalo Madula • Angeline Moseki • Fausio Mussa • Jibran Qureishi • Dmitry Shishkin • Gbolahan Taiwo www.standardbank.com/research 1 Standard Bank African Markets Revealed September 2020 Recovering, but not out of the woods • The worst of the pandemic will arguably be reflected in Q2:20 GDP growth outcomes. Of the countries in our coverage, we see only a handful of economies escaping recession in 2020. • Economic growth in Q2:20 contracted by 6.1% y/y, 3.3% y/y, and 3.2% y/y in Nigeria, Mozambique and Uganda respectively. The Ghanaian economy too contracted by 3.2% y/y in Q2:20, even worse than the 0.4% y/y contraction that we forecast for our bear scenario in the May edition of this publication. • The more diversified economies and those with large subsistence agriculture sectors could post mild, yet positive, growth in 2020. Most East African countries fall into this bracket. Egypt too might also avoid a technical recession this year. • However, Nigeria, Angola, Zambia and even Botswana, being overly reliant on just a few sectors to drive growth, will most likely contract this year. The only question is by how much? • Tourism-dependent economies will take a hit. We still don’t see any meaningful recovery in tourism until a global vaccine is at hand. The weakness in the tourism sector is mostly a BOP problem rather than a growth problem for many African countries. However, the service value chain that relies on a robust tourism sector too, will most likely weigh down growth in these economies. -

At Arusha Commercial Case No 3 of 2019 Crdb

IN THE HIGH COURT OF TANZANIA (COMMERCIAL DIVISION) AT ARUSHA COMMERCIAL CASE NO 3 OF 2019 CRDB BANK PLC.......................................................... PLAINTIFF Vs LAZARO SAMWEL NYALANDU................................... DEFENDANT RULING B.K. PHILLIP, 3 This ruling is in respect of the points of preliminary objection to wit; i. That, the suit is bad in law as it contravenes Order VII, Rule 1 (c) of the Civil Procedure Code, Chapter 33 R.E. 2019. ii. That the suit is bad in law as it contravenes Order VII, Rule 1 (c) of the Civil Procedure Code, Chapter 33 R.E. 2019 as amended by G.N No. 381 of 2019. iii. That, the suit is bad in law as it contravenes section 18 (a), (b)and (c) of the Civil Procedure Code, Chapter 33, R.E. 2019 The plaint reveals that this case emanates from a loan facility agreement signed between the parties herein, whereby the plaintiff granted to the defendant a loan to a tune of TZS 400,000,000/= The defendant offered his property located at Plot No. 9 & 10 Block "B", with CT No. 58063, LO No. 635518, Gomba Area, in Arumeru District, Arusha Region as security i for the loan. It is alleged in the plaint that the plaintiff defaulted the repayment of the loan. In this case the plaintiff prays for judgment and decree against the defendant as follows; i. An order for payment of the sum of Tshs. 304,795,267/= to the plaintiff by the defendant. ii. An order for payment of interest on the principal sum in prayers (i) above at the contractual rate of 14.5% from 16th August, 2019 to the date of Judgement. -

Early Recovery Plan

UNION OF COMOROS COMOROS FLOODING 2012 Early Recovery Plan Moroni, August 2012 TABLE OF CONTENTS ACRONYMS AND ABBREVIATIONS ..................................................................................................................... 3 FOREWORD ....................................................................................................................................................... 4 STATEMENT BY H.E. DR IKILILOU DHOININE, PRESIDENT OF THE UNION OF COMOROS .......................................................... 4 FOREWORD ....................................................................................................................................................... 5 STATEMENT BY MR DOUGLAS CASSON COUTTS, UNITED NATIONS RESIDENT COORDINATOR .................................................. 5 ACKNOWLEDGEMENTS ...................................................................................................................................... 6 EXECUTIVE SUMMARY....................................................................................................................................... 7 BASIC HUMANITARIAN AND DEVELOPMENT INDICATORS FOR THE UNION OF COMOROS ................................. 8 TABLE I. SUMMARY OF REQUIREMENTS – BY SECTOR.......................................................................................... 8 TABLE II. SUMMARY OF REQUIREMENTS – BY UN ORGANIZATION.......................................................................... 9 1. CONTEXT AND HUMANITARIAN CONSEQUENCES ..................................................................................... -

Pricing Guide 2021.Pdf

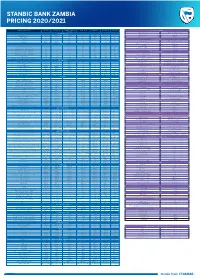

STANBIC BANK ZAMBIA PRICING 2020/2021 TYPE OF TRANSACTION PRIVATE EXECUTIVE ACHIEVER (EVERYDAY CORPORATE COMMERCIAL ENTERPRISE TAMANGA INVOICE DISCOUNTING BANKING) Arrangement Fee 2.5% Secured 5% unsecured ADMINISTRATION Interest rate LCY Customised Montly Management Fees ZMW 330 ZMW 110 ZMW 55 ZMW 200 ZMW 165 ZMW 150 ZMW 100 Interest rate FCY Customised Debit Activity Fees Free Free Free Free Free Free Free DISTRIBUTOR FINANCE Credit Activity Fees Free Free Free Free Free Free Free Arrangement fee 2.5% Secured 5% unsecured Bundle Pricing ZMW 385 ZMW 165 ZMW 87 N/A N/A N/A N/A DEPOSIT Management fee per quarter Customised Local cheque deposit at branch Free Free Free Free Free Free Free Rollover fee Customised Own Bank cheque within clearing area Free Free Free Free Free Free Free Interest rate (ZMW) Customised Own Bank cheque outside clearing area Free Free Free Free Free Free Free Interest rate (USD) Customised Agent Bank cheque within clearing area Free Free Free Free Free Free Free FOREIGN CURRENCY SERVICES Agent Bank cheque outside clearing area Free Free Free Free Free Free Free Purchase of Foreign Exchange Cash Deposit at Branch Free Free Free Free Free Free Free Foreign notes No charge Bulk Cash Deposit Foreign Currency ( Above $50,000) 1% 1% 1% 1% 1% 1% 1% Telegraphic Transfer/SWIFT (inward) US$20 flat WITHDRAWALS Drafts/Bills/Cheques 1.1% min US$40 plus VAT + Foreign charges At branch within K25,000 ATM limit Free Free ZMW 120 N/A N/A N/A N/A Drafts/Bills/Cheques 1.1% min US$40 plus VAT + Foreign charges Own ATM ZMW 9 ZMW 9 ZMW -

Letter of Interest Application

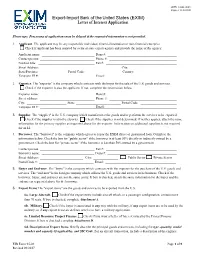

OMB #3048-0005 Expires 11/30/2021 Export-Import Bank of the United States (EXIM) Letter of Interest Application Please type. Processing of applications may be delayed if the requested information is not provided. 1. Applicant. The applicant may be any responsible individual, financial institution or non-financial enterprise. ☐ Check if applicant has been assisted by a city or state export agency and provide the name of the agency: Applicant name: ________________________________ Duns #: __________________________________________ Contact person: _________________________________ Phone #: _________________________________________ Position title: __________________________________ Fax #: ___________________________________________ Street Address: _________________________________________________ City: _____________________________ State/Province: ________________ Postal Code: _____________________ Country: _________________________ Taxpayer ID #: __________________________________ Email: ____________________________________________ 2. Exporter. The "exporter" is the company which contracts with the buyer for the sale of the U.S. goods and services. ☐ Check if the exporter is also the applicant. If not, complete the information below. Exporter name: _________________________________ Duns #: __________________________________________ Street address: _________________________________ Phone #: _________________________________________ City: ________________________ State: ___________________________ Postal Code: ______________________ Taxpayer -

India: an Ideal Partner in Tanzanian Agriculture?

Journal of Language, Technology & Entrepreneurship in Africa Vol. 4 No. 1 2013 India: An Ideal Partner in Tanzanian agriculture? Darlene K. Mutalemwa [email protected] Mzumbe University, Tanzania. Abstract The agricultural sector is the driving force of the Tanzanian economy. Therefore the need to develop and modernize it is of paramount importance for food production, poverty reduction and growth in other sectors. This paper aims at increasing knowledge and understanding of the contribution of India including its private companies, in Tanzanian agricultural investments, development and transformation. The paper concludes with some final remarks broadly stating that while Tanzania has enormous potential for attracting private investment in agriculture, there are serious constraints to India’s effective engagement in Tanzanian agriculture that include the need for improving the business environment, engaging the Indian Diaspora and increasing public expenditures on drivers of productivity. Key Words: Agriculture, India, Tanzania, Partner Introduction The Necessity for a Green Revolution In the opinion of the late President of Tanzania, J.K. Nyerere, Tanzania needs a Green revolution which has been the cornerstone of India’s agricultural achievement, transforming the country from one of food deficiency to self- sufficiency ( Tanzania National Business Council, 2009: ii): “Because of the importance of agriculture in our development, one would expect that agriculture and the needs of the agricultural producers would be the beginning, and the central reference point of all our economic planning. Instead, we have treated agriculture as if it was something peripheral, or just another activity in the country, to be treated at par with all the others, and used by the others without having any special claim upon them… We are neglecting agriculture. -

Export-Import Bank of the United States 2012 ANNUAL REPORT EXPORTS GROW JOBS

EXPORTS GROW JOBS Export-Import Bank of the United States 2012 ANNUAL REPORT EXPORTS GROW JOBS Facts About Ex-Im Bank Did you know? ■ The Export-Import Bank of the United States (Ex-Im Bank), an independent federal government agency, operates at no cost to U.S. taxpayers. ■ After paying all of its operating and program costs during the past five years, Ex-Im Bank contributed $1.6 billion to the U.S. Treasury. ■ More than 85 percent of Ex-Im’s transactions in recent years directly benefited small businesses. ■ Since 2008 Ex-Im Bank has assisted in creating or sustaining more than one million American jobs. 2 | EXPORT-IMPORT BANK OF THE UNITED STATES Table of Contents Mission 2 Reauthorization 3 Chairman’s Message 4 FY 2012 Highlights 6 Supporting U S Jobs 8 Increasing American Competitiveness 10 Customer-Centered Approach 11 Government at the Speed of Business 12 Global Access for Small Business 14 Opening New Markets 18 Sub-Saharan Africa 20 Infrastructure 22 Renewable Energy and Environment 24 Industries 27 Map of Small-Business Support by State 28 FY 2012 Financial Report 29 Directors and Officers 83 Map of Regional Export Finance Centers 84 2012 ANNUAL REPORT | 1 EXPORTS GROW JOBS Mission The Export-Import Bank of the United States (Ex-Im Bank) is the official export-credit agency of the United States. Ex-Im Bank is an independent, self-sustaining executive agency and a wholly owned U.S. government corporation. The Bank’s mission is to support jobs in the United States by facilitating the export of U.S. -

Export-Import Bank of the United States-2017 Annual Report

EXPORT-IMPORT BANK of the UNITED STATES Table of Contents Mission Mission ......................................................................................................................... 1 The Export-Import Bank of the United States (EXIM or competition backed by other governments, EXIM levels the Bank) is the official export credit agency (ECA) of the the playing field by providing buyer financing to match or Message from Vice Chairman of the Board (Acting) ................................................. 2 United States. EXIM is an independent, self-sustaining counter the financing offered by approximately 96 ECAs federal agency that exists to support American jobs by around the world. Export Credit Insurance: American Classic Hardwoods, Memphis, Tennessee .......... 4 facilitating the export of U.S. goods and services—at no EXIM Bank assumes credit and country risks that the private cost to U.S. taxpayers. Working Capital Guarantees: Thrustmaster of Texas Inc., Houston ........................ 6 sector is unable or unwilling to accept. The Bank’s charter EXIM does this in two principal ways. First, when requires that all transactions it authorizes demonstrate Loan Guarantees: Leonardo of Philadelphia, Pennsylvania ..................................... 8 exporters in the United States or their customers are a reasonable assurance of repayment. The Bank closely unable to access export financing from private sources, monitors credit and other risks in its portfolio. The Bank Financial Report ....................................................................................................... -

Stanbic Bank Zambia PMI™ Output Returns to Growth in May

News Release Embargoed until 1030 CAT (0830 UTC) 3 June 2021 Stanbic Bank Zambia PMI™ Output returns to growth in May Key findings PMI sa, >50 = improvement since previous month 60 First rise in activity for 27 months 55 Near-stabilisation of employment 50 45 Sharpest rise in purchase costs since December 40 2016 35 30 '15 '16 '17 '18 '19 '20 '21 Data were collected 12-24 May 2021 Sources: Stanbic Bank, IHS Markit. Output returned to growth in the Zambian private sector meant that firms were able to work through backlogs during May, one month after the same had been the case during May. A modest reduction in outstanding business for new orders. New business ticked back down slightly was recorded, ending a two-month sequence of in the latest survey period, but there were further signs accumulation. that overall business conditions are more conducive to Employment was broadly stable, falling only fractionally growth than has been the case for some time. As a result, and at the joint-slowest pace in the current 16-month firms continued to expand their purchasing activity and sequence of decline. kept their staffing levels broadly unchanged. Firms meanwhile increased their purchasing activity The headline figure derived from the survey is the for the second month running, leading to a further Purchasing Managers’ Index™ (PMI™). Readings above accumulation of inventories as suppliers' delivery times 50.0 signal an improvement in business conditions on improved for the first time in 16 months. Firms reported the previous month, while readings below 50.0 show a that competition among suppliers had been behind deterioration. -

Tanzania Financial Inclusion Products National Risk Assessment Report

The United Republic of Tanzania Ministry of Finance and Planning NATIONAL MONEY LAUNDERING AND TERRORIST FINANCING RISK ASSESSMENT FINANCIAL INCLUSION PRODUCTS RISK ASSESSMENT REPORT DECEMBER 2016 0 TABLE OF CONTENTS TABLE OF CONTENTS ...................................................................................................................................... I DECLARATION ................................................................................................................................................... II ACRONYMS ....................................................................................................................................................... III EXECUTIVE SUMMARY ................................................................................................................................... VI 1. INTRODUCTION ......................................................................................................................................... 1 1.1. BACKGROUND .............................................................................................................................................. 1 1.2. WHAT IS FINANCIAL INCLUSION? ................................................................................................................. 1 1.3. OBJECTIVES OF PRODUCTS RISK ASSESSMENT IN FINANCIAL INCLUSION ................................................ 2 1.4. TANZANIA FINANCIAL SECTOR LANDSCAPE ...............................................................................................