Taxation in the Cyber Age: the Future of Wayfair

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chfh Partners Wayfair.Pdf

Send a release Search Advanced Search Become a member Member sign in Products & Services News Releases For journalists For bloggers Global sites Products & Services Knowledge Center Browse News Releases Contact PR Newswire See more news releases in Furniture and Furnishings | Home Improvement | Construction & Building | Corporate Social Responsibility Wayfair.com Partners with New Jersey Habitat for Humanity Affiliates to Assist Communities Devastated by Hurricane Sandy Donates $50,000 in Home Furnishings to Habitat ReStore Resale Outlets in Asbury Park and Toms River BOSTON, Feb. 14, 2013 /PRNewswire/ -- Wayfair.com, an online retailer of home furnishings, More by this Source today announced a donation to two New Jersey Habitat for Humanity affiliates to directly assist communities devastated by Hurricane Sandy. Earlier this month, Wayfair.com delivered more than Wayfair.com $50,000 worth of home furnishings and decor to Habitat ReStore resale outlets in coastal New Jersey. Funds from the sale of the Simplifies Shopping products at Coastal Habitat for Humanity ReStore in Asbury Park and Northern Ocean Habitat for Humanity ReStore in Toms River for Home will directly support disaster response efforts and home re-builds in the region. Apr 08, 2013, 13:48 ET (Logo: http://photos.prnewswire.com/prnh/20130206/NE55105LOGO ) Wayfair.com "We are delighted to contribute to the re-building efforts in coastal New Jersey where so many people are still in need of safe and Announces Executive affordable housing," said Niraj Shah , CEO and co-founder of Wayfair.com. "Wayfair.com strongly supports Habitat's mission and it Promotions is our hope that by donating home furnishings directly to Restores in the region, we will be able to help people get back on their Mar 25, 2013, 10:30 ET feet following Hurricane Sandy." Wayfair.com Coastal Habitat in Asbury Park and Northern Ocean Habitat in Toms River have been working to address both the short-term and Integrates Flash Deals long-term need for safe and decent housing in the New Jersey communities impacted by Hurricane Sandy. -

The Data Behind Netflix's Q3 Beat Earnings

The Data Behind Netflix’s Q3 Beat Earnings What Happened -- Earnings per share: $1.47 vs. $1.04 expected -- International paid subscriber additions: 6.26 million vs. 6.05 million expected -- Stock price surged more than 8% in extended trading Grow your mobile business 2 Apptopia’s data was a strong leading indicator of new growth -- Netflix increased new installs of its mobile app 8.4% YOY and 13.5% QOQ. -- New international installs of Netflix are up 11.3% YOY and 17.3% QOQ. -- New domestic installs of Netflix are down 3.6% YOY and 8.3% QOQ. Grow your mobile business 3 Other Indicators of Netflix’s Q3 2019 performance Netflix Domestic Growth YoY Netflix Global Growth YoY Q3 2018 - 19 Q3 2018 - 19 Netflix +6.4% Netflix +21.4% Reported: Paid Reported: Paid Subscribers Subscribers Apptopia +7.2% Apptopia +15.1% Estimate: Time Estimate: Time Spent In App Spent In App Apptopia +7.7% Apptopia +16% Estimate: Mobile Estimate: Mobile App Sessions App Sessions Grow your mobile business Other Indicators of Netflix’s Q3 2019 performance -- Netflix reported adding 517k domestic paid subscriber vs. 802k expected -- Its growth this quarter clearly came from international markets -- More specifically, according to Apptopia, it came from Vietnam, Indonesia, Saudi Arabia and Japan Grow your mobile business We’ve Got You Covered Coverage includes 10+ global stock exchanges and more than 3,000 tickers. Restaurants & Food Travel Internet & Media Retail CHIPOTLE MEXICAN CRACKER BARREL ALASKA AIR GROUP AMERICAN AIRLINES COMCAST DISH NETWORK ALIBABA GROUP AMBEST BUY -

Gerald Dingee, Et Al. V. Wayfair, Inc., Et Al. 15-CV-06941-First Amended

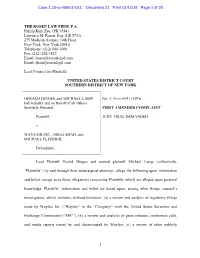

Case 1:15-cv-06941-DLC Document 21 Filed 01/11/16 Page 1 of 26 THE ROSEN LAW FIRM, P.A. Phillip Kim, Esq. (PK 9384) Laurence M. Rosen, Esq. (LR 5733) 275 Madison Avenue, 34th Floor New York, New York 10016 Telephone: (212) 686-1060 Fax: (212) 202-3827 Email: [email protected] Email: [email protected] Lead Counsel for Plaintiffs UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK GERALD DINGEE and MICHAEL LAMP No. 1:15-cv-6941 (TPG) Individually and on Behalf of all Others Similarly Situated, FIRST AMENDED COMPLAINT Plaintiff, JURY TRIAL DEMANDED v. WAYFAIR INC., NIRAJ SHAH, and MICHAEL FLEISHER, Defendants. Lead Plaintiff Gerald Dingee and named plaintiff Michael Lamp (collectively, “Plaintiffs”) by and through their undersigned attorneys, allege the following upon information and belief, except as to those allegations concerning Plaintiffs, which are alleged upon personal knowledge. Plaintiffs’ information and belief are based upon, among other things, counsel’s investigation, which includes, without limitation: (a) a review and analysis of regulatory filings made by Wayfair Inc. (“Wayfair” or the “Company”) with the United States Securities and Exchange Commission (“SEC”); (b) a review and analysis of press releases, conference calls, and media reports issued by and disseminated by Wayfair; (c) a review of other publicly 1 Case 1:15-cv-06941-DLC Document 21 Filed 01/11/16 Page 2 of 26 available information concerning Wayfair; (d) a review of public statements by Overstock.com, Inc. (“Overstock”); and (e) interviews with witnesses. Plaintiffs believe that further substantial evidentiary support will exist for the allegations set forth herein after a reasonable opportunity for discovery. -

Wayfair: Marketplaces and Foreign Vendors

Maurer School of Law: Indiana University Digital Repository @ Maurer Law Articles by Maurer Faculty Faculty Scholarship 2018 Wayfair: Marketplaces and Foreign Vendors David Gamage Indiana University Maurer School of Law, [email protected] Adam Thimmesch University of Nebraska - Lincoln Darien Shanske University of California, Davis Follow this and additional works at: https://www.repository.law.indiana.edu/facpub Part of the Taxation-Federal Commons, and the Taxation-State and Local Commons Recommended Citation Gamage, David; Thimmesch, Adam; and Shanske, Darien, "Wayfair: Marketplaces and Foreign Vendors" (2018). Articles by Maurer Faculty. 2722. https://www.repository.law.indiana.edu/facpub/2722 This Article is brought to you for free and open access by the Faculty Scholarship at Digital Repository @ Maurer Law. It has been accepted for inclusion in Articles by Maurer Faculty by an authorized administrator of Digital Repository @ Maurer Law. For more information, please contact [email protected]. ACADEMIC PERSPECTIVES ON SALT state tax notes® Wayfair: Marketplaces and Foreign Vendors by Adam Thimmesch, Darien Shanske, and David Gamage decision and to analyze key questions it has raised.2 In this article, we consider issues regarding marketplaces such as Amazon.com and eBay and foreign vendors. We conclude that state governments should apply their new nexus standards to the major marketplaces and should not let fears about in-state citizens shifting to purchasing from foreign vendors stand in the way of efforts to apply more inclusive nexus standards to out-of-state vendors. Marketplaces Adam Thimmesch is Wayfair is already ushering in a new regime a professor at the for interstate sales and use tax transactions University of Nebraska wherein state governments should be able to College of Law; Darien successfully tax most transactions between in- Shanske is a professor state citizens and out-of-state vendors. -

Wayfair: Its Implications and Missed Opportunities

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Washington University St. Louis: Open Scholarship Washington University Journal of Law & Policy Volume 58 Current Issues in State Tax Symposium 2019 Wayfair: Its Implications and Missed Opportunities Richard D. Pomp Alva P. Loiselle Professor of Law, University of Connecticut Law School Follow this and additional works at: https://openscholarship.wustl.edu/law_journal_law_policy Part of the Taxation-Federal Commons, Taxation-State and Local Commons, and the Tax Law Commons Recommended Citation Richard D. Pomp, Wayfair: Its Implications and Missed Opportunities, 58 WASH. U. J. L. & POL’Y 001 (2019), https://openscholarship.wustl.edu/law_journal_law_policy/vol58/iss1/7 This Article is brought to you for free and open access by the Law School at Washington University Open Scholarship. It has been accepted for inclusion in Washington University Journal of Law & Policy by an authorized administrator of Washington University Open Scholarship. For more information, please contact [email protected]. Wayfair: Its Implications and Missed Opportunities Professor Richard D. Pomp* INTRODUCTION This Article has its roots in a lone concurrence by Justice Kennedy in Direct Marketing Ass’n v. Brohl,1 a concurrence having nothing to do with the merits of that case. Nonetheless, that concurrence went viral, leading to the most important sales tax case in over a quarter-century: South Dakota v. Wayfair, Inc.2 Because of the cataclysmic impact of Kennedy’s concurrence and its preview of the issues in this Article, it is worth quoting at length: Almost half a century ago, this Court determined that, under its Commerce Clause jurisprudence, States cannot require a business to collect use taxes—which are the equivalent of sales taxes for out-of- state purchases—if the business does not have a physical presence in the State. -

Wayfair Brings Virtual Furnishings and Décor Into the Home with Wayfairview

NEWS RELEASE Wayfair Brings Virtual Furnishings and Décor into the Home with WayfairView 6/9/2016 Online Retailer Launches Smartphone Augmented Reality App, Available in Google Play with the World’s First Tango- Enabled Smartphone BOSTON--(BUSINESS WIRE)-- Wayfair Inc. (NYSE:W), one of the world's largest online destinations for home furnishings and décor, today announced the launch of WayfairView, the company’s rst-party smartphone augmented reality application, available in Google Play. Developed by Wayfair Next, the company’s in-house research and development team, using Google’s technology, WayfairView allows shoppers to visualize furniture and décor in their homes at full-scale before they make a purchase. Consumers will be able to shop with WayfairView on the upcoming Tango-enabled smartphone by Lenovo, the PHAB2 Pro, available this September. “Wayfair Next is laying the groundwork for new innovations that will change the face of retail – all with rst-party technology,” noted Steve Conine, co-chairman and co-founder, Wayfair. “By digitizing our vast catalog through 3-D scanning, we will dramatically improve the visualization of products to create the best possible shopping experience for our customers. With smartphone augmented reality, we can take this a step further. Built using Google’s robust Tango technology, WayfairView will allow shoppers to visualize furniture and décor in their homes by virtually placing real products from Wayfair’s extensive catalog in any room at full-scale.” To use WayfairView, shoppers will be able to view a particular room in their home through the lens of the Lenovo PHAB2 Pro, select a Wayfair product and virtually place that product in the room to see how it ts and looks within the space. -

Wayfair Invites Aspiring Entrepreneurs to Pitch Business Plans in Shark Tank-Like Competition at Heart Home Conference

NEWS RELEASE Wayfair Invites Aspiring Entrepreneurs to Pitch Business Plans in Shark Tank-like Competition at Heart Home Conference 9/2/2015 Judging Panel to Include Wayfair Co-Founder Steve Conine, Battery Ventures General Partner Neeraj Agrawal, Start- Up Institute CEO Diane Hessan and Innovation Journalist Scott Kirsner BOSTON--(BUSINESS WIRE)-- Wayfair (NYSE:W), one of the world’s largest online destinations for home furnishings and décor, today announced The Kitchen Cabinet – Can Your Business Concept Take the Heat?, a business competition for aspiring entrepreneurs in the home space. The Kitchen Cabinet competition will take place at Wayfair’s Heart Home conference on October 2 at the Boston Copley Marriott where entrepreneurs will share their business concepts and receive feedback and strategic advice from a panel of accomplished leaders in the innovation economy. The Kitchen Cabinet panel of advisors includes Wayfair Co-Founder Steve Conine, Battery Ventures General Partner Neeraj Agrawal, Start-Up Institute CEO Diane Hessan and innovation journalist Scott Kirsner. Heart Home attendees are invited to submit their business concepts by September 15, 2015 for the chance to present their business plans to The Kitchen Cabinet advisors. Finalists will have ve minutes to pitch their business concept followed by another ten minute session for questions from the panel of advisors as well as the audience. Judges will select a grand prize winner to be announced at the Heart Home conference party on Friday evening. One People’s Choice winner will also be selected via social media. The grand prize winner will receive a business consultation and a $2500 home oce makeover from Wayfair. -

Having Your Cake and Eating It: an Analysis of Concession-Abuse-As-A-Service

Having Your Cake and Eating It: An Analysis of Concession-Abuse-as-a-Service Zhibo Sun∗, Adam Oest∗, Penghui Zhang∗, Carlos Rubio-Medrano‡ Tiffany Bao∗, Ruoyu Wang∗, Ziming Zhao¶, Yan Shoshitaishvili∗, Adam Doupé∗, Gail-Joon Ahn ∗§ ∗Arizona State University, ‡Texas A&M University - Corpus Christi ¶Rochester Institute of Technology, §Samsung Research ∗{zhibo.sun, aoest, penghui.zhang, tbao, fishw, yans, doupe, gahn}@asu.edu ‡[email protected], ¶[email protected] Abstract companies in the difficult position of choosing between scam mitigation and the happiness of legitimate customers. Concession Abuse as a Service (CAaaS) is a growing scam A perception by vendors who fall victim to concession service in underground forums that defrauds online retailers abuse may be that these attacks are isolated incidents and through the systematic abuse of their return policies (via social can thus be resolved in an ad-hoc fashion. However, through engineering) and the exploitation of loopholes in company a comprehensive analysis of underground forums and a protocols. Timely detection of such scams is difficult as they concession abuse provider, we find that such attacks operate are fueled by an extensive suite of criminal services, such at scale, target merchants across multiple industry sectors, as credential theft, document forgery, and fake shipments. involve complex coordination between different underground Ultimately, the scam enables malicious actors to steal arbitrary actors, and overcome current industry best practices and goods from merchants with minimal investment. mitigations to reliably yield success for the criminals. In this paper, we perform in-depth manual and automated In this paper, we show that concession abuse is, in fact, analysis of public and private messages from four large a prevalent criminal business service to which even unso- underground forums to identify the malicious actors involved phisticated cybercriminals can subscribe and subsequently in CAaaS, carefully study the operation of the scam, and profit with minimal investment. -

Case Study Introductions Contents Module One: Crocs Case Introduction

Case Study Introductions Contents Module One: Crocs Case Introduction ......................................................................................................... 1 Module Three: Wayfair Case Introduction ................................................................................................... 2 Module Five: Alibaba Case Introduction ...................................................................................................... 2 Module Seven: Uber Case Introduction ....................................................................................................... 3 Module Eight: General Electric Case Introduction ....................................................................................... 4 Resources for Case Study Introductions ....................................................................................................... 5 Module One: Crocs Case Introduction Since its inception in 2002, Crocs (NASDAQ: CROX) has sold more than 300 million pairs of shoes in more than 90 countries around the world. The company considers itself a world leader in innovative casual. By 2012, the trendy shoe brand was at the height of popularity (Max, 2013). The company was pursuing an aggressive retailing strategy, offering over 300 different designs at nearly 600 retail stores worldwide, with 315 normal stores, 157 outlet stores, and 122 kiosks. From this perspective, things looked bright for this quirky, proprietary footwear manufacturer. Then in 2013, the company’s performance began to publicly unravel. -

How Did the Supreme Court Change Online Sales Taxation?

ISSUE BRIEF 06.26.18 How Did the Supreme Court Change Online Sales Taxation? Joyce Beebe, Ph.D., Fellow, Center for Public Finance Last week, the U.S. Supreme Court ruled presence in the state;5 this is the result of that states can impose sales taxes on out- a 1992 Supreme Court ruling, Quill Corp. of-state retailers, even if they do not have a v. North Dakota.6 In 2017, South Dakota’s physical presence in the state. The decision Supreme Court struck down the state’s ends months of suspense and attention on digital sales tax law (S.B. 106); South Dakota the future of e-commerce. In July 2017, a then brought the case to the U.S. Supreme House subcommittee heard testimony on Court, in hopes of overturning Quill. the right of states to collect sales taxes Although earlier estimates varied,7 a from out-of-state merchants that do not recent U.S. Government Accountability Office have a physical presence in the destination (GAO) report indicated that based on current state.1 Several states, eager to defend their law, state and local governments were right to tax remote sellers, had passed already able to collect most remote sales tax “notice and reporting” laws, which require revenues that would be owed.8 Most large remote sellers to either collect sales taxes or remote sellers are either established retailers submit an annual report of each consumer’s that already have physical stores in many purchases to the state government.2 Some states, or have entered into agreements states have targeted marketplace providers with state governments to voluntarily collect such as Amazon and eBay, which previously sales taxes regardless of physical presence. -

Visa Account Updater Merchant List

Visa Account Updater Merchant List The Visa Account Updater (VAU) Merchant List includes all merchants enrolled as of May 1, 2016. It is consolidated in an attempt to relay the most relevant and meaningful merchant name as merchants enroll at differing levels: by subsidiary, franchise, or parent organization. Visa recommends that issuers and merchants do not actively market the service to cardholders because: 1. We do not have 100% penetration on all sides. 2. We cannot guarantee that the information exchange between the financial institution and merchant will occur in time for the cardholder's next billing. 3. Some merchants on this list may have only certain divisions or geographic regions participating. Therefore, we do not want to create an expectation that the service will address all account update issues for all merchants listed. Visa Confidential: This document contains Visa's proprietary information for use by Visa issuers, acquirers, merchants and their processors solely in support of Visa card programs. Disclosure to third parties or any other use is prohibited without prior written permission of Visa Inc. Merchant Name Web Site 1 Bloc LLC www.justmeans.com 100K Portfolio www.100kportfolio.com 100TB 121 Limited www.121Limited.com 125-Bonner & Partners www.agora-inc.com 1760335 ontario inc. www.cottagecountry.com 1800 Flowers 1-800-Flowers.com, Inc 190-Sovereign Society www.agora-inc.com 193-World Currency Watch www.agora-inc.com 195-Boom & Bust www.agora-inc.com 2 Checkout.Com. www.2co.com 2 Min Miracle 2-10 Holdco, Inc. www.2-10.com 2-10 Home Buyers Warranty www.2-10.com 21st Century Insurance and Financial Services www.21st.com 2251723 Ontario Inc. -

Wayfair Unveils Immersive Home Design Experience with Daydream Virtual Reality App

NEWS RELEASE Wayfair Unveils Immersive Home Design Experience with Daydream Virtual Reality App 11/10/2016 IdeaSpace App Allows Consumers to Explore and Shop Beautifully Designed Virtual Showrooms on Daydream, Google’s Mobile VR Platform BOSTON--(BUSINESS WIRE)-- Wayfair Inc. (NYSE:W), one of the world’s largest online destinations for home furnishings and décor, today announced the launch of IdeaSpace, the company’s second virtual reality application for designing spaces with furniture and décor. Available on Daydream, Google’s high quality, mobile VR platform, IdeaSpace enables consumers to explore a variety of uniquely designed spaces and shop their favorite nds in an interactive setting. IdeaSpace was built by Wayfair Next, the company’s internal research and development team, using Google’s virtual reality technology. This Smart News Release features multimedia. View the full release here: https://www.businesswire.com/news/home/20161110005830/en/ “Discovery is an essential part of the Wayfair shopping experience as consumers explore our unmatched selection and inspirational content to nd new ideas for their homes,” said Steve Conine, co-founder and co-chairman, Wayfair. “Inspired by Wayfair’s Get the Look resource, where shoppers can explore featured interiors from designers as well as Wayfair commercials and catalogs, IdeaSpace allows customers to browse beautifully styled spaces and products in a completely immersive experience.” By placing any Daydream-ready phone, such as Google's Pixel phone, into the Daydream View headset, shoppers are transported to a number of custom-designed rooms they can move through with a swipe on the Daydream controller. To “get the look,” shoppers can point the cursor at featured 3-D products, click to display additional details and rotate for a complete 360-degree view, then save their favorite products all within the app.