11/28/10

CHAPTER 11: USING SUPPLY AND DEMAND: TRADE, BUBBLES, MARKET- MAKING Opening anecdote The Market for Foreign Exchange Purchasing Power Parity The Effects of Currency Appreciation and Devaluations Bubbles Summary & Homework Problems

I. INTRODUCTION

This is Luke Froeb, author with Brian McCann of Managerial Economics: a problem-solving approach, and this short video is designed to accompany chapter 11, “Trade, Bubbles, and Market Making.”

In November, 2010, the US Federal Reserve announced what they called “Quantitative Easing,” which basically means printing money to buy long term debt. This increases the supply of long term loans which is designed to lower US interest rates, which encourages investments. Remember that in Chapter four we showed how a lower cost of capital increases the NPV of investment projects.

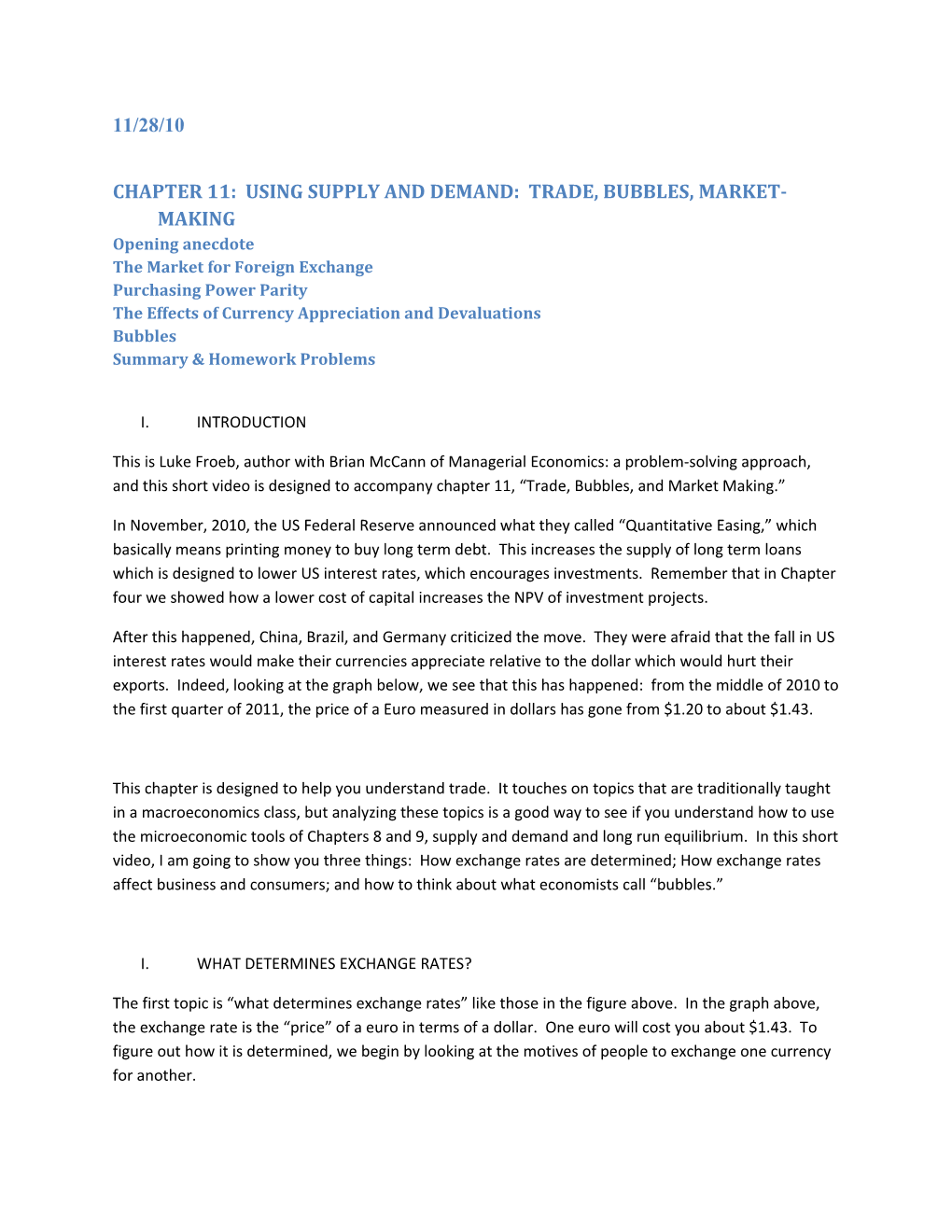

After this happened, China, Brazil, and Germany criticized the move. They were afraid that the fall in US interest rates would make their currencies appreciate relative to the dollar which would hurt their exports. Indeed, looking at the graph below, we see that this has happened: from the middle of 2010 to the first quarter of 2011, the price of a Euro measured in dollars has gone from $1.20 to about $1.43.

This chapter is designed to help you understand trade. It touches on topics that are traditionally taught in a macroeconomics class, but analyzing these topics is a good way to see if you understand how to use the microeconomic tools of Chapters 8 and 9, supply and demand and long run equilibrium. In this short video, I am going to show you three things: How exchange rates are determined; How exchange rates affect business and consumers; and how to think about what economists call “bubbles.”

I. WHAT DETERMINES EXCHANGE RATES?

The first topic is “what determines exchange rates” like those in the figure above. In the graph above, the exchange rate is the “price” of a euro in terms of a dollar. One euro will cost you about $1.43. To figure out how it is determined, we begin by looking at the motives of people to exchange one currency for another. We think of demand for Euros as everyone who wants to sell dollars to buy euros. These are mainly Americans who want to buy European goods and services or invest in Europe. To do so, they have to trade their dollars for Euros. Actually, they may not be the one exchanging dollars for euros. Rather it may be importer, or it may be the European manufacturer who gets paid in dollars, but has to pay workers in euros. The point is that everytime a US consumer buys a European good, someone has to sell dollars to buy euros. This represent the demand for euros. Think of all these people lining up at a bank or calling a broker and asking to sell dollars to buy euros.

[PICTURE A BANK WITH THE US CONSUMERS AND INVESTORS –STICK FIGURES WITH COWBOY HATS--ON ONE SIDE WHO WANT TO SELL DOLLARS TO BUY EUROS. LABEL THIS “DEMAND FOR EUROS”]

Now think of who is on the other side of this transaction: everyone in Europe who wants to buy US goods and services or invest in the US has to sell euros to buy dollars. This is the supply of euros. They line up on the other side of the bank

[SAME BANK BUT NOW ADD EUROPEAN CONSUMERS AND INVESTORS ON THE OTHER SIDE WHO WANT TO SELL DOLLARS TO BUY EUROS. DRAW THE EUROPEAN STICK FIGURES WITH BERETS, LABEL THIS THE “SUPPLY OF EUROS”]

The bank plays the role of market maker, adjusting the price of a euro so that the lines on either side of the bank are equally long. If something increases in the demand for euros, then the US side of the line gets longer, and the market maker will raise the price of a euro to make the lines the same size [SHOW THE US LINE GETTING SHORTER AND THE EUROPEAN LINE GETTING LONGER AS THE PRICE OF A EURO INCREASES].

This is exactly what happened in the chart above. As US interest rates went down, some Europeans decided to borrow in the US at low interest rates, sell their dollars to buy euros, and invest in Europe. This represents an increase in the demand for euros.

We can model this with our usual demand and supply curves. On the vertical axis is the “price” of a euro, measured in dollars. The “quantity” is the amount of euros exchanged for dollars. The demand for euros is everyone who wants to sell dollars to buy euros, and the supply of euros is everyone who wants to sell euros to buy dollars. The price of a euro increases as the demand for euros increases [GRAPH LABEL: “DEMAND AND SUPPLY OF EUROS”: SHOW AN INITIAL EQUILIBRIUM PRICE—THE INTERSECTION OF DEMAND AND SUPPLY--OF $1.21, AND THEN THE DEMAND INCREASES AND PRICE GOES UP TO $1.43, WHILE QUANTITY INCREASES AS WELL, BUT NO NUMBERS ON THE QUANTITY AXIS]

There is an equivalent way to model this, with the demand and supply of dollars. Here the demand for dollars is everyone who wants to sell euros to buy dollar—and the supply of dollars is everyone who wants to sell dollars to buy euros. The price of a dollar is 0.82 euros [can you use euro symbol], which is computed as 1/$1.20. The price of a dollar decreases to .70 euros as the supply of euros increases [GRAPH LABEL: “DEMAND AND SUPPLY OF DOLLARS”: SHOW AN INITIAL EQUILIBRIUM PRICE—THE INTERSECTION OF DEMAND AND SUPPLY--OF 0.83, AND THEN THE SUPPLY INCREASES AND PRICE GOES DOWN TO 0.70, WHILE QUANTITY INCREASES AS WELL, BUT NO NUMBERS ON THE QUANTITY AXIS] II. WHAT IS THE EFFECT OF A DEPRECIATION OF THE DOLLAR?

As the price of a euro increases, we say that the euro appreciates relative to the dollar, or equivalently that the dollar depreciates relative to the euro. Lets look at the effect of a depreciation on the prices and quantities of goods sold in the US. The demand curve is the aggregate demand of US consumers plus export demand, and the supply is the aggregate supply of goods for sale in the US. We imagine that exporters buy US goods and then sell them abroad. As the US dollar depreciates, export demand increases because one euro buys more dollars so US exports look cheaper to European consumers. This increases demand for US goods and services. As we see in the graph below, price increases.

We see is that a depreciation of the dollar helps US suppliers as it increases domestic price, but it hurts US consumers, because prices go up, and they respond by consuming less.

[GRAPH LABEL: “DEMAND AND SUPPLY OF GOODS IN US”: SHOW AN INITIAL EQUILIBRIUM PRICE AND QUANTITY—THE INTERSECTION OF DEMAND AND SUPPLY-- THEN THE DEMAND INCREASES AND PRICE GOES UP WHILE QUANTITY INCREASES AS WELL, BUT NO NUMBERS ON THE AXES]

Across the Atlantic, a very different story is unfolding. Lets look at the effect of a dollar depreciation on the prices and quantities of goods sold in Europe. The demand curve is the aggregate demand of European consumers plus export demand, and the supply is the aggregate supply of goods for sale in Europe. We imagine that exporters buy European goods and then sell them in the US. As the US dollar depreciates, export demand decreases because European exports look more expensive to US consumers. This decreases demand for European goods and services. As we see in the graph below, domestic prices in Europe decrease.

[GRAPH LABEL: “DEMAND AND SUPPLY OF GOODS IN EUROPE”: SHOW AN INITIAL EQUILIBRIUM PRICE AND QUANTITY—THE INTERSECTION OF DEMAND AND SUPPLY-- THEN THE DEMAND DECREASES AND PRICE GOES DOWN WHILE QUANTITY DECREASES AS WELL, BUT NO NUMBERS ON THE AXES]

What we see is that a depreciation of the dollar hurts European suppliers as it decreases domestic price, but it helps European consumers, because prices go down, and they respond by consuming more.

BOTTOM LINE: currency devaluations help suppliers, but hurt consumers.

III. BUBBLES

The last topic I want to cover are “bubbles.” A bubble is a price that cannot be explained by the forces of demand and supply, so it may seem odd that we trying to analyze them using demand and supply. And while there is a lot about bubbles we do not understand, we can use economic tools to examine the role that that expectations play in keeping a bubble going once it starts.

For example, if you see house prices go up this year, it might seem natural to expect them to go up next year. If you are a buyer, this would cause you to accelerate your purchases so that you can buy at a lower price. And if you are a seller, you might delay putting your house up for sale, so you can sell at a higher price next year.

We illustrate these changes in the figure below. [INSERT FIGURE 11-1 FROM THE BOOK, with demand increasing and supply decreasing] Demand increases, and supply decreases, with the result that expectations about future prices become self-fulfilling. Once prices go up, and people form expectations that they will continue to rise, these expectations can become self fulfilling.

So when does a bubble pop? This would be the most useful thing for us to know but, as of yet, there is no way to predict this moment.

However, we can spot the existence of a bubble by using the long run relationships of chapter 9. For example, Robert Shiller spotted the housing bubble by comparing the price of owning a house to the price of renting. In equilibrium, these prices should be close because owners can decide to sell and rent, and renters can decide to buy and own. In long run equilibrium, they should be indifferent between renting and owning, which should keep the prices relatively close.

In the figure below, we see that in 2005, the price of owning a house was 1.6 times as high as the price of renting a house. This caused economist Robert Shiller to call “bubble.” It turns out that he was about a year early with his call, as the housing bubble burst in 2006. Today the price of owning a house is only 20% higher than the price of renting.

This picture illustrates one of my favorite real estate maxims, “all my rich friends sold too early.” Robert Shiller is not a friend of mine, but he probably made money followeing his own investment advice.