August 19, 2015

To: Board of Directors

From: John Pamer

RE: Auto Loan Participation opportunity

EXECUTIVE SUMMARY: The current pool being offered is through a broker relationship with ABC Financial Services (a subsidiary of ABC Credit Union). The originating credit union is Sample FCU, based in Tampa, FL. Sample’s financials indicates a well-managed credit union and a well-managed indirect auto loan program.

FACTS: Internal auto loan demand remains weak. As we have discussed in previous meetings, the majority of auto lending is now done indirectly. We lack the infrastructure to service a large indirect loan operation. We wish to continue to diversify our loan mix, and not rely on mortgage loan volume to supply our loan growth.

We purchased a participation pool from Sample FCU in July 2013 for $2,130,515. The current remaining balance on that pool is $807,364. That pool had an average credit score of 661 and has seen no charge- offs to date. In May of 2014 we purchased a second pool from Sample FCU for $2,154,103, with a current remaining balance of $1,446,276. That pool had an average credit score of 667 and has seen net charge offs of $6,342, or .29% of the original balance.

The new pool purchase would be approximately $2,574,060, giving us a total outstanding amount of approximately $4,827,700 in indirect pool loans with Sample FCU. Per NCUA regulations we can have up to $5,000,000 in participation loans with a single entity.

THE SELLING CREDIT UNION: Sample FCU in Tampa, FL--Federal Charter #12345. Financial Highlights as of June 30, 2015:

$91.9 Million in assets

.77% ROA

9.48% Net worth ratio

$58.4 Million in outstanding indirect loans

.38% reportable delinquency in indirect loans

.26% net charge off ratio in indirect loans

Federal charter: examined by NCUA

THE POOL FOR SALE: 90% of $2,860,067, approximately $2,574,060. Final amount at settlement will differ based on payments received.

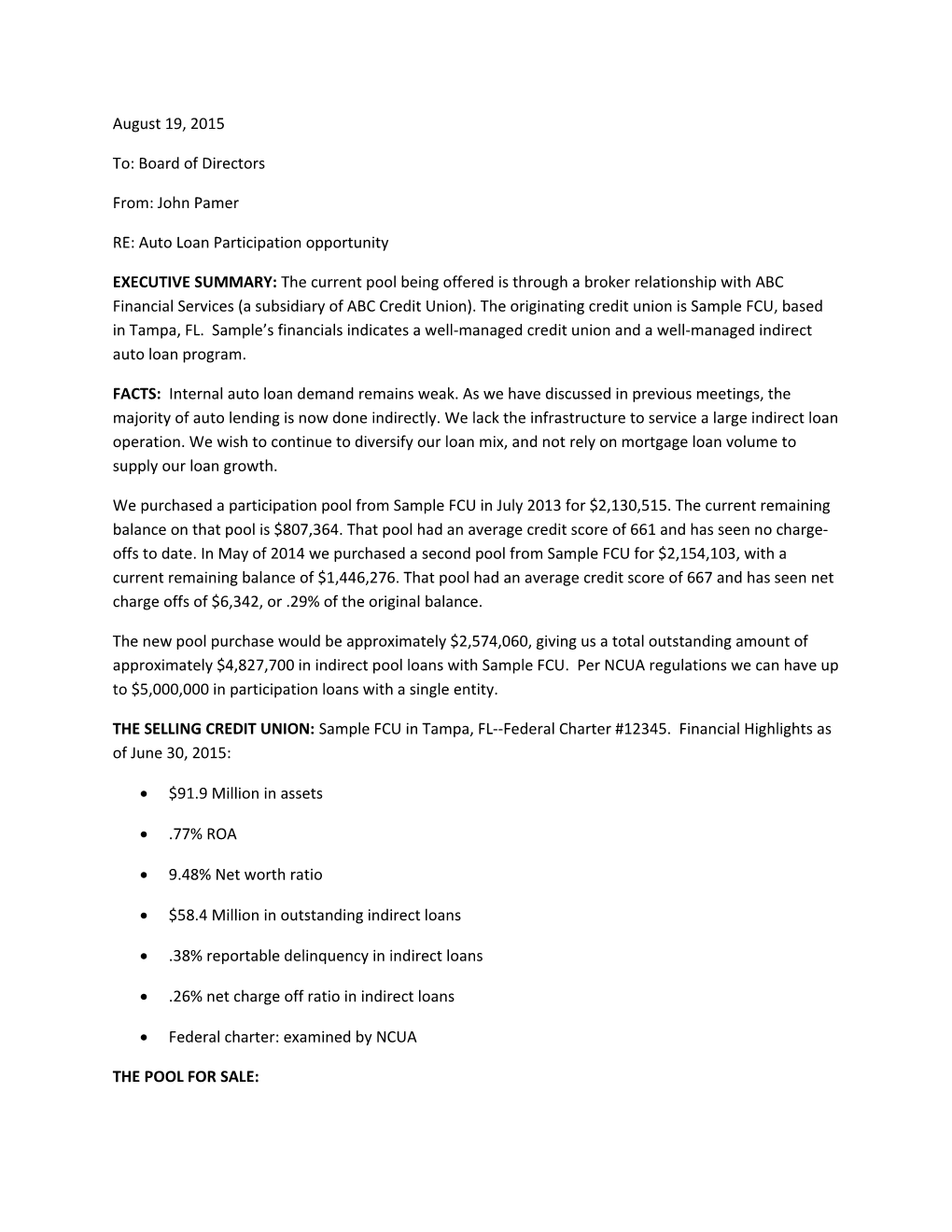

Risk weighting:

Row Labels Count of Risk Group Sum of Average of Interest Balance Rate A 37 $851,174.30 3.26 B 34 $989,935.84 6.00 C 22 $613,215.45 8.39 D 13 $306,486.39 10.28 E 4 $99,254.81 13.72 Grand Total 110 $2,860,066.79 6.34

Pass Through Coupon: 3.88%

Average credit score of overall pool: 663

Loans seasoned at least 3 months

No Repos

No Bankrupts

Indirect Loans

Balance $5,000 +

Cars/Trucks/Motorcycles

No loans delinquent more than ten days

No loans have reported delinquency 29 days

No loans have reported 11-30 days more than 5 times

Sample FCU is offering a pass through rate of 3.88% on this portfolio. The broker fee to ABC Financial is .375% of the funded amount, approximately $9,653.

ALTERNATIVES:

Since purchasing a pool from ABC Credit Union in late 2014, we have sought additional sellers of auto loan portfolios. We have received the following proposals:

1. A pool of $1.2 Million Direct Autos from XYZ Credit Union for a price of 101 plus 25 basis points servicing and a yield of 2.25%. 2. A pool of $1.2 Million indirect autos from XYZ Credit union at a price of 104 plus 25 basis points servicing for a yield of 2.25%.

3. A pool of direct and indirect autos from PDQ Financial Services with a pass through rate of 3.41%, a price of 101.5 plus 25 basis points servicing plus 25 basis points commission. Average credit score 704. Expected yield 2.5 to 2.6%

4. A pool of direct autos from PDQ Services with a pass through rate of 2.62%. Purchase price is par with a 25 basis point fee to LPC.

These offers are not as attractive as the Sample FCU offering.

RISK ANALYSIS:

1. Liquidity Risk

o With over $5.7 Million in short-term CD’s (most less than 1 year remaining) and $5.5 + Million in overnight funds held at Catalyst, we have ample liquidity to fund this purchase.

2. Credit Risk

o We will establish an allowance for loan loss equal to .5% of the portfolio (note this is higher than Sample FCU’s charge off ratio of .26%). As losses occur, we would transition to our standard one year ALLL calculation.

3. Transaction Risk

o Sample FCU has extensive experience underwriting indirect auto loan, and as evidenced by their financial reports, they have adequate collection and recovery controls in place.

4. Interest Rate Risk

o Because of the relatively short duration, the pool would only decline approximately 3-5% in an up 300 basis point shock scenario. This compares favorably to mortgage loans, which typically decline 15%-20% in an up 300 basis point shock scenario.

5. Concentration Risk

o Per NCUA regulations, we can have up to $5 Million in outstanding loan participations with a single entity. We will ensure that the aggregate total of C, D and E paper does not exceed 60% of our net worth, as required by our policy.

PROFIT AND LOSS ESTIMATE:

Revenue: $261,900, assuming a five year life

Credit Losses: $33,000, assuming .50% charge off rate Brokerage fee: $9,650

Opportunity Cost: $66,000, assuming 1% return on alternate investments

Net margin: $153,250.

DUE DILIGENCE WE WILL PERFORM:

Prior to acceptance of the portfolio for purchase, we will request a 15% sample of loan files of our choosing. We will evaluate the original loan file and document our findings. We reserve the right to reject certain loans or the entire pool if we determine such loans are not properly underwritten or otherwise pose undue risk.

RECOMMENDATION:

Approve the purchase of the loan pool from Sample FCU for up to $2,574,000, subject to due diligence underwriting to be performed by Diablo Valley FCU.

ATTACHMENTS:

Alternative pool summary offered by XYZ

Alternative pool summary offered by PDQ Services

FPR Financial Summary of Sample FCU

FPR Ratio Analysis of Sample FCU