COURSE OUTLINE

COURSE : MULTIPARADIGM ACCOUNTING CODE : - CREDITS : 3 LECTURERS : ALI DJAMHURI PHD , DR. ARI KAMAYANTI

Course Description

This course aims to explain and give understanding about various worldviews (multiparadigm) of seeing accounting in its social context. By understanding the various paradigms, accounting and its impact on politics, society, culture and information technology, can be developed and emancipated. Students would be able to enrich themselves with sufficient knowledge of positivism, interpretivism, critical and postmodern paradigms and hence they would be able not just to understand accounting within each paradigm but also to create accounting according to the paradigm they choose.

COURSE OBJECTIVE The course is expected to help students achieve (1) understanding that it is humans’ obligation to God to develop accounting (2) understanding that accounting discipine and practices are intertwined with various world views; (2) enrichment of oneself with stock of accounting world views (3) continuous improvement of oneself (self empowerment) to help society in creative and ethical-religius manner.

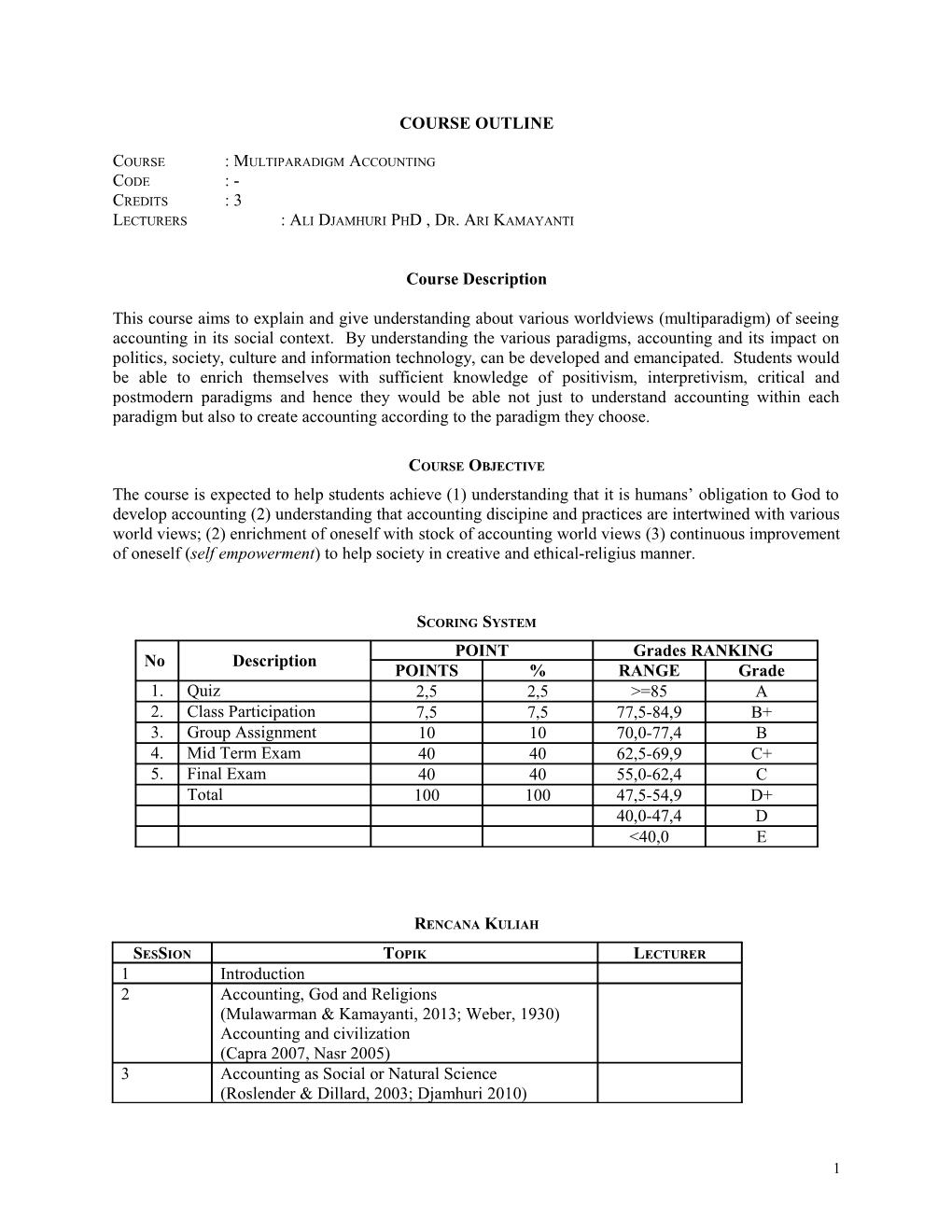

SCORING SYSTEM POINT Grades RANKING No Description POINTS % RANGE Grade 1. Quiz 2,5 2,5 >=85 A 2. Class Participation 7,5 7,5 77,5-84,9 B+ 3. Group Assignment 10 10 70,0-77,4 B 4. Mid Term Exam 40 40 62,5-69,9 C+ 5. Final Exam 40 40 55,0-62,4 C Total 100 100 47,5-54,9 D+ 40,0-47,4 D <40,0 E

RENCANA KULIAH

SESSION TOPIK LECTURER 1 Introduction 2 Accounting, God and Religions (Mulawarman & Kamayanti, 2013; Weber, 1930) Accounting and civilization (Capra 2007, Nasr 2005) 3 Accounting as Social or Natural Science (Roslender & Dillard, 2003; Djamhuri 2010)

1 4 Accounting, Nations and Laws (Abeysekera, n.d.; Merino, Mayper, & Tolleson, 1989) 5 Accounting, tradition and Globalization (Geertz 1976, Estes: Tyranni of bottom line, Hopwood 2009)

6 Political Economy of Accounting (Tinker, 1980) The Nature of Man (Jensen & Meckling, 1998)

7 MID EXAMINATION

8 Accounting and Organizations (Hopwood, 1989) The origin of NPM (Barzelay, 2002)

9 Paradigms in Social Science, (Burrell dan Morgan chapter 1-3, The Integral Paradigm (Jeffries, 1999), Paradigms in Accounting (Chua, 1986) 10 Accounting in Positive Paradigm (Burrell dan Morgan chapter 4); (Watts & Zimmerman, 1990) 11 Accounting in Interpretive Paradigm (Burrell dan Morgan 1979 chp 6),(Morgan, 1988) 12 Accounting in Critical Paradigm (Burrell dan Morgan 1979 chp 8-10), (Dillard, 1991) 13 Accounting in Postmodern Paradigm 14 FINAL EXAMINATION

REFERENCES

Abeysekera, I. (n.d.). International Harmonisation of Accounting Imperialism- An Australian Perspective (pp. 1–41). University of Victoria, Footscray Park Campus.

Barzelay, M. (2002). Origins of the new public management: an international view from public administration/political science

Chua, W. F. (1986). Radical Developments in Accounting Thought. The Accounting Review, 61(4), 601– 632.

Dillard, J. F. (1991). Accounting as a Critical Social Science. Accounting, Auditing & Accountability Journal, 4(18-28).

Estes, R. (1996). Tyranny of the Bottom Line: Why Corporations Make Good People Do Bad Things. Berret-Koehler Publisher. USA.

Hopwood, A. G. (1989). Accounting and Organisation Change. Accounting, Auditing & Accountability Journal, 3(1), 1–17.

Jeffries, V. (1999). The Integral Paradigm: The truth of Faith and the Social Sciences. The American Sociologist, (Winter), 36–55.

2 Jensen, M. C., & Meckling, W. H. (1998). The Nature of Man. Journal of Applied Corporate Finance, 7(2), 4–19.

Merino, B. D., Mayper, A. G., & Tolleson, T. G. (1989). Neo Liberalism and Corporate Hegemony: A Framework of Analysis for Financial Reorting Forms in the United States.

Morgan, G. (1988). Accounting as Reality Construction: Towards a New Epistemology for Accounting Practice. Accounting, Organizations and Society, 13(5), 477–485.

Mulawarman, A. D. (2012). Akuntansi Syariah di Pusara Kegilaan “IFRS-IPSAS” Neoliberal: Kritik atas IAS 41 dan IPSAS 27 mengenai Pertanian. In The 6th Hasanuddin Days (pp. 1–24).

Mulawarman, A. D., & Kamayanti, A. (2013). Islamic Accounting Anthropology: an Alternative to Solve Modernity Problems. Forthcoming. Malang.

Riduwan, A., Triyuwono, I., Irianto, G., & Ludigdo, U. (2010). Semiotika Laba Akuntansi: Studi Kritikal-Postmodernis Derridean. Jurnal Akuntansi dan Keuangan Indonesia, 7(1), 38–60.

Roslender, R., & Dillard, J. P. (2003). Reflections on The Interdisciplinary Perspectives on Accounting Project. Critical Perspectives on Accounting, 14, 325–351. doi:10.1016/cpac.2002.0526

Tinker, A. M. (1980). Towards a Political Economy of Accounting: An Empirical Illustrations of The Cambridge Controversies. Accounting, Organizations and Society, 5(1), 147–160.

Watts, R. L., & Zimmerman, J. L. (1990). Positive Accounting Theory : A Ten Year Perspective. The Accounting Review, 65(1), 131–156.

Weber, M. (1930). The Protestant Ethic and the Spirit of Capitalism. London: Routledge.

3