Doing Business in Belgium

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

OECD Economic Surveys Belgium February 2020

OECD Economic Surveys Belgium February 2020 OVERVIEW www.oecd.org/economy/belgium-economic-snapshot/ This Overview is extracted from the Economic Survey of Belgium. The Survey is published on the responsibility of the Economic and Development Review Committee (EDRC) of the OECD, which is charged with the examination of the economic situation of member countries. This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. OECD Economic Surveys: Belgium© OECD 2020 You can copy, download or print OECD content for your own use, and you can include excerpts from OECD publications, databases and multimedia products in your own documents, presentations, blogs, websites and teaching materials, provided that suitable acknowledgment of OECD as source and copyright owner is given. All requests for public or commercial use and translation rights should be submitted to [email protected]. Requests for permission to photocopy portions of this material for public or commercial use shall be addressed directly to the Copyright Clearance Center (CCC) at [email protected] or the Centre français d’exploitation du droit de copie (CFC) at [email protected]. EXECUTIVE SUMMARY 1 Executive Summary Belgium performs well in many economic and well-being dimensions, but some risks are building up The resilience of public finances should be increased Improving labour market outcomes is key Boosting potential growth requires higher productivity growth 2 EXECUTIVE SUMMARY Belgium performs well in many economic increase vulnerabilities and lower the resilience and well-being dimensions, but some risks of the financial system. -

GOING GLOBAL EXPORTING to BELGIUM a Guide for Clients

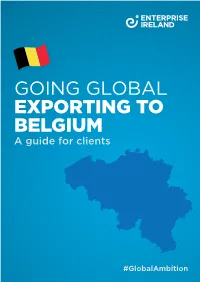

GOING GLOBAL EXPORTING TO BELGIUM A guide for clients #GlobalAmbition Capital Brussels Population 11.43m1 GDP per capita ¤35,3002 GDP growth (2018) 1.4%3 ANTWERPEN Unemployment rate 4 OOST-VLAANDEREN LIMBURG WEST-VLAANDEREN 5.7% VLAAMS - BRABANT Enterprise Ireland client exports (2018) BRABANT WALLON ¤467.5m HAINAUT LIEGE (Belgium & Luxemburg)5 NAMUR LUXEMBOURG 2 WHY EXPORT TO BELGIUM? Known as the heart of Europe, MANY IRISH COMPANIES ARE Belgium is a hub of international EXPORTING TO BELGIUM. WHAT’S cooperation and networking. STOPPING YOU? It is a country of three regions: Flanders, Wallonia One of the highest rates of and the Brussels-Capital Region, and has three official languages: Dutch, French and German. A Biotech R&D activity in the modern private enterprise economy, it is often EU13. Antwerp is the world’s viewed as a springboard into mainland Europe. second largest chemical Situated at the crossroads of three major cultures cluster after Heuston14. – Germanic, Roman and Anglo-Saxon - it is a good “test market” for companies looking to grow into the broader European markets by establishing a local Audiovisual services account presence or through trade. for 80% of Belgium’s Belgium has 16% of Europe’s Biotech6 industry creative service exports and and 19% of Europe’s pharmaceutical exports7. It 90% of its imports15. is incredibly successful given its modest size, by population and geography. The Belgian economy continues to grow at a modest Pharma and Life Sciences pace, mainly supported by robust growth in exports. has been a continuously It is ranked as the 11th largest export economy in the strong sector for Irish world, with a positive trade balance and its latest 16 fiscal reforms improving its attractiveness. -

Partitive Article

Book Disentangling bare nouns and nominals introduced by a partitive article IHSANE, Tabea (Ed.) Abstract The volume Disentangling Bare Nouns and Nominals Introduced by a Partitive Article, edited by Tabea Ihsane, focuses on different aspects of the distribution, semantics, and internal structure of nominal constituents with a “partitive article” in its indefinite interpretation and of potentially corresponding bare nouns. It further deals with diachronic issues, such as grammaticalization and evolution in the use of “partitive articles”. The outcome is a snapshot of current research into “partitive articles” and the way they relate to bare nouns, in a cross-linguistic perspective and on new data: the research covers noteworthy data (fieldwork data and corpora) from Standard languages - like French and Italian, but also German - to dialectal and regional varieties, including endangered ones like Francoprovençal. Reference IHSANE, Tabea (Ed.). Disentangling bare nouns and nominals introduced by a partitive article. Leiden ; Boston : Brill, 2020 DOI : 10.1163/9789004437500 Available at: http://archive-ouverte.unige.ch/unige:145202 Disclaimer: layout of this document may differ from the published version. 1 / 1 Disentangling Bare Nouns and Nominals Introduced by a Partitive Article - 978-90-04-43750-0 Downloaded from PubFactory at 10/29/2020 05:18:23PM via Bibliotheque de Geneve, Bibliotheque de Geneve, University of Geneva and Universite de Geneve Syntax & Semantics Series Editor Keir Moulton (University of Toronto, Canada) Editorial Board Judith Aissen (University of California, Santa Cruz) – Peter Culicover (The Ohio State University) – Elisabet Engdahl (University of Gothenburg) – Janet Fodor (City University of New York) – Erhard Hinrichs (University of Tubingen) – Paul M. -

2017-11-30 DP Winter in Brussels EN

PRESS KIT Brussels, 30 November 2017 A bright winter in Brussels... If the sun's rays are scarcer and no longer bring warmth and comfort at this time of the year, Brussels undertakes to brighten winter days and warm hearts with events and activities of all kinds which will lend rhythm to the season there. As it does every year, Brussels is putting on its finery for the close of year festivities. From Winter Wonders to the many Christmas markets that flourish in the four corners of the capital, not forgetting the magnificent son et lumière show that further glorifies one of the most beautiful "Main Squares" in the World, young and old will have plenty to feast their eyes on. A great chance to enjoy the magic of the holidays and turn your back on gloom in the heart of the capital of Europe. Contents Unmissable events this winter in Brussels ............................................................................................... 2 Exhibitions .......................................................................................................................................................... 3 Christmas Markets ........................................................................................................................................... 7 New Year’s outings ........................................................................................................................................... 9 What can you do with the children this winter? ................................................................................... -

'Talk Your Way out of Belgium!'

Master Thesis in International Business Strategy ‘Talk your way out of Belgium!’ A study on multilingualism in Belgium and its impact on an SME’s internationalisation Authors: Alena Kalb & Marijn Maas Supervisor: Richard Owusu Examiner: Per Servais Date: 23rd of May Academic term: Spring 2018 Subject: Business Administration with specialization in International Business Strategy, Degree Project Level: Master Course code: 4FE81E Abstract This thesis aims to connect the fields of multilingualism and internationalisation by studying language strategies of SMEs located in Belgium. Thereby the access to foreign networks in relation to internationalisation theories and the role of language capabilities and multilingualism is examined. This combination of different academic fields in international business and linguistics has previously not been studied satisfyingly and this research thus furthermore provides theoretical and managerial implications in this matter. Hence, this study addresses the briefly presented knowledge gap by answering the research question: What effect does the multilingualism in Belgium have on an SME’s internationalisation? The two following sub-research questions have been raised additionally to ensure the ability to answer the main research question: 1. What is the impact of the multilingualism in Belgium on an SME’s liability of foreignness when going international? 2. How does a language strategy support an SME’s internationalisation process and create a multilingual capability? Empirical data is collected both qualitatively by interviewing three Belgian SMEs and quantitatively by analysing secondary data of 30 Belgian company websites and their vacancy job postings, to provide answers to these questions. The findings are analysed by applying a conceptual framework, which was created by the authors. -

The London House of Rothschild and Its Belgian Contacts (1815‒1860)¹

The London house of Rothschild and its Belgian contacts (1815‒1860)¹ Hans Willems explains the significance of correspondence in The Rothschild Archive to the historian of Belgian financial history and the Antwerp Stock Exchange. The manner in which it is possible to conduct transactions at the Brussels stock exchange may, from a technological point of view, be ranked amongst the most progressive systems in the world today. As a full-fledged partner within Euronext,² the Brussels exchange makes use of the virtual market environment, which allows members (clients) of the exchange to log in via their computer and engage in trades from any place in the world. Methodology has indeed come a long way since the inception of the modern Belgian stock exchange at the time of the French occupation (1798–1815), when communications relied on a The Bourse at Antwerp slow-moving mail service or carrier pigeons, rather unreliable messengers. So while during the in 1802, an engraving from the collection of the first half of the nineteenth century, personal contact between the brokers and their clients was Antwerp Stock Exchange certainly very important, the technical impediments made smooth-running exchange transac- archives. tions practically impossible. University of Antwerp. During this period, the Antwerp stock exchange dominated the market for transactions in commodities and government bonds that were undertaken in the Belgian regions. Only after Belgium’s independence in 1830, under the stimulus of transactions in corporate shares and Belgian government bonds, did the Brussels exchange begin to gain steadily in importance, to the extent that, as of the second half of the nineteenth century, it played a leading role in Belgian stock exchange history. -

Comparative Review of the Foreign Language Learning History of a Japanese and a Flemish-Dutch Native Speaker

Comparative Review of the Foreign Language Learning History of a Japanese and a Flemish-Dutch native Speaker Masako Nishikawa-Van Eester, Nishogakusha University, Japan The Asian Conference on Language 2020 Official Conference Proceedings Abstract How we learn a foreign (second, third, fourth, …) language contains diverse approaches. It depends on, to the great extent, each learner’s personal background and aptitude such as the starting age, native language, motivation, goal(s), learning context, and life history. It is also dynamic, in the process of learning the target language, in a sense that 1) those previously mentioned factors can change longitudinally and 2) those factors are influenced by the community, society, culture and historical/geographical condition which the learner is originally attached to. What is reported in this qualitative research project is a twofold case study of two foreign language learners, one is a Japanese from Kobe, and the other is a Belgian from Flanders (the Dutch-speaking region). The former thus is a Japanese native speaker who also uses English and Dutch for her work and academic activities (together with her some knowledge of German, French and Afrikaans), and the latter is a Dutch native speaker who uses mainly Dutch, English and Japanese in business (with his background of learning Latin, German, French, Spanish and Portuguese). Through the observation and comparison of those two language learners – juxtaposing their similarities and contrasting the differences – we discover several pedagogical insights in language learning activities, which might be of help for those who struggle to learn foreign languages (specifically English as the first foreign language) in Japan. -

Narrative Report on Belgium

NARRATIVE REPORT ON BELGIUM PART 1: NARRATIVE REPORT Rank: 50 of 133 Belgium comes in at number 50 in the 2020 Financial Secrecy Index, with a global scale weight of 1.72 per cent. Belgium has always had How Secretive? 45 a relatively large financial services industry given the size of the country, but recent improvements in financial transparency means it has a relatively low secrecy score of 45, reflecting significant changes over the course of the past decade. Although the use of Belgium as Moderately 0 to 25 a secrecy jurisdiction has declined, there remain issues for domestic secretive tax inspectors accessing Belgian accounts. The country also remains a corporate tax haven. The end of bank secrecy in Belgium? 25 to 50 Bank secrecy was formally introduced in Belgian tax legislation in 1980 but had existed informally for a long time prior to that. The domestic provisions governing bank secrecy (article 318 of the Income Tax Code) prevented the tax administration from investigating the accounts of 50 to 75 non-residents when requested by a foreign administration. The tax administration could only force the bank to release client information when provided with evidence that the bank was an accessory to serious Exceptionally tax fraud. However, in recent years, a number of measures have been secretive 75 to 100 introduced to weaken bank secrecy. In the aftermath of recent financial scandals like the Panama Papers and the Paradise Papers, considerable public pressure emerged calling for increased transparency to ensure fair taxation. Bank secrecy is under attack more than ever. How big? 1.72% When the European Union Savings Tax Directive came into effect in 2005, Belgium initially opted to levy withholding taxes on savings income instead of opting for the EU’s automatic information exchange with the relevant taxpayer’s home jurisdiction. -

Casteau Handbook

CASTEAU HANDBOOK Military Family Services (Europe) www.cafconnection.ca/Europe Date published: Date revised: TABLE OF CONTENTS GREETINGS FROM YOUR MFS(E) TEAM ....................... 8 MFS(E) Services ............................................................................................... 8 European Advisory Committee ......................................................................... 10 Using This Guide ............................................................................................ 10 SOME HELPFUL RESOURCES ..................................... 12 OVERVIEW OF BELGIUM ........................................... 13 Map OF BELGIUM (with mons) ......................................................................... 13 Geography/Politics ......................................................................................... 14 Climate ......................................................................................................... 14 Languages ..................................................................................................... 14 Religion ........................................................................................................ 15 Canadian/Expat Community ............................................................................ 15 Cultural Nuances, Etiquette and Traditions ........................................................ 15 Public Holidays ............................................................................................... 16 Belgian public holidays -

Taxation of Companies Under Belgian Income Tax Law

IFA Issue – Articles Eric Osterweil and Marc Quaghebeur* Taxation of Companies under Belgian Income Tax Law This article sets forth the principal features of 2. General Comments Belgium’s income tax system as applied to companies, focusing on selected aspects that With few exceptions, commercial entities that have legal may be of interest to foreign investors. After an personality are subject to the company income tax in introduction and some general comments, Belgium. Thus, entities in the form of a corporation, lim - the article discusses, among other things, ited liability companies and most types of partnerships the computation of a company’s taxable income, are subject to company income taxation. Belgium does the tax rates, withholding taxes and foreign tax not recognize fiscal transparency for any type of com - credits, the general and specific anti-avoidance pany having legal personality except in the case of Eco - rules in Belgian law, the tax treatment of non- nomic Interest Groupings and European Economic resident companies, and Belgian companies in Interest Groupings. international tax planning. Partnerships formed under company law that in other jurisdictions might be transparent for income tax pur - 1. Introduction poses are subject to the company income tax. Their part - ners are taxed only on the distribution of income to This article sets forth the principal features of Belgium’s them. income tax system as applied to companies with empha - sis on selected aspects that may be of interest to foreign Companies that are resident in Belgium are subject to investors. full company income taxation, while non-resident com - panies are generally subject to company income taxation As an EU Member State, Belgium is obliged to comply only on income derived from Belgian sources. -

Belgium Taxation and Investment 2012

Taxation and Investment in Belgium 2012 Reach, relevance and reliability A publication of Deloitte Touche Tohmatsu Limited Contents 1.0 Investment climate 1.1 Business environment 1.2 Currency 1.3 Banking and financing 1.4 Foreign investment 1.5 Tax incentives 1.6 Exchange controls 2.0 Setting up a business 2.1 Principal forms of business entity 2.2 Regulation of business 2.3 Accounting, filing and auditing requirements 3.0 Business taxation 3.1 Overview 3.2 Residence 3.3 Taxable income and rates 3.4 Capital gains taxation 3.5 Double taxation relief 3.6 Anti-avoidance rules 3.7 Administration 3.8 Other taxes on business 4.0 Withholding taxes 4.1 Dividends 4.2 Interest 4.3 Royalties 4.4 Branch remittance tax 4.5 Wage tax/social security contributions 5.0 Indirect taxes 5.1 Value added tax 5.2 Capital tax 5.3 Real estate tax 5.4 Transfer tax 5.5 Stamp duty 5.6 Customs and excise duties 5.7 Environmental taxes 5.8 Other taxes 6.0 Taxes on individuals 6.1 Residence 6.2 Taxable income and rates 6.3 Inheritance and gift tax 6.4 Net wealth tax 6.5 Real property tax 6.6 Social security contributions 6.7 Other taxes 6.8 Compliance 7.0 Labor environment 7.1 Employees’ rights and remuneration 7.2 Wages and benefits 7.3 Termination of employment 7.4 Labor-management relations 7.5 Employment of foreigners 8.0 Deloitte International Tax Source 9.0 Office locations Belgium Taxation and Investment 2012 1.0 Investment climate 1.1 Business environment Belgium is a constitutional monarchy in which ultimate power rests with a bicameral parliament. -

University Entrance Language Tests: a Matter of Justice

LTJ0010.1177/0265532217706196Language TestingDeygers et al. 706196research-article2017 CORE Metadata, citation and similar papers at core.ac.uk Provided by Ghent University Academic Bibliography /$1*8$*( Article 7(67,1* Language Testing 1 –28 University entrance language © The Author(s) 2017 Reprints and permissions: tests: A matter of justice sagepub.co.uk/journalsPermissions.nav https://doi.org/10.1177/0265532217706196DOI: 10.1177/0265532217706196 journals.sagepub.com/home/ltj Bart Deygers KU Leuven, Belgium Kris Van den Branden KU Leuven, Belgium Koen Van Gorp Michigan State University, USA Abstract University entrance language tests are often administered under the assumption that even if language proficiency does not determine academic success, a certain proficiency level is still required. Nevertheless, little research has focused on how well L2 students cope with the linguistic demands of their studies in the first months after passing an entrance test. Even fewer studies have taken a longitudinal perspective. Set in Flanders, Belgium, this study examines the opinions and experiences of 24 university staff members and 31 international L2 students, of whom 20 were tracked longitudinally. Attention is also given to test/retest results, academic score sheets, and class recordings. To investigate the validity of inferences made on the basis of L2 students’ scores, Kane’s (2013) Interpretation/ Use Argument approach is adopted, and principles from political philosophy are applied to investigate whether a policy that discriminates among students based on language test results can be considered just. It is concluded that the receptive language requirements of university studies exceed the expected B2 level and that the Flemish entrance tests include language tasks that are of little importance for first-year students.