The Future of U.S. Manufacturing – A Literature Analysis (Part III)

2012 Kathryn Hewitt – Intern, MIT Washington Office, Spring 2012

(with additional entries from Queenie Chan - Intern, MIT Washington Office, Summer 2012) Table of Contents Foreword...... 3 Reports Summarized: National Science and Technology Council – A National Strategic Plan for Advanced Manufacturing (February 2012)...... 4-6

Susan Helper, Timothy Krueger, and Howard Wial, Metropolitan Policy Program at BROOKINGS – Why Does Manufacturing Matter? Which Manufacturing Matters? A Policy Framework (February 2012) ...... 7-10

David Autor, David Dorn, Gordon Hanson - The China Syndrome: Labor Market Effects of Import Competition in the United States (MIT Economics paper August 2011)...... 12-13

Connect Innovation Institute – Two Systems of Innovation: Recommendations for Policy Changes to Support Innovation, Production and Job Creation (February 2012) ...... 14-15

Council on Competitiveness – U.S. Manufacturing Competitiveness Initiative: Make an American Manufacturing Movement (December 2011)...... 16-19

Information Technology and Innovation Foundation – Worse than the Great Depression: What the Experts are Missing about American Manufacturing Decline (March 2012)...... 20-24

Institute for Defense Analyses – Emerging Global Trends in Advanced Manufacturing (March 2012) ...... 25-27

Gregory Tassey, “Beyond the Business Cycle: The Need for a Technology-Based Growth Strategy” (NIST working paper Feb. 2012)……………………………………………………………………….28-31

Susan Houseman, Christopher Kurz, Paul Lengermann, and Benjamin Mandel. 2010. "Offshoring and the State of American Manufacturing." Upjohn Institute Working Paper No. 10-166 (Kalamazoo, MI: W.E. Upjohn Institute)……………………………………………………………..32-33

Jonas Nahm and Edward S. Steinfeld, Scale-Up Nation: Chinese Specialization in Innovative Manufacturing (MIT working paper March 12, 2012)…………………………………………………….34-37

U.S. Department of Commerce, Economics and Statistics Administration, The Benefits of Manufacturing Jobs (May 9, 2012).………………………………………………………………………………….38-39

2 Steering Committee for the Advanced Manufacturing Partnership (for PCAST), Capturing Domestic Competitive Advantage in Advanced Manufacturing (July 17, 2012)………………..40-42

Additional Suggested Reports to Review ...... 43

Foreword

The following is a summary and analysis of reports issued by various institutions looking at the topic of advanced manufacturing and its future in the United States. At this pivotal point in America’s manufacturing history, decisions are being made as a result of several study findings. The following analysis looks at both studies and their findings along with policy recommendations. There is heavy attention given the critical, emerging trends in advanced manufacturing, how they align with the investment and growth interests of nations around the world, and what the industry is expected to look like several decades down the road. The end of the report contains a page with several suggested further reports to review. This summary was prepared by Kathryn Hewitt, Intern, MIT Washington Office, Spring 2012; it was supplemented with additional summaries by Queenie Chan, MIT’13, Intern, MIT Washington Office, Summer 2012.

This summary is preceded by two similar reports issued earlier by MIT Washington Office: Future of U.S. Manufacturing – A Literature Review, Parts I and II. Link to these previous MIT Washington Office summaries: http://web.mit.edu/dc/policy.html (available under “Policy Resources” - “Manufacturing”).

3 National Science and Technology Council - A National Strategic Plan for Advanced Manufacturing (February 2012)(interagency group including NIST, NSF, DOD, DOE)

(http://www.whitehouse.gov/sites/default/files/microsites/ostp/iam_advancedmanu facturing_strategicplan_2012.pdf)

The National Science and Technology Council (NSTC) issued a plan documenting “the fundamental importance of advanced manufacturing” to the nation’s competitiveness and security and setting forth key objectives and priorities for federal policy in this area.

The acceleration of innovation for advanced manufacturing requires bridging a number of gaps in the present U.S. innovation system, particularly the gap between research and development (R&D) activities and the development of technologies innovation in domestic production of goods. This strategic plan “lays out a robust innovation policy that would help to close these gaps and address the full lifecycle of technology.” It also incorporates intensive engagement among industry, labor, academia, and government at the national, state and regional levels. Partnerships among diverse stakeholders, varying by location and objective, are a keystone of the strategy.

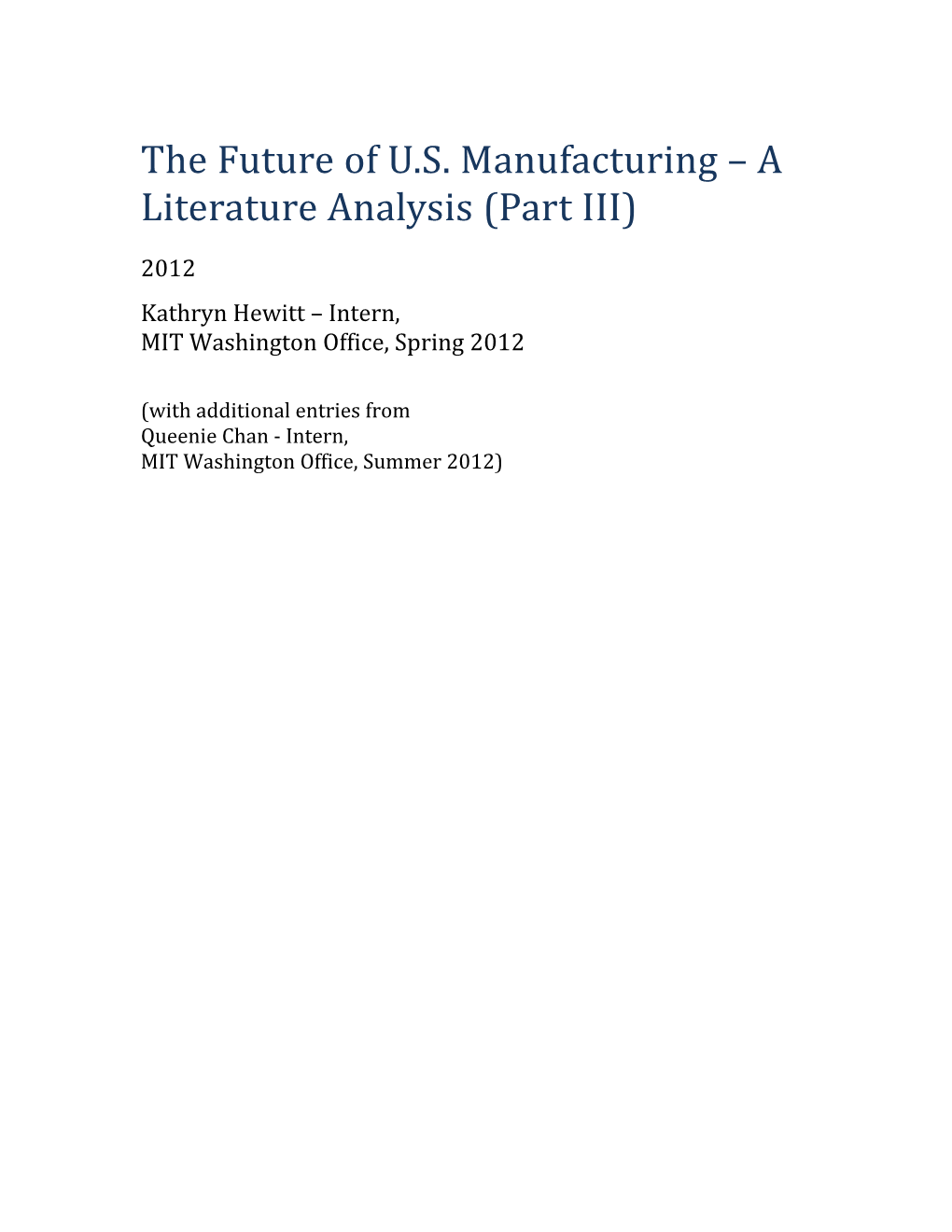

4 Manufacturing as a percentage of total GVA (Source: OECD, Industry and Services, STAN database, 2008)

The strategy seeks to achieve five objectives. These objectives are interconnected; progress on any one will make progress in the other seems easier. A large number of Federal agencies, coordinated through the NSTC, have important roles to play in the implementation of the strategy.

Objective 1: Accelerate investment in advanced manufacturing technologies, especially by small and medium-sized manufacturing enterprises, by fostering more effective use of Federal capabilities and facilities, including early procurement by Federal agencies of cutting-edge products.

Objective 2: Expand the number of workers who have the skills needed by a growing advanced manufacturing sector and make the education and training system more responsive to the demand for skills.

Objective 3: Create and support national and regional public-private, government-industry-academic partnerships to accelerate investment in and deployment of advanced manufacturing technologies.

Objective 4: Optimize the Federal government’s advanced manufacturing investment by taking a portfolio perspective across agencies and adjusting accordingly.

Objective 5: Increase total U.S. public and private investments in advanced manufacturing R&D.

5 Of particular interest are four categories of investment that “help to position promising, nascent technologies for broad adoption and commercialization”:

1. Advanced Materials

2. Production Technology Platforms

3. Advanced Manufacturing Processes

4. Data and Design Infrastructure

The appendix of the strategy also contains a skills competency model framework for Advanced Manufacturing. The model was developed through collaborating efforts of the DOL Employment and Training Administration (ETA) and other industry organizations. The updated model was completed in 2010 and has acquired new information on Sustainable and Green manufacturing with an update in key behaviors in several competency areas.

6 Susan Helper, Timothy Krueger, and Howard Wial - Metropolitan Policy Program at BROOKINGS - Why Does Manufacturing Matter? Which Manufacturing Matters? A Policy Framework (February 2012)

(http://www.google.com/url? sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=0CC4QFjAA&url=http%3A%2F %2Fwww.brookings.edu%2F~%2Fmedia%2FFiles%2Frc%2Fpapers %2F2012%2F0222_manufacturing_helper_krueger_wial %2F0222_manufacturing_helper_krueger_wial.pdf&ei=t12ET4y- HYbc9ASuyI3XCA&usg=AFQjCNHwbtm6hOGAFROI2mamWo2v8gCDvw)

Summary Manufacturing matters to the United States because it provides high-wage jobs, commercial innovation (the nation’s largest source), a key to trade deficit reduction, and a disproportionately large contribution to environmental sustainability. The manufacturing industries and firms that make the greatest contribution to these four objectives are also that that have the greatest potential to maintain or expand

employment in the United States. Computers and electronics, chemicals (including pharmaceuticals), transportation equipment (including aerospace and motor vehicle and parts), and machinery are especially important.

7 Productivity and wages vary greatly within as well as between industries. In any industry, manufacturers that are not already at the top have room to improve their performance by adopting “high-road” production, in which skilled workers make innovative products that provide value for consumers and profits for owners. Analysis

In asking the main question: Why does manufacturing matter? A few data points are helpful to understand the answer.

Manufacturing today accounts for 12 percent of the U.S. economy and about 11 percent of private-sector workforce.

Manufacturing provides high-wage jobs.

Manufacturing is the major source of commercial innovations and is essential for innovation in the service sector.

Manufacturing can make a major contribution to reducing the nation’s trade deficit.

Manufacturing makes a disproportionately large contribution to environmental sustainability.

8 From a policy development perspective it is useful to identify the major factors that seem to determine which industrial cities are likely to make a successful transition away from their manufacturing foundation, while still acknowledging these economic “roots”. And in reading the papers above and others, these factors seem to coalesce around the following:

Education/training: those industrial cities that have outperformed their peers have done a better job of identifying and developing the skills required by employers;

Taking a regional perspective: those cities that have performed better than average have looked beyond their city limits for solutions to their problems; this willingness to engage in active, positive collaboration with other cities and towns in the same “economic region” seems to have paid dividends for all of the participants;

Access to Capital: “resurgent” and “resilient cities in general, have done a better job of identifying and developing multiple sources of economic

9 development capital including private investment and philanthropic sources of capital;

Leadership: while difficult to measure, the impact of effective leadership was easy to see in terms of the performance of resurgent cities. This leadership can originate in the public or private sector and is very often a combination of both centers of influence.

Many thought the U.S. was losing manufacturing jobs because of increased manufacturing productivity. This study contends, however, that the historical pattern of productivity gains leading to job growth not contraction remains in effect.

American manufacturing will not realize its potential automatically. While U.S. manufacturing performs well in wages and productivity compared to the rest of the U.S. economy, it performs poorly compared to manufacturing output in certain other high-wage countries. American manufacturing needs strengthening in four key areas. 1. Research and development

2. Lifelong training of workers at all levels 3. Improved access to finance

4. An increased role for workers and communities in creating and sharing in the gains from innovative manufacturing

10 These problems can be solved with the help of public policies that do the following:

Promote high-road production.

Include a mix of policies that operate at the level of the entire economy, individual industries, and individual manufacturers.

Encourage workers, employers, unions and government to share responsibility for improving the nation’s manufacturing base and to share in the gains from such improvements. This study does not necessarily suggest the U.S. manufacturing will dominate the global economy the way that it once did, but manufacturing remains a segment of our economy that is of critical importance and deserving of focus.

11 David Autor, David Dorn, Gordon Hanson - The China Syndrome: Local Labor Market Effects of Import Competition in the United States (MIT Economics paper August 2011)

(http://www.google.com/url? sa=t&rct=j&q=&esrc=s&source=web&cd=1&cts=1331666601611&ved=0CCgQFjAA&ur l=http%3A%2F%2Fecon-www.mit.edu%2Ffiles%2F6613&ei=fJ5fT- zWEoTb0QH46czMBw&usg=AFQjCNH5H3-e2o-5HpC5OZl7apGaIPXf3Q)

Abstract

“We analyze the effect of rising Chinese import competition between 1990 and 2007 on local U.S. labor markets, exploiting cross-mark variation in import exposure stemming from initial differences in industry specialization while instrumenting for imports using changes in Chinese imports by industry to other high-income countries. Rising exposure increases unemployment, lowers labor force participation, and reduces wages in local labor markets. Conservatively, it explained one-quarter of the contemporaneous aggregate decline in U.S. manufacturing employment. Transfer benefits payments for unemployment, disability, retirement, and healthcare also rise sharply in exposed labor markets. The deadweight loss of financing these transfers is one to two-thirds as large as U.S. gains from trade with China.” Summary

There are two main parts to the paper. The first, and main, conclusion is that areas most impacted by Chinese imports have lower labor force participation and reduced wages in both manufacturing and non-manufacturing firms.

12 The impact on wages and employment-to-population ratios spread across both non- manufacturing and manufacturing sectors. There are real costs, real losers to international trade, and the frictions that prevent these workers from being reabsorbed into the economy are also real. The costs are, at the least, more medium- term than is most commonly assumed. One of the main points in this paper as well is how clear it is that the normal compensation for losses from trade mechanisms—especially the Trade Adjustment Assistance Act (TAA)—amount to little more than rounding errors. The real mechanisms for redistribution effects from trade losses are workers going on disability and health insurance compensation. Food stamps play a major role, and the growth of food stamps over the past two decades could be thought of as part of trade policy in addition to welfare policy.

These amounts are just redistribution, not economic gains or losses in themselves. However, if you assume redistribution is a leaky bucket, the deadweight losses are about equal to the trade gains. The gains from trade with China are between $32 and $61 per person. The deadweight losses are estimated at $52 from the transfer mechanisms in place. This is a provocative framing and numerical analysis. One conclusion is that since the consequences of trade are very real, and the frictions involved in adjusting in the short and medium term are serious, the government needs to back its free trade regime with serous employment subsidies and mechanisms for coping with the consequences of trade. Another avenue of research that is important is the assumption that reduced employment from trade situation is

13 temporary and the gains from trade are permanent. Are these, particularly the first, reasonable assumptions? Under what conditions might they break down? Main Conclusions

The analysis finds that exposure to Chinese import competition affects local labor markets along multiple margins beyond its impact on manufacturing employment. Consistent with standard theory, growing Chinese imports reduce manufacturing employment in the exposed markets. More interesting is the conclusion that it also triggers a decline in wages that is primarily observed outside of the manufacturing sector. Reductions in both employment and wage levels lead to a steep drop in the average household earnings in affected regions. To summarize, studying labor markets in regions of U.S. where Chinese produced goods have captured markets, they found widespread patterns of rising unemployment and reduced wages not only in the affected manufacturing sectors but in a wide range of dependent and related job sectors, in both services and production. They found that the gains from trade were almost equally offset by deadweight losses, particularly through a rise in transfer payments for unemployment, health and disability insurance and food stamps required to cope with employment declines. The losses from trade tended to disproportionately impact particular affected production regions, resulting in significant disruptions there. This last conclusion emphasizes the importance of rising transfer payments though multiple federal and state programs. The largest of these transfers are federal disability, retirement and in-kind medical transfer payments. Unemployment insurance and income assistance programs play an important role, however secondary. Overall, the increase in U.S. importance of Chinese goods during the past few decades have ultimately caused a hindrance to regional employment and household incomes. These negative effects extend outside manufacturing and into the livelihood of worker and households in affected fields besides manufacturing.

Dan Breznitz andPeter Cowhey, Connect Innovation Institute - America’s Two Systems of Innovation: Recommendations for Policy Changes to Support Innovation, Production and Job Creation (February 2012)

14 (http://www.connect.org/programs/innovation-institute/docs/breznitz-cowhey- white-paper-0212.pdf) The report by Dan Breznitz and Peter Cowhey, writing for Connect’s Innovation Institute, evaluates the bipartisan consensus in Washington when it comes to the promotion of innovation. Most would agree that innovation is key to creating and maintaining new jobs and to boosting America’s competitiveness. The report outlines a strategy for manufacturing products and production innovation based on the interdependence of services and manufacturing in a new global setting. This strategy focuses on four building blocks that are critical to the future of American firms. These four building blocks are: 1. Shared production assets: firms need to fund and use assets held in common by a variety of contractual and institutional mechanisms. 2. Effective innovation network structures: markets, contracts, and firms no longer provide adequate “glue” for effectively linking together pools of innovators.

3. Flexible business models: restructuring the traditional definitions of supply and demand functions in markets is often as important as an innovative product. 4. Specialized financial institutions: risk assessment capacity and lending/investment models appropriate to different types of innovation. Research was conducted to focus on the concern of the growing inability of the U.S. innovation system to orchestrate the move from novel-product-innovation to novel- production located in the U.S. The report feels our concerns should be that:

a. High value-added innovations are no longer yielding the production and job base for American we assumed that they would be.

b. The supply base of small and medium firms for middle value-added products which could benefit from supply chain factors is both dwindling and not truly innovative. c. The changing mix of skills necessary for production and incremental product innovation in the small and medium enterprises (SME) supplier base falls outside of the range of core skills in the traditional production shops.

d. Our system of financing innovation has become increasingly fragmented, focusing on specific financial vehicles, which in turn specialize primarily in just one kind of innovation or one specific set of companies, and then necessitate a financial exit within a relatively short time frame.

The second part of the report discusses the need to update the conventional model if any viable solutions are going to transpire. These recommendations for the

15 Conventional Model are mainly focused on the financing end of both public and private sectors. 1. The U.S. Government funding for research and development is inadequate in size and has become too bureaucratized and conservative to allow clusters to achieve their potential.

2. The funding mechanism for startup and fast growth tech companies is no longer robust. Our practitioners focused on two problems.

a. The ability to fund commercial innovation at early stages is a growing problem.

b. Besides the initial money to start up, the struggle to keep the best people during the early stages of growth was crucial to success.

3. Concentrate on improving financing for the scale up of startup firms. When startup firms begin to scale up for large undertakings, especially production, they need to look for new sources of financing. They face problems with regard to commercial lending and funding from large (multinational).

The U.S. has all the necessary factors to continue to lead the world in innovation, while enjoying its job growth benefits. However, it is imperative to have a model that fits the needs of production firms, to achieve it within the next few years. Summary:

To summarize, Breznitz and Cowhey argue that the U.S. needs to better link the two systems of innovation it maintains. The first, the novel and breakthrough product/technology innovation system includes university research supported by R&D agencies – it is often known as the “pipeline” system, and uses “technology push” to implement its advances. The second, the process and incremental innovation system, emphasizes engineering enhancements to products and technologies including the way they are produced, distributed, and serviced, and is dominated by industry. Both are vital, yet our current technology policy model pays great attention to the former and little to the latter; the first system rarely comes to bear to assist the second. Manufacturing historically fallen into the second category, considered engineering/process and industry dominated, although, as has been demonstrated repeatedly over the decades, it can be novel and breakthrough as well. It has never been the focus of a major federal R&D effort. This is part of the reason why the U.S. continues to innovate technologies yet the product evolution occurs abroad. The authors suggest we should work to unify our systems, and bring the remarkable innovation talent in the first to support the second, as well as the first. This innovation organization reform is an important part of what we must accomplish if we to implement new manufacturing technology paradigms.

16 Council on Competitiveness - U.S. Manufacturing Competitiveness Initiative: Make an American Manufacturing Movement (December 2011) (www.compete.org/images/uploads/File/.../USMCI_Make.pdf)

The report by the Council on Competitiveness on America’s call to action in the manufacturing movement looks to address urgent macro-economic problems and submitting a solution to several challenges facing the US today. The report summarizes five challenges, along with solutions, to the domestic manufacturing movement, while outlining the five priority recommendations stemming from the challenges and solutions presented.

This report is in entirety based domestically. It looks to the involvement of the President, Congress, the public sector, education sector, and business sector to implement what is seen as not only a solution, to the manufacturing decline looming on the horizon but also, to the ever daunting economic and job crisis facing the US today. Further more, the report places a heavy emphasis on the national conversion which will need to take place for a flourishing manufacturing sector to emerge and turn things around on the home front. Where America Falls Short:

1. Production at scale for innovative start-ups: a. Risk capital firms regularly condition investing in a start-up on a commitment to produce overseas. U.S. tax policy, regulatory delays, structural costs and more competitive offshore incentives are commonly cited as threats to the capital firm realizing a return on its investment.

2. Domestic expansions and retooling of existing facilities: a. Tight credit lending, uncertainty over future U.S. policies and non- competitive structural costs are casing many firms to delay investment or increase capacity overseas.

3. Attracting production facilities to serve global markets:

17 a. Although the United States remains competitive as a global manufacturing export platform for several key products, many suspect America underperforms in drawing investment for this purpose. Across the globe, some manufacturing has to be performed in-country to serve that market. Manufactured goods in other sectors, however, are also produced for global or regional export, not all of which is low-margin or labor intensive. In these cases, the less competitive U.S. tax, regulatory and structural environments likely causes a loss of investment.

Five Challenges and Solutions to Make an American Manufacturing Movement 1. Challenge: Fueling the Innovation and Production Economy from Start-up to Scale-Up a. Solution: Enact fiscal reform, transform tax laws and reduce regulatory and other structural costs and create jobs. i. Congress should require agencies to begin reducing the costs and burdens of current and proposed regulations. ii. Congress should immediately reform section 404 of the Sarbanes-Oxely Act to increase entrepreneurs’ access to U.S. public capital markets and grow new companies.

iii. Congress should reduce the costs of tort litigation from the current level of almost two percent of GDP—some $248 billion —down to one percent by 2020. iv. Congress and the administration must take action on fiscal reform to achieve $4 trillion in debt reductions by 2021. 2. Challenge: Expanding U.S. Exports, Reducing the Trade Deficit, Increasing Market Access and Responding to Foreign Governments Protecting Domestic Producers.

a. Solution: Utilize multilateral for a, forge new agreements, advance IP protection, standards and export control regimes to grow high-value investment and increases exports. i. Industry CEOs and government leaders should elevate and advance U.S. technical standards and the voluntary consensus standards-setting process.

ii. Congress and the administration should ensure the President’s Export Control Reform Initiative is completed by the end of 2012 and push for improved foreign export control systems.

18 iii. Focus on actions to encourage China make permanent the special intellectual property rights campaign it ran from October 2010 to June 2011

3. Harnessing the Power and Potential of American Talent to Win the Future Skills Race

a. Solution: Prepare the next generation of innovators, researchers and skilled workers.

i. Congress should implement immigration reform to ensure the world’s brightest talent innovate and create opportunities in the United States. ii. Congress, states, academia, industry and national laboratories should renew efforts to expand STEM education and create opportunities to integrate into the workplace.

iii. The Small Business Administration should create a program modeled after the SCORE program for retired business executives to mentor and counsel entrepreneurs. iv. Industry and labor should develop state-of-the-art apprenticeship programs for 21st century manufacturing. v. The administration should create opportunities for America’s soldiers. vi. Academia, industry and government should launch the American Explorers Initiative to send more Americas abroad to study, perform research and work in global business.

vii. Congress should create opportunities and incentives for older Americans to remain vibrant contributors in the workforce.

4. Challenge: Achieving Next-Generation Productivity through Smart Innovation and Manufacturing

a. Solution: Create national advanced manufacturing clusters, networks and partnerships, prioritize R&D investments, deploy new tools, technologies and facilities, and accelerate commercialization of novel products and services.

i. Congress, the administration, industry, academia and labor should develop partnerships to create a national network of advanced manufacturing clusters and smart factor ecosystems.

19 ii. Congress, the administration, national laboratories and universities should advance the U.S. manufacturing sector’s use of computational modeling and simulation and move the nation’s High Performance Computing capabilities toward Exascale.

iii. The U.S. Department of Commerce through the Economic Development Administration, in partnerships with the Council on Competitiveness should expand the Midwest Project for SME-OEM Use of Modeling and Simulation through the National Digital Engineering and Manufacturing Consortium (NDEMC).

iv. Accelerate innovation from universities and national laboratories by facilitating greater sharing of intellectual property and incentivizing commercialization. 5. Challenge: Creating Competitive Advantage through Next Generation Supply Networks and Advanced Logistics. a. Solution: Development and deploy smart, sustainable and resilient energy, transportation, production and cyber infrastructures. i. Congress should increase the number of public-private infrastructure partnerships and explore opportunities to privatize large infrastructure projects.

ii. Congress should authorize the Export-Import Bank to fun domestic infrastructure projects.

iii. Congress should develop and implement a national strategy to reduce overall energy demand by rewarding efficiency and improving transmission infrastructure. iv. Congress and the administration should create a Joint Cyber Command to import cyber infrastructure and protect traditional defense, commercial and consumer interests.

Priority Recommendations from the Five Challenges 1. Congress should permanently replace the current world-wide double taxation system with a territorial tax system to facilitate the repatriation of earnings and restructure the corporate tax code to increase investment, stimulate production at scale and neutralize sovereign tax incentive investment package.

20 2. Congress, the administration and industry should intensify efforts to support the President’s goal to double exports from $1.8 to $3.6 trillion and reduce the trade deficit by more than 50 percent.

3. Federal, state and local governments along with high schools, universities, community colleges, national laboratories and industry should prioritize Career and Technical Education (CTE) programs and push for greater integration of community colleges in the innovation pipeline.

4. Congress and the administration should leverage R&D investments across the federal research enterprise to solve challenges in sustainable smart manufacturing systems and to ensure a dynamic discovery and innovation pipeline.

5. Congress and the administration should drive the private sector to develop and utilize all sources of energy on a market basis while enforcing efficiency standards to ensure a sustainable supply of energy to manufacturers.

Information Technology and Innovation Foundation (ITIF) - Worse then the Great Depression: What the Experts Are Missing about American Manufacturing Decline (March 2012)

21 (http://www.itif.org/publications/worse-great-depression-what-experts-are-missing- about-american-manufacturing-decline)

The erosion of American manufacturing in the past decade has been far more severe than commonly recognized, with sharp declines not only in employment but also in output, according to a new report by the Information Technology and Innovation Foundation (ITIF).

“Worse than the Great Depression: What the Experts Are Missing about American Manufacturing Decline” debunks widely held myths about productivity gains, restructuring, and a manufacturing renaissance, and reveals the stark reality of a historic decline in U.S. competitiveness and unprecedented deindustrialization. The report explains what the United States is experiencing is not merely another boom and bust cycle but a structural decline more akin to what Britain experienced in the 1960s and 1970s when it lost its industrial leadership.

“What we discovered flies in the face of nearly all the reporting and commentary on manufacturing and reveals a disturbing truth,” said ITIF president Robert Atkinson, the report's chief author. “U.S. manufacturing jobs have been lost not simply because the sector is more productive. It is producing less. And unlike some high-wage nations, America is not replacing low-value-added manufacturing with high-valued- added manufacturing or opening new plants to replace closed ones. There is difference between restructuring and decline. American manufacturing is in decline.”

From January 2000 to January 2010, the United States lost one-third of its manufacturing jobs, almost 5.5 million. This is likely the highest rate of manufacturing job loss in American history, exceeding even the rate of loss in the Great Depression. In addition, economy-wide job losses in the past decade were far more concentrated in manufacturing than during the Great Depression. But unlike the period after the Depression or in the recoveries from recessions after World War II, the recent rebound in manufacturing has been far weaker than portrayed by recent news reports, and comes off the steepest decline of any post-war recession.

In the face of these unprecedented losses, expert opinion has been remarkably blasé, attributing the massive job loss to manufacturing's superior productivity performance. That view is based almost entirely on one number - change in real manufacturing value added as a share of GDP. But the report finds that U.S. government data significantly overstates this macro number, in part by vastly overstating value-added growth in the computer and electronic products sector and by miscalculating the price of imports of intermediate manufacturing inputs.

22 U.S. government statistics significantly overstate the change in U.S. manufacturing output, and by definition productivity, in part because of massive overestimation of output growth in the computer and electronics sector.

According to the U.S. Bureau of Economic Analysis, growth of output in the computer and electronics sector accounted for more than all the output growth in U.S. manufacturing. In other words, collectively the other 18 U.S. manufacturing sectors produce less today than they did in 2000. In fact, when measured accurately, real manufacturing output declined by 11 percent in the past decade, at a time when the overall economy grew by more than 11 percent. Compare that to prior decades when manufacturing output grew by upwards of 35 percent. Something went seriously wrong in the 2000s.

The report also refutes the commonly expressed view that other industrialized high- skill nations are also failing behind in manufacturing. There's nothing normal or preordained about rich countries losing manufacturing. While nations such as

23 Austria, German, Korea, the Netherlands and Sweden have seen increased or stable manufacturing output growth, only the United States and a handful of other nations (e.g. Canada, Spain, Italy and the UK) have seen outright losses).

The report shows these losses have not been due to declining demand for manufactured goods. Demand has stayed robust. What has declined is U.S. production of those goods as the manufacturing trade deficit has soared.

Despite the sobering findings, the report also emphasizes that manufacturing is still critical to America's economic future. Manufacturing still adds $1.6 trillion to GDP, employs 12 million people and is a traded sector, which means when we lose a manufacturing job due to foreign competition it is not automatically replaced by the market.

ITIF emphasizes that policy changes like a more competitive corporate tax code, increases in funding for manufacturing-focused R&D and programs to train manufacturing workers, and increased efforts to fight unfair or illegal trade practices can stem the tide and help restore the U.S. manufacturing base.

“America needs to wake up to the fact that a series of grave policy errors have left us a production foundation that is too weak to support the kind of economy we need to build. We will need new policies to build a new manufacturing foundation,” said Atkinson. “This is a central economic task for America for this decade.”

Among the findings in the report:

Productivity: Between 2000 and 2010, government data overestimated manufacturing labor productivity by a remarkable 122 percent. Output: Rather than rising by 16% as the government data indicated, manufacturing output during that period actually fell by 11 percent. If manufacturing output had grown at the same rate as the rest of the business sector, the United States would currently have 13.3 million more jobs. Job losses: Today, more Americans are unemployed - a total of 12.8 million - than there are Americans who work in manufacturing, 12 million. On average, every day for the past 12 years, the United States lost 3,643 jobs - 1,243 net manufacturing jobs plus approximately 2,400 additional jobs because of manufacturing's multiplier effect. Manufacturing capital stock: While the amount of capital (e.g. machines, factories, computers) grew by 20 to 40 percent per decade prior to 2000, in this past decade it grew by less than 2 percent. Plant closings: Since 2000, a net 60,300 manufacturing plants closed, or 15 per day. Recovery: While the economy has been adding manufacturing jobs during the current recovery, for every six jobs lost in the 2000-2010 period, only one was restored as of January 2011.

24 Decline in the States: Only two U.S. states experienced less than double-digit declines in manufacturing employment in the 2000s.

Summary of Underlying Points/Findings:

Employment: Over the past fifty years manufacturing’s share of GDP has shrunk from 27% to below 12%. For most of this period (1965-2000), manufacturing employment generally remained constant at 17 million; over the past decade it fell precipitously by 31.4%, to just below 12 million. All manufacturing sectors saw job losses between 2000 and 2010, but lower value sectors readily subject to globalization, such as textiles and furniture, were most adversely affected, losing almost 70% and 50% of their jobs, respectively. Investment: Manufacturing fixed capital investment (plant, equipment and IT) grew in the 2000s at its lowest rate as a percent of GDP (below 1.5% annually) since this data began to be compiled at the end of World War II. If this number is adjusted for cost changes, manufacturing fixed capital investment actually declined in the 2000s (down 1.8%) -- the first decade this has occurred since data collection began in the 1950’s. In contrast, manufacturing investment grew at an average of 5.5% annually in the 1990s. Investment in the 2000s declined in 15 of 19 industrial sectors measured by Bureau of Economic Analysis. Output: While we have been assuming from published government statistics that U.S. manufacturing net output as a share of world output has been stable, [only passed last year by China], we may have been fooling ourselves. ITIF argues [and other economic evaluations suggest] that the official U.S. output data have been significantly overstated. The official government data indicate that net output in 16 of 19 manufacturing sectors declined in the 2000s, in many significantly, but show these declines were offset by two sectors, computing and energy. ITIF makes three arguments. First, the number of foreign components in U.S. manufactured products has risen sharply and these have not been adequately accounted for, overstating U.S. output. Second, although employment in the computer sector declined by 43%, a significant amount of computer production moved offshore, and nominal U.S. industry shipments in this sector barely grew, government data included an inflationary output factor for increased computer quality and performance that caused the computing sector’s output to be significantly overstated in the 2000s. Third, output in the energy sector, similarly, was significantly overstated. Adjusting for these factors, ITIF found that net U.S. manufacturing value actually fell by 11% in the 2000s.

Productivity: Since output is a factor in productivity, assumptions about strong productivity growth in manufacturing must be scaled back as well, although manufacturing still significantly exceeds service sector productivity. ITIF finds manufacturing productivity grew by 32% between 2000 and 2010, not by the BEA’s much higher estimate of 71%. As adjusted, against 19 other leading manufacturing nations, the U.S. was 10th in productivity growth and 17th in net output growth.

25 Many thought the U.S. was losing manufacturing jobs because of increased manufacturing productivity. ITIF finds, however, that productivity gains accounted for only about a third of the 5.8 million manufacturing job loss of the past decade. This means we have to look elsewhere for reasons why manufacturing lost nearly one third of its workforce in a decade.

In short, U.S. manufacturing employment is down, manufacturing capital investment is down, manufacturing output is down, and manufacturing productivity is lower than previously estimated.

26 Institute for Defense Analyses (STPI) - Emerging Global Trends in Advanced Manufacturing (March 2012) (https://www.ida.org/upload/stpi/pdfs/p-4603_final2a.pdf)

This report on Emerging Global Trends in Advanced Manufacturing is by the Science & Technology Policy Institute (STPI - part of the Institute for Defense Analyses), prepared for the Office of the Director of National Intelligence. The study stresses that manufacturing technologically is a moving frontier. This is a brief overview of an in depth report.

In 20 years, manufacturing is expected to advance to new frontiers, resulting in an increasingly automated and data-intensive manufacturing sector that will likely replace traditional manufacturing as we know it today.

The report highlights five converging overall trends: • Ubiquitous role of information technology. • Reliance on modeling and simulation in the manufacturing process. • Acceleration of innovation in supply-chain management. • Move toward the ability to change manufacturing systems rapidly in response to customer needs and external impediments. • Acceptance and support of sustainable manufacturing. A number of these trends are not simply technological, but have organizational and business-model focused as well.

On the technology side, the authors see major advances in two mature areas and two emerging technologies. The mature areas are semiconductor fabrication and advanced materials with a focus on integrated computational materials engineering. The emerging technologies are additive manufacturing (aka 3D printing) and biomanufacturing with a focus on synthetic biology.

As a result of the combination of the overall trends and the technological advances, they postulate the following future scenarios:

Our research into advanced manufacturing points to an increasingly automated world that will continue to rely less on labor-intensive mechanical processes and more on sophisticated information-technology-intensive processes. This trend will likely accelerate as advances in manufacturing are implemented.

Over the next 10 years, advanced manufacturing will become increasingly globally linked as automation and digital supply-chain management become the norm across enterprise systems. This trend will be enabled by adaptive sensor networks that allow intelligent feedback to inform rapid analyses and decision-making.

Countries and companies that invest in cyber and related physical infrastructure will be positioned to lead by exploiting the resulting increased flow of information.

27 The underlying expansion in computing and sensing capabilities will, in turn, enhance the importance of semiconductors beyond today's computing and information technology sectors.

Advanced manufacturing processes will likely be more energy and resource efficient in the future, as companies strive to integrate sustainable manufacturing techniques into their business practices to reduce costs, to decrease supply-chain risks, and to enhance product appeal to some customers.

From a technological standpoint, advances in materials and systems design will likely accelerate and transform manufactured products. For example, large global vi investments in grapheme and carbon nanotubes for nanoscale applications have the potential to fundamentally change electronics and renewable-energy applications.

Further, self-assembly-based fabrication processes and biologically inspired designs will be integrated into the manufacturing process as technologies advance and cost- effective implementations are realized.

Establishing an advanced manufacturing sector will continue to be a priority for many countries, with progress depending importantly on trends in the private sector, such as the size and growth of the market.

In 20 years, many of the early trends and techniques that begin to emerge at 10 years are expected to be more fully adopted, with advanced manufacturing pushed toward new frontiers. Manufacturing innovations will have displaced many of today's traditional manufacturing processes, replacing labor-intensive manufacturing processes with automated processes that rely on sensors, robots, and condition-based systems to reduce the need for human interventions, while providing data and information for process oversight and improvement.

Advanced manufacturing will increasingly rely on new processes that enable flexibility, such as biologically inspired nanoscale-fabrication processes and faster additive manufacturing techniques capable of assembling products by area or by volume rather than by layering materials as is done today.

Over the next 20 years, manufacturers will also increasingly use advanced and custom-designed materials, developed using improved computational methods and accelerated experimental techniques. As computational capabilities increase, materials designs, processing, and product engineering will become more efficient, reducing the time from product concept to production In 20 years, synthetic biology could change the manufacturing of biological products. Coupled with advances in genomics, proteomics, systems biology, and genetic engineering, synthetic biology will offer a toolbox of standardized genetic parts that can be used in the design and production of a new system. The catalyst to new products will be increased understanding of cellular functions and disease models.

28 The report does not have specific policy-oriented recommendations. However, chapter 4 looks at the enabling factors need for success, including the policies of many nations to promote advanced manufacturing. The table below was taken from the report itself.

Table 3. Importance of location factors for location decisions from the perspective of all manufacturing companies.

Locational Driver Score, 1–10: Talent-driven innovation* 9.22 Cost of labor and materials 7.67 Energy costs 7.31 Economic, trade, financial, and tax systems* 7.26 Infrastructure quality* 7.15 Investment in manufacturing and innovation* 6.62 Legal and regulatory system* 6.48 Supplier network 5.91 Local business dynamics 4.01 Health care* 1.81

Source: Data from Deloitte Manufacturing Competitiveness Index (Deloitte Council on Competitiveness 2010).

* Factor is relatively movable through public policy, as opposed to broader market factors

As they point out in their conclusions: “Establishing an advanced manufacturing sector will continue to be a priority for many countries, with progress depending importantly on market factors. Companies will locate in countries that have large and growing markets. Country-specific policies that spur advanced manufacturing will set the stage for manufacturing sectors to emerge in both developed and developing countries. “

29 Gregory Tassey, “Beyond the Business Cycle: The Need for a Technology-Based Growth Strategy” (NIST working paper Feb. 2012), 3-8, (http://www.nist.gov/director/planning/upload/beyond-business-cycle.pdf)

In recent years, economic recessions have plagued the world and nations have scrambled to restore their economies. Tassey’s paper examines the reasons monetary and fiscal stimuli in the United States has only had a modest impact and proposes more structural solutions to bring the economy back to its former level. He argues that the economic stimulus of close to $800B imposed in the U.S. 2009-10 has not had as large an impact as intended as a result of structural problems in the economy, and that the only way to combat it is with higher rates of productivity growth accomplished from sustained investment in intellectual, physical, human, organizational, and technical infrastructure capital.

Tassey first outlines the limitations of the existing fiscal policies in establishing long- term economic growth. Policy analysts continue to argue for more of the same monetary and short-term fiscal stimulus, but, according to Tassey, the U.S. economy is not structurally sound enough to benefit from this strategy. The current policies include monetary policies and fiscal policies.

The Federal Reserve Board implemented monetary policies aim to induce consumers to spend, banks to lend, and businesses to invest by lowering interest rates dramatically, but the market did not respond as expected. Their next step involved “quantitative easing,” in which the Fed purchased long-term financial assets from private institutions with new, electronically-created money in order to expand money supply, lower long-term interest rates, inflate assets, and encourage increased consumption. However, as the economic slowdown wears on, the rates approach the risk premium and create a risk-adjusted rate of zero. Quantitative easing also flattens the yield curve, which eliminates the incentive for banks to lend. Stimulating demand in one sector while suppressing it in another, Tassey concludes, is counterproductive.

Though an investment component was included in the fiscal policies, the amount and composition was too small, short-term, and inadequate to sustain long-term economic growth (the R&D component of stimulus was only approximately $20M). One problem was that American business increased investments in other economies rather than domestically because global market opportunities have increased and other nations are now offering better incentives for R&D and commercialization than the U.S. government [according to a recent ITIF study, for example, the U.S. R&D tax credit is now only 27th in the world in terms of incentive value].

Some important factors for successful recovery are an increase in R&D levels that can be invested with the increase in national investment, and increased productivity and efficiency in economic assets as technology quickly accelerates the world’s economy. Tassey explains that these necessary structural changes are unlikely to

30 happen automatically because of the “installed wisdom,” illustrated above, where traditional neoclassical economists retain growth policies that are proving inadequate, and the “installed-base” effect, where owners of accumulated economic assets face high risk in writing off old assets and switching to new assets and therefore prefer to keep the viability of their assets by lobbying for relief from taxes and regulations. In order to successfully recover from the recession, policies should focus on addressing these structural problems of the U.S. economy.

The core structural problem that Tassey focuses on in his proposed model is the lack of investment in technology for long-term economic growth. As mentioned above, technology drives productivity, and in the competitive global economy, investment-driven recovery should focus its efforts on developing productivity- enhancing technologies. Tassey suggests this to be done through a new system involving public-private processes for developing and assimilating technology to increase productivity and ensure long-term economic growth.

This new model takes into account the evolution of technology from a tool developed and commercialized by large firms to a dynamically evolving asset developed by public-private partnerships and commercialized by both large and small firms. If economic growth is to be achieved, policymakers should work to increase the multifactor productivity, which requires investments in input factors such as technology, education, capital formation, and industry infrastructure. To improve technology, the U.S. needs to make a larger investment in R&D – the American Recovery and Reinvestment Act (ARRA) in 2009 provided $787 billion to stimulate the economy; however, as noted, less than 2% of this money was allocated to support scientific research, despite the history of American innovation being the main driver of economic growth. However, in addition to the amount of R&D invested, the composition and efficiency of R&D is critical to successfully compete in a global economy with shrinking R&D cycle times.

With such limited funds in the present day, investment in R&D has to be optimally allocated to maximize the impact of sparse funding. The composition of R&D investment, therefore, is an important consideration. Traditionally, the government has focused on mission-oriented research (national defense, health, and space exploration, etc.) rather than on economic growth, which has yielded technology that spins off into private industries for commercial application. However, the spin- off process is lengthy, and, in light of shorter technology life cycles, this approach to technology R&D is no longer competitive. Other countries have recognized and acted on this need to spur breakthrough technology research by funding universities, research organizations, and private industries in developing new technology platforms and industries.

To address the efficiency of R&D investment, Tassey’s proposal utilizes more players in the technology field. He predicts a high rate of success in economic growth through joint efforts between government and industry (both small and large firms) to cooperate in supply, development, and deployment. The organizational format,

31 termed the “regional innovation cluster,” directs technology-based economic growth through regional co-location of public and private R&D assets. Clusters would increase productivity in R&D, allow for risk pooling and co-funding, and facilitate effective management of intellectual property.

Manufacturing industries in particular can play a major role in directing long-term economic growth in a technologically advanced economy. The manufacturing sector is responsible for a 67% share of domestic industry R&D and 57% employment of R&D personnel. However, the intensity of U.S. investment in R&D (R&D as a percent of GDP), and hence growth rate in R&D, is drastically lower than other countries, as can be seen below.

If U.S. manufacturing moves overseas, the nation’s R&D capacity will be crippled, along with its economy, innovation, and potential to recover economically. To improve the economy, the focus should be on innovative research to develop manufacturing processes that can make quality products that are cost-competitive in the global marketplace. One of the challenges with these manufacturing technologies now is the change in focus from mass-producing homogenous products to a wider scope of semi-customized products that can serve a variety of submarkets – for example alternative energy technologies are looking for the capability to convert waste and cellulosic feedstock into a different types of fuels and chemicals. The same manufacturing process has to be able to produce different products that still fit the relevant standards.

To take advantage of technology, Tassey recommends investing in research and development by providing a competitive R&D tax incentive, ensuring an adequate supply of skilled R&D workers in the technology fields, and implementing a new public-private research infrastructure via regional technology-based clusters. If the

32 U.S. wants to rescue its economy and continue being a world leader, investment in technology R&D needs to increase.

(Source: Queenie Chan, MIT ’13)

33 Houseman, Susan, Christopher Kurz, Paul Lengermann, and Benjamin Mandel, "Offshoring and the State of American Manufacturing." Upjohn Institute Working Paper No. 10-166 (Kalamazoo, MI: W.E. Upjohn Institute, June 2010). ( http://research.upjohn.org/up_workingpapers/166 )

Houseman and colleagues Kurz, Lengermann and Mandel examine the effects of offshoring on the manufacturing industry and provide a bias correction for an output assumption they find to be misreported. Their correction affects statistics in input cost and import price indexes, which are affected by moving from more expensive domestic suppliers to low-cost foreign suppliers. They find that the growth in the U.S. manufacturing output from 1997-07 is overstated, specifically that when bias from offshoring is factored in, the official output data overstates a fifth to half of the growth in the non-computer/electronic manufacturing industry.

The emerging trend of offshoring has led to trade deficits, where the cost of imports to make the product exceeds the value from exporting the good. It has also raised questions about the impact of offshoring on manufacturing. From 1997 to 2007, the U.S. manufacturing sector lost more than 20 percent of its employment, spurring discussions as to whether or not this arose as a result of offshoring.

Unlike other studies, this paper distinguishes between imported and domestic material inputs in its analyses, which makes a major difference in assessing output . They found that the contribution from imported materials was the largest percentage out of all the inputs, and that it comes to more than twice the contribution from capital. They also found a negative contribution from domestic materials and labor.

An interesting trend in the manufacturing industry, that many experts have explained by assuming high productivity growth, is the disparity between employment and output. As employment steeply declined in the past decade, the outputs of the manufacturing industry appeared to be strong, leading to an assumption of high productivity gains. Houseman, et al, posit that this perspective is incorrect when the output data is re-evaluated.

One of the reasons they evaluate is the apparent massive growth seen in one sector of manufacturing, the computer and electronic products industry. Computers and electronics accounted for about 90 percent of manufacturing value added, and when taken out of the calculation of average annual growth rate, this rate dropped to less than a third of the published growth rate for all manufacturing. The aggregate manufacturing production output numbers, then, are not indicative of the entire field of manufacturing, but rather highly skewed by the results for the computer and electronics industry.

The second reason for the disparity between employment and production is that the price indexes do not capture the manufacturer’s lower cost when shifting from

34 domestic suppliers to lower-cost foreign suppliers. U.S. producers and importers cannot report the price drops that buyers experience when shifting their purchases from domestic to foreign suppliers, but if price indexes did reflect these drops, one would find that import prices increase more slowly than domestic prices.

The bias to value added from offshoring results from Houseman, et al’s, finding that the differences in the price deflators for imported and domestic semiconductors were not incorporated in the output data. The price for imported semiconductors fell less rapidly than the domestic counterparts, and, after adjusting for offshoring, the multifactor productivity growth is 0.1 to 0.2 percentage points lower and the average annual productivity growth is reduced to between 6 and 14 percent.

The findings from this study bring to light flaws in previous evaluations of growth in the manufacturing industry. The reduction in input cost for manufacturing does not, in fact, result from greater efficiency and productivity, but rather from loss of jobs via offshoring. Growth of imports has been understated, and consequently productivity gains based on import growth statistics have also been misstated. The U.S. manufacturing industry is not nearly as well off as previous studies have indicated, and as offshoring becomes more common, new economic models that incorporate the effect of low-cost imports on output and the economy are needed.

(Source: Queenie Chan, MIT ’13)

35 Jonas Nahm and Edward S. Steinfeld, Scale-Up Nation: Chinese Specialization in Innovative Manufacturing (MIT working paper March 12, 2012)(working draft of research paper available through MIT Production in the Innovation Economy study)

In this paper, Nahm and Steinfeld examine what makes China so successful in the manufacturing industry. China went from 5.7% of the global manufacturing output in 2000 to an impressive 19.8% in 2011, the highest in the world. While many attribute this extraordinary growth to the low cost of production in China (with cheap labor and cheap parts), Nahm and Steinfeld assess the importance of innovation in this growth as well.

The many theories behind why global manufacturing concentrates in China have two underlying themes: (1) that manufacturing naturally migrates to the lowest cost environment, and (2) that the knowledge required for manufacturing is trivial. One common opinion is that China has developed product know-how because of its strong position within manufacturing as a location for outsourcing, and that knowledge flows unidirectionally from outside into China to support related innovation. A second opinion is that the information technology revolution allowed the process of manufacturing to separate from the innovation processes of R&D, product definition, design, branding, and marketing. Neither of these link innovation and manufacturing, however, which Nahm and Steinfeld argue is the key factor to China’s rapid advancement in manufacturing.

“Innovative manufacturing” takes into account the possibility of proprietary know- how and specialization (innovation) being embedded in the fabrication and assembly process itself (manufacturing). China’s particular form of innovative manufacturing specializes in rapid scale-up and cost reduction, with globally unparalleled skills in simultaneous management of tempo, production volume, and cost. Consequently, production is able to scale up quickly and with drastic reductions in unit cost. This has enabled the nation to expand even in industries that are highly automated or not on governmental priority lists, despite virtually no labor cost advantage or government subsidies, respectively. Nahm and Steinfeld take these unexpected growth areas to show that costs and government support are not sufficient to explain China’s success in manufacturing.

36 Chinese firms have acquired unique skills for marching down and redefining cost curves, as seen in the graph above. They also have managed to further develop production processes that were previously considered fully mature and impervious to further cost reductions or technological improvements. Nahm and Steinfeld attribute this to the accumulation of firm-specific expertise in manufacturing via extensive, multidirectional inter-firm learning in an international dimension.

The scale-up effect of Chinese manufacturing can be examined through the wind turbine sector, the solar photovoltaics (PV) sector, and the consumer electronics sectors, which vary across several dimensions. Wind turbine manufacturing has extensive government support and a large domestic market, and crystalline silicon solar PV panel production had no domestic market. In both, however, China excelled and drove costs down – wind turbines by producing in China and selling to the domestic market, and solar PVs by exporting to countries with high demand, lowering solar PV module prices from $2.75/watt in 2009 to $1.10/watt in 2012. Another sector that illustrates the uniqueness of Chinese manufacturing is consumer electronics fabrication and assembly. Multinational corporations like Foxconn, Quanta, and Delta handle all fabrication and assembly in their China-based factories and have been found able to scale-up rapidly, accommodate late-stage design changes, and take on additional design responsibilities while still driving down prices.

Chinese firms’ exhibit different patterns of behavior associated with the knowledge- intensive scale-up model, including:

1. Backward design

37 Chinese firms find a huge cost advantage in their system of backward design. They take existing products and create alternatives that may be more simple, with cheaper materials, and easier to manufacture, which make them easier to scale at low cost and higher speed. Here, the cost curve drives product selection even if quality and performance are sacrificed. The process can be either in collaboration with other firms to develop the most cost-effective model, or in direct competition with another firm’s product archetype.

Even though foreign firms have attempted to replicate this strategy of cost- driven design, the speed of Chinese firms’ process of backward design gives them an edge in competitive markets. In one case, a European turbine firm ran into issues with lengthy negotiation and approval processes involving its headquarters, and by the time they were ready to sell their product, the Chinese market had already moved on to larger turbine sizes.

2. Foreign design and Chinese manufacturing: Partnership Some foreign companies have realized the power Chinese firms have in manufacturing and have partnered to use this to their advantage. With the foreign firm providing the design and the Chinese firm figuring out how to make it commercially viable through cost effective manufacturing, the two firms together can surge ahead in the market. This type of partnership is an example of multidirectional learning. While foreign firms provide the design concept, Chinese firms provide their vast expertise in replacing, redesigning, and substituting parts for reducing the cost of manufacturing the product.

In a real case with a European engineering firm’s turbine design concept, both sides acknowledged the learning benefits from this type of partnership. The European firm had no manufacturing capacity and involvement in this cooperation helped them maintain competitiveness and innovation capacity. The Chinese firm gained a commercial advantage in a highly competitive market environment.

3. Rapidly scaled product innovation Chinese firms use their understanding of scaled-up manufacturing to commercialize their own new products by being able to see commercial potential in products that have been discarded because they were deemed to costly or risky to develop. Here, the product innovation has already taken place and been thrown away, but these Chinese firms pick it up and bring it to life with their ability to tweak and use existing production lines to rapidly scale the product with modified materials.

4. Technology Absorption and Collaborative Development Another business pattern Nahm and Steinfeld observed with Chinese companies involves the Chinese firm producing a product that is incorporated as a component of an international innovator’s technology. This type of cooperation goes beyond a simple commercial transaction to a process of co-development of

38 the technology. Chinese firms’ involvement in products that can be incorporated leads to a wide market; for example, a Chinese firm’s liquid nanomaterial can be used in flat panel displays, solar panels, or LED lighting, and offering the nanomaterial as a part for integration into these large-scale products provides an instant market.

This, too, is an example of multidirectional learning, where both parties bring knowledge to the table. However, in this business model, the Chinese product platform determines the features and markets of these new technologies, rather than the foreign firm providing the design.

Nahm and Steinfeld’s findings indicate that the success of manufacturing in China is not just a model of the global best practice but a redefinition of the global standard. Also, learning may not be, as previously believed, a result of an oligopolistic environment but rather driven by intense competition between many companies. A large number of international commercial partnerships and knowledge flows also contributed largely to China’s learning process. Nahm and Steinfeld illustrate that learning is centered around the creativity of entrepreneurs and multidirectional flows of knowledge across linked, cross-border networks rather than on political hierarchies.

The Chinese place at the top of the global manufacturing charts indicate that the U.S. should pay attention to their method for success. Nahm and Steinfeld’s research points to the importance of multidirectional learning and Chinese firms’ talent for innovative manufacturing. Some foreign firms have already benefited and learned from the Chinese approach of prioritizing speed and flexibility over fixed corporate rules and procedures. The paper suggests that global firms will have to either form partnerships with Chinese companies or learn how to mimic their scale-up know- how to successfully compete in commercializing future technology.

(Source: Queenie Chan, MIT ‘13)

39 U.S. Department of Commerce, Economics and Statistics Administration, The Benefits of Manufacturing Jobs (May 9, 2012) http://www.esa.doc.gov/Reports/benefits-manufacturing-jobs

The U.S. Commerce Department’s Economics and Statistics Administration (ESA) has released a new report, “The Benefits of Manufacturing Jobs,” an analysis of wages and benefits of manufacturing workers, which finds that total hourly compensation for manufacturing workers is 17 percent higher than for non-manufacturing workers. This includes premiums in both wages and employer-provided benefits, such as health insurance and retirement plans.

The report finds that in addition to higher compensation for manufacturing jobs, the share of manufacturing workers with more than a high school degree has been steadily increasing, and now more than half of all manufacturing workers have at least some college education. Further, manufacturing jobs are more STEM (science, technology, engineering, and math) intensive than non-manufacturing industries. According to the Bureau of Labor Statistics, manufacturing employment has expanded by nearly 500,000 jobs or 4 percent since January 2010 — the strongest cyclical rebound since the wake of the dual recessions in the early 1980s.

The report, then indicates manufacturing employment means higher wages and important benefits.

Specific findings from “The Benefits of Manufacturing Jobs” include:

• On average, hourly wages and salaries for manufacturing jobs are $29.75 an hour compared to $27.47 an hour for non-manufacturing jobs. Total hourly compensation, which includes employer-provided benefits, is $38.27 for workers in manufacturing jobs and $32.84 for workers in non-manufacturing jobs, a 17 percent premium. • Even after controlling for demographic, geographic, and job characteristics, manufacturing jobs maintained significant wage and benefit premiums. • The educational attainment of the manufacturing workforce is rising steadily. In 2011, 53 percent of all manufacturing workers had at least some college education, up from 43 percent in 1994. • The innovative manufacturing sector relies more heavily on STEM education than non-manufacturing. For instance, nearly 1 out of 3 (32 percent) college- educated manufacturing workers has a STEM job, compared to 10 percent in non-manufacturing. • Higher educational attainment for manufacturing workers carries higher premiums and the size of the premium, including or excluding benefits, increases consistently with educational attainment. • Furthermore, the compensation premium has risen over the past decade across

40 all levels of educational attainment.

Note: In April, the Commerce Department released “Intellectual Property and the U.S. Economy: Industries in Focus,” a comprehensive report co-produced by ESA and the U.S. Patent and Trademark Office (USPTO) which found that IP-intensive industries support at least 40 million jobs and contribute more than $5 trillion dollars to U.S. gross domestic product (GDP).

(Source: ESA webite)

41 Advanced Manufacturing Partnership Steering Committee (for PCAST), Capturing Domestic Competitive Advantage in Advanced Manufacturing (July 17, 2012) ( http://1.usa.gov/PkRHqi )

On July 17th, the President’s Council of Advisors on Science and Technology (PCAST) released a report to the President for revitalizing the nation’s advanced manufacturing sector. The report was prepared and approved by the PCAST Advanced Manufacturing Partnership (AMP) Steering Committee chaired by Susan Hockfield, former president of MIT, and Andrew Liveris, chairman, president and CEO of The Dow Chemical Company. Entitled Capturing Domestic Competitive Advantage in Advanced Manufacturing, the report identifies opportunities for investments in advanced manufacturing that have the potential to transform U.S. industry.

More than 1,200 stakeholders representing industry, academia, and government at all levels participated in four regional meetings across the nation. A diverse set of experts in advanced manufacturing technology, education, and policy issues were also consulted to build upon the ideas presented by the stakeholders. One of the regional meetings was held at MIT on November 28th; video of that event can be found at: http://web.mit.edu/manufacturing/amp/event/. Others were held at Georgia Tech, Berkeley, and the University of Michigan. See meetings summary at: http://www.whitehouse.gov/sites/default/files/microsites/ostp/amp_final_report _annex_6_amp_regional_meeting_summaries_july_update.pdf

The Advanced Manufacturing Partnership Steering Committee proposes that the U.S. establish a national advanced manufacturing strategy. This strategy will serve as a national framework that, when implemented by states and local communities, will aim to bring about a sustainable resurgence in advanced manufacturing in the United States. The AMP Steering Committee developed a set of 16 recommendations around three key pillars: · Enabling innovation · Securing the talent pipeline · Improving the business climate These recommendations aim at reinventing manufacturing in a way that ensures U.S. competitiveness, feeds into the nation’s innovation economy, and invigorates the domestic manufacturing base. The objective is to position the nation to lead the world in new disruptive advanced manufacturing technologies that are changing the face of manufacturing. The report identifies, based on industry and academic surveys, 11 such technology areas that appear especially promising for implementation. The AMP Steering Committee report asserts that a number of important steps taken now will be critical to strengthen the nation’s innovation system for advanced

42 manufacturing. While some of the largest U.S. firms have the depth and resources to be ready for this challenge, a significant number of small and medium-sized U.S. firms operate largely outside the present innovation system. AMP found that the U.S. will only lead in advanced manufacturing if all companies are able to participate in the transformations made possible through innovations in manufacturing. When implemented, these recommendations will set the stage for advanced manufacturing to thrive in the United States. The 16 recommendations are summarized below: Enabling Innovation · Establish a National Advanced Manufacturing Strategy: Create and maintain a national advanced manufacturing strategy by putting in place a systematic process to identify and prioritize critical cross-cutting technologies. · Increase R&D Funding in Top Cross-Cutting Technologies: In addition to identifying a “starter list” of cross-cutting technologies that are vital to advanced manufacturing, establish a process for evaluating technologies for research and development (R&D) funding. · Establish a National Network of Manufacturing Innovation Institutes (MIIs): Create a network of MIIs as public-private partnerships to foster regional ecosystems in advanced manufacturing technologies. MIIs are one vehicle to integrate many of the Committee’s recommendations. · Empower Enhanced Industry/University Collaboration in Advanced Manufacturing Research: Change the treatment of tax-free, bond-funded facilities at universities to enable greater and stronger interactions between universities and industry. · Foster a More Robust Environment for Commercialization of Advanced Manufacturing Technologies: Connect manufacturers to university innovation ecosystems and create a continuum of capital access from start-up to scale-up. · Establish a National Advanced Manufacturing Portal: Create a searchable database of manufacturing resources as a key mechanism to support access by small and medium-sized enterprises to enabling infrastructure.

Securing the Talent Pipeline · Correct Public Misconceptions About Manufacturing: Create and maintain a national advertising campaign focused on parents and students to build excitement and interest in careers in manufacturing. · Tap the Talent Pool of Returning Veterans: Connect returning veterans who possess many of the key skills needed to fill the manufacturing skills gap to the manufacturing talent pipeline. · Invest in Community College Level Education: Increase investment in community and technical colleges to help address manufacturers’ skill needs, following the best practices of leading

43 innovators. · Develop Partnerships to Provide Skills Certifications and Accreditation: Establish stackable credentials to allow coordinated action by organizations that feed the advanced manufacturing talent pipeline, taking advantage of the portability and modularity of the credentialing process. · Enhance Advanced Manufacturing University Programs: Challenge universities to bring new focus to advanced manufacturing through the development of educational modules and courses. · Launch National Manufacturing Fellowships & Internships: Create national fellowships and internships in advanced manufacturing in order to provide needed resources and national recognition on manufacturing career opportunities.

Improving the Business Climate · Enact Tax Reform: Enact specific tax reforms that can “level the playing field” for domestic manufacturers. · Streamline Regulatory Policy: Create a framework for smarter regulations relating to advanced manufacturing. · Improve Trade Policy: Initiate specific actions that will to improve the nation’s trade policies. · Update Energy Policy: Establish updated energy policies that address the needs of U.S. manufacturers.