Revenue Is 85% from the U.S. S&P Credit Rating: A

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Hershey Company Scares up Halloween Fun This Season with Delicious New Treats and Classic Favorites

FOR IMMEDIATE RELEASE CONTACTS: Jody Cook Corey Dunavan The Hershey Company JSH&A Public Relations 717.534.4288 630.932.7968 [email protected] [email protected] THE HERSHEY COMPANY SCARES UP HALLOWEEN FUN THIS SEASON WITH DELICIOUS NEW TREATS AND CLASSIC FAVORITES From Delighting Trick-or-Treaters to “Boo-ing” the Neighbors, Hershey’s Halloween Experts Offer Sweet Treats for the Season HERSHEY, Pa. – September 15, 2008 – Halloween is the season of ghosts, goblins and best of all, candy. The experts at The Hershey Company are emphasizing the “treat” in trick-or-treat this year by offering an assortment of new and classic candy, certain to delight trick-or-treaters, bolster “boo-ing” gifts and sweeten seasonal candy dishes. From favorites such as Hershey®’s Milk Chocolate Snack Size Bars to new Whoppers® Malted Milk Balls Haunted House Cartons, Hershey’s “spook-tacular” selection offers something for everyone. Trick-or-Treating and Halloween Party Essentials Hershey’s has delicious candies for every occasion this season, whether treating trick-or-treaters or filling the office candy dish. New products this year include: Hershey®’s Kisses® Candy Corn Flavored Candies Twizzlers® Candy snack-sized Rainbow Twists Hershey’s Tombstone-shaped Moulded Bars in Milk Chocolate and Cookies ‘n’ Crème flavors Hershey’s and Reese’s® Boo Crew (foil-wrapped milk chocolate or peanut butter-filled milk chocolate candies) Demon Treats Assorted Bag (Milk Duds® Candy, Reese’s Pieces® Candy, Whoppers Malted Milk Balls, Kit Kat® Wafer Bars and Hershey’s Milk Chocolate) Candy Caldron Assorted Bag (Jolly Rancher® Lollipops, Jolly Rancher Doubles Candy, Twizzlers Strawberry Mini-Bars and Twizzlers® Pull ‘n Peel® Candy with Green Apple and Tropical flavors) Treat yourself with classic favorites people scream for year after year, such as Hershey’s Milk Chocolate, Reese’s Peanut Butter Cups and Kit Kat Wafer Bars in a snack-size package that’s perfect for the trick-or-treat bag. -

Mckeesport Candy Co. CANDY CIGARETTES & CIGARS

412-678-8851 [email protected] FAX: 412-673-4406 McKeesport Candy Co. Visit CandyFavorites.com to view products. *** Please note that website prices reflect suggested retail *** CHANGEMAKERS EFRUTTI GUMMI CHANGEMAKER 7272 ANGEL MINTS 110 4090 GUMMI BRACELET 40 7248 CANDY CIGARETTES 24 42134 BAKERY SHOPPE - SHARE SIZE 12 7171 CARAMEL CREAMS 170 7177 GUMMI BURGER 60 7347 CELLA CHERRY- INDIVIDUALLY WRAPPED 72 3752 GUMMI CUPCAKES 60 7173 CHARLSTON CHEW - VANILLA 96 42133 EFRUTTI GUMMI CHEESECAKES 30 4277 CHICKO STICK 36 40078 GUMMI DONUTS - SHARE SIZE 12 COWTALES 7262 GUMMI HOT DOG 60 5067 COWTALES - CARAMEL APPLE 36 4105 GUMMI PIZZA 48 5304 COWTALES - CHOCOLATE BROWNIE 36 40079 GUMMI RAINBOW UNICORN - SHARE SIZE 12 7270 COWTALES - STRAWBERRY SMOOTHIE 36 63151 GUMMI SEA CREATURES 60 7263 COWTALES - VANILLA 36 7266 GUMMI SOUR GECKO 40 7269 FUN DIP 48 EFRUTTI GUMMI BAGS - LARGE 7275 ICE CUBES 100 43030 GUMMIUNIVERSE SHELF TRAY 12 46001 JOLLY RANCHER FILLED POPS 100 6943 GUMMI LUNCH BAG SHELF TRAY 12 7286 JUNIOR MINTS - BOXES 72 42111 GUMMI LUNCH BAG SOUR TRAY 12 5443 MALLO CUPS - FUN SIZE 60 42008 GUMMI MOVIE BAG SHELF TRAY 12 4848 PRETZEL RODS 450 43203 GUMMI TREASURE HUNT SHELF TRAY 12 7313 PUMPKIN SEEDS - INDIAN 36 25¢ PRE-PRICED BOXES 5040 RAZZLES CHANGEMAKERS 240 3395 BERRY CHEWY LEMONHEADS 24 4423 RAIN-BLO GUM - MINI PACKS 48 4018 BOSTON BAKED BEANS 24 7215 REESE PEANUT BUTTER CUPS - MINI 105 7912 APPLEHEADS 24 7156 SATELLITE WAFERS 240 7913 CHERRYHEADS 24 5089 SATELLITE WAFERS - SOUR 240 5154 CHEWY LEMONHEADS 24 7318 SIXLETS -

Order Book--7-3-13A.Xlsx

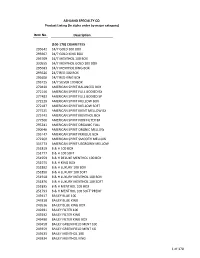

ASHLAND SPECIALTY CO. Product Listing (In alpha order by major category) Item No. Description (100-178) CIGARETTES 295642 24/7 GOLD 100 BOX 295667 24/7 GOLD KING BOX 295709 24/7 MENTHOL 100 BOX 330555 24/7 MENTHOL GOLD 100 BOX 295683 24/7 MENTHOL KING BOX 295626 24/7 RED 100 BOX 295600 24/7 RED KING BOX 295725 24/7 SILVER 100 BOX 279430 AMERICAN SPIRIT BALANCED BOX 272146 AMERICAN SPIRIT FULL BODIED BX 277483 AMERICAN SPIRIT FULL BODIED SP 272229 AMERICAN SPIRIT MELLOW BOX 272187 AMERICAN SPIRIT MELLOW SOFT 277525 AMERICAN SPIRIT MENT MELLOW BX 275743 AMERICAN SPIRIT MENTHOL BOX 277566 AMERICAN SPIRIT NON FILTER BX 293241 AMERICAN SPIRIT ORGANIC FULL 290940 AMERICAN SPIRIT ORGNIC MELLOW 295147 AMERICAN SPIRIT PERIQUE BOX 272260 AMERICAN SPIRIT SMOOTH MELLOW 333773 AMERICAN SPIRIT USGROWN MELLOW 251819 B & H 100 BOX 251777 B & H 100 SOFT 251959 B & H DELUXE MENTHOL 100 BOX 251975 B & H KING BOX 251892 B & H LUXURY 100 BOX 251850 B & H LUXURY 100 SOFT 251918 B & H LUXURY MENTHOL 100 BOX 251876 B & H LUXURY MENTHOL 100 SOFT 251835 B & H MENTHOL 100 BOX 251793 B & H MENTHOL 100 SOFT"PREM" 249417 BAILEY BLUE 100 249318 BAILEY BLUE KING 249516 BAILEY BLUE KING BOX 249391 BAILEY FILTER 100 249292 BAILEY FILTER KING 249490 BAILEY FILTER KING BOX 249458 BAILEY GREEN FIELD MENT 100 249359 BAILEY GREEN FIELD MENT KG 249433 BAILEY MENTHOL 100 249334 BAILEY MENTHOL KING 1 of 170 ASHLAND SPECIALTY CO. Product Listing (In alpha order by major category) Item No. Description 249532 BAILEY MENTHOL KING BOX 249474 BAILEY SKY BLUE 100 249375 BAILEY SKY BLUE -

2021 1H 4' 10 Shelf Inline

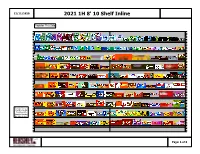

12/11/2020 2021 1H 8' 10 Shelf Inline Register This Side Replace Reese's Crunchy Cookie Cup King with Reese's Crunchy Bar King in April Page: 1 of 6 12/11/2020 2021 1H 8' 10 Shelf Inline Register This Side 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 Shelf: 10 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 Shelf: 9 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 Shelf: 8 1 2 3 4 5 6 7 8 9 10 11 12 13 14 Shelf: 7 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 Shelf: 6 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Shelf: 5 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Shelf: 4 Replace Reese's 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Crunchy Cookie Shelf: 3 Cup King with Reese's Crunchy Bar King in April 1 2 3 4 5 6 7 8 9 10 11 12 13 14 Shelf: 2 1 2 3 4 5 6 7 8 9 10 11 12 13 14 Shelf: 1 Page: 2 of 6 12/11/2020 2021 1H 8' 10 Shelf Inline Segment-Packtype Mints Bottle & Mega Gum Nonchocolate King and Standard Chocolate King Singles Gum Chocolate Standard Register This Side EXTRA EXTRA EXTRA ICE ICE ICE ICE ICE ICE ICE TRIDENT TRIDENT REFRESHE REFRESHE REFRESHE BREAKERS BREAKERS BREAKERS BREAKERS BREAKERS BREAKERS BREAKERS VIBES S/F MENTOS MENTOS MENTOS VIBES R RS RS S/F CUBE S/F CUBE S/F CUBE S/F CUBE S/F CUBE S/F CUBE S/F CUBE SPEARMINT PURE FRESH PURE FRESH PURE WHITE EXTRA EXTRA 5 COBALT S/F POLAR BERRY 5 RAIN PEPPERMI SPEARMIN WNTRGRN ARCTIC RASPBRY CINN BLK CHR S/F GUM - FRESH GUM - S/F GM SWT SPEARMINT 5 SPRMNT ICE MIX TRIDENT POLAR 35PC 5 RAIN 5 5 DENTYNE TROP BT SPEARMINT MNT 35PC NT T GRAPE SORBT MINT 50PC GUM SGR ICE 35PC 35PC -

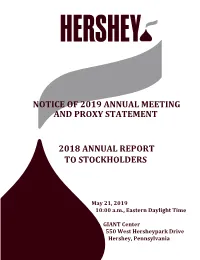

2019 Proxy Statement and 2018 Annual Report

NOTICEOF201ͻANNUALMEETING ANDPROXYSTATEMENT 201ͺANNUALREPORT TOSTOCKHOLDERS May 2ͳ, 201ͻ 10:00 a.m., Eastern Daylight Time GIANT Center 550 West Hersheypark Drive Hershey, Pennsylvania Michele Buck President and Chief Executive Officer April 11, 2019 Dear Stockholder: I am pleased to invite you to The Hershey Company’s 2019 Annual Meeting of Stockholders. Our meeting will be held on Tuesday, May 21, 2019, at 10:00 a.m. Eastern Standard Time. Detailed instructions for attending the meeting and how to vote your Hershey shares prior to the meeting are included in the proxy materials that accompany this letter. Your vote is extremely important to us, and I encourage you to review the materials and submit your vote today. This year we are celebrating the company’s 125th anniversary. We are one of the few Fortune 500 companies that are connecting with consumers as strongly today as we were more than a century ago and that is because, quite simply, we love making the brands that our consumers love. As we celebrate this extraordinary milestone, I am honored to lead a company with teams of people who care about one another and their communities, have deep pride in our incredible portfolio of brands and recognize that as the stewards of this incredible legacy, we are entrusted to build for the future and make the strategic decisions that ensure Hershey is well-positioned for generations to come. As I look back on 2018, the marketplace continues to be dynamic and fast-moving. We have amazing brands in categories that are growing. Consumers continue to snack throughout the day and Hershey is offering more snacking options to satisfy their needs by broadening our product portfolio beyond confection to reflect the changing way people want to snack. -

6' 10 Shelf Inline.Psa

8/22/2019 6' 10 Shelf Inline Register This Side 3 ft 3 ft Adds Deletes Deletes Deletes Page: 1 of 5 Shelf Schematic Report Planogram #1 Name: 6' 10 Shelf Inline h: 5 ft 4.00 in w: 6 ft d: 6 ft Segment: 1 Name: 10 h:1.00 in w: 72.00 in d: 12.00 in Location ID UPC ID Name Size UOM Height Width Depth Facings #1 3400000843 ICE BREAKERS ICE CUBES CUBE PK PEPPERMINT 40 CT 40.00 CT 3.26 in 2.51 in 2.59 in 1 #2 3400000847 ICE BREAKERS ICE CUBES CUBE PK SPEARMINT 40 CT 40.00 CT 3.26 in 2.51 in 2.59 in 1 #3 3400000545 ICE BREAKERS ICE CUBES ARCTIC GRAPE 40 PC 40.00 PC 3.26 in 2.51 in 2.61 in 1 #4 3400000848 ICE BREAKERS ICE CUBES CUBE PK RASPBRY SORBT ... 40.00 CT 3.26 in 2.51 in 2.59 in 1 #5 1254601264 TRIDENT VIBES S/F SPEARMINT 40.00 PC 3.60 in 2.38 in 2.40 in 1 #6 2200001918 00022000019189 ORBIT WHITE S/F PPRMNT 40.00 PC 3.45 in 2.50 in 2.50 in 2 #7 2200001917 00022000019172 ORBIT WHITE S/F SPRMNT 40.00 PC 3.45 in 2.50 in 2.50 in 2 #8 7339001404 MENTOS PURE FRESH GUM - FRESH MINT 50.00 PC 50.00 PC 3.91 in 2.31 in 2.25 in 1 #9 7339001405 MENTOS PURE FRESH GUM - SPEARMINT 50. PC 50.00 PC 3.92 in 2.48 in 2.25 in 1 #10 7339001393 MENTOS PURE FRSH S/F GUM MINT 15.00 PC 3.85 in 3.90 in 6.40 in 1 #95 2200001788 EXTRA POLAR ICE 35.00 PC 3.30 in 4.35 in 0.90 in 1 #96 2200001787 EXTRA SPEARMINT 35.00 PC 3.30 in 4.35 in 0.90 in 1 #66 2200002190 00022000021908 EXTRA REFRESHER S/F SPRMNT 40.00 PC 3.35 in 2.75 in 2.05 in 2 #67 2200001789 00022000017895 5 COBALT 35.00 PC 3.25 in 4.35 in 0.85 in 2 #97 1254631255 DENTYNE ICE S/F PPRMNT 16.00 PC 2.15 in 3.70 -

Candy Bar Sayings

Candy Bar Sayings: 1. Package of M&M’s a. Magnificent and Marvelous Staff member b. Much and Many Thanks c. Magical and Marvelous Teacher 2. Cotton Candy- a. “You make the fluffy stuff around here because…. ” 3. Peanut M&M’s a. You are anything but plain 4. 100 Grand Candy Bar a. You are worth a 100 Grand to us b. We wouldn’t trade you for a 100 Grand 5. Reese’s Pieces a. We love you to pieces b. We love how you helped keep us from falling to pieces c. You were the piece we were missing d. Thank you for teaching the kids the missing pieces this year e. You are an important piece to our team 6. Milky Way: a. You are the best in the Milky Way b. You are the brightest star in the Milky Way c. Your smile brightens the Milky Way 7. DOTS: a. Thanks for helping us connect the dots 8. Mike and Ikes: a. Mike and Ike think you are special 9. Sweet-tarts a. Thank you for being such a sweet-tart 10. Smarties a. You are one of our smarties 11. Mints a. We mint to tell you how much we appreciate you b. You are a breath of fresh air 12. Snickers a. You keep it together even when the kids want to make you snicker b. Laugh and the whole world laughs with you 13. Lifesavers a. You are a lifesaver 14. Whoppers a. You go to great lengths to help the kids grow whoppers b. -

Master Candy List

412-678-8851 [email protected] FAX: 412-673-4406 McKeesport Candy Co. Visit CandyFavorites.com to view products. CHANGEMAKERS EFRUTTI GUMMI CHANGEMAKER 7272 ANGEL MINTS 110 4090 GUMMI BRACELET 40 7248 CANDY CIGARETTES 24 42134 BAKERY SHOPPE - SHARE SIZE 12 7171 CARAMEL CREAMS 170 7177 GUMMI BURGER 60 7347 CELLA CHERRY- INDIVIDUALLY WRAPPED 72 3752 GUMMI CUPCAKES 60 7173 CHARLSTON CHEW - VANILLA 96 42133 EFRUTTI GUMMI CHEESECAKES 30 4277 CHICKO STICK 36 40078 GUMMI DONUTS - SHARE SIZE 12 COWTALES 7262 GUMMI HOT DOG 60 5067 COWTALES - CARAMEL APPLE 36 4105 GUMMI PIZZA 48 5304 COWTALES - CHOCOLATE BROWNIE 36 40079 GUMMI RAINBOW UNICORN - SHARE SIZE 12 7270 COWTALES - STRAWBERRY SMOOTHIE 36 63151 GUMMI SEA CREATURES 60 7263 COWTALES - VANILLA 36 7266 GUMMI SOUR GECKO 40 7269 FUN DIP 48 EFRUTTI GUMMI BAGS - LARGE 7275 ICE CUBES 100 43030 GUMMIUNIVERSE SHELF TRAY 12 46001 JOLLY RANCHER FILLED POPS 100 6943 GUMMI LUNCH BAG SHELF TRAY 12 7286 JUNIOR MINTS - BOXES 72 42111 GUMMI LUNCH BAG SOUR TRAY 12 5443 MALLO CUPS - FUN SIZE 60 42008 GUMMI MOVIE BAG SHELF TRAY 12 4848 PRETZEL RODS 450 43203 GUMMI TREASURE HUNT SHELF TRAY 12 7313 PUMPKIN SEEDS - INDIAN 36 25¢ PRE-PRICED BOXES 5040 RAZZLES CHANGEMAKERS 240 3395 BERRY CHEWY LEMONHEADS 24 4423 RAIN-BLO GUM - MINI PACKS 48 4018 BOSTON BAKED BEANS 24 7215 REESE PEANUT BUTTER CUPS - MINI 105 7912 APPLEHEADS 24 7156 SATELLITE WAFERS 240 7913 CHERRYHEADS 24 5089 SATELLITE WAFERS - SOUR 240 5154 CHEWY LEMONHEADS 24 7318 SIXLETS 48 3396 CHEWY LEMONHEADS - REDRIFIC 24 7154 SOFT PEPPERMINT PUFFS -

The Hershey Company and the Cocoa Controversy

Center for Ethical Organizational Cultures Auburn University http://harbert.auburn.edu The Hershey Company and The Cocoa Controversy INTRODUCTION Chocolate is enjoyed by millions, mainly in decadent desserts, candies, and drinks. It contains fiber, iron, magnesium, copper manganese, potassium, phosphorus, zinc and selenium, which are nutritional antioxidants. Dark chocolate, with at least 70% cocoa, is considered protective against heart disease because it can reduce blood pressure, improve blood flow, raise HDL cholesterol (known as the good cholesterol), and lower total LDL cholesterol, or less desirable cholesterol. In one study, it was shown to reduce calcified arterial plaque by 32%. Other studies indicate that long term consumption of dark chocolate may protect skin from sun damage and reduce the risk of cancer, help with cognitive function in elderly people, and improve brain blood flow, oxygen levels and nerve function. As science learns more about the health benefits of dark chocolate, its demand continues to grow. Developing countries are discovering that chocolate beans improve their sweet treats and candies, thus creating even greater worldwide demand. Cocoa beans grow mostly in tropical climates, mainly in Western Africa, Asia and Latin America, the largest exporters being Ghana and the Ivory Coast. With over $7.5 billion dollars in sales every year, the Hershey Company is one of the world’s largest producers of chocolate and candy products. Hershey’s products are sold in more than 70 countries and include Hershey’s Kisses and Hershey’s Milk Chocolate Bars as well as brands such as Reese’s, Whoppers, Almond Joy, and Twizzlers. Although Hershey strives to be a model company and has several philanthropic, social, and environmental programs, the company has struggled with ethical issues related to the labor issues associated with West African cocoa communities, including child labor. -

Hershey Foods Corporation, Hershey, PA 17033-0819 Cadbury • Caramello Candy Bar OU-D • Dairy Milk Chocolate Candy Bar OU-D

11 Broadway New York, NY 10004 * Tel: (212) 563-4000 * Fax: (212) 564-9058 * www.ou.org February 15, 2005 TO WHOM IT MAY CONCERN: This is to certify that the following products, listed under their respective brand names, prepared by Hershey Foods Corporation, Hershey, PA 17033-0819 are manufactured under the supervision of the Kashruth Division of the Orthodox Union and are kosher when bearing the symbol adjacent to each product as indicated below. Products designated below as OU are certified kosher pareve. Products designated below as OU-D are certified kosher dairy. The company is authorized to place only this symbol on packaging. Products that appear below with one asterisk are Kosher for Passover and year-round use. Brand: Cadbury Symbol • Caramello Candy Bar OU-D • Dairy Milk Chocolate Candy Bar OU-D • Dairy Milk Chocolate Paste OU-D • Dairy Milk Chocolate Solid Bunny OU-D • Fruit & Nut Milk Choc. Candy Bar OU-D • Mini-Eggs Sugar Coated Milk Choc. Candy OU-D • Raspberries & Creme Candy Bar OU-D • Roasted Almond Milk Choc. Candy Bar OU-D • Royal Dark Chocolate Candy Bar OU-D • Royal Dark Mint Bar OU-D Brand: Heath Symbol • Bites OU-D • Ground Butter Brickle OU-D • Ground English Toffee Chunks OU-D • Ground Toffee OU-D • Heath Bits-O-Brickle OU-D • Heath Bits-O-Heath OU-D • Heath Butter Brickle Candy OU-D • Heath Center OU-D • Heath Dark Chocolate OU-D • Heath Dark Chocolate Pyramids OU-D • Heath English Toffee OU-D • Heath English Toffee Bar OU-D Rabbi Menachem Genack Effective from 02/01/2005 through 01/31/2006 Rabbinic Administrator Page: 1 of 20 11 Broadway New York, NY 10004 * Tel: (212) 563-4000 * Fax: (212) 564-9058 * www.ou.org February 15, 2005 LETTER OF CERTIFICATION - continued Company: Hershey Foods Corporation Brand: Heath - Cont. -

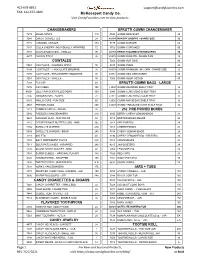

Gum * Bubble/Kids/Novelty Types- (0200) Gum * Mini Packs

PAGE : 1 SOLD TO CUST NO. DATE : _______________ GUM * BUBBLE/KIDS/NOVELTY TYPES- (0200) 360959 TRIDENT GUM S/F ISLAND BERRY 12/BX 530324 AIRHEAD GUM BL RASPBERRY 14PC 12/BX 360906 TRIDENT GUM S/F MINT BLISS 12/BX 530320 AIRHEAD GUM CHERRY 14 PC 12/BOX 360913 TRIDENT GUM S/F MINT SW TWST 12/BOX 530322 AIRHEAD GUM WATERMELON 14 PC 12/BOX 360951 TRIDENT GUM S/F ORIGINAL 12/BOX 350250 BIG LEAGUE CHEW GRAPE 12/BOX 361003 TRIDENT GUM S/F PASSION FRT 12/BOX 350202 BIG LEAGUE CHEW GIRL 12/BOX 360919 TRIDENT GUM S/F PEPPERMINT 12/BOX 350200 BIG LEAGUE CHEW ORIGINAL 12/BOX 360901 TRIDENT GUM S/F SPEARMINT 12/BOX 350170 BIG LEAGUE CHEW SOUR APPLE 12/BOX 360911 TRIDENT GUM S/F TROPIC TWIST 12/BX 350160 BIG LEAGUE CHEW WATERMELON 12/BOX 360957 TRIDENT GUM S/F WINTERGREEN 12/BOX 350174 BIG LEAGUE CHEW 5-BALL GRAPE 18/BOX 360962 TRIDENT GUM S/F WTR/MLN TWIST 12/BX 350176 BIG LEAGUE CHEW 5-BALL ORIG 18/BX 361031 TRIDENT LAYERS CHERRY + LIME 12/BX 750300 BUBBLE TAPE BUBBLE GUM 24/BOX 361026 TRIDENT LAYERS GRAPE+LEMONADE 12/BX 350400 BUBBLE YUM REGULAR 18/BOX 361020 TRIDENT LAYERS SBERRY/CITRUS 12/BX 350778 BUBBLICIOUS BUBBLE GUM 18/BOX 361035 TRIDENT LAYERS W-MELON/TROPIC 12/BX 350710 BUBBLICIOUS GONZO GRAPE 18/BOX 326001 WRIG "5" ASCENT PTP 10/BX 350900 BUBBLICIOUS S/BERRY SPLASH 18/BOX 326010 WRIG "5" COBALT PTP 10/BX 350950 BUBBLICIOUS WATERMELON 18/BOX 327040 WRIG "5" PRISM WATERMELON PTP 10/BX 351030 HUBBA BUBBA MAX SB/WM 18/BOX 326020 WRIG "5" RAIN PTP 10/BX 351015 HUBBA BUBBA ORIGINAL 18/BOX 328005 WRIG "5" REACT MINT PTP 10/BX 351452 RAINBLO -

Halloween Candy Cheat Sheet

Halloween Candy Cheat Sheet Halloween Candy Cheat Sheet Halloween Candy Cheat Sheet Almond Joy, snack size = 2 PPV Almond Joy, snack size = 2 PPV Almond Joy, snack size = 2 PPV Baby Ruth bar, fun size, 1 bar = 2 PPV, 2 bars = 5 Baby Ruth bar, fun size, 1 bar = 2 PPV, 2 bars = 5 Baby Ruth bar, fun size, 1 bar = 2 PPV, 2 bars = 5 PPV PPV PPV Bit-O-Honey, 1 piece = 1 PPV, 6 pieces = 4 PPV Bit-O-Honey, 1 piece = 1 PPV, 6 pieces = 4 PPV Bit-O-Honey, 1 piece = 1 PPV, 6 pieces = 4 PPV Butterfinger, fun size = 3 PPV Butterfinger, fun size = 3 PPV Butterfinger, fun size = 3 PPV Candy Apple, 5 ounce = 5 PPV Candy Apple, 5 ounce = 5 PPV Candy Apple, 5 ounce = 5 PPV Candy corn, 20 pieces = 4 PPV Candy corn, 20 pieces = 4 PPV Candy corn, 20 pieces = 4 PPV Candy Corn, Brach’s Big Bag, 26 pieces = 4 PPV Candy Corn, Brach’s Big Bag, 26 pieces = 4 PPV Candy Corn, Brach’s Big Bag, 26 pieces = 4 PPV Caramel Apple = 10 PPV Caramel Apple = 10 PPV Caramel Apple = 10 PPV Charms Blow Pop, 1 pop = 2 PPV Charms Blow Pop, 1 pop = 2 PPV Charms Blow Pop, 1 pop = 2 PPV Dots, fun size = 2 PPV Dots, fun size = 2 PPV Dots, fun size = 2 PPV Dove Milk Chocolate, 1 piece = 1 PPV, 5 pieces = 6 Dove Milk Chocolate, 1 piece = 1 PPV, 5 pieces = 6 Dove Milk Chocolate, 1 piece = 1 PPV, 5 pieces = 6 PPV PPV PPV Gummi Bears, 14 pieces = 3 PPV Gummi Bears, 14 pieces = 3 PPV Gummi Bears, 14 pieces = 3 PPV Heath, miniatures, 6 pieces = 7 PPV Heath, miniatures, 6 pieces = 7 PPV Heath, miniatures, 6 pieces = 7 PPV Hershey’s milk chocolate bar, snack size = 6 PPV Hershey’s milk chocolate