Missouri Public Service Commission Case No. Wr-2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

E-Mail: [email protected] State Bar No. 12293 October

500 LEE STREET EAST SUITE I600 * t?O. BOX 553 * CHARLESTON, WEST VIRGINIA 25322 TELEPHONE: 304-340- IO00 * TELECOPIER: 304-340-1 I30 ~.jac~son~e~~~coi~ DIRECT TELEPHONE: (304) 340-1008 DIRECT TELECOPIER: (304) 340-1 080 E-Mail: [email protected] State Bar No. 12293 October 12,2018 VIA HAND DELIVERY Confidential Materials Enclosed Ingrid Ferrell, Executive Secretary Public Service Commission of WV 201 Brooks Street Charleston, West Virginia 25323 Re: West Virginia-American Water Company 201 8 Consolidated Water and Wastewater Rate Filings Case Nos. 18-0573-W-42T and 18-0576-8-42T Dear Ms. Ferrell: Enclosed are an original and twelve copies of the rebuttal testimony of the following witnesses on behalf of the Company: Brian K. Bruce, Rod P. Nevirauskas, Christina Chard, Jamie D. Hawn, Gregory P. Roach, Carolyn Mount, John R. Cox, John R. Wilde, Ann E. Bulkley, and Patrick L. Baryenbruch. Ms. Hawn’s testimony contains two confidential exhibits (Exhibits JDH-2 and JDH-5), which have been provided under seal. We have also included public redacted versions of these exhibits. Please file this testimony and circulate the additional copies to the appropriate parties at the Commission. Please also date stamp the extra copies provided and return them with our messenger. As always, we appreciate your assistance. Sincerely yours, Nicklaus A. Presley NAP/mrv Enclosures Rob Passrnore Ralph Clark John Auville Andrew Gunnoe Chris Howard Mandi Kay Carter Jackie Roberts Ann E. Bulkley Torn White Patrick L. Baryenbruch 4850-800 1-9576.vI BridgepotxWV Charlescon,W 8 Marunrburg WV * Morgantown WV *Wheeltng.WV Denver. -

We Keep Life Flowing

WE KEEP LIFE FLOWING amwater.com 1025 Laurel Oak Road | Voorhees, NJ 08043 “American Water” and the star logo are the registered trademarks of American Water Works Company, Inc. All rights reserved. 2018 PROXY STATEMENT AMERICAN WATER WORKS COMPANY, INC. March 27, 2018 Dear American Water Stockholder: I am pleased to invite you to attend American Water’s Annual Meeting of Stockholders on May 11, 2018. This year’s proxy statement provides you with information on three important subject matters: namely, the annual meeting, our executive compensation program and our commitment to sound corporate governance. We have expanded our corporate governance disclosures compared to previous years to include our commitment and actions in environmental, social and governance, which we consider to be both a strength and differentiator for American Water. We continue to simplify and improve the readability of our proxy statement. As we did last year, we have included an executive summary highlighting our operating results for 2017, as well as important operational and financial information that is included elsewhere in the proxy statement. We have also continued to present information more clearly by using bulleted lists, tables and graphics, shorter sentences and a “plain English” writing style throughout. We have also reduced or eliminated duplicative or unnecessary information where possible. The Board and I believe that these efforts reflect our ongoing commitment to making the proxy statement’s information easier to read and understand. As part of our strong commitment to our investors, our Board along with management have continued constructive and open dialogue with our investors. To this end, in 2017, in addition to over 260 visits with investors by senior management, we received increased input from our stockholders on key corporate governance and executive compensation topics important to them. -

Indiana-American Water Company, Inc. Iurc Cause No

INDIANA-AMERICAN WATER COMPANY, INC. IURC CAUSE NO. 45142 DIRECT TESTIMONY OF ANN E. BULKLEY SPONSORING ATTACHMENTS AEB-1 THROUGH AEB-13 DIRECT TESTIMONY OF ANN E. BULKLEY CAUSE NO. 45142 1 I. BACKGROUND 2 Q. Please state your name, affiliation, and business address. 3 A. My name is Ann E. Bulkley. I am employed by Concentric Energy Advisors, Inc. 4 (“Concentric”) as a Senior Vice President. My business address is 293 Boston Post Road 5 West, Suite 500, Marlborough, Massachusetts 01752. 6 Q. On whose behalf are you submitting this testimony? 7 A. I am submitting this testimony on behalf of Indiana-American Water Company (“IAWC” 8 or the “Company”), a wholly-owned subsidiary of American Water Works Company Inc. 9 (“AWK”). 10 Q. Please describe your background and professional experience in the energy and 11 utility industries. 12 A. I hold a Bachelor’s degree in Economics and Finance from Simmons College and a 13 Master’s degree in Economics from Boston University, with more than 20 years of 14 experience consulting to the energy industry. I have advised numerous energy and utility 15 clients on a wide range of financial and economic issues with primary concentrations in 16 valuation and utility rate matters. Many of these assignments have included the 17 determination of the cost of capital for valuation and ratemaking purposes. My 18 qualifications and testimony listing are presented in more detail in Appendix A. Bulkley - 1 1 Q. Please describe Concentric’s activities in energy and utility engagements. 2 A. Concentric provides financial and economic advisory services to many and various 3 energy and utility clients across North America. -

WE KEEP LIFE FLOWING 2017 Annual Repo Rt

WE KEEP LIFE FLOWING 2017 Annual Repo rt 2017 ANNUAL REPORT DEAR FELLOW STOCKHOLDER, Creating value for customers, communities, employees and stockholders is a driving force at American Water. This is reflected in the positive results that the company delivered in 2017. American Water’s 2017 financial performance, detailed in this report, gives the Board confidence that the company is well-positioned to achieve its stated target of a 7 to 10% long-term diluted earnings per share (EPS) compound annual growth rate. Additionally, in recognition of this financial performance, our Board increased the quarterly dividend by 10.7% in the second quarter of 2017, from 37.5 cents to 41.5 cents per share. This is consistent with our goal to achieve our target payout ratio in a range of 50 to 60%. As an owner of American Water, you enjoyed a total shareholder return (TSR) of 29% during 2017—well above the total shareholder return for the S&P 500 Index, which for 2017 was 21.8%. These results are an outcome of the sound execution by American Water employees of our business strategy, which allowed the company to continue to provide safe, clean, reliable and affordable water and wastewater services. By focusing on customers, communities, employee development and environmental leadership, American Water has established a pathway to sustainable and profitable growth. On behalf of American Water and the Board, we want to thank you for your continued support and investment. We look forward to seeing you at our Annual Meeting of Stockholders on May 11. Sincerely, George MacKenzie Chairman of the Board AMERICAN WATER 2017 ANNUAL REPORT 1 DEAR FELLOW STOCKHOLDER, American Water is pleased to provide you another year of strong financial performance. -

Volume 21 Pennsylvania-American Water Company 2020 General Base Rate Case R-2020-3019369 (Water) R-2020-3019371 (Wastewater)

VOLUME 21 PENNSYLVANIA-AMERICAN WATER COMPANY 2020 GENERAL BASE RATE CASE R-2020-3019369 (WATER) R-2020-3019371 (WASTEWATER) DIRECT TESTIMONY AND EXHIBIT OF ANN E. BULKLEY STATEMENT NO. 13 EXHIBIT NO. 13-A PAWC Statement No. 13 PENNSYLVANIA-AMERICAN WATER COMPANY Direct Testimony of Ann E. Bulkley, Senior Vice President Concentric Energy Advisors, Inc. Concerning Fair Rate of Return and Capital Structure Docket Nos. R-2020-3019369 (Water) R-2020-3019371 (Wastewater) Date April 29, 2020 Direct Testimony of Ann E. Bulkley Table of Contents Page No. I. WITNESS IDENTIFICATION AND QUALIFICATIONS ...................................................... 1 II. PURPOSE AND OVERVIEW OF TESTIMONY ................................................................. 2 III. REGULATORY PRINCIPLES ............................................................................................. 7 IV. CAPITAL MARKET CONDITIONS ................................................................................... 10 A. CURRENT MARKET CONDITIONS ...................................................................................... 11 B. THE EFFECT OF MARKET CONDITIONS ON VALUATIONS .............................................. 18 C. EFFECT OF TAX REFORM ON THE ROE AND CAPITAL STRUCTURE ............................ 29 V. PROXY GROUP SELECTION .......................................................................................... 37 VI. COST OF EQUITY ESTIMATION ..................................................................................... 44 A. IMPORTANCE -

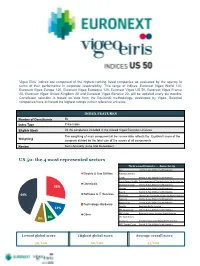

US 50: the 4 Most Represented Sectors

Vigeo Eiris’ indices are composed of the highest-ranking listed companies as evaluated by the agency in terms of their performance in corporate responsibility. This range of indices: Euronext Vigeo World 120, Euronext Vigeo Europe 120, Euronext Vigeo Eurozone 120, Euronext Vigeo US 50, Euronext Vigeo France 20, Euronext Vigeo United Kingdom 20 and Euronext Vigeo Benelux 20, will be updated every six months. Constituent selection is based on data from the Equitics® methodology, developed by Vigeo. Selected companies have achieved the highest ratings in their reference universe. INDEX FEATURES Number of Constituents 50 Index Type Price Index Eligible Stock All the companies included in the related Vigeo Euronext Universe The weighting of each component at the review date reflects the Equitics® score of the Weighting company divided by the total sum of the scores of all components Review Semi-Annually (June and December) US 50: the 4 most represented sectors New constituents – June 2019 AES Electric & Gas Utilities North America Electric & Gas Utilities American Electric Power Electric & Gas Utilities North America Bristol Myers Squibb Pharmaceuticals & Biotechnology North America Chemicals Dominion Energy Electric & Gas Utilities North America 28% Entergy Electric & Gas Utilities North America Exelon Electric & Gas Utilities North America Software & IT Services 44% Medtronic Health Care Equipment & Services North America NiSource Electric & Gas Utilities North America NRG Energy Electric & Gas Utilities North America Technology-Hardware -

American Water Works Company Inc. 2016 Annual Report

THE CYCLE OF SUCCESS 2016 Annual Repo rt 2016 ANNUAL REPORT 2015 ANNUAL REPORT 2016 ANNUAL REPORT • THE CYCLE OF SUCCESS DEAR FELLOW STOCKHOLDER, DEAR FELLOW STOCKHOLDER, American Water and its 6,800 employees delivered another year of strong financial performance, as detailed in this annual report, which gives the board confidence that the company is well positioned to achieve its stated target of 7 to 10 percent compound annual growth rate in diluted earnings per share (EPS) growth, anchored off 2015 EPS. In recognition of this financial performance, during 2016 our board continued its long-standing commitment to the company’s dividend, and increased the quarterly cash dividend payment from 34 cents to 37.5 cents per share, an increase of approximately 10 percent. The company has increased its dividend every year since its initial public offering in April 2008, and this is our fourth consecutive year of dividend increases of about 10 percent. This dividend is also consistent with our stated target payout ratio of 50 to 60 percent. As an owner of American Water, you enjoyed a total shareholder return (TSR) of 23.6 percent during 2016 — well above the total shareholder return for the S&P 500 Index, which for 2016 was 12 percent. These results stem from the successful execution of American Water’s business strategy, which allowed the company to continue to provide safe, clean, reliable and affordable water and wastewater services. Through a concentrated focus on engaged employees, smart investments, safe and efficient operations, and highly satisfied customers, American Water has a pathway to sustainable and profitable growth. -

Surrebuttal Testimony of Charles R. Hyneman

Exhibit No.: _______________ Issue(s): Environmental Cost Adjustment Mechanism (ECAM)// Tank Painting// Accrual Accounting and Rate Case Matching Principle// Service Company Labor Expense Adjustment// Service Company “Reasonableness Test”// Short-Term Incentive Compensation (“AIP”)// Long-Term Incentive Compensation (“LTIP”)// Income Tax Expense/Normalization Violation// General Ratemaking Principles// Atrazine Settlement// Pension Trackers// Insurance Other Than Group Witness/Type of Exhibit : Hyneman/Surrebuttal Sponsoring Party : Public Counsel Case No .: WR-2015-0301 SURREBUTTAL TESTIMONY OF CHARLES R. HYNEMAN Submitted on Behalf of the Office of the Public Counsel MISSOURI-AMERICAN WATER COMPANY CASE NO. WR-2015-0301 March 4, 2016 TABLE OF CONTENTS Testimony Page Introduction 1 Environmental Cost Adjustment Mechanism (ECAM) 1 Tank Painting 17 Accrual Accounting and Rate Case Matching Principle 21 Service Company Labor Expense Adjustment 24 Service Company “Reasonableness Test” 25 Short-Term Incentive Compensation (“AIP”) 31 Long-Term Incentive Compensation (“LTIP”) 37 Income Tax Expense/Normalization Violation 42 General Ratemaking Principles 49 Atrazine Settlement 52 Rate Case Expense 53 Pension Trackers 55 Insurance Other Than Group 57 SURREBUTTAL TESTIMONY OF CHARLES HYNEMAN MISSOURI-AMERICAN WATER COMPANY CASE NO. WR-2015-0301 1 I. INTRODUCTION 2 Q. Please state your name, title and business address. 3 A. Charles R. Hyneman, Chief Public Utility Accountant, Office of the Public Counsel (“OPC” 4 or “Public Counsel”), P.O. Box 2230, Jefferson City, Missouri 65102 . 5 Q. Are you the same Charles Hyneman who filed direct and rebuttal testimonies in WR- 6 2015-0301? 7 A. I am. 8 Q. What is the purpose of your rebuttal testimony? 9 A. The purpose of this rebuttal testimony is to provide the OPC response to the February 11, 10 2016 revenue requirement rebuttal testimonies of Missouri Public Service Commission 11 (“Commission”) Staff and Missouri American Water Company (“MAWC”) witnesses 12 regarding certain issues. -

August 24, 2018 INDIANA UTILITY REGULATORY COMMISSION

STATE OF INDIANA INDIANA UTILITY REGULATORY COMMISSION IN THE MATTER OF THE INDIANA UTILITY ) REGULATORY COMMISSION'S ) INVESTIGATION INTO THE IMPACTS OF ) THE TAX CUTS AND JOBS ACT OF 2017 AND ) CAUSE NO. 45032 S4 POSSIBLE RATE IMPLICATIONS UNDER ) PHASE 2 FOR INDIANA AMERICAN WATER ) COMP ANY, INC. TESTIMONY OF RALPH C. SMITH - PUBLIC'S EXHIBIT NO. 2 ON BEHALF OF THE INDIANA OFFICE OF UTILITY CONSUMER COUNSELOR August 24, 2018 Respectfully Submitted, .. "' . - CERTIFICATE OF SERVICE This is to certify that a copy of the foregoing Office of Utility Consumer Counselor Testimony of Ralph C. Smith has been served upon the following counsel of record in the captioned proceeding by electronic service on August 24, 2018. Hillary J. Close Todd A. Richardson Lauren M. Box Aaron A. Schmoll BARNES & THORNBURG LLP Joseph P. Rompala 11 South Meridian Street LEWIS & KAPPES, P.C. Indianapolis, Indiana 46204 One American Square, Suite 2500 Email: [email protected] Indianapolis, JN 46282 [email protected] Email: [email protected] [email protected] [email protected] Nikki G. Shoultz Comtesy copy to: Kristina Kern Wheeler A [email protected] J. Clu·istopher Janak [email protected] BOSE MCKINNEY & EVANS LLP 111 Monument Circle, #2700 Robert M. Glennon Indianapolis, Indiana 46204 3697 N. County Road 500 E. Email: [email protected] Danville, Indiana 46122 [email protected] Email: [email protected] [email protected] Courtesy Copy to: Jennifer Washburn Margo Tucker CITIZENS ACTION COALITION 1915 West 18, Street, Suite C Indianapolis, Indiana 46202 Email: [email protected] [email protected] INDIANA OFFICE OF UTILITY CONSUMER COUNSELOR 115 West Washington Street Suite 1500 South Indianapolis, JN 46204 [email protected] 317/232-2494-Phone 317/232-5923 - Facsimile Public's Exhibit No. -

Market Commentary Third Quarter 2020

Market Commentary Third Quarter 2020 REVIEW AND OUTLOOK Performance as of 9/30/20 Q3 2020 YTD 2020 Reaves LTV Wrap Composite1, gross of fees 8.70% -2.38% Reaves LTV Wrap Composite1, net of fees 8.04% -4.20% S&P 500 Index2 8.93% 5.57% Russell 1000 Value Index3 5.59% -11.58% INTRODUCTION Reaves’ LTV Strategy Wrap Composite returned 8.7% in the third quarter of 2020, improving the year-to-date return to -2.4%. Excluding any de minimus positions, all segments of the compos- ite were positive in the quarter, led by railroads, cable broadband, and utilities focused on renewable energy development. This last group is something we focus on in more detail below. ENERGY TRANSITION Energy transition has been a primary driver of utility sector performance over the past 18 months. The performance of utilities actively developing renewable generation, and those with small carbon footprints, have diverged markedly from those that generate a significant portion of profits from fossil fuels related activity. This dispersion is as wide as it has ever been. As part of our research process, we track two groups of utilities companies: the first group contains low carbon renewable energy utilities and the second group has fossil fuel utilities. On average, over the last eighteen months, the companies in the low carbon group have outperformed the fossil fuel group by about 60%.4 As the cost of renewable energy continues to decline, we believe the next couple of decades will see accelerating growth. Additionally, there is increasing global policy support. -

Vanguard Russell 1000 Index Funds Annual Report August 31, 2020

Annual Report | August 31, 2020 Vanguard Russell 1000 Index Funds Vanguard Russell 1000 Index Fund Vanguard Russell 1000 Value Index Fund Vanguard Russell 1000 Growth Index Fund See the inside front cover for important information about access to your fund’s annual and semiannual shareholder reports. Important information about access to shareholder reports Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your fund’s annual and semiannual shareholder reports will no longer be sent to you by mail, unless you specifically request them. Instead, you will be notified by mail each time a report is posted on the website and will be provided with a link to access the report. If you have already elected to receive shareholder reports electronically, you will not be affected by this change and do not need to take any action. You may elect to receive shareholder reports and other communications from the fund electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you invest directly with the fund, by calling Vanguard at one of the phone numbers on the back cover of this report or by logging on to vanguard.com. You may elect to receive paper copies of all future shareholder reports free of charge. If you invest through a financial intermediary, you can contact the intermediary to request that you continue to receive paper copies. If you invest directly with the fund, you can call Vanguard at one of the phone numbers on the back cover of this report or log on to vanguard.com. -

2021 Annual Report

MARCH 31, 2021 2021 Annual Report iShares Trust • iShares Russell Top 200 ETF | IWL | NYSE Arca • iShares Russell Top 200 Growth ETF | IWY | NYSE Arca • iShares Russell Top 200 Value ETF | IWX | NYSE Arca • iShares Russell 1000 ETF | IWB | NYSE Arca • iShares Russell 1000 Growth ETF | IWF | NYSE Arca • iShares Russell 1000 Value ETF | IWD | NYSE Arca • iShares Russell 2000 ETF | IWM | NYSE Arca • iShares Russell 2000 Growth ETF | IWO | NYSE Arca • iShares Russell 2000 Value ETF | IWN | NYSE Arca The Markets in Review Dear Shareholder, The 12-month reporting period as of March 31, 2021 reflected a remarkable period of disruption and adaptation, as the global economy dealt with the implications of the coronavirus (or “COVID-19”) pandemic. As the period began, the response to the virus’s spread was well underway, and countries around the world instituted economically disruptive countermeasures. Stay-at-home orders and closures of non-essential businesses became widespread, many workers were laid off, and unemployment claims spiked, causing a global recession and a sharp fall in equity prices. As April 2020 began, stocks were near their lowest point since the beginning of the pandemic. However, a steady recovery began, as businesses started re-opening and governments learned to adapt to life with the virus. Equity prices continued to rise throughout the summer, fed by strong fiscal and monetary Rob Kapito support and improving economic indicators. Many equity indices neared or surpassed all-time highs late President, BlackRock, Inc. in the reporting period following the implementation of mass vaccination campaigns and passage of an additional $1.9 trillion of fiscal stimulus.