Copyright © 2007 Tax Analysts Tax Notes

MARCH 26, 2007

LENGTH: 2149 words

DEPARTMENT: News, Commentary, and Analysis; Viewpoint

CITE: Tax Notes, Mar. 26, 2007, p. 1255; 114 Tax Notes 1255 (Mar. 26, 2007)

HEADLINE: 114 Tax Notes 1255 - MEASURING THE TRADE-OFF BETWEEN TAX EXPENDITURES AND TAX RATES. (Section 1 -- Individual Tax) (Release Date: MARCH 07, 2007) (Doc 2007-5863)

AUTHOR: Forman, Jonathan Barry University of Oklahoma

CODE: (Section 1 -- Individual Tax)

SUMMARY: Jonathan Barry Forman is the Alfred P. Murrah professor of law at the University of Oklahoma and the author of Making America Work (Urban Institute Press 2006).

GEOGRAPHIC: United States

REFERENCES: Subject Area: Individual income taxation; Legislative tax issues; Politics of taxation; Tax policy issues

TEXT:

Measuring the Trade-Off Between Tax Expenditures and Tax Rates

Release Date: MARCH 07, 2007 By Jonathan Barry Forman High tax rates distort individual decisions about work and savings. With a broader tax base, however, we could have lower tax rates. In this article I estimate how much we could reduce average individual income tax rates if we repealed some of the largest tax expenditures.

Table 1 on the next page shows the Office of Management and Budget's recent estimates of the 10 largest income tax expenditures. Those estimates can be thought of as rough estimates of how much more revenue the federal government would collect if those special provisions were repealed. For example, if we repealed the exclusion for employer-provided healthcare coverage, Treasury could collect around $ 160 billion in 2008./1/

This article estimates how much average individual income tax rates could be cut if we repealed the tax expenditures in Table 1.

Consider a tax system that raises $ 1 trillion in revenue by imposing a 10 percent tax on a $ 10 trillion tax base. If we expanded that tax base by $ 2 trillion to $ 12 trillion, we could raise that $ 1 trillion with a tax rate of just 8-1/3 percent. Mathematically: $ 1 trillion = 10 percent x $ 10 trillion = 8-1/3 percent x $ 12 trillion. In fact, the average tax rate imposed by the individual income tax is around 10 percent. For example, according to the Urban- Brookings Tax Policy Center, the average effective income tax rate imposed on individuals in 2007 is 10.3 percent./2/

Next we need an estimate of the approximate size of the individual income tax base. The 2008 federal budget estimates that the federal government will collect about $ 1.25 trillion in individual income taxes in 2008./3/ Assuming an average individual income tax rate of 10 percent, our hypothetical individual income tax base will be around $ 12.5 trillion in 2008 ($ 12.5 trillion x 10 percent = $ 1.25 trillion)./4/

Now we have the approximations that we need to estimate the average individual income tax rate reductions that could result from repeal of the tax expenditures in Table 1. For example, if Congress were to repeal the current exclusion for employer- provided healthcare coverage, Table 1 tells us the federal government would collect around $ 160 billion more revenue in 2008. For our purposes, it's as if repealing the exclusion expands the individual income tax base by $ 1.6 trillion ($ 160 billion divided by 10 percent = $ 1.6 trillion)./5/

Of course, if the tax base grows, we can cut the average tax rate and still raise the same amount of revenue. More specifically, if the tax base increased by $ 1.6 trillion, from $ 12.5 trillion to $ 14.1 trillion, we could cut the average tax rate from 10 percent to 8.86 percent ($ 1.25 trillion = 8.86 percent x $ 14.1 trillion). The difference between the original 10 percent average tax rate and the after-repeal 8.86 percent tax rate is 1.14 percentage points, and that -- 1.14 percentage points -- is our estimate of the average individual income tax rate reduction that could be achieved by repealing the current exclusion for employer-provided healthcare coverage. Table 1. Top 10 Income Tax Expenditures, 2008 (in millions) ______Provision Revenue Effect ______

Exclusion of employer contributions for $ 160,190 medical insurance premiums and medical care

Deductibility of mortgage interest on 89,430 owner-occupied homes

Accelerated depreciation of machinery 64,670 and equipment

Capital gains (except agriculture, 51,960 timber, iron ore, and coal)

Employer plans 48,480

Deductibility of charitable 45,760 contributions, other than education and health

401(k) plans 43,970

Capital gains exclusion on home sales 38,890

Step-up basis on capital gains at death 35,900

Exclusion of net imputed rental income 35,680 ______

Source: Executive Office of the President and Office of Management and Budget, Analytical Perspectives, Budget of the United States Government, Fiscal Year 2008 (2007), table 19-3.

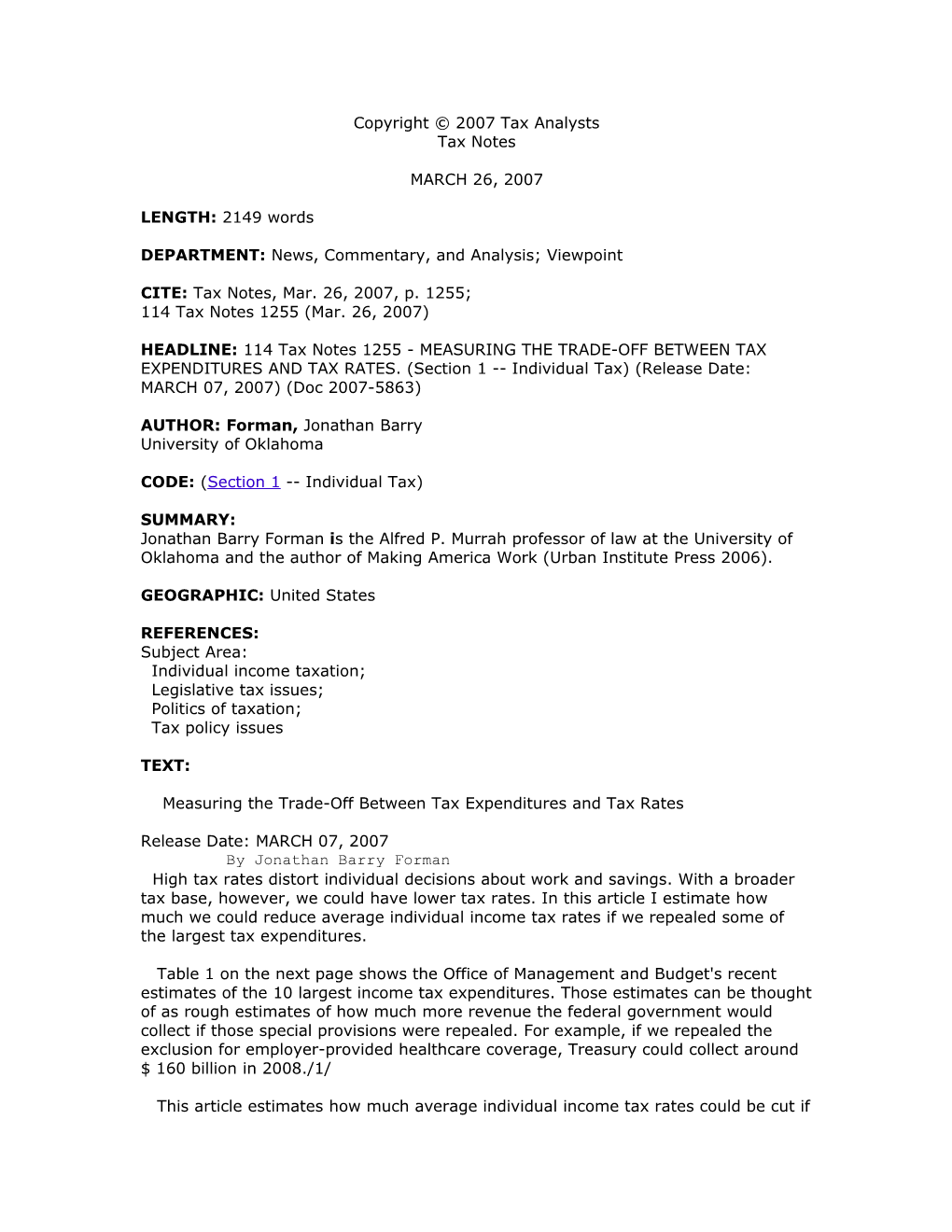

Table 2. Estimates of the Average Individual Income Tax Rate Reductions That Could Result From Repeal of 8 of the Top 10 Income Tax Expenditures, 2008 ______

Minus Rate Equals Average Average Tax Reduction From Tax Rate After Rate Under Repeal of Repeal of Provision Current Law Provision Provision ______

Exclusion of 10% 1.14% 8.86% employer contributions for medical insurance premiums and medical care

Deductibility of 10% 0.67% 9.33% mortgage interest on owner-occupied homes

Accelerated 10% n/a n/a depreciation of machinery and equipment

Capital gains 10% 0.40% 9.60% (except agriculture, timber, iron ore, and coal)

Employer plans 10% 0.37% 9.63%

Deductibility of 10% n/a n/a charitable contributions, other than education and health

401(k) plans 10% 0.34% 9.66%

Capital gains 10% 0.30% 9.70% exclusion on home sales

Step-up basis on 10% 0.28% 9.72% capital gains at death

Exclusion of net 10% 0.28% 9.72% imputed rental income

Repeal of all 10% 2.88% 7.12% eight individual income tax expenditures ______

Source: Author's computations. In sum, if we repealed the exclusion for employer-provided healthcare coverage, we could reduce the average individual income tax rate from 10 percent to 8.86 percent./6/

Table 2 on the previous page provides estimates of the average individual income tax rate reductions that could result from repeal of most of the tax expenditures in Table 1. For eight of the provisions in Table 1, all of the current revenue losses are attributable to reductions in individual income tax revenues. For the accelerated depreciation and charitable contribution tax expenditures however, some of the revenue losses result from reductions in individual income tax liabilities and some from reductions in corporate income tax liabilities./7/ For clarity, no individual income tax rate reduction estimates are computed for those two tax expenditures. Finally, Table 2 offers an estimate of the total reduction in the average individual income tax rate that could result from repealing all eight of the remaining tax expenditures./8/

As Congress struggles to find revenue to fix the alternative minimum tax in the short run, and the fiscal gap in the long run, painful reforms will be needed. The individual income tax rate reduction estimates in this article highlight the trade-off between costly tax expenditures and lower tax rates. The bottom line is that the more tax expenditures we can repeal, the lower we can keep tax rates; and low tax rates are good for workers, good for savers, and good for the economy. Logically, of course, it would be hard to imagine an income tax base being larger than the gross domestic product ($ 14.7 trillion in 2008). If so, then the average individual income tax rate could not fall below 8.5 percent. ($ 1.25 trillion = 8.5 percent x $ 14.7 trillion.) FOOTNOTES /1/ Because taxpayers are likely to behave somewhat differently after repeal, those estimates "do not necessarily equal" the increase in federal revenues that would result from repeal. Executive Office of the President and Office of Management and Budget, Analytical Perspectives, Budget of the United States Government, Fiscal Year 2008 (2007), at 286. In general, repealing a tax expenditure will raise less revenue than Table 1 suggests. For example, if Congress repealed the exclusion for employer-provided healthcare, coverage levels would almost certainly fall, and, consequently, income tax revenues would actually increase by less than $ 160 billion.

/2/ Urban-Brookings Tax Policy Center, Table T06-0307 (Current-Law Distribution of Federal Taxes by Cash Income Class, 2007) (Nov. 30, 2006 result), http://www.taxpolicycenter.org/taxmodel/tmdb/tmtemplate.cfm?ttn=t06-0307. See also Congressional Budget Office, Historical Effective Tax Rates: 1979 to 2003 (2005).

/3/ The gross domestic product in 2008 is projected to be $ 14.71 trillion, and individual income tax receipts are projected to be $ 1.25 trillion (about 8.5 percent of GDP). Executive Office of the President and Office of Management and Budget, Analytical Perspectives, Budget of the United States Government, Fiscal Year 2008, tables 12-1 and 17-1.

/4/ That is roughly the same as the government's estimate of total U.S. personal income. According to the Economic Report of the President, total U.S. personal income grew from $ 9.7 trillion in 2004 to $ 10.2 trillion in 2005. Council of Economic Advisers, Economic Report of the President (2007), table B-29. At that rate, total U.S. personal income should be close to $ 12.5 trillion by 2008.

/5/ Equivalently, $ 1.6 trillion x 10 percent = $ 160 billion. To be sure, repealing the exclusion for employer-provided healthcare would not actually expand the individual income tax base that much. After all, the exclusion benefits more high- income, high- bracket employees than low-income, low-bracket employees. Consequently, repeal of the exclusion might actually increase the tax base by just $ 0.8 trillion -- but the average tax bracket of those affected might be 20 percent. Still, conceptualizing the repeal as if it were an expansion of the tax base by $ 1.6 trillion is reasonable -- as an intermediate step toward ultimately estimating how much average tax rates could be cut as a result of the repeal. Please bear with me.

/6/ To be sure, high-bracket taxpayers would bear most of the burden of the repeal (as they get most of the benefits of the exclusion), but when all is said and done, repealing the exclusion could result in a reduction in the average individual income tax rate by 1.14 percentage points, from 10 percent to 8.86 percent. Alternatively, if repealing the exclusion only increased the tax base by $ 0.8 trillion (as considered in footnote 5), then the average individual income tax rate would only drop to 9.4 percent. ($ 12.5 trillion + $ 0.8 trillion = $ 13.3 trillion; $ 1.25 trillion = 9.4 percent x $ 13.3 trillion.)

/7/ In 2008 corporations will get $ 44.78 billion of the tax expenditure for accelerated depreciation, and individuals will get $ 19.89 billion; corporations will get $ 1.44 billion of the tax expenditure for charitable contributions, and individuals will get $ 44.32 billion. Executive Office of the President and Office of Management and Budget, Analytical Perspectives, Budget of the United States Government, Fiscal Year 2008, table 19-2.

/8/ Mathematically, I added the remaining eight tax expenditure estimates from Table 1 together; divided that sum by 10 percent; added that result to the $ 12.5 trillion hypothetical individual income tax base for 2008; and divided the latter sum by the $ 1.25 trillion in individual income tax that we will need to raise that year. The result -- 7.12 percent -- is the average effective tax rate after repeal of those eight tax expenditures. ($ 504,500 million = $ 160,190 million + $ 89,430 million + $ 51,960 million + $ 48,480 million + $ 43,970 million + $ 38,890 million + $ 35,900 million + $ 35,680 million; $ 504,500 million divided by 10 percent = $ 5.045 trillion; $ 5.045 trillion + $ 12.5 trillion = $ 17.545 trillion; $ 17,545 trillion x 7.12 percent = $ 1.25 trillion.) I know that there are interaction effects among these eight tax expenditures and behavioral effects from their repeal, so technically they should not be added together; but I couldn't resist. Admit it, inquiring minds want to know. END OF FOOTNOTES