Deathcare Accounting

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

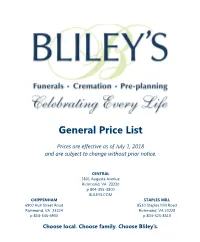

General Price List

General Price List Prices are effective as of July 1, 2018 and are subject to change without prior notice. CENTRAL 3801 Augusta Avenue Richmond, VA 23230 p 804-355-3800 BLILEYS.COM CHIPPENHAM STAPLES MILL 6900 Hull Street Road 8510 Staples Mill Road Richmond, VA 23224 Richmond, VA 23228 p 804-545-6900 p 804-523-8510 Choose local. Choose family. Choose Bliley’s. You have many choices of firms to Please feel free to contact any one of care for you and your family here in our Associates or myself with any Richmond and we are grateful that questions or you have chosen Bliley’s. We hope needs that that the information provided in this you have. booklet will help you in selecting the Sincerely, service and/or ceremony that best honors the life of your loved one. M. Carey Bliley President Our firm has been a part of the Richmond community since 1874, and we take great pride in being the TABLE OF CONTENTS city’s most preferred provider of What Makes Us Unique 2 Funeral and Cremation Services. We Why Should Bliley’s understand that experiencing a loss, Assist With Your Ceremony? 3-4 is a very difficult and emotional time Reception and Catering 5-6 for you and your family. Know that Standards of Excellence 7 we are here to support you and help All About Cremation 8 guide you through this time with complete professionalism, care, and General Price List 9-15 compassion – attributes our firm has Our Commitment To You 17 always been known for. -

The Sociological Functions of Funeral Mourning: Illustrations from the Old Testament and Africa

Ademiluka: Functions of Funeral Mourning OTE 22/1 (2009), 9-20 9 The Sociological Functions of Funeral Mourning: Illustrations from the Old Testament and Africa S. O. ADEMILUKA (KOGI STATE UNIVERSITY, NIGERIA) ABSTRACT Funeral mourning is an essential rite of passage in many societies. While there are differences among those aspects peculiar to each culture, there are certain motifs common to mourning in all cultures. Among such common motifs are the sociological functions which in most cultures are served by funeral mourning rituals. Hence this study examines the sociological functions that funeral mourning serves in the Old Testament and in Africa. The fact that mourning serves certain functions in the society has an implication for theology in Africa. A INTRODUCTION In the Old Testament, as in Africa, death is accorded the most important significance in the midst of other rites of passage. Hence death is mourned with varied activities. In both contexts mourning involves various elements, such as the number of days set aside for it, abstention from certain engagements, self- abasement, the dirge, and etcetera. In both contexts funeral mourning also serves certain sociological functions. For example, in Africa it serves the purpose of the preservation of cultural heritage. However, in Africa, several aspects of this tradition are dying out, giving way to Christianity and Western civilisation. The aim of this article therefore is not to compare funeral mourning in the Old Testament with what is happening in Africa but to identify the various aspects of mourning in both cultural contexts with a view to ascertaining the sociological functions they serve. -

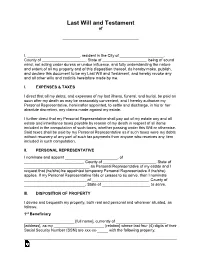

Last-Will-And-Testament-Template.Pdf

Last Will and Testament of ___________________________________ I, ________________________, resident in the City of ____________________, County of ____________________, State of ____________________, being of sound mind, not acting under duress or undue influence, and fully understanding the nature and extent of all my property and of this disposition thereof, do hereby make, publish, and declare this document to be my Last Will and Testament, and hereby revoke any and all other wills and codicils heretofore made by me. I. EXPENSES & TAXES I direct that all my debts, and expenses of my last illness, funeral, and burial, be paid as soon after my death as may be reasonably convenient, and I hereby authorize my Personal Representative, hereinafter appointed, to settle and discharge, in his or her absolute discretion, any claims made against my estate. I further direct that my Personal Representative shall pay out of my estate any and all estate and inheritance taxes payable by reason of my death in respect of all items included in the computation of such taxes, whether passing under this Will or otherwise. Said taxes shall be paid by my Personal Representative as if such taxes were my debts without recovery of any part of such tax payments from anyone who receives any item included in such computation. II. PERSONAL REPRESENTATIVE I nominate and appoint ________________________, of ___________________________, County of ________________________, State of ______________________________ as Personal Representative of my estate and I request that (he/she) be appointed temporary Personal Representative if (he/she) applies. If my Personal Representative fails or ceases to so serve, then I nominate _____________________________of __________________________, County of ____________________________, State of ______________________ to serve. -

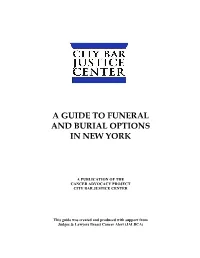

A Guide to Funeral and Burial Options in New York

A GUIDE TO FUNERAL AND BURIAL OPTIONS IN NEW YORK A PUBLICATION OF THE CANCER ADVOCACY PROJECT CITY BAR JUSTICE CENTER This guide was created and produced with support from Judges & Lawyers Breast Cancer Alert (JALBCA) © City Bar Justice Center (Updated 2019) CONTENTS Page INTRODUCTION ……………………………………………………………… 3 FUNERALS ……………………………………………………………………… 4 Consumer Rights and the Funeral Rule …………………….…………….. 4 New York State Funeral Home Rules ……………………………….…… 4 Making Funeral Arrangements in New York State ………………………. 5 Disposition of Remains ……………………………………………….…………. 6 FUNERAL AND BURIAL OPTIONS ……………………………….………… 7 Full Service Funeral ……………………………………….……………… 7 Direct Burial ……………………………………………….……………… 7 Environmentally Friendly/Green Burials ………………………………….. 7 Home Funerals and Burials ………………………………………………. 9 Cremation ………………………………………………………………… 10 PRE-NEED FUNERAL PLANNING ………………………………………….. 11 ORGAN AND TISSUE DONATION …………………………………………. 12 CEMETERIES ………………………………………………………………….. 13 FINANCIAL ASSISTANCE …………………………………………………… 14 SAMPLE FORM: APPOINTMENT OF AGENT TO CONTROL DISPOSITION OF REMAINS City Bar Justice Center A Guide to Funeral and Burial Options in New York 2 INTRODUCTION The City Bar Justice Center’s Cancer Advocacy Project provides cancer patients and survivors with no-cost legal information and advice. Experienced volunteer attorneys counsel clients on issues relating to life-planning, such as wills and advance directives, unjust treatment by insurance companies and discrimination in the workplace. Thoughts of end-of-life planning are often prompted by advancing age or a serious illness. While some people are able to prepare advance directives and organize a burial plan, others are understandably focused on the day-to-day challenges of combating ill health. Unfortunately, many people find themselves dealing with funeral arrangements as a matter of urgency, either on their own behalf, or on behalf of a loved one. Contemplating where to start can seem overwhelming. -

Prepaid Funeral Contracts

Prepaid Funeral Contracts A prepaid funeral contract is a legal agreement which requires payment in advance for funeral services, cemetery services or merchandise and the physical delivery and retention of which would occur after death. You can pay for the contract outright, through an insurance policy, or by an investment that you own. A prepaid funeral contract can be funded by a trust or by insurance. The seller may offer one or both of the following funding types: n For a trust-funded prepaid funeral contract where payments are placed in an approved interest- bearing restricted bank account or formal trust account to pay for the future cost of the selected funeral goods and services. Payments on the contract are made to the seller. n For an insurance-funded prepaid funeral contract where payments are used to purchase an insurance policy or annuity to pay for the future cost of the selected funeral goods and services. Payments are not made to the seller but to the insurance company that is funding the contract. Financial Education Before purchasing a prepaid funeral contract, you should: n Find out if the funeral home is properly licensed, has a good reputation, and is financially stable. Not all funeral homes have a license to sell prepaid contracts. Ask family and friends for a recommendation. Shop around and interview several funeral homes. To verify a funeral home or funeral director’s license, and to check for disciplinary action, you may contact the Corporations, Securities, and Commercial Licensing Bureau at: 517-241-9288. n Be prepared. When you visit or call a funeral home, the personnel may try to sell you a contract. -

Funeral Rites Across Different Cultures

section nine critical incident FUNERAL RITES ACROSS DIFFERENT CULTURES Responses to death and the rituals and beliefs surrounding it tend to vary widely across the world. In all societies, however, the issue of death brings into focus certain fundamental cultural values. The various rituals and ceremonies that are performed are primarily concerned with the explanation, validation and integration of a peoples’ view of the world. In this section, the significance of various symbolic forms of behaviour and practices associated with death are examined before going on to describe the richness and variety of funeral rituals performed according to the tenets of some of the major religions of the world. THE SYMBOLS OF DEATH Social scientists have noted that of all the rites of passage, death is most strongly associated with symbols that express the core life values sacred to a society. Some of the uniformities underlying funeral practices and the symbolic representations of death and mourning in different cultures are examined below: THE SIGNIFICANCE OF COLOUR When viewed from a cross-cultural perspective, colour has been used almost universally to symbolise both the grief and trauma related to death as well as the notion of ‘eternal life’ and ‘vitality’. Black, with its traditional association with gloom and darkness, has been the customary colour of mourning for men and women in Britain since the fourteenth century. However, it is important to note that though there is widespread use of black to represent death, it is not the universal colour of mourning; neither has it always provided the funeral hue even in Western societies. -

Cultural Guidelines for Working with Families Who Have Experienced Sudden and Unexpected Death

CULTURAL GUIDELINES FOR WORKING WITH FAMILIES WHO HAVE EXPERIENCED SUDDEN AND UNEXPECTED DEATH Culture includes the beliefs, customs, and arts of a particular society, group, or place. How people respond to issues of death or dying is directly related to their cultural backgrounds. Anyone who works with families should be sensitive to their culture, ethnic, religious, and language diversity. This tip guide provides practical cultural guidelines for working with families who have experienced sudden and unexpected death. CULTURE GUIDE INTRODUCTION Contents Cultural Beliefs about Family and Loss........ 4 African American.......................... 5 Amish ................................... 6 Arab American............................ 7 Asian American ........................... 8 Bosnian American . 9 European American.......................10 Hispanic or Latino........................11 Micronesian American ....................12 Native American .........................13 Somali American .........................14 Religious Beliefs about Death and Loss ......15 Buddhism ...............................16 Christianity .............................17 Hinduism ...............................18 Islam ...................................19 Jehovah’s Witness ........................20 Judiasm.................................21 Mormonism .............................22 Santeria.................................23 Additional Resources ...................24 This guide was developed by: The Missouri Department of Mental Health dmh.mo.gov Disaster and -

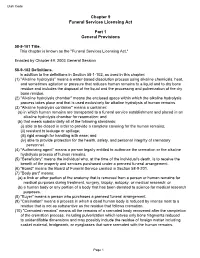

Chapter 9 Funeral Services Licensing Act Part 1 General Provisions

Utah Code Chapter 9 Funeral Services Licensing Act Part 1 General Provisions 58-9-101 Title. This chapter is known as the "Funeral Services Licensing Act." Enacted by Chapter 49, 2003 General Session 58-9-102 Definitions. In addition to the definitions in Section 58-1-102, as used in this chapter: (1) "Alkaline hydrolysis" means a water-based dissolution process using alkaline chemicals, heat, and sometimes agitation or pressure that reduces human remains to a liquid and to dry bone residue and includes the disposal of the liquid and the processing and pulverization of the dry bone residue. (2) "Alkaline hydrolysis chamber" means the enclosed space within which the alkaline hydrolysis process takes place and that is used exclusively for alkaline hydrolysis of human remains. (3) "Alkaline hydrolysis container" means a container: (a) in which human remains are transported to a funeral service establishment and placed in an alkaline hydrolysis chamber for resomation; and (b) that meets substantially all of the following standards: (i) able to be closed in order to provide a complete covering for the human remains; (ii) resistant to leakage or spillage; (iii) rigid enough for handling with ease; and (iv) able to provide protection for the health, safety, and personal integrity of crematory personnel. (4) "Authorizing agent" means a person legally entitled to authorize the cremation or the alkaline hydrolysis process of human remains. (5) "Beneficiary" means the individual who, at the time of the individual's death, is to receive the benefit of the property and services purchased under a preneed funeral arrangement. (6) "Board" means the Board of Funeral Service created in Section 58-9-201. -

Symbols in the Funeral Mass

Symbols in the Funeral Mass Many of the symbols used during the funeral liturgy reflect the sacrament of Baptism – it is through Baptism that our loved one has already shared Christ’s death and resurrection. At the Funeral Mass we offer worship, praise and thanksgiving to God, we are strengthened by our belief in the resurrection and find strength and consolation through our faith in God. The Reception of the Deceased at the entrance to the church is a reminder that the church is the home of all Christians. At Baptism, we were received at the same door and the sprinkling of holy water at this time reminds us of the person's Baptism and initiation into the community of faith. The Placing of the Pall on the casket serves to remind us of the white garment received at Baptism. The Paschal Candle reminds us of Christ, the Light of the World, His victory over sin and death and of our share in that victory by virtue of our baptism. The Paschal candle reminds us of the Easter vigil, the night when we await the Lord's resurrection and when new light for the living and the dead is kindled. Incense is used during the final commendation at the Funeral Mass as a sign of honor to the body of the deceased, which through baptism became the temple of the Holy Spirit. It is also a sign of our prayers for the deceased rising to our Lord and as a symbol of farewell. The Cross that is usually placed in or on the casket is a reminder that we, as Christians, were marked with the cross in baptism and through Jesus' suffering on the cross, we are brought to his resurrection. -

Filing of Last Wills and Burial Instructions

DIOCESE OF MARQUETTE FILING OF LAST WILLS AND BURIAL INSTRUCTIONS There comes a time when all of us must depart this life, a time when we are called home by our Merciful Father. As our Lord Jesus said, “no one knows the time or the day”. In order that funeral arrangements can be made with convenience for all involved and in accordance with the desires of the priest who dies, it is requested that a Will and/or a Letter of Instructions be on file in the Chancery. Please note that the Last Will and a document of funeral and burial instructions are two different items. It cannot be overemphasized how important it is to have these documents on file. Having them on file alleviates many problems during a very stressful and difficult time for the family and those charged with planning the funeral. 1) WILLS Your Last Will or Testament is a legal declaration of how you wish to dispose of your property after death. It has no force or effect until after the death of the testator and can be canceled or modified at any time before death. Some reminders regarding priests' Wills: A. Your Will should be prepared by an attorney practicing law in the State of Michigan to ensure its validity. B. Authentic, signed Wills should not be kept in safe-deposit boxes. C. Provisions should be made for proper disposition of sacred vessels and other consecrated or sacred objects. D. A Will should not contain burial instructions. E. Photocopies of a signed Will have no legal force. -

Funeral Assistance

Coronavirus (COVID-19) Funeral Assistance The COVID-19 pandemic has brought To be eligible for funeral assistance, you must meet overwhelming grief to many families. At FEMA, these conditions: our mission is to help people before, during and • The death must have occurred in the United States. after disasters. We are dedicated to helping • The applicant must be a U.S. citizen, non-citizen ease some of the financial stress and burden national or qualified alien who incurred funeral caused by the virus. expenses after January 20, 2020. • There is no requirement for the deceased person FEMA is providing financial assistance for to have been a U.S. citizen, non-citizen national or COVID-19-related funeral expenses incurred after qualified alien. January 20, 2020. • The deceased person’s death certificate must indicate the death was attributed to or caused by COVID-19. If a death occurred between Jan. 20 and May 16, 2020, and the death certificate doesn’t attribute the death to COVID-19, include a signed statement from the death certificate’s certifying official, local coroner or medical examiner that links the cause of death to COVID-19. Which expenses will qualify for reimbursement? Examples of eligible expenses may include, but not limited to: • Transportation to identify the deceased • A marker or headstone individual • Clergy or officiant services • The transfer of remains • The use of funeral home equipment or staff • A burial plot or cremation niche • Cremation or interment costs What information do I need to provide to FEMA? Please have the following information before contacting FEMA to apply: • Name, social security number, date of birth, mailing address and contact phone numbers. -

Last Will & Testament: Add a Letter Covering These 14 Wishes

Last Will & Testament: Add a Letter Covering These 14 Wishes Potomac Financial Private Client Group, LLC 6723 Whittier Avenue, Suite 305 McLean, VA 22101 703-891-9960 [email protected] www.potomacfinancialpcg.com By Richard Atkinson Having a will is necessary, but there is a great deal of information the legal document does not include. Here’s what to cover in a supplemental letter that specifies preferences, discloses critical logistic info, and will save your family significant stress during a difficult time. You might be surprised how many people die each usually not included in the will. Here are several year without a will. There are numerous reasons suggestions you may consider including in your or for this major oversight, including those who your loved one’s accompanying letter: cannot or will not think about death, those who believe talking about and creating a will may cause problems with their partner or family members, 1. People to be notified at the time of death. and those who don’t want to spend money on Certain people and institutions need to be lawyers. notified at time of death, including your lawyer, executor, trustee, and accountant, along with Having a proper will goes a long way to prevent federal pension authorities. Relatives and family arguments. The guesswork is eliminated and special friends will want to know as soon as the family is clear on your intentions. Furthermore, possible, so providing the names, addresses, a will may actually save money, because without and telephone numbers will make it easier for one, the provincial/state authorities are in control, the person assuming this responsibility.