Introduction In this assignment I have made a portfolio of 5 stocks and analyzed their performance over a period of 2 weeks. Before selecting the stock for the portfolio and determining their weightage in the portfolio I have conducted an in depth analysis of each stock. I have tracked the performance of the portfolio on daily basis; my analysis also includes determining the average return of the portfolio and index based on the daily return of two week period. In the analysis I have determined the standard deviation of the market index and the portfolio which is based on the daily return during a 2 week period. Apart from all above I have also plotted the daily return of both our portfolio and market index on a scatter diagram which represent the comparative return of both market index and out portfolio over a period of 2 weeks with dates on X-axis and returns on Y-axis. In order to make the analysis more meaningful I have also determined the beta of the portfolio which is one of the most important variables in financial analysis. Diversification of portfolio A diversified portfolio is a portfolio which consists of least unsystematic risk. To further explain the meaning of well diversified portfolio I have to first understand the types of risk associated with investing in stocks. There are many risks associated with the financial instruments but these risks can be broadly categorized under two heads; Systematic Risk Unsystematic Risk Systematic risk this risk is also known as market risk or Un-diversifiable risk. As the name itself suggests this risk cannot be diversified. This risk is inherent in all type of investments and is caused due to the macroeconomic factors such as inflation, type of govt., market conditions (inflation or recession). Systematic risk is measured by the help of Beta coefficient. If the company has high beta ( i.e. more than 1) then investing in such company is considered as more risky in comparison to the companies having low beta ( i.e. lower than 1). Unsystematic risk this risk is associated with particular nature of industry or company (poor management, lack of raw material, strike of workers) and is also known as specific risk, residual risk or diversifiable risk. This type of risk can be minimized by the help of diversification. Diversification is a process by which unsystematic risk can be reduced. There is a very popular phrase associated with technique “Don’t keep all your eggs in one basket”. This theory suggests that an investor should not invest all his funds in one industry or company rather he should invest his funds in different industries so that he can easily diversify the industry specific risk. 'Risk cannot be eliminated but it can be minimized' this statement truly provides us a message that risk can never be eliminated it can only be minimized. The reason being the systematic risk, even if the proper diversification is done then only the unsystematic risk can be eliminated and not the systematic risk. Thus we can only minimize the risk and cannot eliminate it. In the current situation we have invested the funds in different sectors with different amount of money being invested in each sector, this represents that portfolio is well diversified. As per the calculations beta of the portfolio is 1.09, as we have already discussed that beta closer to 1 means that change in market will not affect the portfolio much and performance of portfolio will move in the same direction where the market returns will move. I have also computed standard deviation of both the portfolio and the market index, standard deviation of portfolio is 1% whereas standard deviation of market index is 0.78% which shows that market index is less risky as compared to the portfolio as the standard deviation of market index is less than that of the portfolio. Beta of portfolio Beta of a stock is always dynamic and it depends on the market conditions and relationship of the company with the market. Beta factor is used by the investors to value the stock and measure risk associated with the stock. Beta is measure of volatility of stock in relation to the market. Stock analysts use the Beta factor to analyze stock’s risk profile. The beta of market is always 1 and other stocks derive their beta value on the basis of their deviation from the market return. Those stock which deviates more than the market have a higher beta i.e. more than 1 and the stocks which does not deviate more than the market have low beta i.e. less than 1. Stocks having high beta are considered as more risky and the stocks having low level beta are considered as less risky. Therefore required rate of return of stocks having high beta is more than the required rate of return of stocks having low level of beta. All the stocks in the current portfolio belong to the different industry and as per the calculation the covariance of the portfolio is positive. When the covariance is positive it means that beta of portfolio is also positive, in order to determine the beta of portfolio we have compared the return of the portfolio with the market index return i.e. S&P 500 index returns. Beta of portfolio is determined using the following formula:- Beta of portfolio = Covariance of portfolio and stock/Variance of portfolio Beta of the current portfolio is 1.09 (Refer attached Excel sheet). Expected return/average return of portfolio Expected return of a portfolio is computed on the basis of current performance of the stock and future prospects of the stocks in the portfolio. Expected return is also based on the concept of risk and return relationship. Relationship between risk and return is a “direct” or “positive” relationship which means when risk raises the expected return on the asset also raises and vice versa. If the asset is less risky than the expected return of an investor is not high but if the risk involved is high then in such case the expected return of an investor is also high. This relationship holds for both individuals as well as management of the companies. The concept of risk and return is also used for “pricing the risk”. Expected return of the current portfolio is 0.19% (Refer to Excel spreadsheet). This return is for a two week period and shall not be confused with per annum percentage. When comparing the portfolio with the market index I have also determined the average return of the market index which is equivalent to 0.14%. Market return is less than the average return of the portfolio which means I have selected an efficient portfolio and exceeded the market rate of return. Major factors contributing to the success of portfolio Share prices of each stock have affected the portfolio in its own way. The following are the major changes in the values of stock which affected the portfolio: 1) Share prices of Apple was affected largely during this period due to various events going in the company such as demand raised by the company from Samsung to pay $405 Million for patent breech, Probe by tax authorities against Apple for evading $1.35 Million of taxes in Italy, Apple launched “Retina Display” Ipad mini as of November 13 etc. All these events affected the share price and the market value of Apple Inc. in a different way, so as far as the difference in the sale and purchase price is concerned (i.e. the value of stock as on 6th November and 18th November) it is not substantial but the price during the period (6th November to 18th November) changed substantially. 2) No substantial change is witnessed in the share prices of Boeing Company, there is upsurge in the prices of share on the 13th, 14th and 15th of November and the possible reason could be that Boeing is in final stage of its deal with Abu Dhabi’s Etihad and is expecting to get more orders from Gulf countries. 3) Share prices of Walt Disney also trembled after it posted its quarterly results, Disney fails after earnings and payroll data is well above expectation. Due to these incidents price of Walt Disney Co. declined 1.3% to $66.30 before the opening bell. 4) There is no major event in the case of General Motors but still its share price rose by almost 10% during past 2 weeks which means that speculators have been bullish over GM. 5) Analysis of the share prices of Johnson & Johnson also reflects that the market price of shares has been around $93 per share and only minor fluctuations have been seen in the price of shares. Johnson & Johnson has to pay $2.2 Billion to end the US drug probes but this news did not affect the prices of shares because the effect of this news has already been adjusted in the share prices.

Market Index vs. Portfolio I have compared the market index and stock portfolio in order to determine whether the performance of portfolio was better than or worse than the market index. My comparison is based on the market value of the original portfolio and the tentative market value of the funds if all the money was invested in market index instead of a portfolio of stocks. If I could have invested the funds in the index than at the end of the holding period i.e. on November 18th I could have received $100,592.42 but the value of portfolio on November 18th is $101,410 which means the value of portfolio is higher than that of the index value and this shows that I have invested in the right place. So as an investor I have gained over and above the market return and the investment has been better off as compared to market index. So far as risk is concerned the portfolio is a little risky as compared to the market index but as per the risk and return relationship it is difficult to get larger returns without taking higher risks. Conclusion

Analysis of the investment portfolio and market indices for past two weeks I have come to a conclusion that the portfolio is performing well and as far the beta of the portfolio it remains close to one there is no problem in keeping funds in this portfolio. The future of the portfolio seems bright as all the stocks in the portfolio are stocks of blue chip companies and the fundamental and financial analysis of the companies also suggests that the companies have strong financial position and the market value of these stocks is not going to dilute unless there is a huge market driven factor show up. Exhibits Average return of portfolio and S&P 500 index

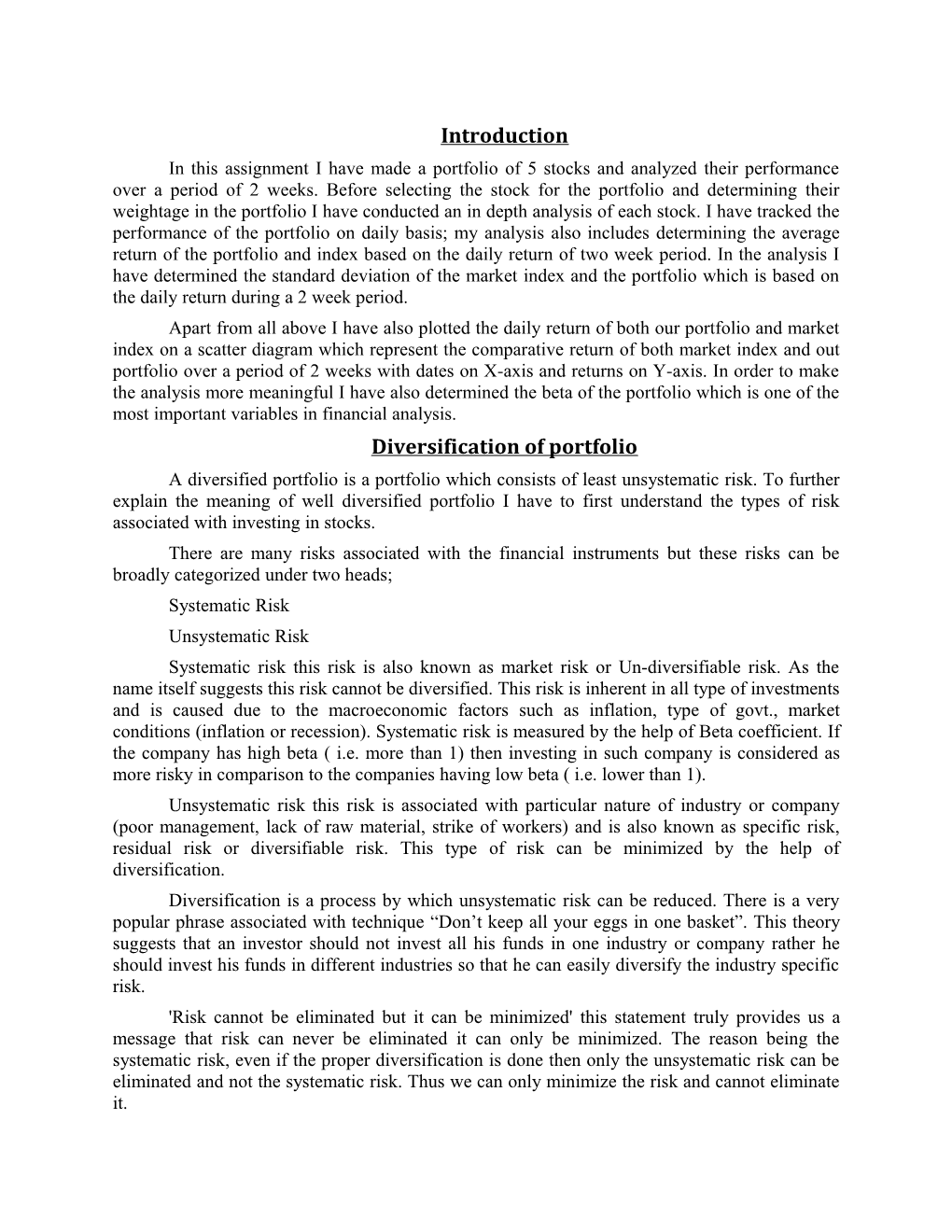

Date Portfolio return Index return

November 7, 2013 -1.46% -1.26% November 8, 2013 1.69% 1.28% November 11, 2013 -0.16% 0.07% November 12, 2013 -0.36% -0.23% November 13, 2013 0.93% 0.77% November 14, 2013 1.06% 0.46% November 15, 2013 0.16% 0.40% November 18, 2013 -0.36% -0.35%

Average return 0.19% 0.14% Standard deviation 1.00% 0.78% Variance 0.010% 0.006% Covariance 0.007% Beta of portfolio 1.09

Chart showing return of portfolio and index over a period of 2 weeks Table showing index return and values over a period of 2 weeks

Total units of index purchased using 53.66 Cash balance 4456

Date Value of index (including cash) Return

November 6, 2013 $ 99,463.38 November 7, 2013 $ 98,210.92 -1.26% November 8, 2013 $ 99,469.82 1.28% November 11,2013 $ 99,538.51 0.07% November 12,2013 $ 99,313.13 -0.23% $ November 13,2013 100,081.03 0.77% $ November 14,2013 100,543.59 0.46% $ November 15,2013 100,949.27 0.40% $ November 18,2013 100,592.42 -0.35%

Table showing portfolio return and values over a period of 2 weeks Cash balance $4,456

Date Value of index (including cash) Return

November 7, 2013 $ 98,602.00 -1.46% $ November 8, 2013 100,191.00 1.69% $ November 11,2013 100,037.50 -0.16% November 12,2013 $ 99,698.00 -0.36% $ November 13,2013 100,581.00 0.93% $ November 14,2013 101,604.00 1.06% $ November 15,2013 101,761.50 0.16% $ November 18,2013 101,409.50 -0.36%