Practice 2 solution

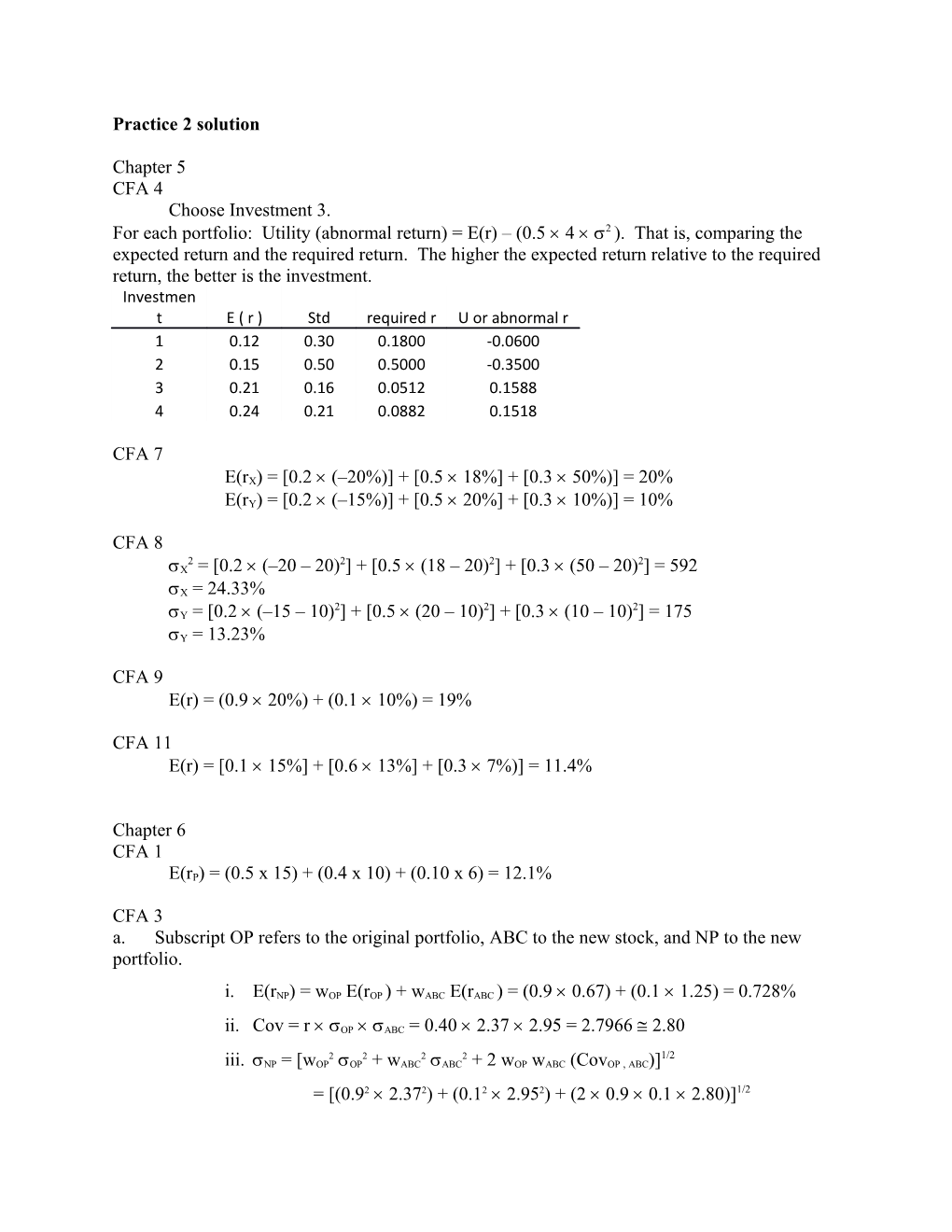

Chapter 5 CFA 4 Choose Investment 3. 2 For each portfolio: Utility (abnormal return) = E(r) – (0.5 4 ). That is, comparing the expected return and the required return. The higher the expected return relative to the required return, the better is the investment. Investmen t E ( r ) Std required r U or abnormal r 1 0.12 0.30 0.1800 -0.0600 2 0.15 0.50 0.5000 -0.3500 3 0.21 0.16 0.0512 0.1588 4 0.24 0.21 0.0882 0.1518

CFA 7

E(rX) = [0.2 (–20%)] + [0.5 18%] + [0.3 50%)] = 20%

E(rY) = [0.2 (–15%)] + [0.5 20%] + [0.3 10%)] = 10%

CFA 8 2 2 2 2 X = [0.2 (–20 – 20) ] + [0.5 (18 – 20) ] + [0.3 (50 – 20) ] = 592

X = 24.33% 2 2 2 Y = [0.2 (–15 – 10) ] + [0.5 (20 – 10) ] + [0.3 (10 – 10) ] = 175

Y = 13.23%

CFA 9 E(r) = (0.9 20%) + (0.1 10%) = 19%

CFA 11 E(r) = [0.1 15%] + [0.6 13%] + [0.3 7%)] = 11.4%

Chapter 6 CFA 1 E(rP) = (0.5 x 15) + (0.4 x 10) + (0.10 x 6) = 12.1%

CFA 3 a. Subscript OP refers to the original portfolio, ABC to the new stock, and NP to the new portfolio.

i. E(rNP) = wOP E(rOP ) + wABC E(rABC ) = (0.9 0.67) + (0.1 1.25) = 0.728%

ii. Cov = r OP ABC = 0.40 2.37 2.95 = 2.7966 2.80

2 2 2 2 1/2 iii. NP = [wOP OP + wABC ABC + 2 wOP wABC (CovOP , ABC)] = [(0.92 2.372) + (0.12 2.952) + (2 0.9 0.1 2.80)]1/2 = 2.2673% 2.27%