Week 4 Understanding Interest Rates

Interest rates – a key economic variable.

Interest rates affect economic activity. They determine whether people decide to save or spend. They determine whether people buy homes, cars or other goods. They determine whether firms will invest in capital equipment.

5 types of loans

o Simple loans – state how much must be paid back to the borrower at maturity. Example: you borrow $1000 today and agree to pay back $1300 two years from today.

o Fixed payment loan – like a car loan. You pay back a certain amount each month, say, for a certain number of months until the loan is paid off.

o Coupon bonds – Face value = $1000 Maturity date = 10 years

Coupon rate = 5% / year

Such a piece of paper would pay you $50 per year for 10 years and then $1000 at the end of ten years. So the face value is what you get at the maturity date of the bond. The coupon rate and the face value together determine how much you get each year.

At one time these bonds had little strips of paper (coupons) that the holder sent in to the company in order to receive payment (called clipping a coupon).

How much would one pay for such a piece of paper? That is market determined and depends on the market rate of interest.

o Discount bonds – (zero coupon bonds) Do not make regular payments like coupon bonds. You receive the face value at maturity. If the above bond had been a discount bond you would have received $1000 at the end of 10 years, but no annual payment. You might pay, say, $200 for such a bond. Clearly you would pay much less for a discount bond that for a coupon bond with the same face value.

1 o Consuls or consols – coupon bonds with no maturity date Face value = $1000

Coupon rate = 5%

How much would one pay for a consol? This instrument will pay you $1000X0.05 = $50/year on a $1000 investment. Suppose that you have some money to invest and that the market rate of interest is 10%. If you give the owner of the consol $1000 you will only earn 5% on your $1000 which is a bad deal because you could be earning 10%. If you gave the owner of the consol $500 then you would earn 10% on your $1000.

Suppose that the market rate of interest fell to 5%. Now how much would the consol be worth. If you gave the owner $1000 you would earn 5% on the consol. If the market rate of interest fell to 2.5% the consol would be worth $2000.

Market interest rate Price of consol 10% $500 5% $1000 2.5% $2000

Note the inverse relationship between the price of an existing consol and the market rate of interest. This will occur constantly in this course. If market rates of interest fall then bond prices go up.

Present Value, Future Value and the Yield to Maturity.

Future value. How much money will you have at maturity if you invest a sum PV in a debt instrument where the interest rate is I? o Simple loan of $1000 for 1 year at 5% . FV=(1 + i ) PV = (1 + 0.5)1000 = 1050 o Simple loan of $1000 for 2 years at 5% compounded yearly FV=(1 + i )(1 + i ) PV = (1.05)(1.05)1000 . FV =1102.50

2 Present value Reverse the process. If you want to get a certain amount of money in the future and the interest rate is I , how much will you need to invest now? o You want $1000 from a simple loan for 1 year at 5% FV 1000 . PV = = = 952.38 (1+i) ( 1 + 0.05) o You want $1000 from a simple loan for 2 years compounded yearly FV 1000 . PV = = = 907.03 (1+i)( 1 + i) ( 1 + 0.05)( 1 + 0.05)

Yield to maturity (internal rate of return) -- often considered most accurate measure of interest rates. You have a certain amount now (PV), you would like to have a certain amount in the future (FV), then what the interest rate have to be to get you there

Given PV and FV solve for i.

o Simple loan. You have $800 now and you want $1000 one year from now

FV PV = (1+ i) FV PV = (1+ i) FV (1+i) = PV FV 1000 i = -1 = - 1 = 1.25 - 1 = 0.25 PV 800

o Simple loan compound over two years. Have $800 want $1000 FV PV = (1+i) (1 + i )

2 FV (1+i) = PV 1+i = FV PV i =FV -1 =1000 - 1 = 1.118 - 1 = 0.118 PV 800

3 o For simple loans, the simple interest rate equals the yield to maturity. o Fixed payment loan this kind of loan has the same payment every period of the life of the loan (auto loan) FP FP FP FP PV = + + +⋯ + (1+i)1( 1 + i) 2( 1 + i) 3 ( 1 + i)n

where

PV = loan value = present value FP = Fixed yearly payment n = number of years until maturity

Find the yield to maturity by solving for i.

This will be quite difficult to solve by hand if n>2. For fixed payment loans with large number of years to maturity people use (a) tables, (b) financial calculators, or (c) a spreadsheet or some other computer program. o Coupon bond C C C C F PV = + + +⋯ + + (1+i)1( 1 + i) 2( 1 + i) 3 ( 1 + i)n( 1 + i) n

where

PV = price of the coupon bond (the present value when you buy it) C = yearly coupon payment F = face value of the bond n = number of years to maturity

Again solving for I (the yield to maturity) will be difficult calling for something other than hand methods.

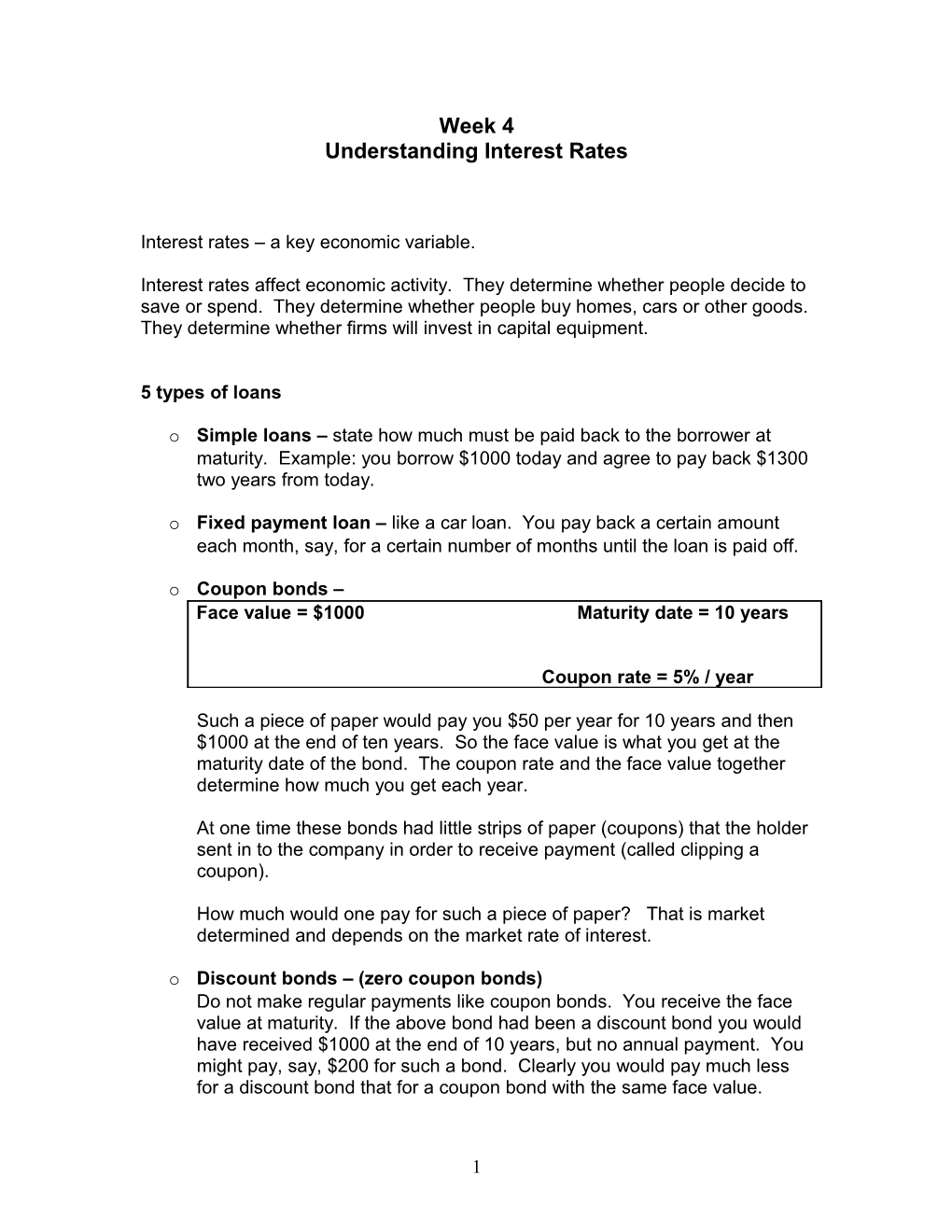

4 Computing yield to maturity using EXCEL.

Figure 1. Using EXCEL to compute the yield to maturity for a 10% coupon rate bond maturing in 10 years with a $1000 face value. See Table 1 on page 73 of the Mishkin text.

Excel also has an internal rate of return function which may be easier to understand if payments are made on a yearly basis

5 Figure 1 shows the commands to use the YIELD function in EXCEL to compute yields to maturity. Compare this with the results shown on Table 1 in Mishkin. Note that the price was divided by 10 as required by EXCEL

Some things to note 1. When the coupon bond is priced at its face value, the yield to maturity equals the coupon rate 2. The price of the coupon bond and the yield to maturity are negatively related: that is as the yield to maturity rises the price of the bond falls. As the yield to maturity falls the price of the bond rises. The same held for the consol. 3. The yield to maturity is greater than the coupon rate when the bond price is below the face value.

o Discount bonds FV . PV = n (1+ i)

Again solve for i.

Figure 2. Using EXCEL to compute the yield to maturity of a discount bond with a 10 year maturity date and a face value of $1000. Again note that yield to maturity and the price of the bond have a negative relationship.

6 Other Measures of Interest Rates

Current Yield (for coupon bonds) . This is an approximation of the yield to maturity for a coupon bond. Back before calculators and spreadsheet existed it was used because it was easy to calculate compared to the yield to maturity.

C i = c P

ic = current yield P = Price of the coupon bond C = Yearly coupon payment

The current yield will be a good approximation to the yield to maturity for bonds with lengthy maturity dates. It will not be such a good approximation for bonds with short maturity dates. It will be a good approximation for bonds when the price of the bond is close to the par value of the bond. It will not be such a good approximation when the price is not close to the par value. However both the yield to maturity and the current yield will decrease if the bond price increases.

7 Figure 3. shows the yields to maturity of a bond with a $100 coupon, a face value of $1000, and a price of $900 for different maturity dates. Compare these with the current yield of 100/900 = 0.11111 for each maturity date. Note that the approximation is pretty good for bonds with a maturity of 10 and 20 years.

Figure 4. shows the yields to maturity and current yields for coupon bonds with a $100 coupon payment, a $1000 face value, a 20 year maturity and various bond prices. In this case the current yield is a pretty good approximation for the prices shown.

Figure 3: Yields to maturity and current yields for coupon bonds with $100 coupon, $1000 face value and $900 price for different maturities.

8 Figure 4. Yields to maturity and current yields for coupon bonds with a $100 coupon payment, a $1000 face value, a 20 year maturity and various bond prices.

Yield on a discount basis

. Solve for I (yield to maturity) for a discount bond (particularly short term bonds like treasury bonds . FV PV = (1+ i)n is a little tough without a computer of calculator, so we use and approximation FV- PV 360 i = db FV days to maturity

idb = yield on a discount basis FV = face value PV = prive of bond (present value) this calculation tends to understate the yield to maturity

9 Note that the yield on a discount basis always understates the yield to maturity. Also note that the understatement is more severe the longer the maturity. But this may work reasonably well for short term bonds like T-bills.

10 Distinction between interest rates and rates of return.

Suppose you purchased the following consol for $1000 Face value = $1000

Coupon rate 5%

This consol will pay FV*coupon rate = $1000X0.05 = $50 per year. So you will earn an interest rate of 5% on your $1000. But suppose that some time in the future you decide to sell the consol and the market interest is 10%. How much will you be able to sell the bond for? An investor with $1000 can earn $100 per year on the market, so he won’t give you $1000 for the bond. He will give you $500 so that he will earn his 10%. You just suffered a capital loss.

If you sold the bond for $500 after one coupon payment you would receive $500+ $50 on your investment of $1000. The rate of return on your investment then is $500+ $50 - $1000 - $450 RET = = =0.45 = - 45% $1000 $1000

Generally the formula for the rate of return on an investment held from time t to time t+1 is C+ P - P RET = t+1 t Pt RET = the rate of return

Pt= the price of the bond at P t

Pt+1= the price of the bond at P t + 1 C = the coupon payment

This can be rewritten as

RET= ic + g

P- P g =t+1 t = the rate of capital gain Pt C ic = = the current yield Pt

11 Table 2: This is Table 2 from your text showing one year rates of return on different maturity 10% coupon rate bonds when interest rates rise from 10% to 20%. (all these bonds were purchased at par or face value). The one year bond is unaffected because it has matured and you collect the face value. The others sell at a capital loss.

Excel has a Price function that can compute these values

Figure 5. The price of the bonds shown in Table 2 as calculated by Excel

Note: Prices and returns for long term bonds are more volatile than for short term bonds. The risk of facing a capital loss is call interest rate risk. Also note that the rate of return calculation assumes that you hold the bond for one year. This is so we only have one coupon payment to worry about. If the bond were

12 held for more than one coupon payment we would have to include the reinvestment of the coupon payments in the calculation and that would get a little messy.

Real and Nominal Interest Rates

Real interest rates are nominal interest rates adjusted for inflation. Nominal interest rates are what you actually pay when you make a loan or what you receive when you lend money. That is nominal rates are the terms in which the contract is written. The relationship between them is given by Fisher’s equation

e i= ir +p or e ir = i -p i = the nominal interest rate

ir = the real interest rate p e = the expected rate of inflation

Suppose that you lend someone $100 at a 5% interest rate because you would like to have $105 of real goods a year from now. If you can’t get more real goods a year from now you would be just as happy to have $100 of real goods now.

If the inflation rate is 5% then you will have $105 one year from now, but it will only buy the same goods that you could have now. All you will have done is postponed using those goods for a year. In order to be able to purchase the $105 of real goods you need to build an inflation factor into the terms of the loan. So the nominal rate you will require is e i= ir +p =5% + 5%

So if you want 5% more of real goods you should charge a 10% nominal interest rate if you expect the inflation rate to be 5%.

How about taxes

The Fisher equation presented above ignores the effect of the marginal tax rate. Again the goal is to get a certain amount of real good in the future and the government is going to get a part of the interest payment. Fisher’s equation adjusted for marginal taxes is e ir = i(1 -t) - p i +p e i = r (1-t ) t = the marginal tax rate.

13 So if you want 5% more real goods a year from now and you expect the inflation rate to be 5% and if you are in the 30% tax bracket then you should charge a nominal rate of

i +p e 5%+ 5% i =r = =14.29% (1-t ) ( 1 - 0.3) in order to get an actual increase of 5% in real terms.

14 Reading the Wall Street Journal

Page 80 in Mishkin text

Rate means the coupon rate

Bid is how much a dealer will pay for such a bond

Asked is how much they will sell it for (Asked – Bid = profits)

Ask Yld = Asked Yield = yield to maturity if you buy it ask the asked price.

Chg is how much the bid price has changed from the previous day (in 32nds)

All bonds are in terms of a $100 face value bond. So if the particular bond in question has a face value of $1000 multiply these prices by 10. You don’t want to have one table for $100 bonds and another for $500 bonds and another for $1000 bonds, etc.

Consider T-bond 1 with a asked price of 99:30. This is Wall Street short hand for 99+30 = 99.938 = 999.38 a price of 32 if we are talking about a $1000 face value bond.

The current yield is 3 3 C 5 5 + 5.375 i = =8 = 8 = = 5.38% c P 99.938 99.938 99.938 and the current yield is fairly close to the yield to maturity

15 For T bond 2

C =81 = 8.50 2 i = 5.26 P =100 : 05 = 100 + 5 32 = 100.156 C 8.5 i = = = 8.49% c P 100.156

For T bond 3

C = 6 1 2 i = 6.82 P =96 : 03 = 96 + 3 32 = 96.0938 C 6.5 i = = = 6.76% c P 96.0938

The current yield is close to the yield to maturity for T bond 3 but not for T bond 2. That is because the maturity date (2026) for T bond 3 is about 26 years away (the data is taken from the 26 Jan 2000 issue of the Wall Street Journal. This is very close to a consol so it is not surprising that the coupon rate, the yield to maturity and the current yield should be very close.

The current yield on T bond 2 is not close to the yield to maturity. (8.49% compared to 5.26%). Also note that the coupon rate and the yield to maturity are not close for this bond either.

16 Panel B on page 80 in Mishkin is for Treasury bills (short term discounted bonds).

These are discount bonds. The Bid and the Asked refer to discount yields not prices. Note here that the Bid is higher than the Asked. These are not prices however these are yields. Recalling the negative relationship between yields and prices the Bid yield should be higher than the Asked yield so the the Bid Price will be lower than the Asked price.

The Chg column refers to how much the Asked yield has changed from the previous day. It is in terms of basis point. A basis point is 1/100th of a percentage point. The Feb 17 bill increased by 4 basis points from the previous day.

The Ask Yld column is the yield to maturity. Note that the Asked discount yield underestimated the yield to maturity.

17 The first column indicates who has issued the bond, AT&T in this case. 5 5 The second item is the coupon rate ( 8 ) This is followed by the maturity date (2004). The Cur Yld is the current yield. The Vol indicates the number of bonds traded that day. The Close indicates the last traded price 941= 94 + 1 = 94 + 0.125 = 94.125 = 941.25 for a $1000 face value bond. 8 8 Then given the face value, the coupon rate, the maturity date and the price paid the yield to maturity could be calculated (but the Journal does not compute it for you).

Note that the Yield to maturity (8.4%) is very close to the coupon rate for Bond 2. That is because it the maturity date is a long way off (31 years). For Bond 1 the maturity date is much sooner (4 years) and the yield to maturity (7.37%) is not close to the coupon rate. Similar statements hold for the current yield.

18