Cara Operations to Merge with Keg Restaurants Ltd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Keg Royalties Income Fund

THE KEG ROYALTIES INCOME FUND THIRD QUARTER REPORT For the three and nine months ended September 30, 2020 TO OUR UNITHOLDERS On behalf of the Board of Trustees, I am pleased to present the results of The Keg Royalties Income Fund (the “Fund”) for the three and nine months ended September 30, 2020. RESULTS Royalty Pool sales reported by the 106 Keg restaurants in the Royalty Pool were $106,166,000 for the quarter, a decrease of $46,288,000 or 30.4% from the comparable quarter of the prior year. Year to date, Royalty Pool sales were $267,012,000, a decrease of $201,949,000 or 43.1%. The decrease in Royalty Pool sales was directly attributed to the temporary closure of all Keg restaurants starting in mid-March for approximately three months due to the Covid-19 pandemic. Royalty income decreased by $1,929,000 or 31.0% from $6,225,000 in the three months ended September 30, 2019 to $4,296,000 in the three months ended September 30, 2020. Year-to-date, royalty income decreased by $8,293,000 or 43.5% from $19,047,000 for the nine months ended September 30, 2019 to $10,754,000 for the nine months ended September 30, 2020. Distributable cash available to pay distributions to public unitholders decreased by $2,061,000 from $3,036,000 (26.7 cents/Fund unit) to $975,000 (8.6 cents/Fund unit) for the quarter and decreased by $4,057,000 from $10,110,000 (89.0 cents/Fund unit) to $6,053,000 (53.3 cents/Fund unit) year to date. -

100 Most Romantic Restaurants in Canada for 2020 Is Generated Solely from Diner Reviews Collected Between December 1, 2018, and November 30, 2019

100 MostIN CANADA Romantic FOR Restaurants 2020 BANFF TORONTO MONTRÉAL The Bison Restaurant Akira Back Bar George WINNIPEG ARDO Restaurant Bonaparte BRAGG CREEK 529 Wellington AB MB ON Auberge du Pommier QC Damas Italian Farmhouse Restaurant Cafe Carlo CONT. Bar Isabel Graziella Restaurant & Bar Blu Ristorante Gyu-Kaku CALGARY BlueBlood Steakhouse Hoogan & Beaufort Alloy Buca Ile Flottante (former Les Bow Valley Ranche Restaurant Buca - Yorkville Deux Singes) Bridgette Bar Byblos - Downtown L’Atelier de Joel Robuchon Byblos - Uptown Le Filet Cardinale DARTMOUTH Deane House Café Boulud Maison Boulud The Canteen on Portland Hy’s Steakhouse Canoe Restaurant and Bar Restaurant Toque! NS Carisma Model Milk HALIFAX POINTECLAIRE Ruth’s Chris Steak House Chiado The Press Gang 40 Westt Steakhouse Teatro Restaurant DaiLo Ten Foot Henry Don Alfonso 1890 QUEBEC CITY The Keg Steakhouse + Bar - George Restaurant Restaurant Le Continental Calgary 4th Ave Giulietta The Lake House Grey Gardens Harbour Sixty The Nash SASKATOON Vero Bistro Moderne Joso’s AURORA SK Hearth Restaurant Vintage Chophouse & Tavern L’Unità Enoteca Fishbone Kitchen + Bar Labora CANMORE BARRIE Maison Selby Tapas Restaurant ON Il Buco Mamakas Taverna EDMONTON Michael’s on Simcoe BEAMSVILLE Bundok Miku Restaurant The Good Earth Vineyard Ruth’s Chris Steak House Mira And Winery Sabor Restaurant Patria Tzin Wine & Tapas HAMILTON Ruth’s Chris Steak House Berkeley North Scaramouche Restaurant Sofi a JORDAN STATION The Keg Steakhouse + Bar - Honsberger Estate Esplanade BRENTWOOD BAY KINGSTON -

Recipe Unlimited Corporation ANNUAL INFORMATION FORM

Recipe Unlimited Corporation ANNUAL INFORMATION FORM March 25, 2021 TABLE OF CONTENTS CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS .......................................................... 1 GENERAL ..................................................................................................................................................................... 2 NON-IFRS MEASURES................................................................................................................................................ 2 CORPORATE STRUCTURE ........................................................................................................................................ 2 DEVELOPMENT OF THE BUSINESS ......................................................................................................................... 3 Three-Year History .................................................................................................................................................... 3 DESCRIPTION OF THE BUSINESS ............................................................................................................................ 5 Multiple Brand Strategy Provides Significant Competitive Advantages .................................................................... 6 Opportunities for Growth ........................................................................................................................................... 8 Recipe’s Operations ............................................................................................................................................... -

Recipe Unlimited Corporation ANNUAL INFORMATION FORM

| Recipe Unlimited Corporation ANNUAL INFORMATION FORM March 29, 2019 TABLE OF CONTENTS Page CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS ......................................... 2 GENERAL .................................................................................................................................................... 3 NON-IFRS MEASURES ............................................................................................................................... 3 CORPORATE STRUCTURE ....................................................................................................................... 5 DEVELOPMENT OF THE BUSINESS ........................................................................................................ 5 DESCRIPTION OF THE BUSINESS ........................................................................................................... 8 DESCRIPTION OF CAPITAL STRUCTURE ............................................................................................. 20 RISK FACTORS ......................................................................................................................................... 23 DIVIDENDS AND DISTRIBUTIONS .......................................................................................................... 36 PRICE RANGE AND TRADING VOLUME OF SUBORDINATE VOTING SHARES ................................ 36 PRIOR SALES .......................................................................................................................................... -

Mid-City Mellow Epitomizes a Traditional View of the Canadian Dream: Owning a Home in an Attractive Setting While Building a Comfortable Nest Egg

Older and mature city homeowners Who They Are Mid-City Mellow epitomizes a traditional view of the Canadian dream: owning a home in an attractive setting while building a comfortable nest egg. In this segment, nearly 90 percent of members own single-detached houses, which typically were built between 1960 and 1990. These older and mature households enjoy upper-middle incomes and well-established neighbourhoods in large cities like Winnipeg, Edmonton, Hamilton and Toronto. With most maintainers over the age of 55, Mid-City Mellow is a mixed group, a collection of both older couples aging in place and middle-aged families raising older children. Few segments have a lower five-year mobility rate. Most households contain third-plus-generation anadC ians, though there’s an above-average concentration of second-generation Canadians and those whose mother tongue is Italian, German, Polish or Ukrainian. With their high school and college educations, those still in the abol ur force earn solid paycheques from a mix of blue-collar and service sector jobs. The retirees and soon-to-be retirees here have the time to enjoy Population: going to hockey, baseball and football games. Many book cruises, casino junkets, ski trips and cultural tours, buoyed by their optimism for their financial future (Financial 910,785 Security). (2.40% of Canada) The upper-middle-class members of Mid-City Mellow inhabit a land of pleasant living. Households: Their older homes are graced with well-tended gardens, hot tubs and driveways 297,151 crowded with midsize cars and SUVs, boats and campers. They like the theatre and (1.99% of Canada) concerts featuring rock and country music, and the segment’s many families with children help explain the popularity of pets, pro hockey and football, as well as casual Average Household restaurants like The Keg, Swiss Chalet and Montana’s. -

Emilio Estevez, Elijah Woods X Jamie Fine, Tyler Shaw and WE Charity's

Emilio Estevez, Elijah Woods x Jamie Fine, Tyler Shaw and WE Charity’s Craig Kielburger celebrate young people leading social change at WE Day Ottawa – WE Day Ottawa will stream live at 9:00 a.m. EST today at we.org/watchweday – – WE Day Ottawa is free to students thanks to partners led by Co-Title Sponsors RBC and TELUS – – WE Day Ottawa photos will be available at 4:00 p.m. EST in the Electronic Press Kit – Ottawa, ON (December 10, 2019) – Today, WE Day Ottawa returns to the Nation’s Capital, at the National Arts Centre bringing together thousands of students and teachers from across Ontario who have created lasting change in their local and global communities. This inspiring celebration for social good features renowned speakers, innovative thought leaders and dynamic performers including Emilio Estevez, Elijah Woods x Jamie Fine, WE Charity co-founder, Craig Kielburger, Olivia Lunny, Tyler Shaw, Chloe Wilde and more. “Being a part of WE Day over the years has been an incredibly rewarding and inspiring experience,” said Multi-Platinum, Award Winning Artist and Producer, Tyler Shaw. “I’m always amazed by the students in attendance who are committed to creating change around the world, and their selflessness in doing so for the issues impacting us all.” More than a one-day event, WE Day is connected to the free, yearlong service learning program WE Schools. Designed to enhance a school or community’s existing social initiatives or spark new ones, WE Schools provides teachers with educational resources and action campaigns to encourage students to further their curricular learning and develop social and emotional skills to succeed beyond the classroom. -

Condo Living in the Royal City

CONDO LIVING IN THE ROYAL CITY REID-REI-G-BRO-CONDO-13.indd 1 2020-06-22 9:43 AM GUELPH, ONTARIO GUELPH, Nicknamed “The Royal City” by its founders two centuries AN ago, Guelph has grown from a farm town into a sophisticated city, proud of its rural roots, its world-class UNCOMMON University and its thriving businesses. Guelph’s residential heritage has grown with it, and CONDOMINIUM continues to evolve with the arrival of REIGN. Here a new generation – a new “ruling class” of young entrepreneurs and creatives – is ready to make the city their own. Welcome to a condominium that leaves the common and everyday behind. An urban living environment adds vibrance and excitement to this already charming and innovative community. REIGN Condo. Live in luxury, live like Royalty. – 3 – REID-REI-G-BRO-CONDO-13.indd 2-3 2020-06-22 9:43 AM A STATELY PRESENCE STATELY A – 5 – REID-REI-G-BRO-CONDO-13.indd 4-5 2020-06-22 9:43 AM DISTINGUISHED ARCHITECTURE IN EVERY DETAIL With its tiered, 6-storey design, this modern mid-rise residence will be a landmark address, fitting in seamlessly with the fabric of the existing neighbourhood. Inside a collection of 86 one and two bedroom suites await, each appointed with its own private balcony or patio. – 7 – REID-REI-G-BRO-CONDO-13.indd 6-7 2020-06-22 9:43 AM THE MARKET THE Guelph is a vibrant city, with its bustling downtown, shops and restaurants, arts, culture and recreation. REIGN puts it all at your doorstep, including Preservation Park, located just a short stroll away, with its 7.7km loop trail offering plenty of paths and places to explore, and a link to Hanlon Creek Conservation Area. -

THE KEG ROYALTIES INCOME FUND March 31, 2021

THE KEG ROYALTIES INCOME FUND ANNUAL INFORMATION FORM March 31, 2021. TABLE OF CONTENTS GENERAL ..................................................................................................................................................... 1 THE KEG ROYALTIES INCOME FUND ...................................................................................................... 1 The Fund ................................................................................................................................................... 1 The Keg Holdings Trust ............................................................................................................................. 1 The Keg Rights Limited Partnership .......................................................................................................... 2 The Keg GP Ltd. ........................................................................................................................................ 2 Keg Restaurants Ltd. ................................................................................................................................. 2 Business of the Partnership ...................................................................................................................... 2 Structure of the Fund ................................................................................................................................. 4 Ownership of the Fund ............................................................................................................................. -

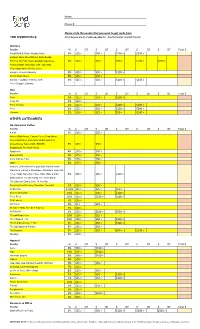

Fundscripformjune2020 (Pdf)

Name: Phone #: Please circle the vendor that you want to get cards from THE ESSENTIALS All cheques are to made payable to: Southminster United Church Grocery Retailer % $ QT $ QT $ QT $ QT $ QT Total $ Food BASIC$, Metro (Ontario Only) 3% $25 > $50 > $100 > $250 > Loblaws, Bloor Street Market, Extra Foods, Fortinos, No Frills, Real Canadian Superstore, 3% $10 > $25 > $50 > $100 > $250 > Real Canadian Wholesale Club, Valu-Mart, Your Independent Grocer, Zehrs Longo's, Grocery Gateway 3% $20 > $50 > $100 > M & M Meat Shops 3% $25 > $50 > Sobeys, Foodland, FreshCo, IGA, 3% $25 > $50 > $100 > $250 > Price Chopper, Safeway Gas Retailer % $ QT $ QT $ QT $ QT $ QT Total $ Esso 2% $25 > $50 > $100 > Irving Oil 2% $50 > Petro-Canada 2% $25 > $50 > $100 > $500 > Shell 2% $25 > $50 > $100 > $500 > Ultramar 2% $10 > $25 > $50 > $100 > OTHER CATEGORIES Restaurant & Coffee Retailer % $ QT $ QT $ QT $ QT $ QT Total $ A & W 4% $10 > $25 > Abbey’s Bakehouse, Canyon Creek Chop House, Duke’s Refresher, Jack Astor’s® Bar and Grill, Loose Moose Tap & Grill®, REDS®, 5% $25 > $50 > Scaddabush,The Antler Room Applebee's 4% $25 > $50 > Boston Pizza 5% $25 > $50 > Earl's Kitchen + Bar 5% $25 > $50 > JOEY 6% $25 > $50 > Kelsey's, D'Arcy McGee's, East Side Mario's, Fionn MacCool's, Harvey's, Milestones, Montana's, New York Fries, Paddy Flaherty's, Prime Pubs, State & Main, 5% $25 > $50 > $100 > Swiss Chalet, The Biermarkt, The Pickle Barrel, The Ultamate Dining Card, Tir Nan Óg Kentucky Fried Chicken, Pizza Hut, Taco Bell 3% $25 > $50 > McDonald's 2.50% $15 > $25 -

Dundas Baptist Church Created on 09/01/2020

Dundas Baptist Church created on 09/01/2020 NAME TELEPHONE PAYABLE TO Dundas Baptist Church NOTES THE ESSENTIALS Grocery Retailer % $ QT $ QT $ QT $ QT $ QT Total $ Loblaws, Bloor Street Market, Extra Foods, Fortinos, No Frills, Real Canadian Superstore, 3% $10 > $25 > $50 > $100 > $250 > Real Canadian Wholesale Club, Valu-Mart, Your Independent Grocer, Zehrs Longo's, Grocery Gateway 3% $20 > $50 > $100 > M&M Food Market 3% $25 > $50 > Metro (Ontario Only), food BASIC$ 3% $25 > $50 > $100 > $250 > Sobeys, Foodland, FreshCo, IGA, Price Chopper, 3% $25 > $50 > $100 > $250 > Safeway Gas Retailer % $ QT $ QT $ QT $ QT $ QT Total $ Esso, Mobil 2% $25 > $50 > $100 > Irving Oil 2% $50 > Petro-Canada™ 2% $25 > $50 > $100 > $500 > Shell 2% $25 > $50 > $100 > $500 > Ultramar 2% $10 > $25 > $50 > $100 > OTHER CATEGORIES Restaurant & Coffee Retailer % $ QT $ QT $ QT $ QT $ QT Total $ A&W 4% $10 > $25 > Abbey’s Bakehouse,Canyon Creek®,Duke’s Refresher® + Bar,Jack Astor’s Bar and Grill®,REDS® Wine Tavern,Scaddabush Italian 5% $25 > $50 > Kitchen & Bar®,The Antler Room,The Loose Moose® Applebee's 4% $25 > $50 > Boston Pizza 5% $25 > $50 > Earls Kitchen + Bar 5% $25 > $50 > JOEY 6% $25 > $50 > Kelseys, Bier Markt, D'Arcy McGee's, East Side Mario's, Fionn MacCool's, Harvey's, milestones, Montana's BBQ & Bar, New York Fries, Paddy 5% $25 > $50 > $100 > Flaherty's, Prime Pubs, State & Main, Swiss Chalet, The Pickle Barrel, The Ultimate Dining Card, Tir Nan Óg Kentucky Fried Chicken,Pizza Hut,Taco Bell 3% $25 > $50 > McDonald’s® 2.5% $15 > $25 > $50 > Moxie's Grill & Bar 10% $25 > $50 > $100 > Pizza Pizza 10% $25 > $100 > $500 > Page 1 / 4 IMPORTANT NOTE : Retailers, rebates and card denominations subject to change without notice. -

Ontario, Canada Featuring Niagara Falls

Ontario, Canada featuring Niagara Falls July 19-30, 2019 Tour Director - Connie VanderPoel 507/530-2294 Driver -Brandon Manley Please note that all times are approximate and everything is subject to change! Courtesy for Fellow Passengers Cell phones: We ask that you turn off your phones and not use them while we are traveling on the bus or involved in a group activity. Using the schedule below, you could plan your calls for free times. Microphone: When the escort or step-on guide is using the microphone, please save your words and conversations until they are done. Often it is difficult to hear in the back of the bus, and people visiting within the group make it just about impossible. Everyone will appreciate this courtesy. DAY 1 FRIDAY, JULY 19, 2019 MARSHALL, MN - DAVENPORT, IA 6:00 Depart Willmar, Southwest Tours, 1308 7th St SE 6:45 Depart Brookings, Super 8 Motel, 3034 LeFevre Drive 7:30 Depart Marshall, Southwest Tour & Travel, 1608 E College Drive (Hwy. 19) 7:45 Depart Sioux Falls, Econo Lodge N 5100 N CLiff Ave. 8:15 Depart Slayton, Prairie Pride Cenex, 3020 20th Street, Hwy. 59 S 8:45 Meeting point Worthington, Old Shopko, 1755 N Humiston Avenue( NE corner of lot) 9:15 - 9:45 Break - Jackson, MN Burger King Restaurant 9:45 - 12:45 Jackson, MN - Charles City, IA 12:45 - 1:45 Lunch - Dave's Restaurant 1:45 - 4:30 Charles City, IA - Davenport, IA 4:30 BW Plus Steeplegate Inn 100 W 76th St, Davenport, IA 52806 . Phone: 563/386-6900 Complimentary full hot breakfast buffet, variety of breakfast items such as: bacon or sausage, eggs, pastries, coffee, tea and juice. -

$ Sacred Heart Catholic School

Sacred Heart Catholic School created on 11/23/2016 NAME TELEPHONE PAYABLE TO NO CHEQUES accepted for this fundraiser. TEACHER PRIMARY EMAIL ADDRESS PARENT/GUARDIAN NAME NOTES ONLINE Payment is available on School Cash Online - please send in paper order form so orders can be verified. Cash Payments will be accepted for this fundraiser. Order Deadline is December 6, 2016 Orders will be ready December 16, 2016 Thank you. Retailer % $ Qty Total Retailer % $ Qty Total THE ESSENTIALS OTHER CATEGORIES GROCERY OTHER RETAILERS food BASIC$,Metro (Ontario Only) 50 American Eagle Outfitters® 6 50 3 100 Bath and Body Works Canada 5 25 Loblaws- Extra Foods, Fortinos, No Frills, Real 50 Best Western 2.5 50 Canadian Superstore, Real Canadian Wholesale Club, Build-A-Bear Workshop 7 25 Valu-Mart, Your Independent Grocer, Zehrs 3 100 250 Cabela's 4 25 Longo's 50 Canadian Tire 4 50 3 100 Chapters - Coles Books, Indigo 5 25 M & M Meat Shops 25 Cineplex - Galaxy, Scotiabank, SilverCity 4 10 3 50 Fairmont Hotels & Resorts - WillowStream 8 100 Sobeys 25 Foot Locker 5 25 Foodland, FreshCo, IGA, Price Chopper, Safeway 3 50 Fruits and Passion 10 25 100 Gap - Baby - Banana Republic, Old Navy 5 50 GAS Giant Tiger 3 25 Esso 25 Home Depot 3 25 2 50 Home Hardware - Home Furniture 3 100 Hudson's Bay - Home Outfitters Irving Oil 2 50 3 50 iTunes Petro-Canada 25 3 25 2 Kernels Popcorn 50 5 15 La Senza - La Senza Express Shell 25 7 25 2 La Vie en Rose - la Vie en Rose aqua 50 8 25 Laura Secord 7 25 Ultramar 25 2 Mark's 7 50 50 Payless Shoe Source 8 25 RESTAURANT & COFFEE