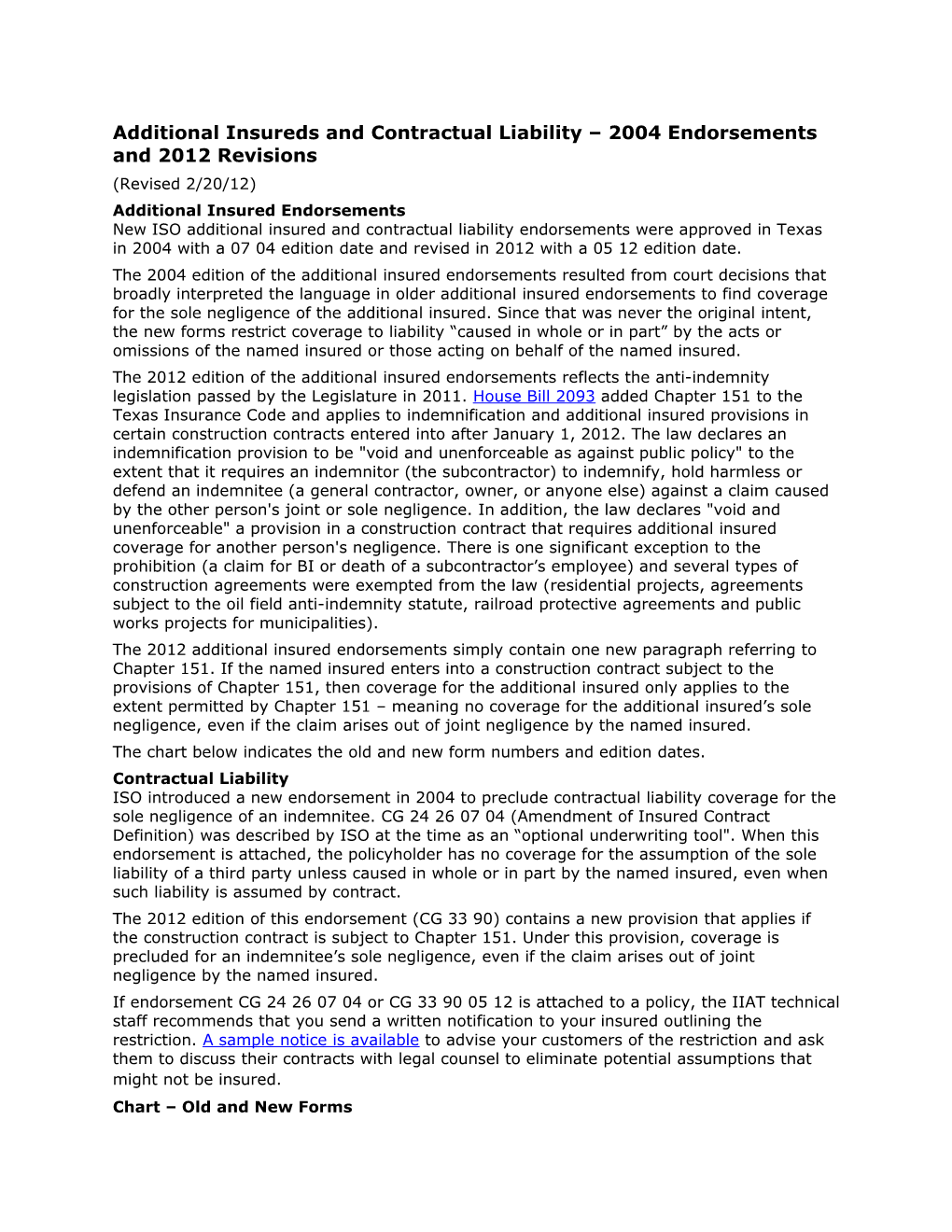

Additional Insureds and Contractual Liability – 2004 Endorsements and 2012 Revisions (Revised 2/20/12) Additional Insured Endorsements New ISO additional insured and contractual liability endorsements were approved in Texas in 2004 with a 07 04 edition date and revised in 2012 with a 05 12 edition date. The 2004 edition of the additional insured endorsements resulted from court decisions that broadly interpreted the language in older additional insured endorsements to find coverage for the sole negligence of the additional insured. Since that was never the original intent, the new forms restrict coverage to liability “caused in whole or in part” by the acts or omissions of the named insured or those acting on behalf of the named insured. The 2012 edition of the additional insured endorsements reflects the anti-indemnity legislation passed by the Legislature in 2011. House Bill 2093 added Chapter 151 to the Texas Insurance Code and applies to indemnification and additional insured provisions in certain construction contracts entered into after January 1, 2012. The law declares an indemnification provision to be "void and unenforceable as against public policy" to the extent that it requires an indemnitor (the subcontractor) to indemnify, hold harmless or defend an indemnitee (a general contractor, owner, or anyone else) against a claim caused by the other person's joint or sole negligence. In addition, the law declares "void and unenforceable" a provision in a construction contract that requires additional insured coverage for another person's negligence. There is one significant exception to the prohibition (a claim for BI or death of a subcontractor’s employee) and several types of construction agreements were exempted from the law (residential projects, agreements subject to the oil field anti-indemnity statute, railroad protective agreements and public works projects for municipalities). The 2012 additional insured endorsements simply contain one new paragraph referring to Chapter 151. If the named insured enters into a construction contract subject to the provisions of Chapter 151, then coverage for the additional insured only applies to the extent permitted by Chapter 151 – meaning no coverage for the additional insured’s sole negligence, even if the claim arises out of joint negligence by the named insured. The chart below indicates the old and new form numbers and edition dates. Contractual Liability ISO introduced a new endorsement in 2004 to preclude contractual liability coverage for the sole negligence of an indemnitee. CG 24 26 07 04 (Amendment of Insured Contract Definition) was described by ISO at the time as an “optional underwriting tool". When this endorsement is attached, the policyholder has no coverage for the assumption of the sole liability of a third party unless caused in whole or in part by the named insured, even when such liability is assumed by contract. The 2012 edition of this endorsement (CG 33 90) contains a new provision that applies if the construction contract is subject to Chapter 151. Under this provision, coverage is precluded for an indemnitee’s sole negligence, even if the claim arises out of joint negligence by the named insured. If endorsement CG 24 26 07 04 or CG 33 90 05 12 is attached to a policy, the IIAT technical staff recommends that you send a written notification to your insured outlining the restriction. A sample notice is available to advise your customers of the restriction and ask them to discuss their contracts with legal counsel to eliminate potential assumptions that might not be insured. Chart – Old and New Forms Old Form New Form CG 20 07 07 04 CG 33 91 05 12 Additional Insured – Engineers, Architects, Texas Additional Insured – Engineers, or Surveyors Architects, or Surveyors

CG 20 10 07 04 CG 33 95 05 12 Additional Insured – Owners, Lessees, or Texas Additional Insured – Owners, Lessees, Contractors – Scheduled Person or or Contractors – Scheduled Person or Organization Organization

CG 20 15 07 04 No change. This endorsement should not be Additional Insured – Vendors used for construction contracts.

CG 20 26 07 04 No change. This endorsement should not be Additional Insured – Designated Person or used for construction contracts. Organization

CG 20 28 07 04 CG 33 96 05 12 Additional Insured – Lessor of Leased Texas Additional Insured – Lessor of Leased Equipment Equipment

CG 20 31 07 04 Additional Insured – Engineers, Architects or Surveyors No change. (Applicable only to the Owners and Contractors Protective Liability Coverage CG 20 32 07 04 CG 33 92 05 12 Additional Insured – Engineers, Architects Texas Additional Insured – Engineers, or Surveyors Not Engaged by the Named Architects or Surveyors Not Engaged by the Insured Named Insured

CG 20 33 07 04 CG 33 93 05 12 Additional Insured – Owners, Lessees or Texas Additional Insured – Owners, Lessees Contractors – Automatic Status When or Contractors – Automatic Status When Required in Construction Agreement with Required in Construction Agreement with You You

CG 20 34 07 04 CG 33 97 05 12 Additional Insured – Lessor of Leased Texas Additional Insured – Lessor of Leased Equipment – Automatic Status When Equipment – Automatic Status When Required in Lease Agreement with You Required in Lease Agreement with You

CG 20 37 07 04 CG 33 94 05 12 Additional Insured – Owners, Lessees or Texas Additional Insured – Owners, Lessees Contractors – Completed Operations or Contractors – Completed Operations

CG 33 90 05 12 CG 24 26 07 04 Texas Changes - Amendment of Insured Amendment of Insured Contract Definition Contract Definition

Important Supreme Court Decision In an important decision that may have implications for the newest 2004 and 2012 editions version of ISO's additional insured endorsements, the Texas Supreme Court, in 2006, interpreted provisions of a company's blanket additional insured endorsement. In Atofina Petrochemicals, Inc. v. Continental Casualty Co., the court made three important observations. (1) The provision in the blanket endorsement that requires a written contract or agreement may refer to agreements made earlier than the final work agreement. In this case, the subcontractor submitted a written construction proposal which included a commitment to furnish insurance. After the proposal was accepted by Fina, it issued purchase orders which purported to "contain the entire agreement between the parties" and did not mention insurance. The court ruled that the purchase orders did not override the original insurance commitment because the orders were consistent with the original construction contract. (2) A provision in Continental's endorsement that requires issuance of a certificate of insurance showing additional insured status is fulfilled even if the certificate is issued after the injury occurs. In this case, the injury which caused the lawsuit against Fina occurred before the agent issued a certificate. The court ruled that the endorsement didn't specifically require issuance of a certificate prior to the injury, only that a certificate be issued. (3) A provision in the endorsement that excluded coverage for the additional insured's sole negligence can only be construed to apply when there are no allegations of injury or damage caused by the insured subcontractor. Interestingly, the court accepted the idea that an additional insured endorsement can exclude the additional insured's sole negligence with no causation by the named insured, which is the primary purpose of the changes made by ISO in the 2004 revisions of it additional insured endorsements. For more information - see IRMI articles, "Additional Insured Changes in the CGL" and "How Will Courts Construe ISO's New Additional Insured Endorsements."

Copyright © 2001 - 2002, Independent Insurance Agents of Texas. All rights reserved. E-mail [email protected] to comment on this material.