Chapter 20: Earnings per Share

Assignment 20-2

Case A Actual Retroactive Months Time Period Shares Adjustment* Outstanding Shares

1 January, shares outstanding 2,500,000 1 January to 28 February 2,500,000 × 1.20 × 2/12 = 500,000 1 March, sold add’l shares 600,000 1 March to 30 June 3,100,000 × 1.20 × 4/12 = 1,240,000 1 July, retired shares (300,000 ) 1 July to 31 October 2,800,000 × 1.20 × 4/12 = 1,120,000 1 November, stock dividend 20% (560,000/2,800,000) 560,000 1 November to 31 December 3,360,000 × 2/12 = 560,000 Total 3,420,000

*Adjustment for 20% stock dividend

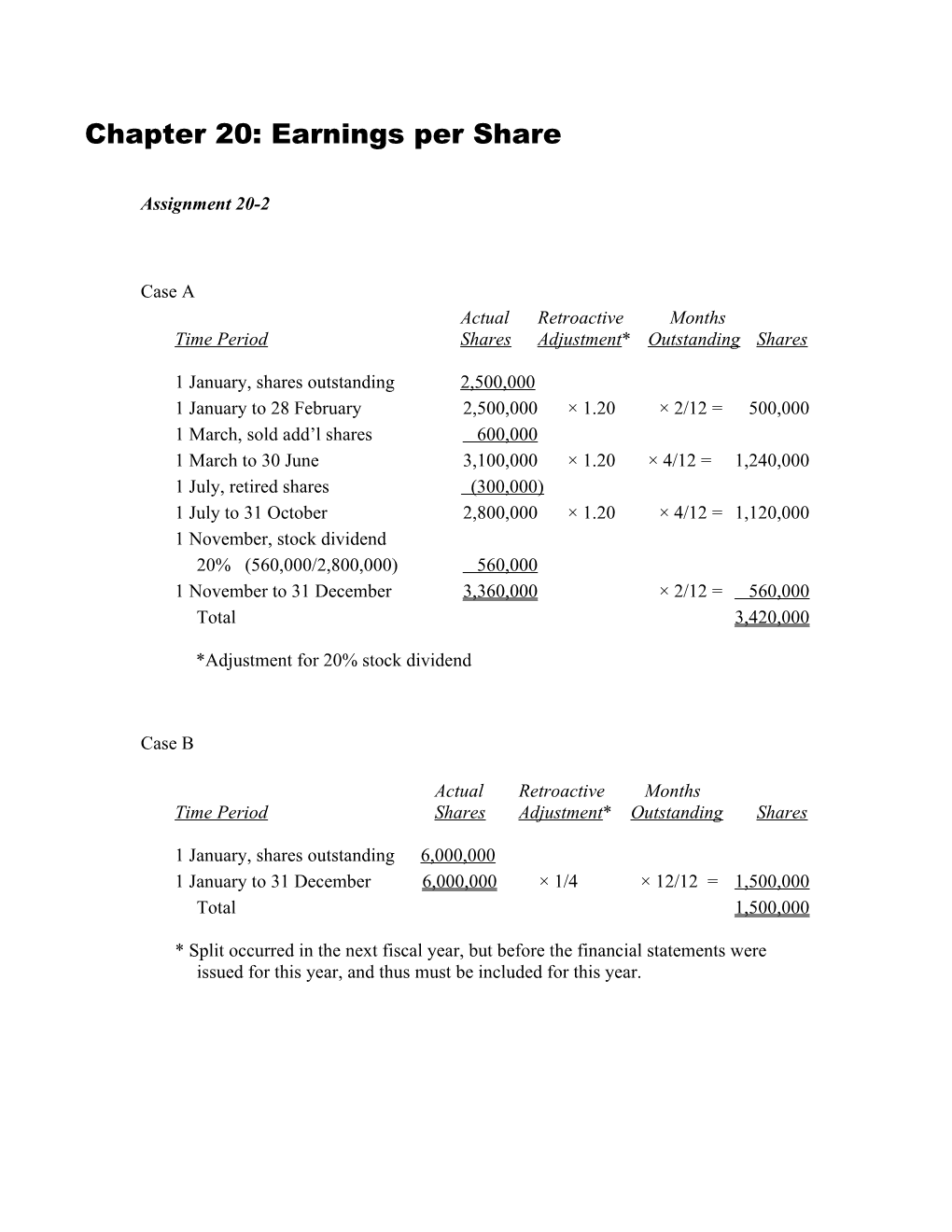

Case B

Actual Retroactive Months Time Period Shares Adjustment* Outstanding Shares

1 January, shares outstanding 6,000,000 1 January to 31 December 6,000,000 × 1/4 × 12/12 = 1,500,000 Total 1,500,000

* Split occurred in the next fiscal year, but before the financial statements were issued for this year, and thus must be included for this year. Case C

Actual Months Time Period Shares Outstanding Shares

1 January, shares outstanding 2,860,000 1 January to 28 February (2,860,000 × 1.10)*3,146,000 × 2/12 = 524,333 1 March, stock dividend 286,000 1 March to 31 May 3,432,000 × 3/12 = 858,000 1 June, retired shares (200,000) 1 June to 31 July 3,232,000 × 2/12 = 538,667 1 November, shares issued but backdated to 1 August (contingency cleared) 400,000 1 November to 31 December 3,632,000 × 5/12 = 1,513,333 Total 3,434,333

* Adjusted opening shares to year-end equivalent for 10% stock dividend Assignment 20-13 Earnings Weighted available to average common shareholders number of shares EPS Basic EPS: Net earnings $600,000 (Note—preferred dividends are already deducted from net earnings) ______$600,000 Shares outstanding: 48,000* × 3/12 12,000 60,000 × 9/12 45,000 57,000 Basic EPS $10 .53

* Bond conversion: ($1,500,000 ÷ 1,000) × 8 = 12,000; 60,000 – 12,000 = 48,000

Individual effects: 12% debentures, actual conversion, Interest: $48,000 × (1 – 0.40) $ 28,800 Shares 12,000 × 3/12 3,000 $9.60 12% debentures outstanding Interest: ($624,000 – $48,000) × (1 – 0.40) $345,600 Shares: ($4,500,000 ÷ $1,000) × 8 36,000 9.60 12.4% debentures Interest ($450,000) × (1 – 0.40) $270,000 Shares: ($3,000,000 ÷ $1,000) × 8 24,000 $11.25

The options are anti-dilutive because exercise price is greater than market value. The individual effect of the 12% debenture items are identical and their order is irrelevant. The 12.4% debenture is anti-dilutive.

Diluted EPS: Basic EPS $600,000 57,000 $10.53 Actual conversion: Bond interest 28,800 Shares 3,000 12% debentures Interest 345,600 Shares ______36,000 Diluted EPS $974,400 96,000 $10 .15 Assignment 20-30

Earnings available to Weighted average common shareholders number of shares EPS Basic EPS: Net earnings $18,000,000 Preferred dividends 600,000 × $0.20 (120,000)

Average shares 3,300,000 × 12/12 3,300,000 3,320,000* × 0/12 — Basic EPS $17,880,000 3,300,000 $5 .42

* 10,000 × 2 = 20,000 shares issued on conversion 31 December 20X6

Individual effects:

1. Preferred shares $0.20 × 600,000 = $120,000 = $0.20 600,000 600,000

2. Options Shares issued: 500,000 Shares retired: ($53 × 500,000) ÷ $75 = 353,333

3. Debentures ($10,000,000 × 10% + $20,000) × (1 – 0.40) = $612,000 = $3.06 $10,000,000 ÷ 100 × 2 180,000

The debentures are converted on 31 December. Therefore they are backdated for the entire year.

Note: The principal is $10,000,000 (note b). Presumably, the $9,000,000 reported is net of the unamortised discount.

Continued on next page Earnings available to Weighted average common shareholders number of shares EPS Diluted EPS: Basic, above $17,880,000 3,300,000 $5.42 Options: Shares issued 500,000 Shares retired ______(353,333 ) 17,880,000 3,446,667 $5.19 Preferred shares: Dividends/Shares 120,000 600,000 18,000,000 4,046,667 $4.45 Actual conversion of debentures: Earnings 612,000 Shares 200,000 Diluted EPS $18,612,000 4,246,667 $4 .38