Pawn Stars: Putting Theories of Negotiation to the Test

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Glitz and Glam

FINAL-1 Sat, Feb 24, 2018 5:31:17 PM Glitz and glam The biggest celebration in filmmaking tvspotlight returns with the 90th Annual Academy Your Weekly Guide to TV Entertainment Awards, airing Sunday, March 4, on ABC. Every year, the most glamorous people • For the week of March 3 - 9, 2018 • in Hollywood stroll down the red carpet, hoping to take home that shiny Oscar for best film, director, lead actor or ac- tress and supporting actor or actress. Jimmy Kimmel returns to host again this year, in spite of last year’s Best Picture snafu. OMNI Security Team Jimmy Kimmel hosts the 90th Annual Academy Awards Omni Security SERVING OUR COMMUNITY FOR OVER 30 YEARS Put Your Trust in Our2 Familyx 3.5” to Protect Your Family Big enough to Residential & serve you Fire & Access Commercial Small enough to Systems and Video Security know you Surveillance Remote access 24/7 Alarm & Security Monitoring puts you in control Remote Access & Wireless Technology Fire, Smoke & Carbon Detection of your security Personal Emergency Response Systems system at all times. Medical Alert Systems 978-465-5000 | 1-800-698-1800 | www.securityteam.com MA Lic. 444C Old traditional Italian recipes made with natural ingredients, since 1995. Giuseppe's 2 x 3” fresh pasta • fine food ♦ 257 Low Street | Newburyport, MA 01950 978-465-2225 Mon. - Thur. 10am - 8pm | Fri. - Sat. 10am - 9pm Full Bar Open for Lunch & Dinner FINAL-1 Sat, Feb 24, 2018 5:31:19 PM 2 • Newburyport Daily News • March 3 - 9, 2018 the strict teachers at her Cath- olic school, her relationship with her mother (Metcalf) is Videoreleases strained, and her relationship Cream of the crop with her boyfriend, whom she Thor: Ragnarok met in her school’s theater Oscars roll out the red carpet for star quality After his father, Odin (Hop- program, ends when she walks kins), dies, Thor’s (Hems- in on him kissing another guy. -

To View & Download My Resume

NAWARA BLUE Producer Driven, organized, detail- WORK EXPERIENCE oriented, and creative professional with extensive Roll Up Your Sleeves (2021 COVID Vaccination Special)- Producer NBC/ Camouflage Films, Inc. (Houston, TX) experience in television production. Skillset includes Put A Ring On It (Season 2)- Supervising Field Producer cultivating stories, tracking OWN / Lighthearted ENT (Atlanta, GA) multiple storylines, producing and directing large cast. Skilled Ready to Love (Season 4)- Supervising Field Producer OWN / Lighthearted ENT (Houston, TX) in talent and crew management, control room and Self Employed (Pilot)- Supervising Field Producer floor producing, and directing Magnolia / Red Productions (Dallas, TX) multiple cameras. Experienced in conducting and writing formal Supa Girlz (Season 1 Documentary)- Supervising Field Producer interviews and OTFs. Proficient in HBO MAX / Film-45 (Miami, FL) scheduling, budgeting, casting, Bride & Prejudice (Season 2)- Supervising Producer clearing locations, writing hot TLC/ Kinetic Content (Atlanta, GA) sheets, outlines, beat sheets, creative decks, show bibles, and Little Women Atlanta (Season 6)- Senior Field Producer any other pertinent production Lifetime/ Kinetic Content (Atlanta, GA) documents. Look Me in The Eye (Pilot)- Senior Field Producer OWN/ Kinetic Content (Los Angeles, CA) Digital proficiencies include Microsoft Office, Google Drive, The American Barbeque Showdown (Season 1)- Field Producer and Social Media platforms. Netflix/ All 3 Media (Atlanta, GA) Love Is Blind (Season 1)- Field Producer EDUCATION Netflix/ Delirium TV, LLC (Atlanta, GA) WAYNE STATE UNIVERSITY, DETROIT MI 2006-2010 Teen Mom 2 (Season 16)- Field Producer Bachelor of Arts, Public Relations MTV/ MTV (Orlando, FL) Member of Alpha Kappa Alpha Sorority Inc. Beta Mu Chapter Married at First Sight: Honeymoon Island (Season 1)- Field Producer Lifetime/ Kinetic Content (Los Angeles, CA & St. -

Lemons, Market Shutdowns and Learning

Lemons, Market Shutdowns and Learning Pablo Kurlat ∗ MIT Job Market Paper November 2009 Abstract I study a dynamic economy featuring adverse selection in financial markets. Investment is undertaken by borrowing-constrained entrepreneurs. They sell their past projects to finance new ones, but asymmetric information about project quality creates a lemons problem. The magnitude of this friction responds to aggregate shocks, amplifying the responses of asset prices and investment. Indeed, negative shocks can lead to a complete shutdown in financial markets. I then introduce learning from past transactions. This makes the degree of informational asymmetry endogenous and makes the liquidity of assets depend on the experience of market participants. Market downturns lead to less learning, worsening the future adverse selection problem. As a result, transitory shocks can create highly persistent responses in investment and output. (JEL E22, E44, D83, G14) ∗I am deeply indebted to George-Marios Angeletos, Ricardo Caballero, Bengt Holmstr¨om and especially Iv´an Werning for their invaluable guidance. I also thank Daron Acemoglu, Sergi Basco, Francisco Buera, Mart´ın Gonzalez-Eiras, Guido Lorenzoni, Julio Rotemberg, Jean Tirole, Robert Townsend and seminar participants at the MIT Macroeconomics Lunch, Theory Lunch and International Breakfast, the LACEA-LAMES 2009 Meeting and the Federal Reserve Board for useful suggestions and comments. All remaining errors are my own. Correspondence: Department of Economics, MIT, Cambridge, MA 02142. Email: [email protected] 1 1 Introduction Financial markets are fragile, volatile and occasionally shut down entirely. The recent financial crisis has intensified economists’ interest in understanding the causes of financial instability and its effects on real economic variables such as investment, output and productivity. -

When Does Behavioural Economics Really Matter?

When does behavioural economics really matter? Ian McAuley, University of Canberra and Centre for Policy Development (www.cpd.org.au) Paper to accompany presentation to Behavioural Economics stream at Australian Economic Forum, August 2010. Summary Behavioural economics integrates the formal study of psychology, including social psychology, into economics. Its empirical base helps policy makers in understanding how economic actors behave in response to incentives in market transactions and in response to policy interventions. This paper commences with a short description of how behavioural economics fits into the general discipline of economics. The next section outlines the development of behavioural economics, including its development from considerations of individual psychology into the fields of neurology, social psychology and anthropology. It covers developments in general terms; there are excellent and by now well-known detailed descriptions of the specific findings of behavioural economics. The final section examines seven contemporary public policy issues with suggestions on how behavioural economics may help develop sound policy. In some cases Australian policy advisers are already using the findings of behavioural economics to advantage. It matters most of the time In public policy there is nothing novel about behavioural economics, but for a long time it has tended to be ignored in formal texts. Like Molière’s Monsieur Jourdain who was surprised to find he had been speaking prose all his life, economists have long been guided by implicit knowledge of behavioural economics, particularly in macroeconomics. Keynes, for example, understood perfectly the “money illusion” – people’s tendency to think of money in nominal rather than real terms – in his solution to unemployment. -

You Can Bet on That TV Listings 2014-12-17 Through 2014-12-30

You Can Bet on That TV Listings 2014-12-17 through 2014-12-30 All times are Eastern or Eastern/Pacific. Movie ratings are from one to four stars. New shows are highlighted in green. 2014 World Series of Poker From Las Vegas. Sports event, Series, 60 min. SUN, DEC 28, 2014, 4:00 PM ESPN SUN, DEC 28, 2014, 8:00 PM ESPN2 SUN, DEC 28, 2014, 9:00 PM ESPN2 2014 World Series of Poker "Final Table" From Las Vegas. Sports event, Series, 120 min. SUN, DEC 28, 2014, 5:00 PM ESPN SUN, DEC 28, 2014, 10:00 PM ESPN2 2014 World Series of Poker APAC From Melbourne, Australia. Sports event, Series, 60 min. SUN, DEC 21, 2014, 8:00 PM ESPN2 SUN, DEC 21, 2014, 9:00 PM ESPN2 SUN, DEC 21, 2014, 10:00 PM ESPN2 SUN, DEC 21, 2014, 11:00 PM ESPN2 21 Students (Jim Sturgess, Kate Bosworth) from the Massachusetts Institute of Technology become experts at card-counting and use the skill to win big at Las Vegas casinos. Drama, Movie (2008 ★★½), 150 min. TUE, DEC 23, 2014, 6:30 PM Esquire TUE, DEC 23, 2014, 11:00 PM Esquire 90 Day Fiance "I'm Gonna Go Home" Chelsea panics before her wedding; Jason and Cassia try to fix their relationship problems in Las Vegas; Mohamed goes missing on Danielle; Brett has to choose between his mother and Daya. Reality, Series, 60 min. SUN, DEC 21, 2014, 9:00 PM TLC SUN, DEC 21, 2014, 11:01 PM TLC THU, DEC 25, 2014, 10:00 PM TLC FRI, DEC 26, 2014, 12:00 AM TLC SUN, DEC 28, 2014, 8:00 PM TLC MON, DEC 29, 2014, 2:00 AM TLC American Greed "The Tran Organization: Blackjack Cheaters" Van Thu Tran and her crime ring steal millions by cheating casinos. -

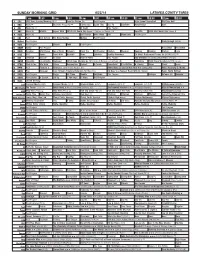

Sunday Morning Grid 6/22/14 Latimes.Com/Tv Times

SUNDAY MORNING GRID 6/22/14 LATIMES.COM/TV TIMES 7 am 7:30 8 am 8:30 9 am 9:30 10 am 10:30 11 am 11:30 12 pm 12:30 2 CBS CBS News Sunday Morning (N) Å Face the Nation (N) Paid Program High School Basketball PGA Tour Golf 4 NBC News Å Meet the Press (N) Å Conference Justin Time Tree Fu LazyTown Auto Racing Golf 5 CW News (N) Å In Touch Paid Program 7 ABC News (N) Wildlife Exped. Wild 2014 FIFA World Cup Group H Belgium vs. Russia. (N) SportCtr 2014 FIFA World Cup: Group H 9 KCAL News (N) Joel Osteen Mike Webb Paid Woodlands Paid Program 11 FOX Paid Joel Osteen Fox News Sunday Midday Paid Program 13 MyNet Paid Program Crazy Enough (2012) 18 KSCI Paid Program Church Faith Paid Program 22 KWHY Como Paid Program RescueBot RescueBot 24 KVCR Painting Wild Places Joy of Paint Wyland’s Paint This Oil Painting Kitchen Mexican Cooking Cooking Kitchen Lidia 28 KCET Hi-5 Space Travel-Kids Biz Kid$ News LinkAsia Healthy Hormones Ed Slott’s Retirement Rescue for 2014! (TVG) Å 30 ION Jeremiah Youssef In Touch Hour of Power Paid Program Into the Blue ›› (2005) Paul Walker. (PG-13) 34 KMEX Conexión En contacto Backyard 2014 Copa Mundial de FIFA Grupo H Bélgica contra Rusia. (N) República 2014 Copa Mundial de FIFA: Grupo H 40 KTBN Walk in the Win Walk Prince Redemption Harvest In Touch PowerPoint It Is Written B. Conley Super Christ Jesse 46 KFTR Paid Fórmula 1 Fórmula 1 Gran Premio Austria. -

Tv Pg 6 3-2.Indd

6 The Goodland Star-News / Tuesday, March 2, 2009 All Mountain Time, for Kansas Central TIme Stations subtract an hour TV Channel Guide Tuesday Evening March 2, 2010 7:00 7:30 8:00 8:30 9:00 9:30 10:00 10:30 11:00 11:30 28 ESPN 57 Cartoon Net 21 TV Land 41 Hallmark ABC Lost Lost 20/20 Local Nightline Jimmy Kimmel Live S&T Eagle CBS NCIS NCIS: Los Angeles The Good Wife Local Late Show Letterman Late 29 ESPN 2 58 ABC Fam 22 ESPN 45 NFL NBC The Biggest Loser Parenthood Local Tonight Show w/Leno Late 2 PBS KOOD 2 PBS KOOD 23 ESPN 2 47 Food FOX American Idol Local 30 ESPN Clas 59 TV Land Cable Channels 3 KWGN WB 31 Golf 60 Hallmark 3 NBC-KUSA 24 ESPN Nws 49 E! A&E Criminal Minds CSI: Miami CSI: Miami Criminal Minds Local 5 KSCW WB 4 ABC-KLBY AMC To-Mockingbird To-Mockingbird Local 32 Speed 61 TCM 25 TBS 51 Travel ANIM 6 Weather Wild Recon Madman of the Sea Wild Recon Untamed and Uncut Madman Local 6 ABC-KLBY 33 Versus 62 AMC 26 Animal 54 MTV BET National Security Vick Tiny-Toya The Mo'Nique Show Wendy Williams Show Security Local 7 CBS-KBSL BRAVO Mill. Matchmaker Mill. Matchmaker Mill. Matchmaker Mill. Matchmaker Matchmaker 7 KSAS FOX 34 Sportsman 63 Lifetime 27 VH1 55 Discovery CMT Local Local Smarter Smarter Extreme-Home O Brother, Where Art 8 NBC-KSNK 8 NBC-KSNK 28 TNT 56 Fox Nws CNN 35 NFL 64 Oxygen Larry King Live Anderson Cooper 360 Larry King Live Anderson Local 9 Eagle COMEDY S. -

Recovering Six Nations' Heritage in Wampums by Stephanie Dearing Explaining His Wife Had Giv Torian Keith Jamieson

Recovering Six Nations' heritage in wampums By Stephanie Dearing explaining his wife had giv torian Keith Jamieson. SIX NATIONS en him instructions to sell But while price presents the plate at a certain price. a rather large stumbling Watching a silver breast The breast plate had been in block, it's one of the least plate, originally given to Six his wife's family for some problems in bringing some Nations by the British dur time, he said. His wife's thing back to where it right ing the negotiations of the mother was a Blackfoot. fully belongs. 1784 Fort Stanwix Treaty, The Silver Dollar shop "The problem is, we don't being sold to a pawn shop owners had an expert come know how they [the seller] featured on the popular tele in to appraise the breast got it," said Jamieson. "Un vision series, Cajun Pawn plate, which was valued less we can find the prov Stars, shocked Brenda Ma at an estimated $25,000 to enance to it, and it was racle Hill, who wondered if $30,000. According to the stolen and they bought sto the breast plate could be re expert, the plate was giv len property, then we· have covered. en to Six Nations Iroquois a shot. But if it was bought "That's ours," Brenda at Fort Stanwix at the sign legitimately from whoever said, explaining how she ing of the 1874 treaty, which received it, then there's not felt upon realizing the breast took place after the Ameri much you can say." plate was historically signif can War of Independence. -

TV Listings SATURDAY, APRIL 1, 2017

TV listings SATURDAY, APRIL 1, 2017 03:00 Man Fire Food 01:20 The Unexplained Files 03:30 Man Fire Food 02:10 How The Earth Works 04:00 Chopped 03:00 The Big Brain Theory 05:00 Guy's Grocery Games 03:48 Mythbusters 06:00 Roadtrip With G. Garvin 04:36 How Do They Do It? 06:30 Roadtrip With G. Garvin 05:00 Food Factory 07:00 Chopped 05:24 The Unexplained Files 08:00 Barefoot Contessa: Back To Basics 06:12 How The Earth Works 08:30 Barefoot Contessa: Back To Basics 07:00 How Do They Do It? 09:00 The Pioneer Woman 07:26 Food Factory 09:30 The Pioneer Woman 07:50 Food Factory 10:00 Siba's Table 08:14 Food Factory 10:30 Siba's Table 08:38 Food Factory 11:00 Anna Olson: Bake 09:02 Food Factory 11:30 Anna Olson: Bake 09:26 How Do They Do It? 12:00 Man Fire Food 09:50 How Do They Do It? 12:30 Man Fire Food 10:14 How Do They Do It? 13:00 Diners, Drive-Ins And Dives 10:38 How Do They Do It? 13:30 Diners, Drive-Ins And Dives 11:02 How Do They Do It? 14:00 Chopped 11:26 How The Earth Works 15:00 Barefoot Contessa: Back To Basics 12:14 How The Earth Works 15:30 Barefoot Contessa: Back To Basics 13:02 How The Earth Works 16:00 The Pioneer Woman 13:50 How The Earth Works 16:30 The Pioneer Woman 14:38 How The Earth Works 17:00 Siba's Table 15:26 Mythbusters 17:30 Siba's Table 16:14 Mythbusters 18:00 Anna Olson: Bake 17:02 Mythbusters 18:30 Anna Olson: Bake 17:50 Mythbusters 19:00 Man Fire Food 18:40 Mythbusters 19:30 Man Fire Food 19:30 NASA's Unexplained Files 20:00 Diners, Drive-Ins And Dives 20:20 Sport Science 20:30 Diners, Drive-Ins And Dives 21:10 -

Less Rationality, More Efficiency: a Laboratory Experiment on “Lemon”

Less Rationality, More Efficiency: a Laboratory Experiment on “Lemon” Markets.y Roland Kirstein¤ Annette Kirstein¤¤ Center for the Study of Law and Economics Discussion Paper 2004-02 Abstract We have experimentally tested a theory of bounded rational behav- ior in a “lemon market”. It provides an explanation for the observation that real world players successfully conclude transactions when perfect rationality predicts a market collapse. We analyzed two different market designs: complete and partial market collapse. Our empirical observations deviate substantially from these theoretical predictions. In both markets, the participants traded more than theoretically predicted. Thus, the ac- tual outcome is closer to efficiency than the theoretical prediction. Even after 20 repetitions of the first market constellation, the number of trans- actions did not drop to zero. Our bounded rationality approach to explain these observations starts with the insight that perfect rationality would require the players to per- form an infinite number of iterative reasoning steps. Bounded rational players, however, carry out only a limited number of such iterations. We have determined the iteration type of the players independently from their market behavior. A significant correlation exists between iteration types and observed price offers. JEL classification: D8 , C7, B4 Encyclopedia of Law and Economics: 0710, 5110 Keywords: guessing games, beauty contests, market failure, adverse selection, lemon problem, regulatory failure, paternalistic regulation yWe are grateful to Max Albert, George Akerlof, Ted Bergstrom, Friedel Bolle, Ralf Fried- mann, Rod Garrat, Hans Gerhard, Wolfgang Kerber, Manfred K¨onigstein,G¨oranSkogh, Dieter Schmidtchen, Jean-Robert Tyran and other seminar and conference participants in Hamburg, Karlsruhe, Kassel, Saarbruecken, Santa Barbara and Zurich for valuable comments (the usual disclaimer applies). -

The Revolution of Information Economics: the Past and the Future

NBER WORKING PAPER SERIES THE REVOLUTION OF INFORMATION ECONOMICS: THE PAST AND THE FUTURE Joseph E. Stiglitz Working Paper 23780 http://www.nber.org/papers/w23780 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 September 2017 I wish to acknowledge research assistance from Andrew Kosenko and editorial assistance from Debarati Ghosh. The views expressed herein are those of the author and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2017 by Joseph E. Stiglitz. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. The Revolution of Information Economics: The Past and the Future Joseph E. Stiglitz NBER Working Paper No. 23780 September 2017 JEL No. B21,D82,D83 ABSTRACT The economics of information has constituted a revolution in economics, providing explanations of phenomena that previously had been unexplained and upsetting longstanding presumptions, including that of market efficiency, with profound implications for economic policy. Information failures are associated with numerous other market failures, including incomplete risk markets, imperfect capital markets, and imperfections in competition, enhancing opportunities for rent seeking and exploitation. This paper puts into perspective nearly a half century of research, including recent advances in understanding the implications of imperfect information for financial market regulation, macro-stability, inequality, and public and corporate governance; and in recognizing the endogeneity of information imperfections. -

Counting Cars

FOR IMMEDIATE RELEASE HISTORY® Revs Up for More Wheeling and Dealing When Danny ‘The Count’ Koker Returns to the Driver’s Seat for an All-New Season of… COUNTING CARS New York, NY – His name is The Count, and his game is one-of-a-kind, customized classic cars and motorcycles. Danny “The Count” Koker doesn’t just love hot rods and choppers. He lives for them. Whether it’s a ’63 Corvette, a classic Thunderbird, a muscle-bound Trans Am, or a yacht-sized Caddy, he knows these high-performance beauties inside and out. What’s more, he’ll do anything it takes to get his hands on those he likes – he’s known for pulling over cars he passes on the road and offering cash for them on the spot, or for using a retailer’s PA system to lure a car owner back to the parking lot to make a deal – and then “flip” them for a profit. Danny and the crew from Count’s Kustoms, his Vegas-based auto repair business, are behind the wheel again for a new season of COUNTING CARS, premiering Tuesday, April 9 at 9pm ET on HISTORY. The heat is on as the boys buy, trick out and re-sell classic cars, bikes and more. Danny is obsessed, so the more rides he buys, the faster they have to move to keep Count’s Kustoms in business. This season’s projects span all eras of cars, trucks, bikes and trikes. They’ll be working with Ziggy Marley to restore and customize Bob Marley’s last car, a 1980 Mercedes 500SL Euro; and customizing a soap box derby car for a youngster.