November 4, 2009

Research Analyst: Tanuka De, M. Com., MBA Zacks Research Digest Sr. Ed.: Ian Madsen, CFA; [email protected]; 1-800-767-3771, x9417

www.zackspro.com 111 N. Canal Street, Suite 1101 Chicago, IL 60606 Allegheny Technologies Inc. (ATI – NYSE) $31.64*

Note: This report contains substantially new material. Subsequent reports will have changes highlighted.

Reason for Report: 3Q09 Earnings Update

Previous Edition: Minor change in estimates, September 10, 2009 (broker material considered till September 1, 2009)

Brokers’ Recommendations: Neutral: 50.0% (5 firms); Negative: 30.0% (3); Positive: 20.0% (2) Prev. Ed.: 7; 2; 2

Brokers’ Target Price: $34.79 (↑ $4.47 from the last edition; 7 firms) Brokers’ Avg. Expected Return: 9.9%

*NOTE: Though dated November 4, 2009, share price and broker material are as of October 29, 2009.

A Flash Update on 3Q09 Earnings was done on October 21, 2009.

Note: The tables below (Revenue, Margins, and Earnings per Share) contain less broker material than the broker material used in the Valuation table. The extra figures in the Valuation table come from reports that did not have accompanying spreadsheet models.

Portfolio Manager Executive Summary

Allegheny Technologies Incorporated (ATI or the Company) is one of the largest and most diversified specialty metals producers in the world. ATI uses innovative technologies to offer growing global markets a wide range of specialty metals solutions. Its products include titanium and titanium alloys, nickel-based alloys and superalloys, stainless and specialty steels, zirconium, hafnium, and niobium, tungsten materials, grain-oriented electrical steel, and forgings and castings, while its major markets are aerospace and defense, chemical process industry/oil and gas, electrical energy, medical, automotive, food equipment and appliance, machine and cutting tools, and construction and mining.

Of the 9 firms covering the stock 50.0% hold a cautious outlook, 30.0% of the firms provided a negative outlook while the remaining 20.0% rendered positive rating. The firm with the highest target price of $45.00 provided a Buy rating, and based the valuation on EV/2010E EBITDA multiple of 11x. The firm with the lowest target price of $25.00 provided a Sell rating and based the valuation on a price-to-book multiple of 1.3x.

Neutral and negative or equivalent outlook – Eight analysts or 70.0% - Target prices range from $25.00 to $35.00. These firms believe that Boeing delays and a stuffed titanium supply chain would remain an overhang over ATI’s earnings well into 2010. In addition, the firms remain concerned due to decline in the commercial aerospace production, weak end market demand trends, and continued high capital spending plans. The Company's commodity stainless steel business also remains a concern, given exposure to consumer-linked end markets and industry capacity growth concerns.

© Copyright 2009, Zacks Investment Research. All Rights Reserved. However, the firms consider ATI’s significantly more diverse product offering and end market exposure compared to its pure-play titanium peers, RTI International Metals, INC (RTI) and Titanium Metals Corp. (TIE), reduce its risk to the overall aerospace/titanium cycle. Furthermore, should aerospace fundamentals meaningfully lag an overall economic recovery, ATI’s diversified market exposure may help it achieve mid-cycle earnings ahead of its peers. Firms favor ATI’s long-term position, value-added approach, and end-market exposure.

Positive or equivalent outlook – Two analysts or 20.0% - Target prices range from $42.00 to $45.00. The firms believe that ATI has a strong balance sheet and has positioned itself very well for future growth through strategic investments, limited debt maturities, and cost reduction efforts, and thus has value for the long-term investors. November 4, 2009

Recent Events

On October 26, 2009, ATI completed the purchase of the assets of Crucible Compaction Metals and Crucible Research for $40.95 million. ATI also announced that the business has been named ATI Powder Metals.

On October 21, 2009, ATI announced its 3Q09 financial results. Highlights are as follows:

Total revenue was $697.6 million, compared with $1,392.4 million in 3Q08. Segment operating profit was $54.0 million, or 7.7% of sales, compared with $251.4 million, or 18.1% of sales, in 3Q08. Net income was $1.4 million, compared with $144.1 million in 3Q08. EPS was $0.01, compared with $1.45 in 3Q08.

Overview

The firms have identified the following key factors for evaluating the investment merits of ATI:

Key Positive Arguments Key Negative Arguments Accelerating Growth: ATI has increased its Global Recession: Global recession could cause production targets, and is coming up with many new end markets to fall, resulting in decreased revenues. projects and new contracts. Exposure to Aerospace: ATI is heavily exposed to Global Presence: ATI is becoming more and more aerospace as 25% of ATI’s sales come from global. ATI's increasing global influence is a positive aerospace. Aerospace, in turn, has been a move to diversify its market risk of being too historically cyclical industry and any downturn in dependent on the US market alone. aerospace would have a negative effect on the Financials: ATI continues to have a strong balance Company. sheet and generate commendable cash flow, which Execution Risk: The announced capacity enables the Company to undertake additional expansion projects and cost-cutting initiatives run a expansion plans or possibly make bolt-on high risk of execution. acquisitions. Downturn in Titanium Market: ATI is spending on Exotic Alloys: Improved pricing and margins in the a significant amount of capital, expanding its exotic alloys segment partially offsets weakness in Titanium production capacity. These projects may titanium and nickel-based alloys, which leads to not yield positive IRRs if the global titanium market strength in the nuclear energy end market. take a downturn due to problems in the aerospace market or overbuild of capacity.

Zacks Investment Research Page 2 www.zackspro.com Allegheny Technologies Incorporated (ATI or the Company), based in Pittsburgh, Pennsylvania, is a diversified producer of specialty materials. The Company markets its products to aerospace and defense, chemical processing, oil and gas, electrical energy, construction and mining, chemical, automotive, food processing equipment and appliances, machine and cutting tools, power generation, transportation, and medical industries. The three main business segments of the Company are as follows:

Flat-Rolled Products (FRP): This segment produces, converts, and distributes stainless steel, nickel- based alloys and super-alloys, and titanium and titanium-based alloys in various forms.

High-Performance Metals (HPM): This segment produces, converts, and distributes nickel and cobalt- based alloys and super-alloys, titanium and titanium-based alloys, zirconium, hafnium, niobium, tantalum, their related alloys, and other specialty materials.

Engineered Products (EP): This segment produces tungsten powder, tungsten carbide materials, and carbide cutting tools. This segment also produces large gray and ductile iron castings and carbon alloy steel forgings.

Further information on the Company is available at http://www.alleghenytechnologies.com/.

NOTE: The Company’s fiscal year coincides with the calendar year. November 4, 2009

Revenue

CONSENSUS PROJECTED SALES

Total Revenue 3Q08A 2Q09A 3Q09A 4Q09E 1Q10E 2008A 2009E 2010E 2011E ($ in million) Zacks Consensus $739.0↓ $812.0 $2,975.0 ↓ $3,380.0↓ $1,392. Digest High 4 $710.0 $697.6 $745.9 ↓ $834.2 $5,310.0 $3,010.0 ↓ $3,929.0↓ $4,860.0 $1,392. Digest Low 4 $710.0 $697.6 $712.5 $834.2 $5,309.7 $2,924.8↓ $3,157.7↑ $4,357.7 $1,392. Digest Average 4 $710.0 $697.6 $729.2↓ $834.2 $5,309.7 $2,967.9↓ $3,561.1↓ $4,608.9 Digest Y/Y Growth 4.3% -51.4% -49.9% -34.5% 0.3% -2.6% -44.1% 20.0% 29.4% Sequential Growth -4.7% -14.6% -1.7% 4.5% 14.4%

3Q09 Summary: The Company reported sales of $697.6 million (in line with the Zacks Digest model), a y/y decline of 50% attributable to significantly lower raw material surcharges and indices and lower shipments. Direct international sales represented 31.0% of 3Q09 sales versus 29% in 3Q08.

One firm (KeyBanc) noted order activity from Asian customers is currently running at over twice the rate of 1H09, which should lead to higher shipment levels in early 2010. Furthermore, European customers have also begun to increase oil and gas orders, an encouraging sign given the degree of weakness in both the end market and the geography.

The Zacks Digest model compiled average revenue projections of $2,967.9 million for FY09, $3,561.1 million for FY10 and $4,608.9 million with a year-over-year decline of 44.1% and a growth of 20.0% and 29.4%, respectively.

Zacks Investment Research Page 3 www.zackspro.com SEGMENT REVENUE

Segment Revenue 3Q08A 2Q09A 3Q09A 4Q09E 1Q10E 2008A 2009E 2010E 2011E ($ M) $2,909. Flat Rolled $764.6 $335.2 $364.2 $338.1↓ 1 $1,415.7↓ $1,554.0↓ High Performance $1,944. Metals $510.2 $320.5 $279.2 $314.4↓ 9 $1,302.0↓ $1,711.0↑ Engineered Products $117.6 $54.3 $54.2 $60.0 ↓ $455.7 $234.0↓ $251.3 ↑ $1,392. $5,309. Total Revenue 4 $710.0 $697.6 $729.2 ↓ $834.2 7 $2,967.9↓ $3,561.1↓ $4,608.9

Note: Blank cells denote brokers did not provide figures.

Flat-Rolled Products (52.4% of 3Q09 sales): The Company reported sales of $364.2 million (in line with the Zacks Digest model), a y/y decline of 52%, primarily attributable to lower shipments and reduced raw material surcharges.

Shipments of standard stainless products (sheet and plate) decreased 3% y/y while total high-value products shipments decreased 32% y/y. Average transaction prices for all products, which include surcharges, were 42% lower due primarily to significantly reduced raw material surcharges.

Demand for certain high-value products, such as Precision Rolled Strip® products and nickel-based alloys, increased compared to 2Q09 while demand for grain-oriented electrical steel remained at reasonably good levels. Demand for most of standard stainless products remained low, yet improved 7% q/q. Additionally, average prices for standard stainless products increased 14% q/q primarily due to higher base selling prices and raw material surcharges

The firms project segment revenue to be $1,415.7 million for FY09 and $1,554.0 million for FY10, with year-over-year decline of 51.3% and growth of 9.8%, respectively.

High Performance Metals (40.0% of 3Q09 sales): The Company reported sales of $279.2 million (in line with the Zacks Digest model), a y/y decline of 42%.

Shipments decreased 37% y/y for both titanium and titanium alloys and nickel-based and specially alloys primarily due to lower demand from commercial aerospace market. Shipments of exotic alloys decreased 24% primarily due to the timing of projects for the chemical process industry. Average selling prices declined 23% y/y for titanium and titanium alloys and 21% y/y for nickel-based and specialty alloys primarily attributable to lower raw material indices as a result of lower raw material costs and a more competitive pricing environment. Average selling prices for exotic alloys increased 23% y/y due to increased demand for certain products and a favorable product mix.

Demand for titanium alloys and nickel-based alloys from the aerospace market was at significantly lower levels as the supply chain continued to adjust to aircraft production schedule push outs and reduced demand from the aero-engine aftermarket. Sequentially, shipment volumes for titanium alloys and nickel- based alloys declined 8% and 20%, respectively. Shipments of exotic alloys declined 23% q/q primarily due to timing of projects for the chemical process industry.

The firms project segment revenue to be $1,302.0 million for FY09 and $1,711.0 million for FY10, with year-over-year decline of 33.1% and 31.4%, respectively.

Zacks Investment Research Page 4 www.zackspro.com Engineered Products (7.8% of 3Q09 sales): The Company reported sales of $54.2 million (in line with Zacks Digest model), a y/y decline of 54%.

Demand for tungsten and tungsten carbide products, forged products, and cast products remained weak. Demand for precision finishing business was good.

The firms project segment revenue to be $234.0 million for FY09 and $251.3 million for FY10 with year- over-year decline of 48.7% in FY09 and a growth of 7.4% in FY10.

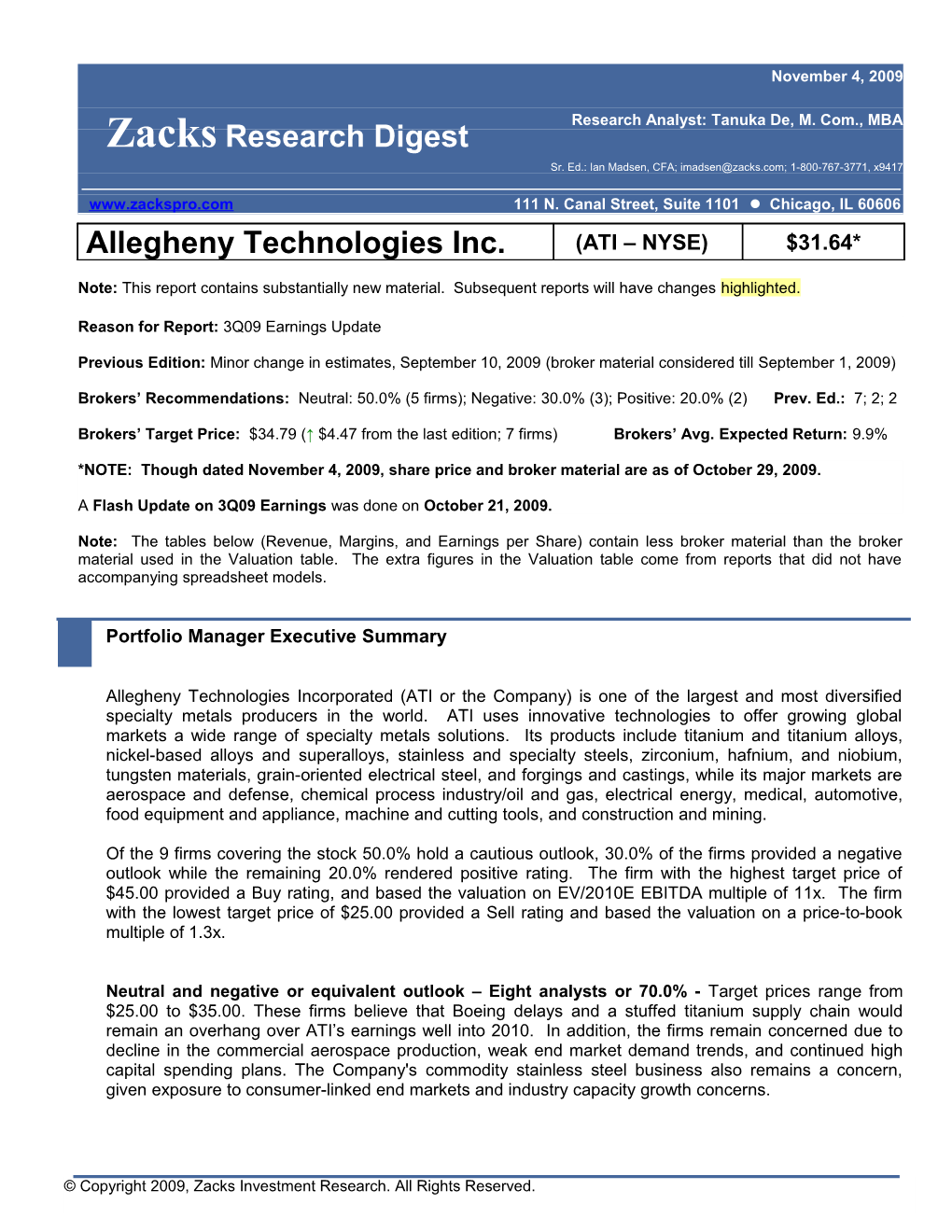

Provided below is a graphical representation of segment revenue:

2008A Re venue Segm e nts 2009E Revenue Segm ents

9% 8%

Flat Rolled Flat Rolled

48% 37% 54% High Performance High Performance Metals 44% Metals

Engineered Engineered Products Products

2010E Reve nue Se gm ents

7%

Flat Rolled

44% High Performance Metals 49% Engineered Products

Please refer to the Zacks Research Digest spreadsheet on ATI for more details.

Margins

CONSENSUS PROJECTED MARGINS

MARGINS 3Q08A 2Q09A 3Q09A 4Q09E 1Q10E 2008A 2009E 2010E 2011E Gross 22.0% 10.6% 21.7% 11.1%↑ 14.0%↓ Operating 16.7% 1.5% 1.5% 1.8%↓ 3.1% 16.4% 2.2%↑ 7.0%↓ 9.9%

Zacks Investment Research Page 5 www.zackspro.com Pre-Tax 16.4% 1.3% 0.4% 0.6%↓ 2.0% 16.2% -0.8%↓ 4.4%↓ 9.4% Net 10.3% 0.5% 0.2% 1.3%↑ 10.4% 0.5% 4.3%↓

Note: Blank cells denote brokers did not provide figures.

Cost of sales in 3Q09, as per the Zacks Digest model, was $603.5 million, down 44.4% y/y from $1,085.8 million in 3Q08.

SG&A expense in 3Q09, as per the Zacks Digest model, was $83.7 million, up 12.7% y/y from $74.3 million in 3Q08.

Segment operating profit was $54.0 million, or 7.7% of sales in 3Q09 versus $251.4 million, or 18.1% of sales, in 3Q08. Reported quarter results were negatively affected by lower shipments and by idle facility, workforce reduction, and startup costs of $18.9 million, partially offset by a LIFO inventory valuation reserve benefit of $4.5 million. The third quarter 2009 LIFO inventory valuation reserve benefit was $22.5 million lower than the LIFO reserve benefit recognized in 2Q09 due to rising raw material costs.

Corporate expenses in 3Q09 were $15.7 million, up from $13.4 million in 3Q08 driven by expenses associated with performance-based incentive compensation programs.

Operating profit, as per the Zacks Digest model was $10.7 million, down from $232.3 million in 3Q08. Operating margin in the reported quarter was 1.5% versus 16.7% in 3Q08.

The firms project operating income to be $66.2 million for FY09, $247.8 million for FY10 and $458.5 million in FY11, with a year-over-year decline of 92.4% and a growth of 274.6% and 85.0%, respectively.

Interest expense, net of interest income, was $8.1 million, up from $1.7 million in 3Q08 due to debt issuances completed in the second quarter of 2009.

3Q09 income tax was a benefit of $1.4 million. This resulted from an effective tax rate of 39.6%, reduced by an income tax benefit of $2.4 million for adjustment of taxes paid in a prior year. 3Q08 included an income tax provision of $83.9 million, or 36.3% of income before tax.

Net income in the reported quarter was $1.4 million versus $144.1 million in 3Q08. Net margin declined from 10.3% to 0.2% in 3Q09.

The firms project pro forma net income to be $15.4 million for FY09 and $151.9 million for FY10, with a year-over-year decline of 97.2% and a growth of 889.6%, respectively.

Expense outlook: The firms project cost of sales to decline at a slower rate than total revenue decline in FY09 (-37.3% versus -44.1%) affecting gross margin expansion. However, cost of sales is expected to grow at a slower rate than the growth in total revenue in FY10 (7.6% versus 20.0%) favoring gross margin expansion.

The firms project SG&A expense to increase versus total revenue decline in FY09 (6.3% versus -44.1%) inducing operating margin contraction. However, SG&A expense is expected to decline versus total revenue increase in FY10 (-3.5% versus 20.0%) and in FY11 (-7.2% versus 29.4%) driving operating margin expansion.

Zacks Investment Research Page 6 www.zackspro.com SEGMENT MARGINS

Margins 3Q08A 2Q09A 3Q09A 4Q09E 1Q10E 2008A 2009E 2010E 2011E Flat Rolled 13.4% 6.7% 3.1% 13.0% 3.8%↓ 10.5%↓ High Performance Metals 27.4% 12.8% 18.4% 27.7% 14.8%↑ 12.3%↑ Engineered Products 5.2% -17.3% -15.9% 4.6% -13.7%↑ -5.3%↑

Note: Blank cells denote brokers did not provide figures.

Flat-Rolled Products: Segment operating profit decreased to $11.3 million from $102.7 million in 3Q08. Operating profit was negatively impacted by lower shipments and approximately $6.0 million of costs associated with idle facilities and workforce reductions. Additionally, operating profit was negatively affected by a $6.8 million charge to adjust the LIFO inventory valuation reserve as a result of rising raw material costs. However, the segment benefited from $25.5 million in gross cost reductions. Operating margin was 3.1% in 3Q09 versus 13.4% in 3Q08.

The firms project segment profit to be $53.5 million for FY09 and $163.7 million for FY10, with year-over- year decline of 85.8%, and growth of 206.0%, respectively.

High Performance Metals: Segment operating profit decreased to $51.3 million from $139.6 million in 3Q08, attributable to lower base-selling prices for most products due to reduced demand and competitive pricing pressures and reduced shipments for most products. Operating profit was also negatively affected by approximately $11.7 million for idle facility, workforce reduction, and start-up costs partially offset by higher margins from exotic alloys and the benefits of gross cost reductions. A LIFO inventory valuation reserve benefit of $10.0 million was recognized in 3Q09. The segment benefited from $17.7 million of gross cost reductions.

The firms project segment profit to be $192.9 million for FY09 and $210.6 million for FY10, with year- over-year decline of 64.2%, and growth of 9.2%, respectively.

Engineered Products: The segment posted operating loss of $8.6 million versus an operating profit of $6.1 million in 3Q08 primarily due to significantly lower shipments, reduced selling prices, and costs associated with workforce reductions and idle facilities, partially offset by a $1.3 million LIFO benefit and the benefits of gross cost reductions. The segment results benefited from $4.0 million of gross cost reductions.

The firms project the segment to post a loss of $32.1 million for FY09 and $13.3 million for FY10, with year-over-year decline of 253.6%, and growth of 58.6%, respectively.

Outlook

One firm (Stifel Nicolaus) expects the Company to start production of new aircraft designs with high specialty alloy content in the near future, leading to increased volume. With increased volume, the firm believes that ATI will be able to attain operating margin in the mid-20% range given its significant operating leverage from recent capital expansion and improvement programs.

Zacks Investment Research Page 7 www.zackspro.com Please refer to the Zacks Research Digest spreadsheet on ATI for more details.

Earnings per Share

EPS in 3Q09 was $0.01, down from $1.45 in 3Q08 and $0.03 in 2Q09.

EPS 3Q08A 2Q09A 3Q09A 4Q09E 1Q10E 2008A 2009E 2010E 2011E Zacks Consensus $0.04↓ $0.21 $0.14↓ $1.25 ↓ Zacks Digest Max. $1.45 $0.03 $0.01 $0.10 ↓ $0.08 $5.67 $0.20↓ $1.86↓ $3.26 Zacks Digest Min. $1.45 $0.03 $0.01 $0.01↓ $0.08 $5.47 $0.10 ↓ $0.78↑ $2.30 Zacks Digest Avg. $1.45 $0.03 $0.01 $0.06 ↓ $0.08 $5.53 $0.14 ↓ $1.33 ↓ $2.78 Y/Y Growth -22.9% -98.1% -99.3% -95.0% 33.3% -23.8% -97.5% 846.4% 109.8% Sequential Growth -7.7% -50.0% -66.7% 450.0% 45.5%

Highlights from the EPS chart are as follows:

2009 forecasts (total 4 firms) range from $0.10 to $0.20; the average is $0.14. 2010 forecasts (total 4 firms) range from $0.78 to $1.86; the average is $1.33. 2011 forecasts (total 2 firms) range from $2.30 to $3.26; the average is $2.78.

Guidance: For 4Q09, the Company expects EPS to be similar to that achieved in 3Q09.

One firm (Goldman) lowered the estimate for 4Q09 primarily due to lower pricing and volume assumptions than previously expected.

Another firm (Longbow) lowered the estimates for FY09 and FY10 based on lower expectations for titanium and nickel-based alloy (NBA) shipments as well as higher interest and corporate expenses.

Another firm (J.P. Morgan) lowered the estimates for FY09 and FY10 to reflect a weaker-than-expected demand environment for ATI’s HPM segment, with the demand weakness only partially offset by a better- than-expected cost structure

One firm (UnionBankSwitz.) lowered the estimate for FY10 to reflect a slower volume recovery in 1H10.

One firm (KeyBanc) raised the estimate for 2010 driven entirely by a much lower pension expense assumption that now incorporates favorable fund asset returns.

As per the Zacks Digest model, the firms expect the share count to decrease by 2.1% y-o-y to 97.8 million by the end of FY09, increase by 0.2% to 97.9 million by the end of FY10 and by 0.1% y-o-y to 98.0 million by the end of FY11. This represents a three-year CAGR of (0.6%) on FY08 shares outstanding.

As per the Zacks Digest model, FY10 EPS is expected to decline at a three-year CAGR of 43.3%, attributable to net income CAGR of (41.2%), and shares outstanding CAGR of (1.7%).

Please refer to the Zacks Research Digest spreadsheet on ATI for more details.

Zacks Investment Research Page 8 www.zackspro.com Target Price/Valuation

Of the ten firms covering the stock, two firms provided positive rating, five assigned neutral ratings, and three rendered negative ratings. The average Zacks Digest price target as provided by the firms is $34.79 (↑ $4.47 from the last report) (9.9% upside from the current price). The price targets range from $25.00 (21.0% downside from the current price) to $45.00 (42.2% upside from the current price), with a median target price at $34.50 (9.0% upside from the current price).

The firm (Stifel Nicolaus) with the highest target price of $45.00 provided a Buy rating, and based the valuation on EV/2010E EBITDA multiple of 11x. The firm (Citigroup) with the lowest target price of $25.00 based the valuation on a price-to-book multiple of 1.3x and provided a Sell rating.

Following 3Q09 earnings update, two firms (Citigroup; Deutsche Bank) raised their target prices.

Rating Distribution Positive 20.0%↑ Neutral 50.0%↓ Negative 30.0%↑ Avg. Target Price $34.79↑ Digest High $45.00↑ Digest Low $25.00↑ Median $34.50↑ No. of Analysts with Target Price/ Total 7/10

Risks to the target price include changes in aircraft delivery patterns, downward movement in air traffic, international business risks, program delays, extended manufacturing delays at Boeing and Airbus, excess production and export of stainless steel out of China.

Metrics detailing current management effectiveness are as follows:

Metric (TTM) Value Industry S&P 500 Return on Assets (ROA) 2.5%↓ 0.8%↓ 2.9%↓ Return on Investment (ROI) 3.0%↓ 0.9%↓ 4.1%↓ Return on Equity (ROE) 4.7%↓ 1.3%↓ 7.4% ↓

ROA, ROI and ROE are higher than the industry averages but ROA and ROI are lower than the overall market averages (as measured by S&P 500) while ROE is at par with the market average.

Capital Structure/Solvency/Cash flow/Governance/Other

Cash Flow and Balance Sheet

Zacks Investment Research Page 9 www.zackspro.com Cash on hand was $826.3 million at 3Q09 end, an increase of $356.4 million from $469.9 million at 4Q08 end. Long-term debt at the end of reported quarter totaled $1,050.4 million versus $496.4 million at the end of 4Q08 end.

Net debt as a percentage of total capitalization at 3Q09 end was 10.5% versus 2.0% at 4Q08 end. Total debt to total capital was 34.0% at the end of 3Q09 versus 20.7% at the end of 4Q08.

There were no borrowings outstanding under ATI’s $400 million unsecured domestic borrowing facility, although a portion of the letters of credit capacity was utilized.

Cash flow from operations during the first nine months of 2009 was $149.4 million (including the voluntary net cash contribution in 2Q09 to the Company’s U.S. defined benefit pension plan) versus $344.6 million during the first nine months of 2008. Excluding the $350.0 million voluntary cash pension contribution and the associated $108.5 million U.S. Federal income tax refund, cash flow from operations for the first nine months of 2009 was $390.9 million.

Capital spending was $97 million in 3Q09. The Company expects to incur $475 million in capex in FY09 (including Crucible acquisition). For FY10, ATI expects capital spending to be in the $300-$400 million range.

Cash used in investing activities was $302.6 million in the first nine months 2009 versus $363.8 million in 3Q08.

Cash provided by financing activities was $509.6 million in the first nine months of 2009 primarily due to receipt of $734.4 million of net proceeds from the second quarter of 2009 debt issuances, partially offset by debt retirements of $189.4 million and dividend payments of $35.3 million.

On July 9, 2009, ATI announced that it made a voluntary $350 million cash contribution to the Company’s U.S. defined benefit pension plan in June 2009 to significantly improve the plan’s funded position. A portion of the net proceeds from ATI’s June 2009 $402.5 million issuance of 4.25% five-year convertible notes were used to make this voluntary contribution. The $350 million voluntary contribution was made as a 2008 plan year contribution for income tax reporting purposes. As a result of the voluntary contribution, 2009 pension expense is expected to be reduced by $27.5 million to $98.7 million. This reduction will be reflected ratably over the last seven months of 2009.

Dividend

On September 29, 2009, ATI paid a quarterly cash dividend of $0.18 per share of common stock to stockholders of record at the close of business on September 21, 2009.

Capital Projects

The Bakers, NC titanium and super alloy forging facility began production in 3Q09. The Rowley, UT premium grade titanium sponge facility is expected to start up by the end of 2009. The melt shop consolidation at Breckenridge, PA is underway, and cost savings from this project are expected to be realized in FY10. Engineering, permitting, and site preparation continue, and the demolition of the existing building began in August. Expansion work at the precision rolled strip mill in China is complete.

Others

Zacks Investment Research Page 10 www.zackspro.com On September 8, 2009, ATI announced that it has entered into an agreement with Rolls Royce plc, to supply nickel based super alloy disc-quality products for commercial jet engine applications. This agreement will extend for a period of ten years and is estimated to generate revenue of about $1 billion. The agreement covers products sold by ATI Allvac, an ATI operating company, to the customer’s first tier suppliers, mainly forgers. November 4, 2009

Potentially Severe Problems

There are none other than those discussed in other sections of this report.

November 4, 2009

Long-Term Growth

The long-term growth rate provided by one firm (BofA Merrill Lynch) is 15.0%.

The firms expect the Company to incur a long-term decline and remain positive on ATI over a longer term based on its growth prospects in the commercial aerospace, military, oil & gas, industrial, and nuclear power markets.

Firms believe that, over a multi-year period, ATI should be an attractive investment given its cyclical earnings leverage, capacity growth profile and management team that has streamlined the Company to better weather the current downturn. They believe that the long-term outlook for jet fuel price expectations, even before the potential impact of carbon cap-and-trade rules, is higher and lower weight generally equals lower fuel consumption and a reduced carbon footprint. Aircraft construction using greater content of light weight, high strength composites and titanium are the logical solutions to these problems. November 4, 2009

Upcoming Events

The Company is expected to release its 4Q09 and FY09 earnings results on January 22, 2010.

Individual Analyst Opinions

POSITIVE RATINGS (20.0%)

Stifel Nicolaus (updated 10/22/09) – The stock is rated Buy with a target price of $45.00. INVESTMENT SUMMARY: ATI signed several long-term supply agreements, ranging from 2 to 10 years, with customers in aerospace and defense, oil and gas, electrical energy and medical. The firm believes these to provide a foundation for expanded market penetration, especially when combined with the pending acquisition of Crucible's powder metallurgy operations.

UnionBankSwitz. (updated 10/21/09) – The firm maintained a Buy rating with a target price of $42.00.

NEUTRAL RATINGS (50.0%)

Zacks Investment Research Page 11 www.zackspro.com Longbow (updated 10/22/09) – The stock is rated Neutral with no specific target price. INVESTMENT SUMMARY: Given the potential risk of further aircraft build rate reductions and falling titanium pricing, the firm prefers to stay cautious on the stock. However, the firm remains favorable on ATI for a longer time period.

Cowen (updated 10/22/09) – The stock is rated Neutral with no specific target price.

Deutsche Bank (updated 10/21/09) – The stock is rated Hold with a target price of $33.00 (raised from $31.00). INVESTMENT SUMMARY: Though ATI’s end-market exposures and financial position remain attractive, the firm is of the opinion that ATI’s defensive market exposure will likely mute any benefit from improved stainless results in the near term.

Goldman (updated 10/22/09) – The stock is rated Neutral with a target price of $35.00. INVESTMENT SUMMARY: The firm believes that ATI is positioning itself to capitalize on return of growth in its end markets, particularly aerospace, through strategic investments in various expansion projects. However, due to absence of any catalyst, the firm does not see much upside in the near term.

KeyBanc (updated 10/21/09) – The stock is rated Hold with no specific target price. INVESTMENT SUMMARY: The firm expects the stock to remain range bound in the near term until order momentum restores backlog levels.

NEGATIVE RATINGS (30.0%)

BofA Merrill Lynch (updated 10/21//09) – The stock is rated Underperform with a target price of $29.00. INVESTMENT SUMMARY: The firm maintained an Underperform view on ATI shares due to a decline in the commercial aerospace production, weak end market demand trends, and continued high capital spending plans. The Company's commodity stainless steel business also remains a concern given exposure to consumer-linked end markets and industry capacity growth concerns.

Citigroup (updated 10/21/09) – The firm maintained a Sell rating with a target price of $25.00 (raised from $22.00). INVESTMENT SUMMARY: Based on a lack of visible improvement in ATI's higher-margin end markets such as aerospace, ongoing de-stocking in the supply chain, continued investment in growth projects resulting in negative free cash and increased net debt, the firm stays bearish on the stock.

J.P. Morgan (updated 10/21/09) – The stock is rated Neutral with a target price of $34.50.

Research Analyst Tanuka De Copy Editor Pushpanjali B. Content Ed. Madhurima Das No. of brokers 10/10 reported/Total brokers Reason for Update Earnings

Zacks Investment Research Page 12 www.zackspro.com