UNO Template

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Defendants and Auto Parts List

Defendants and Parts List PARTS DEFENDANTS 1. Wire Harness American Furukawa, Inc. Asti Corporation Chiyoda Manufacturing Corporation Chiyoda USA Corporation Denso Corporation Denso International America Inc. Fujikura America, Inc. Fujikura Automotive America, LLC Fujikura Ltd. Furukawa Electric Co., Ltd. G.S. Electech, Inc. G.S. Wiring Systems Inc. G.S.W. Manufacturing Inc. K&S Wiring Systems, Inc. Kyungshin-Lear Sales And Engineering LLC Lear Corp. Leoni Wiring Systems, Inc. Leonische Holding, Inc. Mitsubishi Electric Automotive America, Inc. Mitsubishi Electric Corporation Mitsubishi Electric Us Holdings, Inc. Sumitomo Electric Industries, Ltd. Sumitomo Electric Wintec America, Inc. Sumitomo Electric Wiring Systems, Inc. Sumitomo Wiring Systems (U.S.A.) Inc. Sumitomo Wiring Systems, Ltd. S-Y Systems Technologies Europe GmbH Tokai Rika Co., Ltd. Tram, Inc. D/B/A Tokai Rika U.S.A. Inc. Yazaki Corp. Yazaki North America Inc. 2. Instrument Panel Clusters Continental Automotive Electronics LLC Continental Automotive Korea Ltd. Continental Automotive Systems, Inc. Denso Corp. Denso International America, Inc. New Sabina Industries, Inc. Nippon Seiki Co., Ltd. Ns International, Ltd. Yazaki Corporation Yazaki North America, Inc. Defendants and Parts List 3. Fuel Senders Denso Corporation Denso International America, Inc. Yazaki Corporation Yazaki North America, Inc. 4. Heater Control Panels Alps Automotive Inc. Alps Electric (North America), Inc. Alps Electric Co., Ltd Denso Corporation Denso International America, Inc. K&S Wiring Systems, Inc. Sumitomo Electric Industries, Ltd. Sumitomo Electric Wintec America, Inc. Sumitomo Electric Wiring Systems, Inc. Sumitomo Wiring Systems (U.S.A.) Inc. Sumitomo Wiring Systems, Ltd. Tokai Rika Co., Ltd. Tram, Inc. 5. Bearings Ab SKF JTEKT Corporation Koyo Corporation Of U.S.A. -

WML- 30## User Manual (System Model: VI) the Purpose of This Manual Is to Explain Correct Way How to Integrate Module WML- 30## to the End Product

Page 1 of 10 WML-C30_User_Manual 25th Oct 2004 WML- 30## User Manual (system model: VI) The purpose of this manual is to explain correct way how to integrate module WML- 30## to the end product. It includes procedures that shall assist you to avoid unforeseen problems. This manual presents information that shows how module and OEM product, where module integrated, complies with regulations in certain regions. Any modifications, not expressly approved by the manufacturer could void the authority to operate in these regions. Content 1.General 2. Module design application. 3. Regulatory and Safety Compliance. European Union. 3.1 Declaration about performed tests. 3.2. Labelling 4. FCC Regulatory Information 4.1 Labelling. 4.2 Antenna implementation notes. 5. Other regulatory notes for OEM. 6. A separate approval. 1. General This Bluetooth radio module has to be installed and used in accordance with the technical description/installation instructions provided by the manufacturer. This Bluetooth radio module is intended to be placed on the market in all States, where the Bluetooth™ technology and the used frequency band is released. For detail information concerning type approval of this module (e.g. where this module is already pre-approved) please contact the authorised local distributor or the manufacturer. The system may only be implemented in the configuration that was authorized. Note that any changes or modifications to this equipment not expressly approved by the manufacturer could void the user’s authority to operate this equipment. COMMERCIAL IN CONFIDENCE This material may not in whole or part be copied, stored electronically or communicated to third parties without MITSUMI ELECTRIC CO., LTD’s prior agreement in writing. -

Integrated Report (Year Ended March 2019)

Introduction/ Chapter I Chapter II Chapter III Chapter IV President’s message Value Creation Story of MinebeaMitsumi Financial Strategy and Capital Policy Initiatives for Value Creation Initiatives to Support Value Creation 1986 2010 Hamamatsu Plant is established Suzhou Plant is established to expand Development in the electronic devices production of LED backlights Chapter I Value Creation Story of MinebeaMitsumi and components area is expanded History of MinebeaMitsumi Backlights Suzhou Plant (China) FDDs and MODs 2018 Global development ahead of other Hamamatsu Plant (Japan) Kosice Plant in Slovakia commences 2010 1988 production Our plant is established in Cambodia, and Lop Buri Plant is established in Thailand Supply to Europe market is commences production the next year Production in expanded companies For risk diversification, expansion of the electronic production and reduction of costs devices and components Cambodia Plant Speedy diversification through M&As area is expanded 1980 1963 Lop Buri Plant (Thailand) Ayutthaya Plant is AGA (Active Grill Plant is relocated from Kawaguchi, Saitama, and operations 1994 established 1984 Kosice Plant (Slovakia) Shutter) Actuators begin at the Karuizawa Plant, to become the mother The Company Bang Pa-in Plant is Minebea Electronics & plant of all the MinebeaMitsumi Group’s plants advances for the first established as the second Hi-Tech Components , in Miyota-machi, Nagano worldwide time into Thailand, the (Shanghai) Ltd. (our facility in Thailand Resonant devices Group’s largest first plant -

INVESTORS GUIDE 2019 Osaka Office to Our Shareholders and Investors Fukuoka Sales Office Shinjuku Office Shinjuku Support Center Tachikawa Sales Office

TOKYO ELECTRON DEVICE LIMITED Securities code: 2760 Business Locations (As of July 1, 2019) Business Location Domestic Subsidiary Omiya Sales Office Matsumoto Sales Office Sendai Sales Office Tsukuba Sales Office Iwaki Sales Office Nagoya Sales Office Mito Sales Office Kyoto Sales Office INVESTORS GUIDE 2019 Osaka Office To Our Shareholders and Investors Fukuoka Sales Office Shinjuku Office Shinjuku Support Center Tachikawa Sales Office Engineering Center Headquarters (Yokohama) FAST CORPORATION (Yamato-city, Kanagawa prefecture) TOKYO ELECTRON DEVICE Mishima Sales Office NAGASAKI LTD. Hamamatsu Sales Office (Isahaya-city, Nagasaki prefecture) Business/Marketing location Overseas Design and development location Dalian Yokohama Ottawa Seoul Silicon Valley Shanghai Taipei Shenzhen Bangkok Wuxi Hong Kong Singapore Philippines Note on forward-looking statements This Investors Guide was prepared on July 1, 2019. Forward looking statements, including business strategies and business forecasts, were made by the Company’s management, based on information available at that time, and may be revised due to changes in the business environment. Therefore, please be advised that the Company cannot guarantee the accuracy or the reliability of the statements. For the latest information, please refer to our information releases or our website. Note also that product and service names remain the trademarks of their respective owners. Corporate Communications Dept. https://www.teldevice.co.jp World Headquarters Yokohama East Square, 1-4 Kinko-cho, Kanagawa-ku,Yokohama -

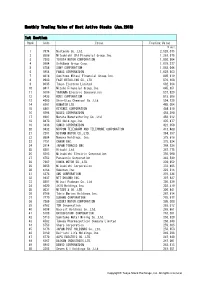

Monthly Trading Value of Most Active Stocks (Jan.2018) 1St Section

Monthly Trading Value of Most Active Stocks (Jan.2018) 1st Section Rank Code Issue Trading Value \ mil. 1 7974 Nintendo Co.,Ltd. 2,526,075 2 8306 Mitsubishi UFJ Financial Group,Inc. 1,261,575 3 7203 TOYOTA MOTOR CORPORATION 1,086,604 4 9984 SoftBank Group Corp. 1,079,377 5 6758 SONY CORPORATION 1,068,044 6 6954 FANUC CORPORATION 1,028,863 7 8316 Sumitomo Mitsui Financial Group,Inc. 895,619 8 9983 FAST RETAILING CO.,LTD. 870,168 9 8035 Tokyo Electron Limited 682,994 10 8411 Mizuho Financial Group,Inc. 645,951 11 6506 YASKAWA Electric Corporation 537,829 12 9433 KDDI CORPORATION 513,306 13 4063 Shin-Etsu Chemical Co.,Ltd. 504,120 14 6301 KOMATSU LTD. 485,054 15 6861 KEYENCE CORPORATION 484,810 16 6594 NIDEC CORPORATION 458,398 17 6981 Murata Manufacturing Co.,Ltd. 458,012 18 8473 SBI Holdings,Inc. 435,477 19 3436 SUMCO CORPORATION 423,058 20 9432 NIPPON TELEGRAPH AND TELEPHONE CORPORATION 413,468 21 7201 NISSAN MOTOR CO.,LTD. 394,197 22 8604 Nomura Holdings, Inc. 379,616 23 7751 CANON INC. 375,624 24 2914 JAPAN TOBACCO INC. 368,526 25 6501 Hitachi,Ltd. 367,775 26 6503 Mitsubishi Electric Corporation 350,098 27 6752 Panasonic Corporation 342,549 28 7267 HONDA MOTOR CO.,LTD. 339,952 29 8058 Mitsubishi Corporation 333,495 30 4755 Rakuten,Inc. 329,315 31 6273 SMC CORPORATION 315,134 32 9437 NTT DOCOMO,INC. 307,827 33 8801 Mitsui Fudosan Co.,Ltd. 305,639 34 5020 JXTG Holdings,Inc. -

第 1 頁,共 5 頁 Hdmi :: ?喃? :: ? 熙? ?蝏 ? 2005/7/19

HDMI :: ?喃? :: ? 熙? ?蝏 ? 第 1 頁,共 5 頁 HDMI 组织 Hitachi, Ltd. Matsushita Electric Industrial Co., Ltd. (Panasonic) Sony Corporation Philips Consumer Electronics International B.V. Thomson, Inc. Silicon Image, Inc. Toshiba Corporation HDMI 许可采纳者 Last Updated on 7/18/2005 2Wire Inc Krell Industries 3S Digital Co Ltd Leader Electronics Corp. 690885 Ontario Inc. LeCroy Japan Corporation A&R Cambridge Ltd (Arcam) LG Electronics Advanced-Connectek Inc. Linktec Technologies Co Ltd Advanced Display Lab Inc. Linn Products Ltd Advanced Knowledge Associates Lin Shiung Enterprise Co Ltd Agilent Technologies Inc. Lite-On Corporation Akai Electric Co Ltd Loewe Opta GmbH Alco Digital Devices Limited Longwell Company Algolith Inc. LPS Device Co Ltd ALI Corporation Main Super Enterprises Co. Amoi Electronics Co Ltd Marshall Electronics AmTran Technology Master Co. LTD-Korea Analog Devices, Inc. Master Hill Electric Wire & Cable Analogix Semiconductor Inc MediaTek Corp. Anam Electronics Co Ltd Meridian Audio Limited Anchor Bay Technologies Metz-Werke GmbH & Co KG Asahi Kasei Microsystems Co Ltd Micronas GmbH http://cn.hdmi.org/about/adopters_founders.asp 2005/7/19 HDMI :: ?喃? :: ? 熙? ?蝏 ? 第 2 頁,共 5 頁 AstroDesign Inc. MIK21 Co., Ltd Asustek Computer Inc Y-S Electronic Co., Ltd ATI Technologies, Inc. Mitac Technology Corp Audio Partnership PLC Mitsubishi Electric Corporation Audio-Technica Corporation Mitsumi Electric Co., Ltd. Aurora Multimedia Corp Molex Incorporated Avid Technology Inc. Morning Star Industrial BAFO Technologies/TWN 1st Line Elect Cor Motorola, Inc. Bang & Olufsen MSL Enterprises Corp BBK AV Electronics Corp Ltd. Mstar Semiconductor, Inc. BenQ Corporation Murata Manufacturing Co.,Ltd. Beko Elektronik A.S. -

ALPS ALPINE CO., LTD. Announces Acquisition of Own Shares

January 29, 2019 For Immediate Release Company name: ALPS ALPINE CO., LTD Representative: Toshihiro Kuriyama, Representative Director, President & CEO (Code no.: 6770, First Section, Tokyo Stock Exchange) Please address inquiries to Junji Kobayashi, Senior Manager, Corporate Planning Office Corporate Planning Operations Telephone: +81-3-5499-8026 (IR Direct) https://www.alpsalpine.com/e/ ALPS ALPINE CO., LTD. Announces Acquisition of Own Shares (Under the provision of its Articles of Incorporation in accordance with Article 165, paragraph 2 of the Companies Act) Tokyo, Japan (January 29, 2019) – ALPS ALPINE CO., LTD. (the “Company”) today announced that at the meeting of the Board of Directors held today, a resolution was adopted to acquire its own shares under Article 156 which is applicable in accordance with Article 165, paragraph 3 of the Companies Act. Particulars 1. Reasons for the acquisition of own shares As announced in the press release dated November 26, 2018 titled “Notice Regarding the Management Policy under the Holding Company Structure, including the Basic Policy on Shareholder Returns” (the “Management Policy Press Release”), the Company (ALPS ELECTRIC CO., LTD at the time of the announcement) has decided to implement a share buyback with the aim of improving capital efficiency and responding to dilution that may occur due to the business integration and share exchange between the Company and Alpine Electronics, Inc. (“Alpine”). 2. Contents of acquisition (1) Class of shares to be acquired: Common stock of the Company -

Proposal of a Data Processing Guideline for Realizing Automatic Measurement Process with General Geometrical Tolerances and Contactless Laser Scanning

Proposal of a data processing guideline for realizing automatic measurement process with general geometrical tolerances and contactless laser scanning 2018/4/4 Atsuto Soma Hiromasa Suzuki Toshiaki Takahashi Copyright (c)2014, Japan Electronics and Information Technology Industries Association, All rights reserved. 1 Contents • Introduction of the Project • Problem Statements • Proposed Solution – Proposal of New General Geometric Tolerance (GGT) – Data Processing Guidelines for point cloud • Next Steps Copyright (c)2014, Japan Electronics and Information Technology Industries Association, All rights reserved. 2 Contents • Introduction of the Project • Problem Statements • Proposed Solution – Proposal of New General Geometric Tolerance (GGT) – Data Processing Guidelines for Point Cloud • Next Steps Copyright (c)2014, Japan Electronics and Information Technology Industries Association, All rights reserved. 3 Introduction of JEITA What is JEITA? The objective of the Japan Electronics and Information Technology Industries Association (JEITA) is to promote healthy manufacturing, international trade and consumption of electronics products and components in order to contribute to the overall development of the electronics and information technology (IT) industries, and thereby to promote further Japan's economic development and cultural prosperity. JEITA’s Policy and Strategy Board > Number of full members: 279> Number of associate members: 117(as of May 13, 2014) - Director companies and chair/subchair companies - Policy director companies (alphabetical) Fujitsu Limited (chairman Masami Yamamoto) Asahi Glass Co., Ltd. Nichicon Corporation Sharp Corporation Azbil Corporation IBM Japan, Ltd. Hitachi, Ltd. Advantest Corporation Nippon Chemi-Con Corporation Panasonic Corporation Ikegami Tsushinki Co., Ltd. Japan Aviation Electronics Industry, Ltd. SMK Corporation Mitsubishi Electric Corporation Nihon Kohden Corporation Omron Corporation NEC Corporation JRC Nihon Musen Kyocera Corporation Sony Corporation Hitachi Metals, Ltd KOA Corporation Fuji Xerox Co., Ltd. -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners International Value Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.9% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 4.2% UCB SA 3,232 367,070 AMP Ltd. 247,119 232,705 Total 13,350,657 Aurizon Holdings Ltd. 64,744 199,177 China 0.6% Australia & New Zealand Banking Group Ltd. 340,950 4,253,691 Baidu, Inc., ADR(a) 15,000 1,898,850 Bendigo & Adelaide Bank Ltd. 30,812 134,198 China Mobile Ltd. 658,000 4,223,890 BlueScope Steel Ltd. 132,090 1,217,053 Total 6,122,740 Boral Ltd. 177,752 587,387 Denmark 1.9% Challenger Ltd. 802,400 2,232,907 AP Moller - Maersk A/S, Class A 160 234,206 Cleanaway Waste Management Ltd. 273,032 412,273 AP Moller - Maersk A/S, Class B 3,945 6,236,577 Crown Resorts Ltd. 31,489 200,032 Carlsberg A/S, Class B 12,199 1,643,476 Fortescue Metals Group Ltd. 194,057 2,279,787 Danske Bank A/S(a) 35,892 485,479 Harvey Norman Holdings Ltd. 144,797 471,278 Demant A/S(a) 8,210 257,475 Incitec Pivot Ltd. 377,247 552,746 Drilling Co. of 1972 A/S (The)(a) 40,700 879,052 LendLease Group 485,961 3,882,083 DSV PANALPINA A/S 15,851 2,571,083 Macquarie Group Ltd. 65,800 5,703,825 Genmab A/S(a) 1,071 388,672 National Australia Bank Ltd. -

User's Manual

User’s Manual 78K0/IB2 Fluorescent Ballast Evaluation Board Target Device 78K0/IB2 Microcontroller ZBB-CE-09-0011-E Data Published March 2009 © NEC Electronics Corporation 1/25 z The information in this document is current as of March, 2009. The information is subject to change without notice. For actual design-in, refer to the latest publications of NEC Electronics data sheets or data books, etc., for the most up-to-date specifications of NEC Electronics products. Not all products and/or types are available in every country. Please check with an NEC Electronics sales representative for availability and additional information. z No part of this document may be copied or reproduced in any form or by any means without the prior written consent of NEC Electronics. NEC Electronics assumes no responsibility for any errors that may appear in this document. z NEC Electronics does not assume any liability for infringement of patents, copyrights or other intellectual property rights of third parties by or arising from the use of NEC Electronics products listed in this document or any other liability arising from the use of such products. No license, express, implied or otherwise, is granted under any patents, copyrights or other intellectual property rights of NEC Electronics or others. z Descriptions of circuits, software and other related information in this document are provided for illustrative purposes in semiconductor product operation and application examples. The incorporation of these circuits, software and information in the design of a customer's equipment shall be done under the full responsibility of the customer. NEC Electronics assumes no responsibility for any losses incurred by customers or third parties arising from the use of these circuits, software and information. -

USB 3.0 Adopters.Pdf

Adopting Party Name 3eYamaichi Electronics Co., Ltd. Aces Electronics Co., Ltd. ACES Electronics Co., Ltd. Action Star Enterprise Co., Ltd. Advanced‐Connectek Inc., Acon Agilent Technologies Inc. ALLTOP TECHNOLOGY CO., LTD. Amco Tec International Inc. American Megatrends, Inc. Amphenol Assemble Tech (Xiamen) Co., Ltd. Amphenol ShouhMin Industry (Shenzhen) Co., Ltd. Argosy Research Inc. Astron International Corp. Basler AG Bose Corporation Buffalo Inc. Buffalo Kokuyo Supply Inc. Cambridge Silicon Radio Limited Canon Inc. Chant Sincere Co., Ltd. Cheng Uei Precision Industry Co., Ltd. Chicony Electronics Co., Ltd. Chief Land Electronic Co., Ltd. China Electronics Technology Limited Chrontel, Inc. Circuit Assembly Corp. CNPLUS Co., Ltd. Compupack Technology Co. Ltd. Connect County Holdings Berhad DataFab Systems Inc. Digital Design Corporation Digital Information Technology Studies (ShenZhen) Ltd. DisplayLink (UK) Ltd DongGuan HYX Industrial Co., Ltd. Dongguan Kechenda Electronics Technology Co., Ltd. Dongguan Teconn Electronics Technology Co., Ltd. Dongguan Yuqin Electronics Co., Ltd. EchoStar Technologies, LLC Elektrobit, Inc. FCI USA LLC Foosung Tech Foxconn Interconnect Technology, Ltd ("FIT LTD") Freeport Resources Enterprises Corp. Fujitsu Limited Full in Hope Co., Ltd. Global Connector Technology Ltd. (GCT) Global Unichip Corp. Goodway Technology Co., Ltd. Harris Corporation Hewlett Packard High‐Top Precision Electronic Co., Ltd. Hirose Electric Co., Ltd. Hosiden Corporation Hsi Chin Electronics Co., Ltd. IBM Corporation ICT‐Lanto Limited I‐PEX USA LLC Integral Memory PLC Intel Corporation Japan Aviation Electronics Industry, Limited Jmicron Technology Corporation Jo‐Dan International Joinsoon Electronic Mfg. Co., Ltd. JPC/Main Super Inc J.S.T. Mfg. Co., Ltd. JVC KENWOOD Holdings, Inc. Kawasaki Microelectronics, Inc. Kycon, Inc. KYOCERA MITA Corporation Lenjoy Technology Limited Littelfuse Inc. -

Annual Report 2017/2018

Annual Report 2017-2018 CONTENTS Company Overview Business Domains ……………………………………………… 3 Business Report ………………………………………………… 5 History ………………………………………………………………… 7 Vision Top Message ……………………………………………………… 9 Mid-term Business Plan ……………………………………… 11 Directions of Approaches ……………………………………12 Corporate Philosophy Editorial Policy CSR Alpine values its members as individuals, and is committed to forming an energetic Since fiscal year 2016, Alpine has published an Annual Report that combines the annual report for financial information and the and attractive company where the quality of work is enhanced. Alpine CSR …………………………………………………………13 corporate profile/CSR report for business activities centering on Provision of Products and Services to non-financial information. We consider this report an important Solve Social Problems …………………………………………14 1 Respect for Individuality communication tool to help our stakeholders understand our Sustainable Supply Chain Management ………………15 activities, and actively disclose information on our business Alpine seeks to foster the pride and enthusiasm of each employee, providing the means Customer Satisfaction plans, performance, CSR management policy, environmental and opportunities for growth, and encouraging relationships built on mutual trust. Environment …………………………………………………………16 conservation efforts, and other aspects of our business. Involvement with Local Community ……………………17 2 Creating Value Participation of Diverse Human Resources ………18 Designations Within This Report Alpine eagerly takes up the challenge of maintaining technical leadership Corporate Governance ………………………………………19 Alpine: Refers to the non-consolidated domestic business. Compliance ……………………………………………………… 22 in creating new values that will enhance the quality of human life. Alpine Group: Refers to all consolidated companies around Risk Management the world. Summary of CSR Activities ……………………………… 23 3 Contribution to Society Alps Group: Refers to the corporate group led by Alps Electric.