A STP Model for Indian Securities Market Yogesh Kumar

The securities markets world over are working towards Straight Through Processing (STP) to reduce the trading cycle to T + 1 day. This paper attempts to explain the concept of STP, its variants, and its relevance and suitability for Indian markets.

What is STP? STP is automatic processing of securities transactions from inception of the trade to its settlement, that is, once an order is executed, there is no manual or electronic intervention in the processing chain to complete its settlement. In other words, once a trade has taken place, the movement of securities and funds from one account to another does require no or minimal manual / electronic intervention. It can, therefore, be understood as a concept that eliminates the need to re-enter an information in the processing chain which has already been captured in the chain earlier. If a particular information is already available at any node of the chain and is to be re-used, STP finds out a way to use the already available information instead of re-capturing the information.

There is an apparently compelling desire across markets to move towards STP as it is considered to be a pre-requisite to reduce the settlement cycle to T + 1 day which would further reduce the settlement risk. The current processing chain requires a lot of manual/electronic intervention by market participants such as brokers, investment managers, custodians, depositories and clearing corporation. These interventions require time and consequently under the existing systems it is not possible to switch over to T + 1 settlement cycle. As it minimises or avoids manual/electronic intervention in the processing chain after a trade has been executed, it reduces the chances of errors and the paper work involved and thereby reduces costs leading to increased efficiency and productivity gains. Further, reduction of settlement cycle releases the funds blocked in margins/collateral faster leading to reduced operational cost. Finally, it is a launching pad for streamlining the process related with the settlement of cross boarder trades.

Do the costs and associated risks of not implementing STP/T+1 outweigh the costs and risks of pursuing it? An extensive cost benefit analysis is required to support STP/T+1 implementation. Currently, in terms of business needs, the support for STP/T+1 is weak on two counts. One, the benefits of STP/T+1 in terms of reduction in risk are at best qualitative in nature. Secondly, major markets of the world have made huge investments and built robust settlement infrastructure. This combined with their legal certainty of securities regulations eliminates the principal risk among market participants. Also, in the wake of 9/11, the focus of the securities industry has shifted to Business Continuity Planning and all other initiatives have taken a back seat.

STP for Securities/Funds Settlement As per the Classical model, STP supports settlement of securities at gross level. The model coupled with T + 1 day settlement cycle reduces risk by reducing the time gap between the trade

Assistant Manager. NSE. The views expressed and the approach suggested are of the author and not necessarily of NSE. date and the settlement date. However, it does not support multilateral netting and may lead to enhanced risk in Indian context. The pre-requisites of this model are: (a) Investors’ depository account details are entered at the time of order entry; (b) Order and account details are passed on to the depository after clearing; (c) Settlement is carried out by the depository; (d) Direct debit and credit takes place in the investors’ depository accounts on the settlement day; and (e) The clearing member makes necessary funds arrangement in its bank account.

The Progressive model for STP allows for some intervention during a trade’s life cycle. But it ensures that the benefits of reduced risk due to multilateral netting and shorter settlement cycle are available to the clearing corporation as well as to the clearing members. The pre- requisites of this model are: (a) Netted delivery obligation is made available to clearing members in shortest time after close of trading; (b) Clearing member makes available to the settlement agency the depository account details which are to be debited/credited for its netted delivery obligation; (c) Clearing member makes available to the settlement agency the depository account details which are to be debited/credited for its internal delivery obligations; (d) Direct debit and credit takes place in the investors’ depository accounts on the settlement day; and (e) The clearing member makes necessary funds arrangement in its bank account.

Finally, the radical approach to STP minimizes all risks associated with settlement and eliminates all intervention during a trade’s life cycle. The pre-requisites of this model are: (a) Investor depository account details are entered at the time of order entry; (b) Validation for the availability of securities at the time of order entry and blocking of the same; (c) Trade and account details are passed on to the depository after clearing; (d) Settlement to be carried out by the depository; (e) Direct debit and credit takes place in the investors’ depository accounts on the settlement day; and (f) The clearing member makes necessary funds arrangement in its bank account.

The above models are applicable in case of retail trades. However, to meet the needs of institutional trades settled through custodians, the models require adjustments to incorporate additional requirements of communication among the intermediaries. It may be noted that progressive model supports netting of trades to the extent of netting taking place inter-se retail and institutional trades. Netting between retail and institutional trades is not advised.

For funds settlement, netting does not pose a problem since funds are fungible. But it is necessary for the banking system to support faster movement of funds. For this it would be necessary for markets to have Electronic Funds Transfer facility and may also require the use of ISO15022 standard. It means substantial investment in the banking system is required to support STP. Depending on the model adopted, the funds settlement can take place on net basis or on gross basis. Also, for funds settlement a model similar to the securities settlement is to be adopted if direct debit and credit shall be done to investors’ accounts. Alternatively, funds settlement shall be carried out through the accounts of the clearing members as envisaged for securities settlement in the above models.

Selection of an appropriate STP model for a market is a function of various factors. One of the critical factors is the level of technology used / available in the market. STP for net settlement is crucially dependent on robust, secure and advanced messaging network enabling all the participants to communicate online with the clearing /depository entities. It would also require strong software support allowing participants to know their net position on a regular basis. In case of STP for gross settlement, post trade communication requirement of participants with clearing / depository entity is limited. In this case, such requirement is only for custodial confirmation. Consequently, the level of technology required will be lower than in case of STP for net settlement.

Another factor in determining an appropriate STP model for a market is the existing settlement system. Most likely a market would like to continue to apply the existing system i.e. net or gross settlement system or a mixture of the two. A change-over from one to the other requires a major overhaul which may be difficult to achieve.

Preparing Indian Markets for STP

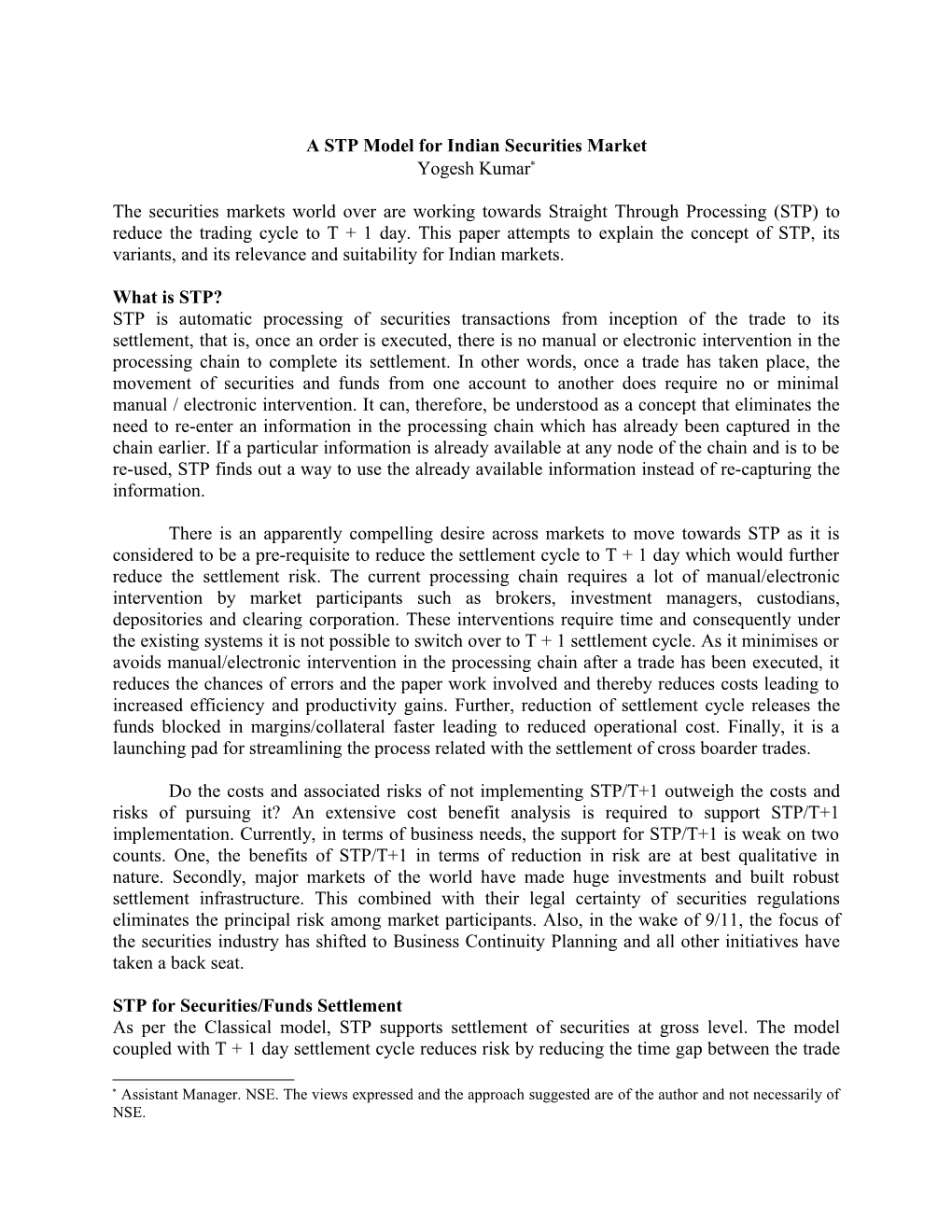

What is required to implement STP? As we know no two markets are similar. So, there can be no single way of implementing the concept. Each market would have to develop implementation strategies as per its unique requirements. A model, which may be appropriate for securities settlement in Indian market, is proposed at Chart 1.

Chart No. 1: STP Flow Chart for Securities Settlement

Stock Exchange’s 2, 3 Trading Trading System Members

4 5,6,13 1

Clearing 7, 13 Clearing Corporation / Custodian House

13 8,10,11

Depository Investors 9,13 Retail / Institutional

Communication with the new database required for STP

1. Investor’s instruction to TM 2. TM places the order 3. TM gets the trade confirmation 4. Trade details passed on to CC / CH 5. CC/CH provides net obligation on retail trades to TM 6. TM provides details of investor a/c to be debited and credited 7. Custodian provides details of institutional investor a/c to be debited and credited 8. Debit instruction to Depository 9. Depository debits respective investors’ accounts 10. Confirmation of the debit instruction 11. Credit instruction to depository 12. Depository credits respective investors’ accounts 13. System for confirmation and obligation of institutional trade

For Indian markets, the Progressive model is better suited as it can be implemented with modifications to incorporate the features peculiar to Indian markets like multiple depositories, settlement by clearing corporation / house, debit to clearing members’ account etc. The model would allow the Indian market to continue to reap in the benefits of netting. Also, the option of square up during the day would continue to be available to the market players.

Adoption of any of these models requires firms to re-architect and re-engineer back- office systems. Similarly, stock exchanges, clearing corporations and depositories have to re- structure their systems. Besides, seamless and inter-active communication network among stock exchange, Clearing Corporation, depository and clearing members is required to be created to eliminate the paper and voice mode of communication. It may also require shifting from end of the day processing to real time or multi-batch mode processing / messaging paradigm. Thus, interfaces, new messaging standards and protocols are some of the IT resources to be mobilized for STP readiness.

An analysis of the steps involved from the initiation of a trade till its settlement in Indian market shows that trade life cycle is full of manual and electronic interventions. To achieve STP, it would be necessary to streamline the process that would eliminate paper work and manual intervention. It is also required to minimize electronic intervention that takes place between clearing members and clearing corporation at the one hand and clearing corporation and depository on the other hand.

Minimisation of the intervention at the level of investor, clearing member and depository participant would require change in some features of the existing structure. One such feature could be direct debit of investors’ account instead of the clearing members’ pool accounts. Clearing members can provide the details of the investors’ account to be debited to clearing corporation which would be passed on to the depository. Necessary safeguards can be added to ensure that fraudulent debits are not done to investors’ account.

Depositories have made some efforts to reduce the paper work at the clearing member and depository participant’s interaction level. This has minimized the requirement of giving delivery out instructions. Similar other efforts can be made to minimize the intervention.

For institutional trades which are settled through custodians, one possibility is to provide near real time trade information to all the intermediaries from a common hub allowing for interactive messaging. Once a trade is executed, all the intermediaries shall be able to view the trade on their terminals. The central hub would also provide the facility for post-trade inter- action that has to take place among these intermediaries. Thus, there would not be any time lag in knowing the status of an order and all the intermediaries can start working simultaneously. This would enable the custodian to confirm / affirm the trade to clearing corporation without loss of time.

As can be seen from the above discussion on the concept of STP and the stage of the Indian market, it is imperative to have wide ranging discussions on the subject prior to formulating any plan. It is also necessary to do a cost benefit analysis to take a view on this matter. The major cost factors are re-engineering of processing for trade data, interfaces, messaging protocols, software development, human resource development, cost of coordinating the effort among all the participants etc. The quantum of these costs would depend on the level of STP sophistication desired to be implemented in a market. The main quantitative benefits are likely to occur on account of: reduction in working capital due to faster rotation of funds, reduced collateral requirements, reduction in the overall daily credit risk by two third and reduction in the cost of resolving errors in the documentation. It is to be clearly understood that STP’s implementation costs and benefits will be spread out across the whole spectrum of participants. Each participant would necessarily have to invest in its systems and procedures in order to make itself STP compliant.

SEBI envisages implementation across various market participants by December 31, 2002. It had, therefore, set up a committee to examine feasibility of introduction of STP and for designing and recommending an expeditious solution for electronic transmission of trade and settlement information in the Indian markets, across participants. The committee has identified three areas to work upon: identification of manual intervention, messaging standards for data and communications backbone.

Finally, STP is considered synonymous with reducing the settlement cycle to T +1. It will be useful to divorce STP from T +1 and then assess the desirability of having STP on its own. A divorced STP can be sold to market participants on the basis of high quantifiable cost benefits arising due to enhanced efficiencies.