Service Provider Intelligence Analysis Launches

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Robinhood, Reddit, Gamestop, and You | 2X Wealth Group to the Sophisticated Goliaths Who Were Short These Stocks

February 3, 2020 | 2X Wealth Group With a combined 50+ years of experience, Robinhood, Reddit, GameStop, 2X Wealth Group is committed to educating and You and empowering investors. We firmly believe financial The Making of a Financial Flash Mob literacy helps people make better decisions. Who doesn’t love the story of David’s triumph over Goliath? This past week a group of “small” investors made tremendous amounts of money (on paper at least) by buying stocks that were heavily shorted by large, sophisticated hedge funds. We explore what happened, factors that spurred the market disruption, the subsequent fallout still unfolding, and finally, what it all means going forward. What Happened? First, it’s important to understand three concepts - short selling, call options, and a short squeeze. If an investor wants to profit from a stock declining in value, they can short the stock. Most understand the concept of buying stock, but shorting is more complicated. Shorting involves selling a stock that you don’t own. So, how do you sell something that you don’t own? The answer is - you borrow the stock through your brokerage firm, and you must put up money to do so. The broker requires that you maintain a balance large enough to repurchase the borrowed stock at any time. Therein lies the risk. If you buy a stock, the most you can lose is the amount you paid. In other words, the value of your investment can only go to zero. If you short a stock, however, there is no limit to the amount you can lose. -

Hedge Fund Spotlight

Welcome to the latest edition of Hedge Fund Spotlight, the monthly Hedge Fund Spotlight newsletter from Preqin providing insights into the hedge fund industry, May 2015 including information on investors, funds, performance and more. Hedge Fund Spotlight uses information from our online product Hedge Fund The $1bn Club Online, which includes Hedge Fund Investor Profi les and Hedge Fund Analyst. Largest Hedge Fund Managers In this month’s feature article, we take a look at the ‘$1bn Club’, a group of the world’s largest May 2015 hedge fund managers, and identify the traits and characteristics that are unique to this Volume 7 - Issue 4 distinguished group which controls a vast proportion of industry capital. Page 2 FEATURED PUBLICATION: Largest Investors in Hedge Funds The 2015 Preqin Sovereign Following on from our feature article, we take an in-depth look at the ‘$1bn Club’ of institutional Wealth Fund Review investors allocating at least $1bn to hedge funds, including the signifi cance of this group, investment preferences and new entrants to the Club. Page 5 The 2015 Preqin Industry News Preqin Sovereign Wealth Fund Review Following the UK general election in May, we take a look at the hedge fund industry in the UK. Page 8 In association with: alternative assets. intelligent data More from Preqin: Hedge Fund Research See what’s new from Preqin this month in the hedge fund universe. Page 9 To find out more, download sample pages or to purchase your copy, please visit: Preqin Investor Network www.preqin.com/swf We examine the activity of the investors on Preqin Investor Network to see which fund types, strategies and regions are of current interest to investors, as well as which institutional investor types have been proactively looking at funds in April. -

Individual Investors Rout Hedge Funds

P2JW028000-5-A00100-17FFFF5178F ***** THURSDAY,JANUARY28, 2021 ~VOL. CCLXXVII NO.22 WSJ.com HHHH $4.00 DJIA 30303.17 g 633.87 2.0% NASDAQ 13270.60 g 2.6% STOXX 600 402.98 g 1.2% 10-YR. TREAS. À 7/32 , yield 1.014% OIL $52.85 À $0.24 GOLD $1,844.90 g $5.80 EURO $1.2114 YEN 104.09 What’s Individual InvestorsRout HedgeFunds Shares of GameStop and 1,641.9% GameStop Thepowerdynamics are than that of DeltaAir Lines News shifting on Wall Street. Indi- Inc. AMC have soared this week Wednesday’stotal dollar vidual investorsare winning While the individuals are trading volume,$28.7B, as investors piled into big—at least fornow—and rel- rejoicing at newfound riches, Business&Finance exceeded the topfive ishing it. the pros arereeling from their momentum trades with companies by market losses.Long-held strategies capitalization. volume rivaling that of giant By Gunjan Banerji, such as evaluatingcompany neye-popping rally in Juliet Chung fundamentals have gone out Ashares of companies tech companies. In many $25billion and Caitlin McCabe thewindowinfavor of mo- that were onceleftfor dead, cases, the froth has been a mentum. War has broken out including GameStop, AMC An eye-popping rally in between professionals losing and BlackBerry, has upended result of individual investors Tesla’s 10-day shares of companies that were billions and the individual in- the natural order between defying hedge funds that have trading average onceleftfor dead including vestorsjeering at them on so- hedge-fund investorsand $24.3 billion GameStopCorp., AMC Enter- cial media. -

YOLO Trading: Riding with the Herd During the Gamestop Episode

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Lyócsa, Štefan; Baumöhl, Eduard; Vŷrost, Tomáš Working Paper YOLO trading: Riding with the herd during the GameStop episode Suggested Citation: Lyócsa, Štefan; Baumöhl, Eduard; Vŷrost, Tomáš (2021) : YOLO trading: Riding with the herd during the GameStop episode, ZBW - Leibniz Information Centre for Economics, Kiel, Hamburg This Version is available at: http://hdl.handle.net/10419/230679 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2018 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ____________ to ____________ Commission file number 001-09148 THE BRINK’S COMPANY (Exact name of registrant as specified in its charter) Virginia 54-1317776 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) P.O. Box 18100, 1801 Bayberry Court Richmond, Virginia 23226-8100 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code (804) 289-9600 Securities registered pursuant to Section 12(b) of the Act: Name of each exchange on Title of each class which registered The Brink’s Company Common Stock, Par Value $1 New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

After the Storm: Unmasking Publicly-Traded, Private Equity Firms to Create Value Through Shareholder Democracy

10 10 GOMBERG.DOCX 3/18/2010 5:03 PM AFTER THE STORM: UNMASKING PUBLICLY-TRADED, PRIVATE EQUITY FIRMS TO CREATE VALUE THROUGH SHAREHOLDER DEMOCRACY Trevor M. Gomberg* I. INTRODUCTION On June 21, 2007, The Blackstone Group L.P. (“Blackstone”), a prominent private equity firm, conducted its initial public offering (“IPO”) of 133.3 million shares of “common units representing limited partner interests,” raising $4.133 billion from public investors.1 Within two weeks of Blackstone’s IPO, Kohlberg, Kravis, Roberts & Co. L.P. (“KKR”), another reputable private equity firm, filed a registration statement with the U.S. Securities and Exchange Commission (“SEC”), intending to raise cash from the public markets.2 Investment banks and journalists reacted in an overwhelmingly positive way to Blackstone’s IPO. Wall Street analysts “positively gushed” over the prospect of Blackstone trading publicly; the strength of its portfolio holdings makes the firm a great investment.3 “Wall Street firms rushed in to advise investors to buy, buy, buy . [as] most of the underwriters came out with positive ratings.”4 Analysts in particular noted Blackstone’s ability to remain profitable even during down markets.5 With a stellar reputation and analyst praise, the IPO may have a far-reaching impact on an industry thrust in the spotlight. * J.D. 2009, cum laude, Albany Law School. I would like to thank Clinical Professor Christine Sgarlata Chung for her resourcefulness and guidance. 1 Press Release, The Blackstone Group, The Blackstone Group Prices $4.133 Billion Initial Public Offering (June 21, 2007), available at http://www.blackstone.com/cps/rde/xchg/bxcom/hs/news_pressrelease_3433.htm. -

Shareholder Activism: Standing up for Sustainability?

Shareholder activism: Standing up for sustainability? REPORT Shareholder activism: Standing up for sustainability? - 1 CONTENTS PREFACE........................................................................................................................4 EXECUTIVE SUMMARY.................................................................................................6 SHAREHOLDER ACTIVISM CASES...............................................................................8 PASSIVE SHAREHOLDING AND THE ‘BATTLE FOR THE SOUL OF CAPITALISM’ ....9 SHAREHOLDER ACTIVISM IN NUMBERS..................................................................10 SHAREHOLDER ACTIVISM FOR SUSTAINABILITY.....................................................11 MATERIALITY AND REPUTATION..............................................................................13 PUBLIC POLICY TRENDS AND SHAREHOLDER RIGHTS..........................................16 THE FUTURE OF SHAREHOLDER ACTIVISM.............................................................19 ANNEX I: ACTIVIST INVESTORS IN SELECTED COUNTRIES.....................................21 ANNEX II: PROXY COMPANIES...................................................................................21 ANNEX III: OVERVIEW OF ACTORS IN ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) SHAREHOLDER ACTIVISM......................................................22 REFERENCES................................................................................................................24 SOURCES.....................................................................................................................27 -

Review and Analysis of 2018 U.S. Shareholder Activism

Review and Analysis of 2018 U.S. Shareholder Activism March 14, 2019 5% increase in total number of publicly announced campaigns against U.S. issuers Elliott, Starboard and Spruce Point lead the way with the most publicly announced campaigns against U.S. issuers Infrequent activists bring 68% of all publicly announced campaigns, up from 56% 56% increase in board seats obtained per announced 2018 campaign, as activists on average obtained 0.8 board seats per campaign Issuers with market capitalizations between $1 – $10 billion targeted in 40% of announced 2018 campaigns despite comprising only 21% of Russell 3000 companies 37% of activist campaigns focus on M&A objectives, up www.sullcrom.com from 26% new york . washington, d.c. Proxy contests focusing on board-related governance los angeles . palo alto matters decrease significantly from 51% to 14% london . paris frankfurt . brussels Proportion of publicly filed settlement agreements tokyo . hong kong . beijing expressly permitting information sharing with the melbourne . sydney activist fund drops from 18% to 7% Introduction On the surface, the 2018 activism data is largely consistent with 2017, but with an uptick in overall activity. The amount of capital invested in new activist positions in 2018 was up approximately $2.5 billion from 2017,1 and activists won more board seats in 2018 than in 2017, mostly through settlements. Although several well-known activists (including Third Point, Pershing Square and Greenlight Capital) announced disappointing investment results in 2018, and the industry experienced negative net asset flows overall, activist funds continue to attract substantial new capital. REVIEW AND ANALYSIS OF 2018 U.S. -

The Costs of Shareholder Activism: Evidence from a Sequential Decision Model

University of Pennsylvania ScholarlyCommons Publicly Accessible Penn Dissertations Fall 2011 The Costs of Shareholder Activism: Evidence from a Sequential Decision Model Nickolay M. Gantchev University of Pennsylvania, [email protected] Follow this and additional works at: https://repository.upenn.edu/edissertations Part of the Corporate Finance Commons, Econometrics Commons, and the Finance Commons Recommended Citation Gantchev, Nickolay M., "The Costs of Shareholder Activism: Evidence from a Sequential Decision Model" (2011). Publicly Accessible Penn Dissertations. 442. https://repository.upenn.edu/edissertations/442 This paper is posted at ScholarlyCommons. https://repository.upenn.edu/edissertations/442 For more information, please contact [email protected]. The Costs of Shareholder Activism: Evidence from a Sequential Decision Model Abstract Recent work on hedge fund activism documents substantial abnormal returns but fails to answer the question whether these returns cover the large costs of activist campaigns. This paper provides benchmarks for monitoring costs and evaluates the net returns to activism. I model activism as a sequential decision process consisting of demand negotiations, board representation and proxy contest and estimate the costs of each distinct stage. A campaign ending in a proxy fight has average costs of $10.71 million. The proxy contest is the most expensive stage, followed by demand negotiations. The estimated monitoring costs consume more than two-thirds of gross activist returns implying that the net returns to activism are significantly lower than previously thought. Even though the mean net return is close to zero, the top quartile of activists earn higher returns on their activist holdings than on their non- activist investments. -

Cecilia Diaz Critical/Cultural Methods Dr. Bob Bednar 4/8//21

Cecilia Diaz Critical/Cultural Methods Dr. Bob Bednar 4/8//21 Research Project Draft Protests in the name of social reform have recently undergone drastic transformations in how they are founded and manifested. The ascension of social media use in the early 2000s gave rise to streamlined instant communication between people that otherwise may have never communicated organically. History has proven that we gather together in times of hardship and join forces when those hardships necessitate change and reform. The internet eliminates the practical issue of distance and facilitates the possibility of an infinite number of formed communities. In the case of protest, it facilitates the ability to organize and gather to demand social and political change. Sebastián Valenzuela suggests that one explanation for use of social networks and political protest may be online expression as a foundation for action. It is stated, “In addition to cognitive preparation, the expression of opinions can be facilitators of political protest” (Valenzuela, 2014). Research has shown that when individuals talk about political subjects publicly, they are more likely to mobilize and engage in political activities. The expression “allows people to face their ideas, make arguments, and reflect on the information obtained” (Schmitt-Beck, 2008). Platforms like Twitter and Facebook have acted as multiplexes for the expression of political views and serve as the foundation for many modern protests such as the Black Lives Matter movement, #MeToo, Arab Spring, and the Sunflower Student Movement. The protest this study will focus on is unique in that it was not founded as a politically driven protest but became one, or perhaps more accurately, was received as one as it gained popularity in mainstream media publics. -

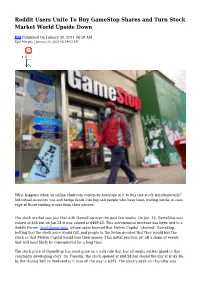

Reddit Users Unite to Buy Gamestop Shares and Turn Stock Market World Upside Down

Reddit Users Unite To Buy GameStop Shares and Turn Stock Market World Upside Down Pdf Published On January 30, 2021 06:19 AM Kyle Murphy | January 30, 2021 06:19:02 AM 0 What happens when an online chatroom convinces everyone in it to buy one stock simultaneously? Individual investors win and hedge funds lose big and people who have been trading stocks in suits rage at those trading stocks from their phones. The stock market saw just that with GameStop over the past few weeks. On Jan. 15, GameStop was valued at $35 but on Jan 28 it was valued at $469.42. This astronomical increase has been tied to a Reddit Forum, Wall Street Bets, whose users learned that Melvin Capital “shorted” GameStop, betting that the stock price would fall, and people in the forum decided that they would buy the stock so that Melvin Capital would lose their money. This initial reaction set off a chain of events that will most likely be remembered for a long time. The stock price of GameStop has since gone on a wild ride that has all media outlets glued to this constantly developing story. On Tuesday, the stock opened at $88.28 but closed the day at $145.96; by the closing bell on Wednesday it rose all the way to $345. The stock's peak on Thursday was $469.42 before trading companies like Robinhood took away the option to buy GameStop stock, causing the stock to temporarily plummet all the way down to $132 by 11:30 a.m on Thursday. -

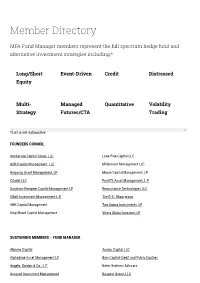

Member Directory

Member Directory MFA Fund Manager members represent the full spectrum hedge fund and alternative investment strategies including:* Long/Short Event-Driven Credit Distressed Equity Multi- Managed Quantitative Volatility Strategy Futures/CTA Trading *List is not exhaustive FOUNDERS COUNCIL Anchorage Capital Group, LLC Lone Pine Capital LLC AQR Capital Management, LLC Millennium Management LLC Balyasny Asset Management, LP Moore Capital Management, LP Citadel LLC Point72 Asset Management, L.P. Davidson Kempner Capital Management LP Renaissance Technologies LLC Elliott Investment Management L.P. The D. E. Shaw group HBK Capital Management Two Sigma Investments, LP King Street Capital Management Viking Global Investors LP SUSTAINING MEMBERS – FUND MANAGER Abrams Capital Axonic Capital LLC Alphadyne Asset Management LP Bain Capital Credit and Public Equities Angelo, Gordon & Co., L.P. Baker Brothers Advisors Assured Investment Management Baupost Group, LLC BlackRock Alternative Investors IONIC Capital Management LLC Bracebridge Capital, LLC Junto Capital Management LP Bridgewater Associates, LP. Kensico Capital Management Brigade Capital Management, LP Kepos Capital LP Cadian Capital Management Kingdon Capital Management, LLC Campbell & Company, LP Laurion Capital Management LP Capula Investment Management LLP Magnetar Capital LLC CarVal Investors Man Group Casdin Capital Marathon Asset Management, L.P. Castle Hook Partners LP Marshall Wace North America LP Centerbridge Partners, L.P. Melvin Capital CIFC Asset Management Meritage Group LP Coatue Management LLC Millburn Ridgeeld Corporation D1 Capital Partners MKP Capital Management Diameter Capital Partners LP Monarch Alternative Capital LP EJF Capital, LLC Napier Park Global Capital Element Capital Management LLC One William Street Capital Management LP Eminence Capital, LP P. Schoenfeld Asset Management LP Empyrean Capital Partners, LP Palestra Capital Management LLC Emso Asset Management Limited Paloma Partners Management Company ExodusPoint Capital Management, LP PAR Capital Management, Inc.