Assumptions of the LP Model

Q: What are the assumptions for the LP model?

A: Additivity, Proportionality, Determinism and Divisibility.

Q: Are these the same assumptions as for the Transportation model?

A: There is one extra – divisibility.

Q: Are the definitions the same as for the Transportation model?

A: Similar, but we change the definitions to reflect the change in model.

Q: Are the defenses the same as for the Transportation model?

A: No.

Q: What is the assumption of Additivity for LP?

A: Additivity is the assumption that the value of one variable does not affect the cost or profit of any other variable.

Q: How is that different from Additivity for the Transportation model?

A: In Transportation, we used the word “route” instead of “variable.”

Q: What was the difficulty with Additivity in the Transportation model?

A: Piggy-backing loads to save money.

Q: Do we have that same problem with LP?

A: No.

Q: Why not?

A: We are not moving a physical product in LP; we are assigning values to variables.

Q: What problem do we have with Additivity in LP?

A: Usually, none at all.

D: Think of what the variables represent in LP – products or services that we provide. Imagine you worked for a bank. Then the number of loans you make would not affect the interest paid on savings accounts. If you manufactured kitchen appliances, then the number of refrigerators you made would not affect the profit earned on dishwashers. Usually, for products and services, this is a good assumption.

Q: What is an example of product or service where this isn’t true?

A: Nintendo.

Page 1 of 8 0347b0ddc08d43e93b26a2839cf54c02.doc, Page 2 of 8

D: Nintendo (or any of its competitors) has two product lines: game cartridges and the playback consoles. Even thought the consoles cost more (between $100 and $200) there is usually no profit on them. The games sell for less ($50?), but are almost 100% profit.

Q: Why is the profit on games 100%?

A: The development costs are sunk costs, since you pay them even if you do not sell a single game. All that is left is materials (a disk), packaging, and shipping.

Q: How is this a problem with Additivity?

A: Think like a computer – if you have one product line (consoles) with a negative profit and one product line (games) with a near-100% profit, clearly you should put all resources toward making the games.

Q: What is wrong with making only games?

A: If you don’t make playback units, no one will buy the games.

Q: What does that have to do with Additivity?

A: Additivity says that the value of one variable (consoles) does not affect the cost or profit of another variable (games). If you do not make any consoles (value = 0), then the profit on games changes to zero. If you do make consoles, the profit on games goes back up. Thus the value of the variable for number of games to make does affect the profit of another variable, games. This is a situation where two products are completely complimentary and Additivity is violated.

Q: What should we do?

A: If you are Nintendo, don’t use LP to determine production amounts.

Q: What is the assumption of Proportionality for LP?

A: Proportionality is the assumption that any per-unit value for a variable is constant for all values of the variable.

Q: How is that different from Proportionality for the Transportation model?

A: In Transportation, we talked about “cost or profit for each route.”

Q: What was the difficulty with Proportionality in the Transportation model?

A: Volume discounting.

Q: Do we have that same problem with LP?

A: Yes, if you generalize “volume discounts” into “economies of scale.”

Q: What problem do we have with Proportionality in LP?

A: Most operations show a decrease in cost (increase in profit) per-unit as volume increases, rather than a constant cost per unit as the assumption of Proportionality says.

Q: What causes the decrease in costs per-unit?

A: Volume discounts are a part of it, but you also have increased experience in your workforce and improved equipment (in essence, shifting variable costs to fixed costs). 0347b0ddc08d43e93b26a2839cf54c02.doc, Page 3 of 8

Q: Why is this a problem?

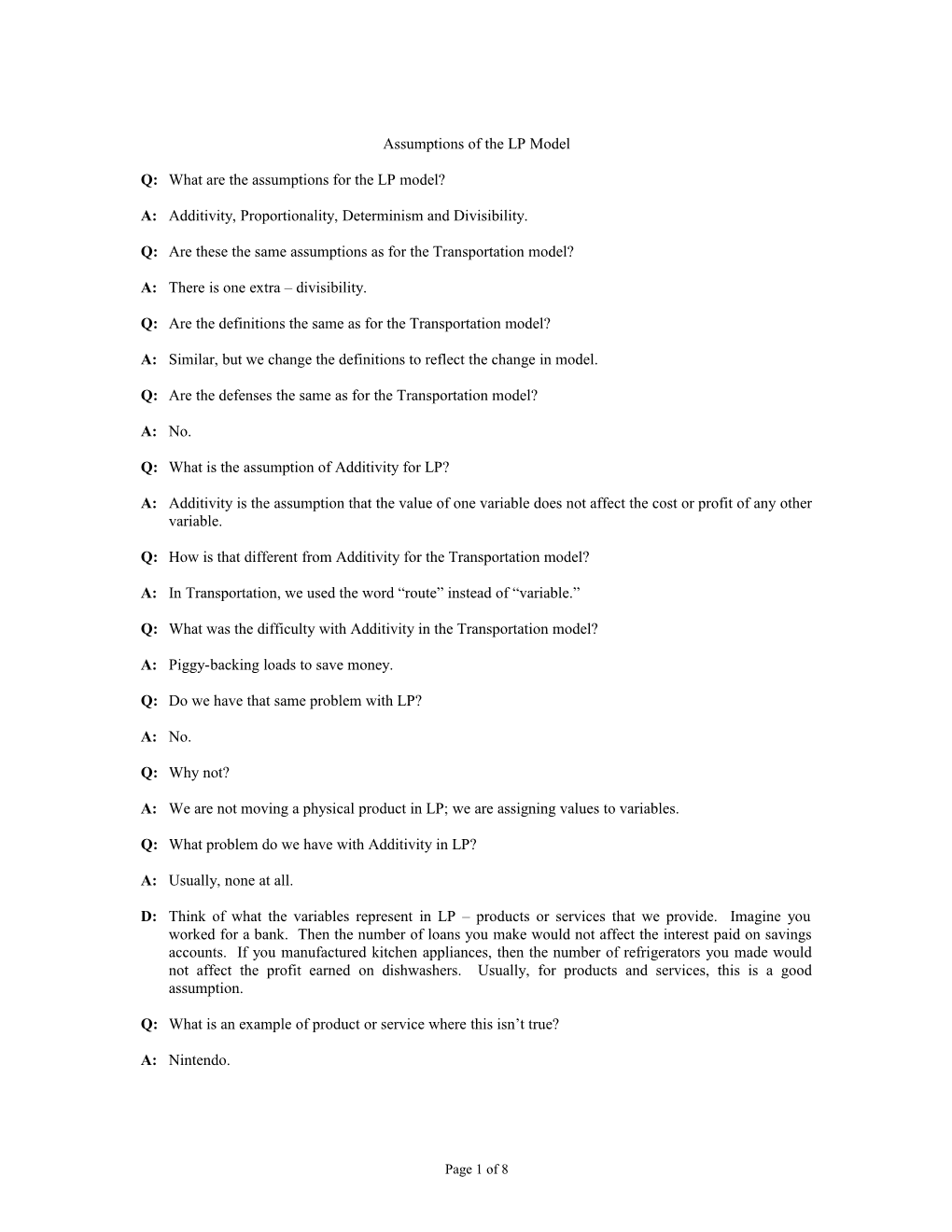

A: Linear Programming does not adjust to these changes in cost. Look at the graph in Figure 1:

Total Profit Economies-of- scale curve

Proportionality line

Volume Figure 1: Profit versus Volume

Q: What does the curved line show?

A: Profit grows slowly when few units are being produced, increases rapidly for a middle range of production, then grows more slowly for high production volumes (you are flooding the market, depressing your selling price).

Q: What does the straight line show?

A: Profit grows at a constant rate, proportional to volume (that’s where the name comes from).

Q: Can you reconcile these two views?

A: Partially. Look at Figure 2:

Total Profit Economies-of- scale curve

Proportionality line

Volume 0347b0ddc08d43e93b26a2839cf54c02.doc, Page 4 of 8

Figure 2: Piecewise Linear Approximation of Economies-of-Scale

Q: What is a “piecewise linear approximation?”

A: Using straight line segments to mimic a curved line, like the yellow highlights in Figure 2.

Q: What is the purpose?

A: The yellow highlights show that for ranges of production volumes (low, middle or high) a single (constant) profit per-unit is pretty close to reality.

Q: Doesn’t the profit per-unit change between the ranges?

A: Yes, and that is what the assumption of Proportionality is telling you.

Q: What is the practical application of Proportionality?

A: Provided your production volume is relatively constant from one period to the next, then you are safe using a single profit per-unit number. If your production volume changes dramatically, you should review your per-unit numbers to see if they have changed.

Q: Isn’t that just common sense?

A: Yes, but there is nothing less common than common sense. The assumption of Proportionality tells you that LP will not allow for this, so you must take care of it on your own.

Q: What is the assumption of Determinism?

A: As always, the assumption that your data is 100% accurate.

Q: Is LP data 100% accurate?

A: No.

Q: Do we perform a sensitivity analysis to decide if our data is acceptably accurate?

A: Yes.

Q: Do we estimate allowable variation and expected variation?

A: No, the computer does the allowable variation for you.

Q: Do we estimate expected variation and compare that to the allowable variation ranges given to us by the computer?

A: No, all we usually do is look at the width of the ranges and ask ourselves if they are “wide enough.”

Q: What does “wide enough” mean?

A: Basically, expected variation. The difference is that in LP, a great many of the parameters are under our control, so there is little or no expected variation. For the rest, rather than try to come up with a figure for expected variation, we simply check to see if we are comfortable with the range that is allowed. See the lecture notes on “Reading an LP Printout” and “Sensitivity Analysis of an LP Problem” for examples. 0347b0ddc08d43e93b26a2839cf54c02.doc, Page 5 of 8

Q: What is the assumption of Divisibility?

A: Literally, that the all variable are continuous.

Q: What does is mean for a variable to be continuous?

A: It means that the variable can have fractions as values.

Q: Is that a problem?

A: Mathematically, no, but from a real-world point-of-view, yes.

Q: What is wrong with variables having fractional values in the real world?

A: Variables represent real-world objects and if those objects cannot be divided into fractions, then the fractional value for the variable cannot be interpreted.

Q: Is that all?

A: No, the assumption really goes further. Mathematically, the fractional value also gives you fractional profit, which can end up overstating the total profit.

Q: Can you give an example?

A: Sure. Suppose B ≡ # of basketballs to make and B = 19.5. That half-basketball takes half the time to make using half the resources of a whole basketball and brings in half the profit. Unfortunately for your customer, half a basketball doesn’t bounce half as high as a whole basketball.

Q: Is this a problem?

A: That depends on the production volume and the cost per-unit.

Q: Could you give an example?

A: Suppose C ≡ # of cars to make and C = 694,864.53574125864951.

Q: Would a computer give you a result like this?

A: Of course; computers just love decimals.

D: Most computer users also love them; they think they are getting very accurate results. Reality is that the accuracy of the input data does not support anywhere near that number of decimals. There is a whole field of study on this called “significant figures.” You may have run across it in a chemistry or physics class.

Q: What is the problem with all the decimals?

A: Since we can’t, really, make and sell a fraction of a product, not even .53574125864951 of one, then we have to round either up or down, and we don’t know which way to go.

Q: What would be the effects of rounding up?

A: We would increase profits for this product, but to do that we would have to steal resources from another product, decreasing profits there.

Q: What would be the effects of rounding down? 0347b0ddc08d43e93b26a2839cf54c02.doc, Page 6 of 8

A: We would decrease profits for this product, and free up resources for some other product to use, increasing profits there.

Q: Which is better?

A: We have no idea.

Q: Is this significant?

A: Actually, no.

Q: Why not?

A: We are making so many cars (694,864) that making one more (694,865) cannot have a significant impact on our profits or resource utilization. Actually, though, the rounding problem goes even further.

Q: How does rounding go even further?

A: When your boss calls to ask for the production numbers for the next period, and you start reeling off 694,864.53574125864951, you will hear a dial tone as your boss hangs up on you before you ever even get to the decimals.

Q: Why did the boss hang up before s/he got all the numbers?

A: Your boss know that output from a computer model such as LP is the starting point for decision making, not the ending point.

Q: What does that mean?

A: In every decision making situation, there are some aspects of the problem that are quantitative (number-oriented) and some aspects that are qualitative (no numbers involved).

Q: Which part is dealt with by a computer?

A: Only the quantitative parts.

Q: Can we just ignore the qualitative parts?

A: No.

Q: How do we include the qualitative parts?

A: Take the solution given to you by the computer, say, by LP, and YOU decide how to change that answer to reflect the qualitative issues.

Q: Could you give an example?

A: Since your variable is “# of cars to make,” we can assume you make cars. All car makers are unionized. Keeping the union happy is definitely important to the car maker, but there is no way to put number to the words “keep the union happy.” This is why your boss hung up after hearing “six hundred and ninety four thousand, eight hundred …” S/he just wrote down “700K” and left it at that, knowing the number would be adjusted up and/or down, until everyone was satisfied (if not happy) with it. 0347b0ddc08d43e93b26a2839cf54c02.doc, Page 7 of 8

Q: Does this affect the assumption of divisibility?

A: To a large extent, it makes the assumption irrelevant.

Q: Are there ever situations where Divisibility is correct?

A: Any time your variables represent something that is measured in units that can be expressed as fractions, this assumption is correct.

Q: What units can be expressed as fractions?

A: Liquids (a fraction of a liter), land (a fraction of an acre), money (a fraction of a penny), cloth (a fraction of a bolt), room (a fraction of an office), or lots of others.

Q: Money?

A: Not always, but think of investing in a mutual fund. The dollar you put in is split between hundreds of different stocks, because most money is simply an entry on a computer, so fractions of a penny are possible.

Q: What is an example of when divisibility is not acceptable?

A: Boeing.

Q: What does Boeing make?

A: Airplanes.

Q: Little tiny model airplanes?

A: No, great, big, expensive airplanes.

Q: What is their production volume per month?

A: Maybe three.

Q: Suppose an LP program told them to produce 2.5 airplanes next month. Would there be a slight difference between producing two airplanes versus three?

A: Most definitely.

Q: Can we let work-in-process handle this?

A: Not really. The assumption says that at the end of the month, whatever you have completed can be sold. This is Cost Accounting taken to an extreme. Companies like Boeing produce to contract, but need to allocate production to various periods, and they want to allocate whole units. So, they can’t use LP.

Q: What do they use?

A: A version of linear programming called “integer programming” or IP.

Q: What is integer programming?

A: Similar to LP except for two things – it always delivers integer solutions and it takes forever to solve. 0347b0ddc08d43e93b26a2839cf54c02.doc, Page 8 of 8

Q: What to you mean by “forever?”

A: Consider a small real-world LP problem, say, 1,000 variables and 5,000 constraints. That could probably be solved over night on a desktop computer. To solve the same problem as an IP would probably take a week or more.

Q: Do companies really use IP, if it takes that long?

A: Only when they have to. Most companies live with the inaccuracy of LP and don’t worry about it. A few companies, like Boeing, are forced to use IP.

Q: What forces a company to use IP?

A: When the production volume is low or the cost per-unit is high, you cannot round the variables, so you use IP.