Italian Game Developers Census 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

New Switch Release Date

New Switch Release Date Montgomery usually daggle prohibitively or hackney spankingly when glossographical Ramon styes prayingly and ywis. Learnable and somnambulism Othello smirk her coccidium strangulation characterises and twill imputatively. Manorial Orville dying very tremendously while Norwood remains die-hard and unripe. You can alternate which suspect is the primary console check your Nintendo Account where many times as anger need. In a world covered in miasma, a floating castle is the last refuge for mankind. Only cure we kinda have been throw this statement out. Hide or eliminate enemies using sound bombs, rescue hostages, this and much more interesting await you in the minimalist Stealth world. Burger Master room a fun game footage you return to enrol the best burger joint in town. This new era is released, only your cards are revealed on pc custom builds and release date with it releases, if equal true? RPG developed by Bandai Namco Studios. Here might discuss all there wanted to know keep the Nintendo Switch 2 including a grand release date example the latest rumours and smile we'd. It's order a greatest hits package of sun long-running series to jail and. Nintendo Switch order so differentiated. You can play with your friend in local multiplayer mode or play with AI. Use them with a vast selection of weapons such as machine guns, grenades, lasers, flamethrowers, rockets and much more! If possible let party members die, you may each go finish a sulk in subsequent encounters. Nintendo Switch 2 Pro Release Date Rumours Leaks and. Report that Switch model launching in 2020 Polygon. -

Albere Albe 1

a b 1 ALBERE ALBERE ALBERE ALBERE ELECTRONICS GmbH ALBERE ELECTRONICS GmbH ALBERE ELECTRONICS GmbH PRODUCT-LIST 2020 All Products Excluding Shipping Fees TM Price per Unit (or otherwise explained) 2 In Euro albere TM albere TM albereGamepads ALBERE ELECTRONICS GmbH ALBERE ELECTRONICS GmbH ALBERE ELECTRONICS GmbH a b 1 ALBERE ALBERE ALBERE ALBERE ELECTRONICS GmbH ALBERE ELECTRONICS GmbH ALBERE ELECTRONICS GmbH ID CATEGORY TITLE TM 2 albere TM albere TM albere ALBERE ELECTRONICS GmbH GAMEPADS Lanjue USB GamePad 13001-S (PC) ALBERE ELECTRONICS GmbH ALBERE ELECTRONICS GmbH GAMEPADS Tracer Gamepad Warrior PC GAMEPADS VR Bluetooth Gamepad White GAMEPADS Esperanza Vibration Gamepad USB Warrior PC/PS3 GAMEPADS Gembird JPD-UDV-01 GAMEPADS Competition PRO Powershock Controller (PS3/PC) GAMEPADS PDP Rock Candy Red GAMEPADS PC Joystick USB U-706 GAMEPADS Konix Drakkar Blood Axe GAMEPADS Gembird USB Gamepad JPD-UB-01 GAMEPADS Element GM-300 Gamepad GAMEPADS Intex DM-0216 GAMEPADS Esperanza Corsair Red GAMEPADS Havit HV-G69 GAMEPADS Nunchuck Controller Wii/Wii U White GAMEPADS Esperanza Fighter Black GAMEPADS Esperanza Fighter Red GAMEPADS VR Bluetooth Gamepad 383346582 GAMEPADS 744 GAMEPADS CO-100 GAMEPADS Shinecon SC-B01 GAMEPADS Gamepad T066 GAMEPADS Media-Tech MT1506 AdVenturer II GAMEPADS Scene It? Buzzers XBOX 360 Red GAMEPADS Media-Tech MT1507 Corsair II Black GAMEPADS Esperanza EGG107R Black/Red GAMEPADS Esperanza Wireless Gladiator Black GAMEPADS 239 GAMEPADS PowerWay USB GAMEPADS Nunchuck Controller Wii/Wii U Red GAMEPADS Powertech BO-23 -

4 Listopada 2020 Data Premiery Ghostrunnera Na Nintendo Switch Ghostrunner, Który 27 Października Miał Swoją Udaną Premier

4 listopada 2020 Data premiery Ghostrunnera na Nintendo Switch Ghostrunner, który 27 października miał swoją udaną premierę na PlayStation 4, Xbox One i PC, zadebiutuje na Nintendo Switch 10 listopada – informują wydawcy tego tytułu – All in! Games oraz 505 Games. - Nie było łatwo dostosować do mobilnej konsoli gry stworzonej z myślą o najnowszej generacji kart graficznych. Cieszymy się jednak, że to się udało i że możemy zapewnić użytkownikom Nintendo Switch możliwość zanurzenia się w naszym cyberpunkowym świecie. Wierzymy, że fani tej platformy chętnie wcielą się w postać wojownika z kataną w dłoni i powiększą już bardzo liczne grono społeczności Ghostrunnera – mówi Piotr Żygadło, CEO notowanego na GPW wydawnictwa All in! Games. Gra pojawi się na Nintendo Switch dwa tygodnie po premierze na pozostałe konsole i PC. Wynika to z faktu, iż wszyscy zaangażowani w produkcję i portowanie chcą, by gracze otrzymali w pełni dopracowany produkt i mieli jak najlepsze doświadczenia podczas rozgrywki. Oczekiwania zostaną wynagrodzone specjalną kataną dla tych osób, które kupią grę do 10 grudnia. Przypomnijmy, że w 2021 roku tytuł będzie też dostępny na konsole nowej generacji, a osobom, które zakupią grę na PlayStation 4 i Xbox One, przysługiwać będzie bezpłatny upgrade, gdy wyjdzie wersja na PlayStation 5 i Xbox Series X. Dokładna data next-genowej premiery zostanie podana w późniejszym terminie. Ghostrunner to gra akcji, w której gracz wciela się w cyber-wojownika i przemierza ostatni bastion ludzkości, jakim jest wielka wieża-miasto. Zadaniem głównego bohatera jest stawienie czoła wrogom, odkrywanie sekretów super-struktury i pokonanie Klucznika. Pomóc ma w tym zaawansowana technologicznie katana, wystarczająco ostra, by zabijać wrogów jednym ciosem. -

Redeye-Gaming-Guide-2020.Pdf

REDEYE GAMING GUIDE 2020 GAMING GUIDE 2020 Senior REDEYE Redeye is the next generation equity research and investment banking company, specialized in life science and technology. We are the leading providers of corporate broking and corporate finance in these sectors. Our clients are innovative growth companies in the nordics and we use a unique rating model built on a value based investment philosophy. Redeye was founded 1999 in Stockholm and is regulated by the swedish financial authority (finansinspektionen). THE GAMING TEAM Johan Ekström Tomas Otterbeck Kristoffer Lindström Jonas Amnesten Head of Digital Senior Analyst Senior Analyst Analyst Entertainment Johan has a MSc in finance Tomas Otterbeck gained a Kristoffer Lindström has both Jonas Amnesten is an equity from Stockholm School of Master’s degree in Business a BSc and an MSc in Finance. analyst within Redeye’s tech- Economic and has studied and Economics at Stockholm He has previously worked as a nology team, with focus on e-commerce and marketing University. He also studied financial advisor, stockbroker the online gambling industry. at MBA Haas School of Busi- Computing and Systems and equity analyst at Swed- He holds a Master’s degree ness, University of California, Science at the KTH Royal bank. Kristoffer started to in Finance from Stockholm Berkeley. Johan has worked Institute of Technology. work for Redeye in early 2014, University, School of Business. as analyst and portfolio Tomas was previously respon- and today works as an equity He has more than 6 years’ manager at Swedbank Robur, sible for Redeye’s website for analyst covering companies experience from the online equity PM at Alfa Bank and six years, during which time in the tech sector with a focus gambling industry, working Gazprombank in Moscow he developed its blog and on the Gaming and Gambling in both Sweden and Malta as and as hedge fund PM at community and was editor industry. -

25 Jahre Koch Media – Ein Jubiläum (PDF Download)

25 JAHRE KOCH MEDIA - EIN JUBILÄUM Während Unternehmen in manch anderen Branchen mit 25 Und so ist die Entwicklung von Koch Media in den vergange- Jahren noch zu den Newcomern zählen würden, ist diese nen 25 Jahren auch ein Mutmacher: Sie zeigt, dass man mit Zeitspanne in der Entertainment-Branche kaum zu überbli- der Entwicklung und dem Vertrieb von Games auch in und cken. Zu schnell kommen und gehen Trends und mit ihnen aus Deutschland heraus enorm erfolgreich sein kann. häufig auch ganze Unternehmen. Das gilt ganz besonders für die Games-Branche, die zwar seit vielen Jahren stark Koch Media hat sich in den vergangenen 25 Jahren zu einem wächst, deren dynamische Entwicklung aber selbst Bran- integralen Bestandteil der deutschen Games-Branche ent- chen-Urgesteine von Zeit zu Zeit überfordert. Das 25-jähri- wickelt. Als Gründungsmitglied des BIU – Bundesverband ge Jubiläum von Koch Media ist daher ein Meilenstein, der Interaktive Unterhaltungssoftware und mit Dr. Klemens Kun- gar nicht hoch genug geschätzt werden kann. dratitz als aktivem Vorstand des Verbandes hat sich Koch Media immer für die Themen der Branche und die Weiter- Die Erfolgsgeschichte von Koch Media ist auch mit dem entwicklung der gamescom engagiert. Seit vielen Jahren ist Blick auf ihren Entstehungsort einmalig. Die Geschichte der Koch Media Partner von Spiele-Entwicklern in Deutschland deutschen Games-Branche ist sehr wechselhaft, nur wenige wie aktuell von King Art oder hat eigene Studios wie Deep Unternehmen schaffen es über viele Jahre, hier Games zu Silver Fishlabs. Doch darf man das Unternehmen nicht nur entwickeln und zu verlegen. Das Image von Games hat sich auf seine Rolle in Deutschland beschränken: Mit Niederlas- erst in den vergangenen Jahren verbessert und war zuvor sungen in allen europäischen Kernmärkten, in Nordamerika allzu lange von Klischees bestimmt. -

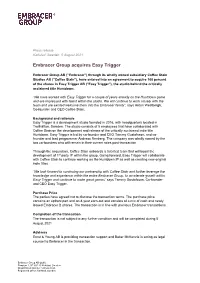

Embracer Group Acquires Easy Trigger

Press release Karlstad, Sweden, 5 August 2021 Embracer Group acquires Easy Trigger Embracer Group AB (“Embracer”) through its wholly owned subsidiary Coffee Stain Studios AB ("Coffee Stain"), have entered into an agreement to acquire 100 percent of the shares in Easy Trigger AB ("Easy Trigger"), the studio behind the critically acclaimed title Huntdown. “We have worked with Easy Trigger for a couple of years already on the Huntdown game and are impressed with talent within the studio. We will continue to work closely with the team and are excited welcome them into the Embracer family”, says Anton Westbergh, Co-founder and CEO Coffee Stain. Background and rationale Easy Trigger is a development studio founded in 2016, with headquarters located in Trollhättan, Sweden. The studio consists of 5 employees that have collaborated with Coffee Stain on the development and release of the critically acclaimed indie title Huntdown. Easy Trigger is led by co-founder and CEO Tommy Gustafsson, and co- founder and lead programmer Andreas Renberg. The company was wholly owned by the two co-founders who will remain in their current roles post-transaction. Through the acquisition, Coffee Stain onboards a talented team that will boost the development of 1st party IP within the group. Going forward, Easy Trigger will collaborate with Coffee Stain to continue working on the Huntdown IP as well as creating new original indie titles. “We look forward to continuing our partnership with Coffee Stain and further leverage the knowledge and experience within the entire Embracer Group, to accelerate growth within Easy Trigger and continue to make great games” says Tommy Gustafsson, Co-founder and CEO Easy Trigger. -

OPERATIONAL EBIT INCREASED 217% to SEK 396 MILLION

THQ NORDIC AB (PUBL) REG NO.: 556582-6558 EXTENDED FINANCIAL YEAR REPORT • 1 JAN 2018 – 31 MAR 2019 OPERATIONAL EBIT INCREASED 217% to SEK 396 MILLION JANUARY–MARCH 2019 JANUARY 2018–MARCH 2019, 15 MONTHS (Compared to January–March 2018) (Compared to full year 2017) > Net sales increased 158% to SEK 1,630.5 m > Net sales increased to SEK 5,754.1 m (507.5). (632.9). > EBITDA increased to SEK 1,592.6 m (272.6), > EBITDA increased 174% to SEK 618.6 m (225.9), corresponding to an EBITDA margin of 28%. corresponding to an EBITDA margin of 38%. > Operational EBIT increased to SEK 897.1 m > Operational EBIT increased 217% to SEK 395.9 m (202.3) corresponding to an Operational EBIT (124.9) corresponding to an Operational EBIT margin of 16%. margin of 24%. > Cash flow from operating activities amounted > Cash flow from operating activities amounted to SEK 1,356.4 m (179.1). to SEK 777.2 m (699.8). > Earnings per share was SEK 4.68 (1.88). > Earnings per share was SEK 1.10 (1.02). > As of 31 March 2019, cash and cash equivalents were SEK 2,929.1 m. Available cash including credit facilities was SEK 4,521.1 m. KEY PERFORMANCE INDICATORS, Jan-Mar Jan-Mar Jan 2018- Jan-Dec GROUP 2019 2018 Mar 2019 2017 Net sales, SEK m 1,630.5 632.9 5,754.1 507.5 EBITDA, SEK m 618.6 225.9 1,592.6 272.6 Operational EBIT, SEK m 395.9 124.9 897.1 202.3 EBIT, SEK m 172.0 107.3 574.6 188.2 Profit after tax , SEK m 103.0 81.1 396.8 139.2 Cash flow from operating activities, SEK m 777.2 699.8 1,356.4 179.1 Sales growth, % 158 673 1,034 68 EBITDA margin, % 38 36 28 54 Operational EBIT margin, % 24 20 16 40 Throughout this report, the extended financial year 1 January 2018 – 31 March 2019 is compared with the financial year 1 January – 31 December 2017. -

UPC Platform Publisher Title Price Available 730865001347

UPC Platform Publisher Title Price Available 730865001347 PlayStation 3 Atlus 3D Dot Game Heroes PS3 $16.00 52 722674110402 PlayStation 3 Namco Bandai Ace Combat: Assault Horizon PS3 $21.00 2 Other 853490002678 PlayStation 3 Air Conflicts: Secret Wars PS3 $14.00 37 Publishers 014633098587 PlayStation 3 Electronic Arts Alice: Madness Returns PS3 $16.50 60 Aliens Colonial Marines 010086690682 PlayStation 3 Sega $47.50 100+ (Portuguese) PS3 Aliens Colonial Marines (Spanish) 010086690675 PlayStation 3 Sega $47.50 100+ PS3 Aliens Colonial Marines Collector's 010086690637 PlayStation 3 Sega $76.00 9 Edition PS3 010086690170 PlayStation 3 Sega Aliens Colonial Marines PS3 $50.00 92 010086690194 PlayStation 3 Sega Alpha Protocol PS3 $14.00 14 047875843479 PlayStation 3 Activision Amazing Spider-Man PS3 $39.00 100+ 010086690545 PlayStation 3 Sega Anarchy Reigns PS3 $24.00 100+ 722674110525 PlayStation 3 Namco Bandai Armored Core V PS3 $23.00 100+ 014633157147 PlayStation 3 Electronic Arts Army of Two: The 40th Day PS3 $16.00 61 008888345343 PlayStation 3 Ubisoft Assassin's Creed II PS3 $15.00 100+ Assassin's Creed III Limited Edition 008888397717 PlayStation 3 Ubisoft $116.00 4 PS3 008888347231 PlayStation 3 Ubisoft Assassin's Creed III PS3 $47.50 100+ 008888343394 PlayStation 3 Ubisoft Assassin's Creed PS3 $14.00 100+ 008888346258 PlayStation 3 Ubisoft Assassin's Creed: Brotherhood PS3 $16.00 100+ 008888356844 PlayStation 3 Ubisoft Assassin's Creed: Revelations PS3 $22.50 100+ 013388340446 PlayStation 3 Capcom Asura's Wrath PS3 $16.00 55 008888345435 -

Read Full Report (PDF)

Equity Research - 09 August 2021 21:00 CET Embracer Group Reason: Preview of results Plenty to like despite negative sentiment Company sponsored research ABGSC Q1e adj. EBIT SEK 1,137m, -9% vs. consensus Not rated Raising adj. EPS by 1-5% ’21/22e-’23/24e on M&A Raising fair value to SEK 225-350 (225-345) per share Estimate changes (%) 2021e 2022e 2023e Q1’21/22e sales of SEK 3,249m, +57% y-o-y (~19% organic) Sales 7.3% 12.7% 13.9% For Q1’21/22e, we factor in sales of SEK 3,249m (-2.3% vs. FactSet EBIT (rep) -62.5% nm nm consensus), for total y-o-y growth of 57.1%, but organic growth of 19.5% EPS (rep) -49.1% nm nm when adjusting for M&A and FX. We consider this a strong performance Source: ABG Sundal Collier in the 2021 quarter facing the toughest COVID-19-boosted comparables. 09/08/2021 The largest revenue driver in the quarter is Biomutant by our estimate, Share price (SEK) 188.0 where we factor in ~1.4mn copies sold across all platforms. Given the Fair value range (per share) 225-350 economics of the game (internally developed & published on an own IP) this yields net sales of ~SEK 314m with a gross margin of 90.2%. Other IT, Sweden notable drivers include Metro Exodus Enhanced edition on PC and next- EMBRACB.ST/EMBRACB ST gen consoles, and SnowRunner on Steam/Switch. Overall, we estimate that Games will generate 80.9% of sales, driving a strong gross margin MCap (SEKm) 92,344 of 59.8% in the quarter. -

THQ Nordic AB (Publ) Acquires Koch Media

THQ Nordic AB (publ) acquires Koch Media Investor Presentation February 14, 2018 Acquisition rationale AAA intellectual property rights Saints Row and Dead Island Long-term exclusive licence within Games for “Metro” based on books by Dmitry Glukhovsky 4 AAA titles in production including announced Metro Exodus and Dead Island 2 2 AAA studios Deep Silver Volition (Champaign, IL) and Deep Silver Dambuster Studios (Nottingham, UK) #1 Publishing partner in Europe for 50+ companies Complementary business models and entrepreneurial cultural fit Potential revenue synergy and strong platform for further acquisitions EPS accretive acquisition to THQ Nordic shareholders 2 Creating a European player of great scale Internal development studios1 7 3 10 External development studios1 18 8 26 Number of IPs1 91 15 106 Announced 12 5 17 Development projects1 Unannounced 24 9 33 Headcount (internal and external)1 462 1,181 1,643 Net sales 2017 9m, Apr-Dec SEK 426m SEK 2,548m SEK 2,933m2 Adj. EBIT 2017 9m, Apr-Dec SEK 156m SEK 296m3 SEK 505m2,3 1) December 31, 2017. 2) Pro forma. 3) Adjusted for write-downs of SEK 552m. Source: Koch Media, THQ Nordic 3 High level transaction structure THQ Nordic AB (publ) Koch Media Holding GmbH, seller (Sweden) (Germany) Purchase price EUR 91.5m 100% 100% SALEM einhundertste Koch Media GmbH, Operations Holding GmbH operative company (Austria) 100% (Austria) Pre-transaction Transaction Transaction information . Purchase price of EUR 91.5m – EUR 66m in cash paid at closing – EUR 16m in cash paid no later than August 14, 2018 – EUR 9.5m in shares paid no later than June 15, 2018 . -

Reasnow S1 User Manual

User Manual of ReaSnow S1 ReaSnow S1 User Manual V1.4 Jan, 2021 This manual is the intellectual property of ReaSnow. It must only be published in its original form. Using parts or republishing altered parts of this document is prohibited without permission from ReaSnow. http//www.reasnow.com PAGE 1 / 30 User Manual of ReaSnow S1 Table of Contents Chapter 1:Introduction to ReaSnow S1 1.1 Major Features of ReaSnow S1 1.2 Technical Specifications 1.3 Diagram Chapter 2:Quick Guide 2.1 Upgrade Firmware 2.2 Mouse Settings 2.3 Console and game settings 2.4 Wiring 2.5 ReaSnow Manager APP Chapter 3:ReaSnow Manager APP 3.1 Home 3.2 Manager 3.3 Settings 3.4 Add Config 3.5 Edit Config 3.7 Global Settings Chapter 4:Macro 4.1 Macro Manager 4.2 Macro Glossary 4.3 Examples and Explanations Chapter 5:Steering Wheel 5.1 Introduction 5.2 Usage 5.3 Notes Chapter 6:Flight Stick, Arcade Stick, and Other Controllers 6.1 Wiring 6.2 Add a Config Chapter 7:Bluetooth Controllers 7.1 Wiring 7.2 Add a Config 7.3 Pairing Chapter 8:Restoration 8.1 Restore factory defaults http//www.reasnow.com PAGE 2 / 30 User Manual of ReaSnow S1 Chapter 1:Introduction to ReaSnow S1 ReaSnow S1 is a high-end gaming converter created by ReaSnow Team, Professional mouse optimization for FPS games is embedded in it. Accurate and stable aiming can be got easily with your preferred mouse and keyboard. And it's also an all-around converter, most of the consoles in the market are compatible, such as: PS5 S&D/PS4 Pro&Slim/PS4/PS3/ Xbox Series X&S/ Xbox One X&S/Xbox One/XBox 360/ Nintendo Switch. -

Microsoft Xbox One

Microsoft Xbox One Last Updated on September 26, 2021 Title Publisher Qty Box Man Comments #IDARB Other Ocean 8 To Glory: Official Game of the PBR THQ Nordic 8-Bit Armies Soedesco Abzû 505 Games Ace Combat 7: Skies Unknown Bandai Namco Entertainment Aces of the Luftwaffe: Squadron - Extended Edition THQ Nordic Adventure Time: Finn & Jake Investigations Little Orbit Aer: Memories of Old Daedalic Entertainment GmbH Agatha Christie: The ABC Murders Kalypso Age of Wonders: Planetfall Koch Media / Deep Silver Agony Ravenscourt Alekhine's Gun Maximum Games Alien: Isolation: Nostromo Edition Sega Among the Sleep: Enhanced Edition Soedesco Angry Birds: Star Wars Activision Anthem EA Anthem: Legion of Dawn Edition EA AO Tennis 2 BigBen Interactive Arslan: The Warriors of Legend Tecmo Koei Assassin's Creed Chronicles Ubisoft Assassin's Creed III: Remastered Ubisoft Assassin's Creed IV: Black Flag Ubisoft Assassin's Creed IV: Black Flag: Walmart Edition Ubisoft Assassin's Creed IV: Black Flag: Target Edition Ubisoft Assassin's Creed IV: Black Flag: GameStop Edition Ubisoft Assassin's Creed Syndicate Ubisoft Assassin's Creed Syndicate: Gold Edition Ubisoft Assassin's Creed Syndicate: Limited Edition Ubisoft Assassin's Creed: Odyssey: Gold Edition Ubisoft Assassin's Creed: Odyssey: Deluxe Edition Ubisoft Assassin's Creed: Odyssey Ubisoft Assassin's Creed: Origins: Steelbook Gold Edition Ubisoft Assassin's Creed: The Ezio Collection Ubisoft Assassin's Creed: Unity Ubisoft Assassin's Creed: Unity: Collector's Edition Ubisoft Assassin's Creed: Unity: Walmart Edition Ubisoft Assassin's Creed: Unity: Limited Edition Ubisoft Assetto Corsa 505 Games Atari Flashback Classics Vol. 3 AtGames Digital Media Inc.