TALKING POINTS FOR FOREIGN INVESTMENT NAVTEQ –Analysis of Automobile Electronics Industry

A. Investment Advantages

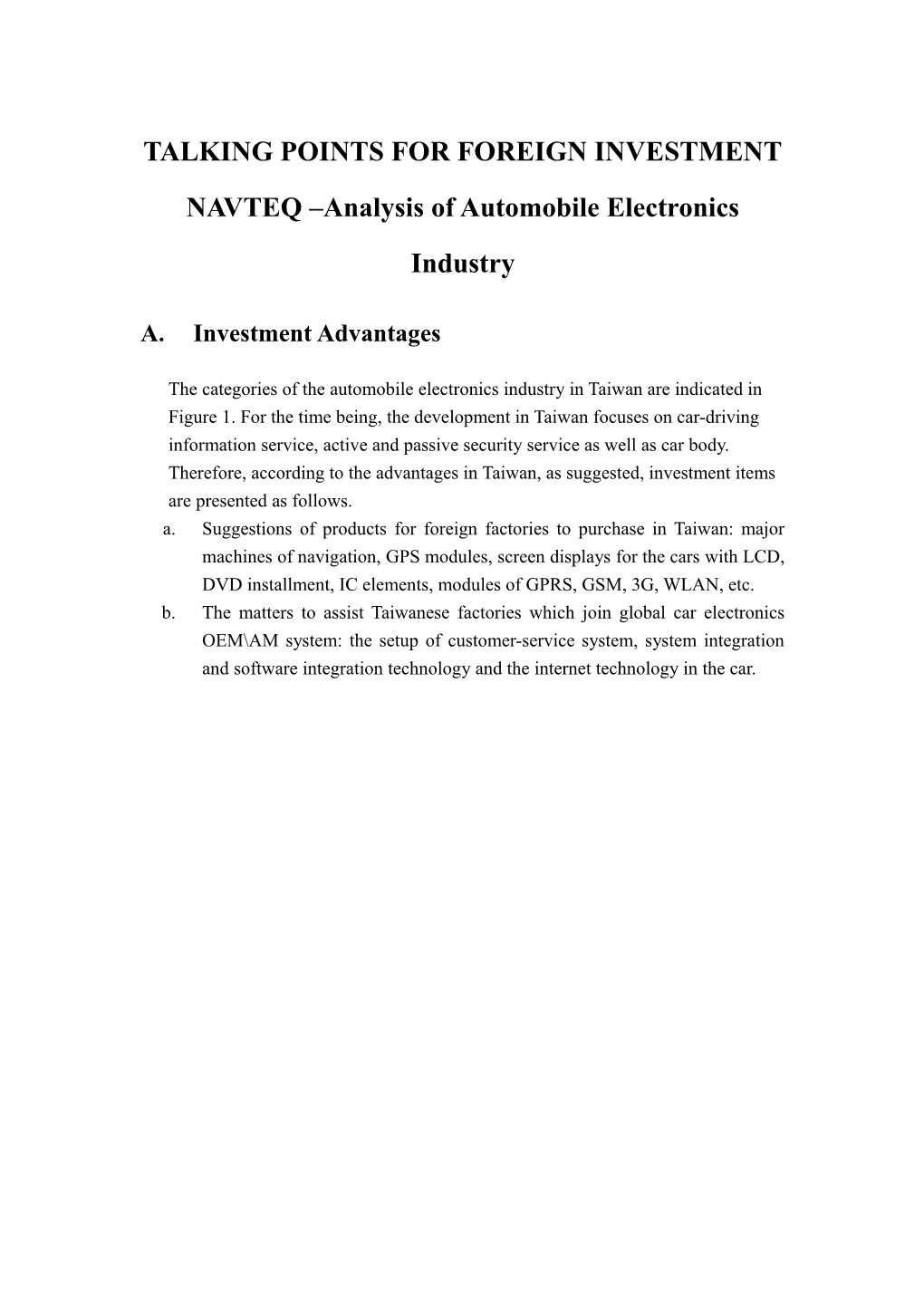

The categories of the automobile electronics industry in Taiwan are indicated in Figure 1. For the time being, the development in Taiwan focuses on car-driving information service, active and passive security service as well as car body. Therefore, according to the advantages in Taiwan, as suggested, investment items are presented as follows. a. Suggestions of products for foreign factories to purchase in Taiwan: major machines of navigation, GPS modules, screen displays for the cars with LCD, DVD installment, IC elements, modules of GPRS, GSM, 3G, WLAN, etc. b. The matters to assist Taiwanese factories which join global car electronics OEM\AM system: the setup of customer-service system, system integration and software integration technology and the internet technology in the car. chassis/ Car body system Engine/ power

suspensio Wir e-t r ansmit Lane-maintenanc Ventilating and Geared Mobile t i ng dr i vi ng stabilityn Car-driving control contTr ace r ol-t r ac e installment air-cleaning speed-changing Parking-assisting Non-gear ki ng Automatic driving Digital-control Fuel display installment control AT/MT Adj ust abl e contelectronic r ol -control suspension speed-changing control installment Transmission control ant i -bumpi ng installment ejectionDigital igniting Mixed sensor system Digital dashboard institution CVT i nst i t ut i on X-by-wireCentralized -powe Temperature and Changeable valve El ect r oni c-con Braking LED car light r controlAdjustably fixed t r ol dr i vi ng air-conditioning controlElectric -control i nst al l ment anti-lock intelligent door HID car light speed navigation control purge Intelligent airbag Automobile institutionBattery management remote control control ACC Co-exit electric and Image identification Driving recorder Finger-print Electronics Header display HUD Driving navigation machine magnetic EMC Pro-adjustability lighting Motor driving Personal-act identification GPS Power control installment PDA Car-driving audio Language system AFS Distance-inspecting radar Changingcontrol frequency control Electric anti-bumping sensor Car semi-conductor entertainment installment identification GP Tire-pressure Micro processor Integrated IC SOC night-driving inspector distribution control Automatic review Large electric current Human-machine light-saving CommunicationMCU,CPU agreement Millimeter wave radar No-key entrance viewer system power lements Image sensor CCD Car-installed installment digital HDD- charging Regional control network Power intermediateS HMI device installment switcher CMOS (car-driving LAN) Electric Electronics active / passive security Car-driving information service 一、 S service

Resource: Electricity Engineering Division of ITRI (Industrial Technology Research Institute) (2005/10) Figure 2: The diagram of automobile electronics industry in Taiwan B. Analysis of Market Status Quo and Size

According to the statistics of SRD Japan Inc., the sales amount of car-driving navigation system of 2003 in Taiwan was 9,2220 sets. Among them, the sales amount of after-sales market reached 76%. Estimated, the future major market of car-driving navigation system will be still after-sales market. Until 2008, the total sale amount of car-driving navigation system will be 17,990 sets. Annual multiple growth rate will be 14.3%. The share of after-sales market will reduce to 67% as detailed in Figure 3.

20,000

15,000

套 set 10,000

5,000

0 2003 2004 2005 2006 2007 2008

售後市場after-sales 7,000 7,500 9,000 10,000 11,000 12,000 market 原廠安裝Installment of the 2,220 2,230 2,940 3,850 4,770 5,990 original factory

Resource:SRD Japan Inc.; IEK-ITIS project of ITRI (2004/12) Figure 3: The market forecast of car-driving navigation system in Taiwan

C. Analysis of Competition and Cooperation

In the aspect of the revenue of each leading automobile electronics factories, Delphi and Bosch, the international large-size factories, still gets the most. And the domestic factories such as USI (Universal Scientific Industry Co., Ltd.), Mobiltron Electronics Co. Ltd., TYC and so on have a rather small size; however, they still have much room to develop. 營收:百萬美元 Revenue: One Million of US Dollars 35,000

30,000 Delphi 27,427 25,000 Bosch 21,927 20,000 Visteon 18,395

15,000 Siemens VDO 10,000 Valeo 9,803

5,000 8,353

環隆、車王、提維西 The total 員工人數:人amount of employees - USI (Universal Scientific Industry Co., Ltd.), -50,000 - 50,000 100,000 150,000 200,000 250,000 300,000 -5,000

Resource: financial statement of each company; the project of IEK-ITIS of Industrial Technology and Research Institute (2003/09) Figure 4: The Comparison of global leading automobile electronics factories

Car-driving Display 導航系統 TelematicsTelematics Navigation System 車用顯示裝置

環隆電氣 台灣松下 Installmen憶聲電子t Universal Scientific Panasonic 後視鏡 怡利電子 怡利電子 Action Electronics台灣松下 Technology Rear Mirrors E-lead Electronics Co., 建生 Industry Co., Ltd. 航欣科技 Security安全氣囊 Air Bag 宏碁集團 友達光電 Jiansheng Co., Letd. 車王電子 Ltd. 台灣電綜 美安 E-Lead行毅科技 Electronics 統寶光電 Mei An Mobiletron Electronics Panasonic 全興科技 公信電子 Hamg Shing博特科技 Industry 元太科技 Co., Ltd. Cyuan Sing Technology Co., Ltd. 航欣科技 天下航太 AUO 奇美電子 ACER Denso Corp. Inc. Radar for driving 伯碩科技 Toppoly Optoelectronics Corp. 倒車雷達 Sienyih Technology Protech Link 六和科技 車王電子backward Prime View International Co., Co., Ltd.康訊科技 Technology Inc. 同致電子 Mobiletron 機械所 LTD, PVI Chi Mei BCOM TeamSharp SpaceTech Electronics Co., Ltd. Optotelectronics Hamg Shing Industry Inc. Tung Thih Enterprise Headed抬頭顯示 display Advanced先進照明ProSense Co. lighting 產 品 器 指紋辨識系統 Co., Ltd. Tung Thih Enterprise Fingerprint 胎壓監測系統 大億燈具 車內影音IC Tire-pressure Supervising productsLiouho Technology 同致電子 徽昌電子 Visual and audio IC in identification system 環隆電氣 堤維西 Co., Ltd. 普誠IC 維嘉科技 System Tayih帝寶工業Co. Light Inc. the car 敦陽科技 Whetron Electronics Co., Wei聯城工業 Jia Technology Universal Scientific Industry Co., TYCSystem DEPO and Auto Parts Ind. Princeton IC 橘的電子 Ltd. Inc. Ltd. Technology Corp. Figure 5: The Automobile Electronics Products in Taiwan IV. Production Cost

A、Land rent Cost a. Rents at the Hsinchu Science-based Industrial Park

Table 4 Land rent at the Hsinchu Science-based Industrial Park

Unit: NT$ Category Area (m2) Rent (per month) Land Over 2,000 NT$ 49/ m2 Standard First floor 531.3~1280.4 NT$ 122/ m2 plant Second floor 531.3~1227.6 NT$ 115/ m2 Third floor 662.97~1346.4 NT$ 106/ m2 Fourth floor 662.97~798.6 NT$ 99/ m2 Deluxe plant 1485 NT$ 204~325/ m2 Incubation center 80 NT$ 184/ m2 160 240 Dormitories Single room 15~18 NT$2,250~2,950/unit Double room 15~21 NT$1,850~3,300/unit Family home 100~290 NT$10,550~33,300/unit Note: The above rents are adjusted on the basis of announced rents for the current year.

b. Rents in the Tainan Science-based Industrial Park Land and plant buildings within the Tainan Science-based Industrial Park are leased, and will not be sold. The government will set and adjust rents on the basis of amortized cost at the time of development and subsequent yearly changes in real estate and land value taxes. Rents within the Tainan Science-based Industrial Park will consequently be lower than those outside the park. Land shall be leased for periods of 20 years, and plants leased for periods of one year. The following rents are currently charged: Units: NT$ Category Term Rent (m2/month) Land 20 years 12.9 Plants 1 year 103~120 Note: Land rents will be adjusted on the basis of announced land prices, public facility development costs, and laws and regulations. B、 Labor Cost Table 5 Average monthly wages for workers in different industries in Taiwan

Unit: NT$ Year Ave. 2001 Ave. 2002 Ave. 2003 Mining and quarrying 44,264 45,006 47,263 Manufacturing 38,586 38,565 39,583 Electricity, gas & water 93,091 89,591 91,034 Construction 37,746 36,848 37,219 Trade 39,760 39,202 39,799 Accommodation & eating-drinking places 25,991 25,828 25,181 Transportation, storage & communication 53,350 51,564 51,396 Finance & insurance 62,625 65,767 64,693 Real estate& rental & leasing 42,604 40,714 39,872 Professional, scientific & technical services 53,191 49,587 50,990 Health care services 54,701 54,115 55,999 Cultural,, sporting & recreational services 41,242 39,489 40,861 Other servies 31,157 30,525 30,057 Source: Monthly Bulletin of Earnings and Productivity Statistics and Annual Report of Earnings and Productivity Statistics published by the Directorate-General of Budget, Accounting and Statistics, Executive Yuan, Jan. 2004

V. Taxation

Table 6 Individual Consolidated Income Tax Rates

Units: NT$ Net consolidated income Tax rate Progressive Tax payable differential 0—370,000 x 6﹪ – 0 = 370,001—990,000 x 13﹪ – 25,900 = 990,001—1,980,000 x 21﹪ – 105,100 = 1,980,001—3,720,000 x 30﹪ – 283,300 = 3,270,001–– x 40﹪ – 655,300 = Table 7 Profit–Seeking Enterprise Income Tax Rates

Taxable income (P) Tax rate Progressive Quick formula bracket differential Less than NT$50,000 0 – Less than NT$100,000 15% None 1. When P is less than NT$71,428: T= (P–50,000x1/2 2. When P is greater than NT$71,428: T=Px0.15 Over NT$100,000 25% 10,000 T=Px0.25–NT$10,000 Note: T is the amount of tax.

VI. Investment Incentives

A、Preferential Taxes

The ROC Government enacted the Statute for Upgrading Industries in 1991 to develop a favorable environment for foreign and overseas Chinese investors in Taiwan and to encourage investment by foreign companies for the purpose of upgrading the ROC’s industrial base. On January 1, 2000, the statute was amended to extend preferential tax measures for another 10 years until December 31, 2009. These measures are detailed in the chart below:

Incentive Measure Nature of Incentive Accelerated Equipment and facilities used exclusively for R&D, experimentation, and quality depreciation of control purposes, and equipment, machinery, and facilities that are utilized for equipment and energy conservation or that use new and clean energy, are eligible for an facilities accelerated depreciation period of two years. If there is any residual post- depreciation service life remaining following the accelerated depreciation period, depreciation may be continued for one or several years within the service life of the assets as specified in the Income Tax Law until the assets are fully depreciated. Investment in Companies may deduct 5% to 20% of the amount of investment in these areas automation from their profit-seeking-enterprise income tax over a five-year period beginning equipment or with the year in which the investment is incurred. technology Investment in recycling and pollution control equipment or technology Investment in equipment or Incentive Measure Nature of Incentive technology for the use of new and clean energy, energy conservation, and industrial wastewater recycling Investment in equipment or technology for reducing greenhouse gas emissions and enhancing energy efficiency Investment in the hardware, software and/or technology that can promote an enterprise’s digital information efficiency, such as the Internet and television functions, enterprise resource planning, communication and telecommunication products, electronics and/or audio visual equipment, and digital content production Research and Companies may deduct 35% of the amount of their investment in R&D or development personnel training from their profit-seeking-enterprise income tax over a Personnel training five-year period beginning with the year in which the investment is incurred. Companies may deduct 50% of the amount of their investment in R&D or personnel training that exceeds the average annual amount of their investment in R&D or personnel training for the previous two years from their profit-seeking-enterprise income tax. Incentive Measure Nature of Incentive The total amount deducted from tax due per year under the previous two items may not exceed 50% of the company's profit-seeking-enterprise income tax due for that year. The amount deducted during the final year, however, is not subject to this limitation. Investment in Companies that invest a specific amount or employ a specific additional number resource-poor or of persons in resource-poor or lesser-developed rural areas may deduct 20% of lesser-developed the invested amount from their profit-seeking-enterprise income tax over a five- rural areas year period beginning with the current year. Investment in The investor may choose one of the following: emerging, Investment tax credits for shareholders: important, and A company or individual who subscribes to the registered stock issued by a strategic industries company in an emerging, important, or strategic industry, and who holds the stock for at least three years, may claim a deduction from the profit-seeking- enterprise income tax or consolidated income tax due over a period of five years beginning with the current year: A profit-seeking enterprise may deduct up to 20% of the cost of such stock from its profit-seeking-enterprise income tax for the current year. An individual may deduct up to 10% of the cost of such stock from the consolidated income tax for the current year, provided that the deductible amount within each year is not more than 50% of the consolidated income tax payable for that year; this limitation will not apply, however, to the amount deducted in the final year. The rate of tax reduction provided above will be reduced by 1 percentage point every two years beginning on Jan. 1, 2000. Five-year tax holiday for companies: A company investing in an important, emerging, or strategic industry may, within two years from the date at which shareholders begin paying their stock price and with the approval of its shareholders’ meeting, select exemption from the profit-seeking-enterprise income tax and waive the right of shareholders to claim income tax deductions as set forth above. Once the selection is made, no change will be allowed. The following provisions must be met: A newly incorporated company that meets these conditions will be exempted from the profit-seeking-enterprise income tax for a period of five consecutive years from the date on which it begins to sell its products or render its services. A company that carries out an expansion project via a capital increase will be exempted from the profit-seeking-enterprise income tax on the increased income derived from the expansion for a period of five consecutive years from the date the newly added equipment begins to operate or the rendering of services begins. However, this provision is limited to the expanded construction of independent production or service units, or the expansion of primary production or service equipment, via Incentive Measure Nature of Incentive capital increase. A company that is eligible for a tax exemption as described above may, within two years of the date on which it starts to sell its products or render its services, choose to defer the commencement of the tax-exemption period. The period of deferment may not be more than four years, and the date on which the exemption period begins following deferment must be the first day of a fiscal year. A company that carries out a capital increase using undistributed profits may apply the three items above. Reinvestment If for the purpose of adjusting its business operations, a company invests production or service equipment and the land on which such equipment is located in a another enterprise in which it holds at least a 40% share, the land value increment tax on the reinvested land may, with prior government approval, be deferred based on the ratio of shares held and upon receipt of a proper guarantee from the company. Investment by When a non-resident individual or profit-seeking enterprise without a fixed foreigners and place of business in the Republic of China receives a dividend distributed by overseas Chinese a company or profit distributed by a partnership located in the Republic of China in which that individual or enterprise has invested under the Statute for Investment by Overseas Chinese or Statute for Investment by Foreign Nationals, 20% of the amount of payment will be withheld as stipulated in the Income Tax Law and the provisions of the Income Tax Law regarding tax filing will not apply. When a non-resident director, supervisor, or manager of a company in the ROC who has invested in that companies under the Statute for Investment by Overseas Chinese or Statute for Investment by Foreign Nationals and who has resided in the ROC for more than 183 days within a tax year for the purpose of operating or managing the invested company receives a dividend from the invested company, 20% of the amount received will be withheld as stipulated in the Income Tax Law and the dividend income will not be included in the individual’s tax return for that year. Salaries paid abroad to directors, managers, or technicians who are sent to the ROC temporarily by foreign profit-seeking enterprises that invest in the ROC under the Statute for Investment by Overseas Chinese or the Statute for Investment by Foreign Nationals to carry out investment, plant construction, or market surveys, and who do not stay in the ROC more than 183 days within a tax year, are not treated as income derived in the ROC and are thus exempt from the income tax. Establishment of When foreign profit-seeking enterprises or branch companies which they have international established within the Republic of China set up themselves, or commission logistics and domestic profit-seeking enterprises to set up logistics and distribution centers in distribution centers Taiwan to engage in the warehousing and simple processing of goods from the said foreign profit-seeking enterprise which are then delivered to domestic Incentive Measure Nature of Incentive customers, the income so derived is exempt from the profit-seeking-enterprise income tax. Company mergers Merged companies are exempt from profit-seeking-enterprise income taxes and securities transaction taxes resulting from their merger, and may apply the provisions for the deduction of losses. In addition, the land increment tax due on land that is owned by a company and is transferred along with the merger of that company may be charged to the account of the surviving enterprise. Establishment of For companies that establish operations headquarters in Taiwan that reach a operations certain scale and that have a major economic effect, the income that they derive headquarters from the provision of management services or research and development to the related companies which they acquire in Taiwan, as well as royalty income, profit from investment, and gain from the disposition of properties, are exempt from the profit-seeking-enterprise income tax; in addition, such companies may procure publicly owned land at preferential prices. Science-based Effective Jan. 1, 2002, machinery and equipment that is imported for a industries company's own use and that is not yet manufactured domestically may, with the approval of the Ministry of Economic Affairs, be exempted from import tariffs and business taxes. Import tariffs and business taxes will be levied on imported machinery or equipment that, within five years of its importation, is sold or its use is changed so that it no longer meets the conditions for tax exemption or conforms to its original use. Machinery or equipment that is sold to companies that operate within science-based industrial parks, economic processing zones, or other science-based industrial companies is not subject to this limitation. Raw materials that are imported by bonded factories are exempt from import tariffs and business taxes. Import tariffs and business taxes will be levied on such raw materials, however, if they are shipped outside the bonded area.

B、R&D Subsidies : Measures for encouraging the development of leading new products

C、Contents

In order to encourage new product development by private manufacturers with R&D potential, and to share some of the burden of risk, the government may provide a subsidy of up to 40% of the cost of development.

D、Scope of Eligible Products a. Products of emerging important strategic industries. b. Products employing key technologies that surpass current standards of industrial technology in Taiwan. c. Products that have a strong linking effect and good market potential, and that can stimulate the development of related industries. d. Intellectual property rights revert to the developing company.

E、 Low-interest Loans

To accelerate industrial development and economic growth, a special fund has been set aside by the Development Fund of the Executive Yuan for cooperation with banks in providing various kinds of special low-interest loans. These include preferential loans for small and medium-sized enterprises (SMEs) to upgrade and purchase automation equipment, and loans to private enterprises for purchasing pollution control and pollution treatment equipment. In addition, the government has allocated NT$100 billion from new postal deposit funds for the “Medium-and Long- term Capital Loan Plan.” Private investors whose projects have a value of NT$ 100 billion or more may apply for loans under this plan.

F、 Government Participation in Investment

a. Investors can ask the government to participate in their investment projects to a maximum of 49% of the total capitalization. The following government agencies represent the government in providing capital: (a) The Sci-Tech Development Fund and other development funds (b) Chiao Tung Bank (c) Management Committee of the Executive Yuan Development Fund b. Investment Focus In the past, the focus was on important productive industries included in economic construction plans, such as petrochemicals and semiconductors. In recent years the focus has been on Ten Emerging Industries, including information, communications, aerospace, and biotechnology.