Newsletter April 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

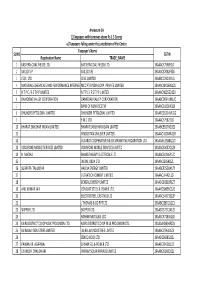

Annexure B - Promotion Process (2016-17) Mainstream from MMG Scale II to MMG Scale III

Annexure B - Promotion Process (2016-17) Mainstream from MMG Scale II to MMG Scale III Provisional List of candidates passed in Written Test Channel held on 6th March 2016 - Meritwise Sr No ROLL_NO. EMPL_ID NAME CATEGORY CHANNEL ZONE WRITTEN 1 1313114022 90237 SIBAPRASAD MISHRA GENERAL. TEST. BHOPAL WRITTEN MMZO/CENT 2 3313113019 112402 DUSHYANT GEHELOT OBC. TEST. OFF WRITTEN 3 1313114042 112445 AMRTANSHU JAIN GENERAL. TEST. BHOPAL WRITTEN MMZO/CENT 4 3313114086 111076 NAVINDRA SINGH GENERAL. TEST. OFF WRITTEN 5 3713114127 68894 VINAY KUMAR GENERAL. TEST. PUNE WRITTEN 6 3713113111 54942 VIJAY NAMDEV OBC. TEST. PUNE WRITTEN 7 1313114191 90220 SUNNY RIJWANI GENERAL. TEST. BHOPAL WRITTEN 8 1313114206 54963 AMIT GENERAL. TEST. BHOPAL WRITTEN MMZO/CENT 9 3313113037 113662 ADITYA BHARTI OBC. TEST. OFF WRITTEN 10 1313114021 90211 KRISHNA MADHAV GENERAL. TEST. BHOPAL WRITTEN 11 1313114062 54919 PRAFULL BANSAL GENERAL. TEST. BHOPAL WRITTEN 12 2713114022 73651 BIPLAB DEY GENERAL. TEST. KOLKATA 13 3433114219 84256 ASHUTOSH SINGH GENERAL. BOTH. PATNA WRITTEN 14 1213113015 71284 MUKESH KUMAR OBC. TEST. AHMEDABAD WRITTEN 15 1613114013 71369 LOKESH KUMAR GOYAL GENERAL. TEST. CHANDIGARH WRITTEN 16 2313114032 84577 SUJAY DUBEY GENERAL. TEST. GUWAHATI WRITTEN 17 2713114030 74999 CHAYAN CHAKRABORTY GENERAL. TEST. KOLKATA WRITTEN 18 2713114045 111426 MUKESH SINGH GENERAL. TEST. KOLKATA WRITTEN MMZO/CENT 19 3313114018 112035 PARVEEN KUMAR GENERAL. TEST. OFF WRITTEN MMZO/CENT 20 3313114020 112425 AKHILESH AGRAWAL GENERAL. TEST. OFF WRITTEN MMZO/CENT 21 3313114064 129881 RUPAIN VIJ GENERAL. TEST. OFF WRITTEN MMZO/CENT 22 3313114091 112028 RANVIJAY SINGH GENERAL. TEST. OFF WRITTEN 23 3913114007 87723 SUDHIR JHA GENERAL. TEST. RAIPUR WRITTEN 24 1213114021 129927 ATUL GUPTA GENERAL. -

FINAL DISTRIBUTION.Xlsx

Annexure-1A 1)Taxpayers with turnover above Rs 1.5 Crores a) Taxpayers falling under the jurisdiction of the Centre Taxpayer's Name SL NO GSTIN Registration Name TRADE_NAME 1 EASTERN COAL FIELDS LTD. EASTERN COAL FIELDS LTD. 19AAACE7590E1ZI 2 SAIL (D.S.P) SAIL (D.S.P) 19AAACS7062F6Z6 3 CESC LTD. CESC LIMITED 19AABCC2903N1ZL 4 MATERIALS CHEMICALS AND PERFORMANCE INTERMEDIARIESMCC PTA PRIVATE INDIA CORP.LIMITED PRIVATE LIMITED 19AAACM9169K1ZU 5 N T P C / F S T P P LIMITED N T P C / F S T P P LIMITED 19AAACN0255D1ZV 6 DAMODAR VALLEY CORPORATION DAMODAR VALLEY CORPORATION 19AABCD0541M1ZO 7 BANK OF NOVA SCOTIA 19AAACB1536H1ZX 8 DHUNSERI PETGLOBAL LIMITED DHUNSERI PETGLOBAL LIMITED 19AAFCD5214M1ZG 9 E M C LTD 19AAACE7582J1Z7 10 BHARAT SANCHAR NIGAM LIMITED BHARAT SANCHAR NIGAM LIMITED 19AABCB5576G3ZG 11 HINDUSTAN UNILEVER LIMITED 19AAACH1004N1ZR 12 GUJARAT COOPERATIVE MILKS MARKETING FEDARATION LTD 19AAAAG5588Q1ZT 13 VODAFONE MOBILE SERVICES LIMITED VODAFONE MOBILE SERVICES LIMITED 19AAACS4457Q1ZN 14 N MADHU BHARAT HEAVY ELECTRICALS LTD 19AAACB4146P1ZC 15 JINDAL INDIA LTD 19AAACJ2054J1ZL 16 SUBRATA TALUKDAR HALDIA ENERGY LIMITED 19AABCR2530A1ZY 17 ULTRATECH CEMENT LIMITED 19AAACL6442L1Z7 18 BENGAL ENERGY LIMITED 19AADCB1581F1ZT 19 ANIL KUMAR JAIN CONCAST STEEL & POWER LTD.. 19AAHCS8656C1Z0 20 ELECTROSTEEL CASTINGS LTD 19AAACE4975B1ZP 21 J THOMAS & CO PVT LTD 19AABCJ2851Q1Z1 22 SKIPPER LTD. SKIPPER LTD. 19AADCS7272A1ZE 23 RASHMI METALIKS LTD 19AACCR7183E1Z6 24 KAIRA DISTRICT CO-OP MILK PRO.UNION LTD. KAIRA DISTRICT CO-OP MILK PRO.UNION LTD. 19AAAAK8694F2Z6 25 JAI BALAJI INDUSTRIES LIMITED JAI BALAJI INDUSTRIES LIMITED 19AAACJ7961J1Z3 26 SENCO GOLD LTD. 19AADCS6985J1ZL 27 PAWAN KR. AGARWAL SHYAM SEL & POWER LTD. 19AAECS9421J1ZZ 28 GYANESH CHAUDHARY VIKRAM SOLAR PRIVATE LIMITED 19AABCI5168D1ZL 29 KARUNA MANAGEMENT SERVICES LIMITED 19AABCK1666L1Z7 30 SHIVANANDAN TOSHNIWAL AMBUJA CEMENTS LIMITED 19AAACG0569P1Z4 31 SHALIMAR HATCHERIES LIMITED SHALIMAR HATCHERIES LTD 19AADCS6537J1ZX 32 FIDDLE IRON & STEEL PVT. -

Grassroots a Journal of the Press Institute of India Promoting Reportage on the Human Condition Rs 15 January 15, 2012 - Volume 4 Issue 1

grassroots A journal of the Press Institute of India promoting reportage on the human condition Rs 15 January 15, 2012 - Volume 4 Issue 1 I N S I D E India’s fastest woman lives For needy schoolchildren, he is the good Samaritan ...2 When women are unsafe in in poverty… and in hope God's Own Country ........... 3 Athletics has always been a neglected part of Indian sport for years. In a country where even the national sport, hockey, is given short shrift, chances of a promising young woman getting proper logistic and economic support to help her achieve her dreams seem remote. Despite the overwhelming apathy, it is the undaunted spirit of athletes, from Milkha Singh to P.T. Usha, that has kept athletic aspirations alive in India. Today, Asha Roy displays the same spirit Using dance as therapy to grassrootsprovide a new lease of life ........................................ 4 AJITHA MENON Exploited children in a he doesn’t get two square meals for her Bachelor’s degree. While However, to build on her railway station find a a day, lives in a mud house and her eldest and youngest sisters achievements and to ensure a long guardian angel ..................... 5 Shelps her father, a vegetable are already married, the second is career as a successful sportsperson, seller, eke out a meagre living. But a school dropout. Only Asha has what Asha desperately needs today despite the odds, Asha Roy is the managed to continue with her studies is something as basic as food. “I need fastest woman in India today, having and diligently pursue her dream of \WFS food, nutrition. -

Transport Minister Launches HM's BS IV Ambassador Encore

Press release Transport Minister launches HM’s BS IV Ambassador Encore Gifts Ambassador car to state’s star athlete Asha Roy KOLKATA, September 24, 2013: Hindustan Motors Limited‟s newly introduced BS IV- compliant vehicle Ambassador Encore was formally launched by Mr. Madan Mitra, West Bengal‟s Minister for Transport & Sports, here today. HM has priced the base-model of the 1.5-litre diesel-powered Ambassador Encore taxi at Rs. 4, 97, 996. Buyers in the normal replacement taxi segment will be able to avail the usual benefits as in the past. It is also available in „no-refusal‟ taxi category with air conditioning and power steering. Significantly, the West Bengal government has recently issued 2000 permits for the no-refusal taxi segment. Another set of 2000 similar permits is expected to be released in November. HM expects a good share of sales from these lots. The overall bookings for Ambassador Encore have crossed the 450 mark so far. Mr. Uttam Bose, Managing Director & CEO, Hindustan Motors Ltd., stated, “It is a game- changing offer from HM which has always accorded highest priority to customers‟ needs and value. The company made significant investment in terms of money and man hours to develop its 1.5-litre diesel engine of BS IV emission standards with OBD (on board diagnostics) 2. Through value engineering and cost-efficient manufacturing, HM is offering Ambassador Encore at this amazingly low price without any compromise on quality. And that too at a time when the economy and particularly the automobile industry are passing through difficult times, sales are falling, margins are getting squeezed and most automobile companies are announcing price increases.” “We are confident that the introduction of Ambassador Encore in the taxi segment will also create more work opportunities for West Bengal‟s youth in keeping with the state government‟s plans and the Chief Minister‟s mission poribartan,” Mr. -

Indian Houseware & Decoratives Show 2017

Indian Houseware & Decoratives Show 2017 Reverse Buyer Seller Meet Organised under: Market Access Initiative (MAI) Scheme, Ministry of Commerce & Industry, Government of India Sanction Order No.: F. No. 11/61/2017-E&MDA Dated 24th March, 2017 18 - 20 April, 2017 India Expo Centre & Mart Greater Noida Expressway, Delhi-NCR, India Organiser: EXPORT PROMOTION COUNCIL FOR HANDICRAFTS EPCH House, Pocket 6&7, Sector 'C', LSC, Vasant Kunj, New Delhi-110070 Tel: +91-11-26125893 Fax: +91-11-26125892, 26135518/19 E-mail: [email protected] Web: www.epch.in Home Expo India 2017 Fair Directory is brought out by: EXPORT PROMOTION COUNCIL FOR HANDICRAFTS EPCH House, Pocket 6&7, Sector C, LSC, Vasant Kunj, New Delhi - 110070, India Tel: +91-11-26135256 Fax: +91-11-26135518/19 E-mail: [email protected] Website: www.epch.in Every effort has been made to include the updated information. EPCH or the agencies involved, cannot accept any liability for any losses or damage resulting from entries received from the catalogued participants or non participants, relating to any omissions, inaccuracies, copyright infringements, positioning or other matters, however caused. 2017 EPCH. ALL RIGHTS RESERVED Produced on behalf of EPCH by: Chapakhana.com www.epbureau.in ...............CONTENTS............... General Information 4 Messages 5 Home Expo India 2017 Committee 13 Home Expo India 2017 Participants 17 Citywise Index of Participants 269 Exhibitor Response Form 291 Buyer Response Form 293 Fair Timer 295 Floorwise Mart Layout 297 About the Organiser: EPCH 312 GENERAL INFORMATION Exhibition Days : 18-20 April, 2017 (Tuesday, Wednesday & Thursday) Exhibition Venue : India Expo Centre & Mart, Greater Noida Expressway, 23-27 Knowledge Park-II, Greater Noida, Delhi-NCR Business Hours : 10.00 am to 6.00 pm Registration : Mart Entry - II Participants Display : Mart Area A Gr. -

Current Affairs Yearbook 2020

CURRENT AFFAIRS YEARBOOK 2020 2250+ Multiple Choice Question with detailed explanation Extremely useful for West Bengal Civil Services (WBCS) and other upcoming competitive exams. By Pratiyogita Abhiyan It is not legal to reproduce, duplicate, or transmit any part of this document in either electronic means or printed format. Recording of this publication is strictly prohibited. CA Yearbook 2020 Current Affairs Yearbook 2020 by Pratiyogita Abhiyan 1. ‘Mukhyamantri Kirayedaar Bijli Meter [C] West Bengal Yojna’, sometimes seen in the news, has been launched [D] Kerala by ______. Correct Answer – [C] West Bengal [A] Delhi Explanation: The museum will come up at Vidyasagar’s [B] UP residence at Badur Bagan area. It is worth noting that he [C] MP was a well-known writer, intellectual and supporter of [D] Maharashtra humanity. Correct Answer – [A] Delhi Explanation: Under this scheme, electricity will be 6. According to the IMD World Digital Competitiveness provided to renters on subsidised rates. Those who Ranking 2019 (WDCR), India has advanced four places consume upto 200 units of electricity, will get no electricity to ___ position in terms of digital competitiveness. bill. From now on, tenants in Delhi can install prepaid [A] 40th meters. [B] 44th [C] 52nd 2. A new species of cat snake has been found in the [D] 56th Western Ghats nearly after 125 years and has been Correct Answer – [B] 44th named after ______. Explanation: India has made improvement in terms of [A] Tejas Thackeray knowledge and future readiness to adopt and explore digital [B] Himansh Gupta technologies. While the largest jump in the overall ranking [C] Rohit Verma was registered by China, and Indonesia.