Annual Report 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

O R K a N G E R 2 0

ANNONSEBILAG AVISA SØR-TRØNDELAG ORKANGER 2013 www.orkanger-aktivum.no Velkommen til folkefest! • Utstillinger • Konserter • Hyggelige sammenkomster • Historiske vandringer og tilbakeblikk • Treffsted • Familiedag Orkanger 20102013 • Kulturelle innslag • Kunstutstillinger • Idrett 18.14. -23.-27. juni 14. - 23. JUNI 2 3 ORKANGER 2013 www. orkanger-aktivum.no ORKANGER 2013 www. orkanger-aktivum.no En festival hvor Orkanger Aktivum inviterer besøkende for alle som fikk delta i disse Orkanger Histories konfirmasjonsbok åpnet under Orkanger 2013. Etter den aktivitetene. med bilder fra 1945 – 2013 blir lansert, offisielle åpningen blir det anledning til et tilbakeblikk i Kaaresgatas historie som stedets og historien om Orkanger kommune for barn og unge å prøve ulike hovedgate, til slik den framstår i dag som boliggate. Nr. 66 fra 1920 til 1963 blir presentert fra friidrettsaktiviteter under kyndig I Orkdal Kunstforenings lokaler i scenen. ledelse. Stafett der idrettslag fra Velkommen til Orkanger var egen kommune fra1920 – 1963. Det vil gjennom utstillinger og foredrag bli orientert om Orkdalsveien 66 blir det anledning til Orkdal og nærkommuner er invitert å se og kjøpe kunst, produsert av Kunst i Johan Richtersgate 2 til konkurranse. Orkanger kommune i denne perioden. Orkdal Rådhus medlemmene i foreningen. I en Marthe M. Maalø med Atelier vil være sentrum for stemmerettighetsjubileet og Orkdal hyggelig atmosfære blir det anledning Mema:M er etablert i Johan ”Hageparty” på Bårdshaug Orkanger 2013! Kommunes 50-årsjubileum som storkommune. Orkanger Vel, til å kjøpe noe å drikke og spise. Det vil Richtersgate 2, tidligere kjent som Herregård som i år ble tildelt avisa Sør-Trøndelags frivillighetspris, har hver kveld bli sang og diktlesning. -

Supplementary File for the Paper COVID-19 Among Bartenders And

Supplementary file for the paper COVID-19 among bartenders and waiters before and after pub lockdown By Methi et al., 2021 Supplementary Table A: Overview of local restrictions p. 2-3 Supplementary Figure A: Estimated rates of confirmed COVID-19 for bartenders p. 4 Supplementary Figure B: Estimated rates of confirmed COVID-19 for waiters p. 4 1 Supplementary Table A: Overview of local restrictions by municipality, type of restriction (1 = no local restrictions; 2 = partial ban; 3 = full ban) and week of implementation. Municipalities with no ban (1) was randomly assigned a hypothetical week of implementation (in parentheses) to allow us to use them as a comparison group. Municipality Restriction type Week Aremark 1 (46) Asker 3 46 Aurskog-Høland 2 46 Bergen 2 45 Bærum 3 46 Drammen 3 46 Eidsvoll 1 (46) Enebakk 3 46 Flesberg 1 (46) Flå 1 (49) Fredrikstad 2 49 Frogn 2 46 Gjerdrum 1 (46) Gol 1 (46) Halden 1 (46) Hemsedal 1 (52) Hol 2 52 Hole 1 (46) Hurdal 1 (46) Hvaler 2 49 Indre Østfold 1 (46) Jevnaker1 2 46 Kongsberg 3 52 Kristiansand 1 (46) Krødsherad 1 (46) Lier 2 46 Lillestrøm 3 46 Lunner 2 46 Lørenskog 3 46 Marker 1 (45) Modum 2 46 Moss 3 49 Nannestad 1 (49) Nes 1 (46) Nesbyen 1 (49) Nesodden 1 (52) Nittedal 2 46 Nordre Follo2 3 46 Nore og Uvdal 1 (49) 2 Oslo 3 46 Rakkestad 1 (46) Ringerike 3 52 Rollag 1 (52) Rælingen 3 46 Råde 1 (46) Sarpsborg 2 49 Sigdal3 2 46 Skiptvet 1 (51) Stavanger 1 (46) Trondheim 2 52 Ullensaker 1 (52) Vestby 1 (46) Våler 1 (46) Øvre Eiker 2 51 Ål 1 (46) Ås 2 46 Note: The random assignment was conducted so that the share of municipalities with ban ( 2 and 3) within each implementation weeks was similar to the share of municipalities without ban (1) within the same (actual) implementation weeks. -

Strandheim Brug

Orkanger Historie STRANDHEIM BRUG Hentet fra Paul Nissens kåseri på Strandheim 15. sept. 2005 Ja, hvordan var det på Orkedalsøren før Standheim Brug ble etablert i 1867? Strandsettersonen ble senere kalt ”Feskarøra”, men det var ikke bare fiskere her. Transport av garkobber d.v.s. renset kobber og senere kobbermalm og svovelkis hadde gått gjennom Orkdalen. Det nevnes at 20 – 40 hester stod for transporten vintres tid. På Øra bodde det fiskere, kroholdere, jekteskippere, handelsmenn, håndverkere, offentlige tjenestemenn, og andre yrkesgrupper. Varer ble transportert på fjorden også til Trondhjem. Siel og roing ble til dels avløst av Dampbåten som kom i 1857 i regulær trafikk. Folk bodde i egne hus på bygslet grunn på gårdene Hov og Nærvik. Folk hadde litt plass og hadde gjerne et par husdyrgris, sau, ku eller geit. Betalin for bygsel var arbeid på gården vår og høst eller betaling i klingende mynt. Pengehusholdning overtok mer av den tungvinte naturalhusholdningen hvor man byttet varer og tjenester. Det ble et tydelig skille på Orkedalsøren etter Strandheim Brug ble etablert i 1867. 3 generasjoner Thams Det er 3generasjoner athams som jar satt sitt store positive preg på utviklingen i Orkdalen. De var gründere – ja, hva er en gründer? De har ideer, ser muligheter, tar sjanser. De får andre med, det satses risikovillig kapital, de orienterer seg i inn- og utland. Og ”Thamsene” de fikk med seg det nyeste i teknologisk utvikling og da tenker jeg særlig på dampmaskiner og el-kraft. Ja, hva må til for å starte og finne stedet? En energikilde : Fossekraft, dampmaskin og el-kraft Transport : Hester, vind og seil, dampbåt, veier og jernbane Råstoff : Skog og tømmer, svovelkis, trekull og koks Arbeidskraft : Folk kommer når det er muligheter, så det ordner seg av seg selv. -

TRANSLATION 1 of 3

114,, Fisheries Pêches TRANSLATION 31 and Oceans et Océans SERIES NO(S) 4888 1 of 3 CANADIAN TRANSLATION OF FISHERIES AND AQUATIC SCIENCES No. 4888 Acid lakes and inland fishing in Norway Results from an interview survey (1974 - 1979) by I.H. Sevaldrud, and I.P. Muniz Original Title: Sure vatn og innlandsfisket i Norge. • Resultater fra intervjuunderseelsene 1974-1979. From: Sur NedbOrs Virkning Pa Skog of Fisk (SNSF-Prosjektet) IR 77/80: 1-203, 1980. Translated by the Translation Bureau (sowF) Multilingual Services Division Department of the Secretary of State of Canada Department of Fisheries and Oceans Northwest Atlantic Fisheries Centre St. John's, NFLD 1982 205 pages typescript Secretary Secrétariat of State d'État MULTILINGUAL SERVICES DIVISION — DIVISION DES SERVICES MULTILINGUES TRANSLATION BUREAU BUREAU DES TRADUCT IONS Iffe LIBRARY IDENTIFICATION — FICHE SIGNALÉTIQUE Translated from - Traduction de Into - En Norwegian English Author - Auteur Iver H. Sevaldrud and Ivar Pors Muniz Title in English or French - Titre anglais ou français Acid Lakes and Inland Fishing in Norway. Results from an Interview Survey (1974 - 1979). Title in foreign language (Transliterate foreign characters) Titre en langue étrangère (Transcrire en caractères romains) Sure vatn og innlandsfisket i Norge. Resultater fra intervjuunders$1(e1sene 1974 - 1979 Reference in foreign language (Name of book or publication) in full, transliterate foreign characters. Référence en langue étrangère (Nom du livre ou publication), au complet, transcrire en caractères romains. Sur nedbç4rs virkning pa skog of fisk (SNSF-prosjektet) Reference in English or French - Référence en anglais ou français • 4eicid Precipitation - Effects on Forest and Fish (the SNSF-project) Publisher - Editeur Page Numbers in original DATE OF PUBLICATION Numéros des pages dans SNSF Project, Box 61, DATE DE PUBLICATION l'original Norway 1432 Aas-NHL, 203 Year Issue No. -

LIS1 Høst 2020 – Aktivitetsoversikt for Kurs Og Gruppeveiledning

Fylkesmannen i Oslo og Viken Oppdatert pr. 01.09.20 LIS1 høst 2020 – aktivitetsoversikt for kurs og gruppeveiledning Kurs i offentlig helsearbeid 20.-21.10.20 Webinar – felles for alle LIS1 i Oslo og Viken Kurs i akuttmedisin og gruppeveiledningene blir organisert etter geografisk tilhørighet som angitt nedenfor: LIS1 med tjeneste i kommuner i sykehusområdet til Sykehuset Østfold Gruppe Østviken sør (Fredrikstad, Sarpsborg, Halden, Moss, Indre Østfold, Rakkestad, Hvaler, Råde, Marker, Våler) Kurs i akuttmedisin/legevaktmedisin 03.-04.09.20 Sarpsborg og Rakkestad legevakt, Helsehuset Sarpsborg Gruppeveiledning Tid: 06.10.20, 17.11.20, 12.01.21. Alle dager kl. 12.00-18.00. Sted: Fylkesmannens lokaler i Moss, Vogts gate 17. Fremmøte i resepsjonen i 1. etasje senest kl. 11.50. Samlingene kan måtte gjennomføres på alternativt vis avhengig av smittesituasjonen. LIS1 med tjeneste i kommuner i sykehusområdet til Ahus, samt Lunner kommune Gruppe Østviken nord 1 (Aurskog-Høland, Nesodden, Enebakk, Lørenskog, Rælingen, Vestby, Frogn, Nordre Follo, Ås) Kurs i akuttmedisin/legevaktmedisin 02.-03.09.20 Ahus, Lørenskog Gruppeveiledning Tid: 02.10.20, 20.11.20, 22.01.21. Alle dager kl. 09.00-15.00. Sted: Fylkesmannens lokaler i Oslo, Holberg Terrasse, Stensberggaten 27. Fremmøte i resepsjonen i 1. etasje senest kl. 08.45. Samlingene kan måtte gjennomføres på alternativt vis avhengig av smittesituasjonen. Gruppe Østviken nord 2 (Lillestrøm, Nes, Gjerdrum, Nittedal, Nannestad, Hurdal, Ullensaker, Eidsvoll, Lunner) Kurs i akuttmedisin/legevaktmedisin 02.-03.09.20 Ahus, Lørenskog Gruppeveiledning Tid: 01.10.20, 27.11.20, 29.01.21. Alle dager kl. 09.00-15.00. Sted: Fylkesmannens lokaler i Oslo, Holberg Terrasse, Stensberggaten 27. -

Askim Kommune Januar

ASKIM Gyldig fra KOMMUNE 2014 JANUAR OM FLEXX Flexx er bestillingstrafikk og inngår som en del av det ordinære kollektivtilbudet i Østfold, men er ikke som en vanlig busstur. Du kan nemlig hentes hjemme og bli kjørt hjem igjen, men du betaler kun busspris. Flexx er for alle, og du kan få hjelp av sjåføren til av- og påstigning om du behøver det. Flexx stopper bare der reisende skal hentes eller leveres, derfor kan kjøretiden variere fra tur til tur. Husk at Flexx må bestilles senest 2 timer før du ønsker å reise. Hvis du har registrert ditt mobilnummer, vil du få en SMS 15 minutter før beregnet hentetid. FLEXX BESTÅR AV DISSE TILBUDENE: FLEXX LINJE er bestillingsruter som kjører fast rute til fast tid, men som kun kjøres hvis noen bestiller tur. Prisen er den samme som din vanlige bussbillett. Alle som bor inntil 2 km fra en Flexx-linje, kan bestille reise og blir hentet hjemme. Dette gjelder ikke i Askim sentrum hvor det er felles møteplasser for av- og påstigning. Husk at du må bestille senest 2 timer før linjens avgangstidspunkt. Fordi Flexx også skal hente andre, må du være klar 15 minutter før henting. FLEXX NATT er et tilbud natt til lørdag og natt til søndag for ungdom mellom 16 og 24 år. Flexx natt starter i Askim sentrum, men kan ta med personer underveis på strekningen. Hver passasjer betaler kr 50,– for turen, og tilbudet kan også brukes av andre hvis det er ledig plass. Alle kjøres hjem på døren, bortsett fra de som går av og på i sentrum. -

Administrative and Statistical Areas English Version – SOSI Standard 4.0

Administrative and statistical areas English version – SOSI standard 4.0 Administrative and statistical areas Norwegian Mapping Authority [email protected] Norwegian Mapping Authority June 2009 Page 1 of 191 Administrative and statistical areas English version – SOSI standard 4.0 1 Applications schema ......................................................................................................................7 1.1 Administrative units subclassification ....................................................................................7 1.1 Description ...................................................................................................................... 14 1.1.1 CityDistrict ................................................................................................................ 14 1.1.2 CityDistrictBoundary ................................................................................................ 14 1.1.3 SubArea ................................................................................................................... 14 1.1.4 BasicDistrictUnit ....................................................................................................... 15 1.1.5 SchoolDistrict ........................................................................................................... 16 1.1.6 <<DataType>> SchoolDistrictId ............................................................................... 17 1.1.7 SchoolDistrictBoundary ........................................................................................... -

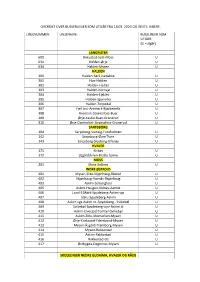

BUSSLINJER SOM UTGÅR: (U =Utgår)

OVERSIKT OVER BUSSERLINJER SOM UTGÅR FRA 18.03. 2020 OG INNTIL VIDERE. LINJENUMMER: LINJENAVN: BUSSLINJER SOM UTGÅR: (U =utgår) LANGRUTER 600 Rekustad-Solli-Moss U 631 Halden-Ørje U 634 Halden-Mysen U HALDEN 300 Halden-Sørli-Isebakke U 301 Hov-Halden U 302 Halden-Holtet U 303 Halden-Kornsjø U 304 Halden-Elgklev U 305 Halden-Sponvika U 306 Halden-Torpedal U 307 Fjell bru-Aremark-Bjørkebekk U 308 Aremark-Strømsfoss-Buer U 309 Ørje-Kasbo-Buer-Granerud U 310 Ørje-Damholtet-Strømsfoss-Granerud U SARPSBORG 104 Sarpsborg-Varteig-Furuholmen U 142 Sarpsborg-Øvre Tune U 143 Sarpsborg-Skjeberg-Ullerøy U HVALER 171 Kirkøy U 172 Utgårdskilen-Bratte bakke U MOSS 201 Moss-Saltnes U INDRE ØSTFOLD 401 Mysen-Slitu-Skjønhaug-Båstad U 402 Skjønhaug-Havnås-Skjønhaug U 403 Askim-Solbergfoss U 405 Askim-Haugen-Vidnes-Aamot U 406 Lund-S Mørk-Spydeberg-Askim vgs U 407 Libru-Spydeberg-Askim U 408 Askim vgs-Askim st.-Spydeberg - Svikebøl U 409 Svikebøl-Spydeberg torv-Askim st U 410 Askim-Elvestad-Tomter-Svikebøl U 411 Askim-Slitu-Momarken-Mysen U 412 Ørje-Kroksund-Ydersbond-Mysen U 413 Mysen-Åsgård-Trømborg-Mysen U 414 Mysen-Rakkestad U 415 Askim-Rakkestad U 416 Rakkestad-Os U 417 Østbygda-Degernes-Mysen U SKOLELINJER NEDRE GLOMMA, HVALER OG RÅDE 150 Grålum skole U 151 Jelsnes skole U 152 Kurland skole U 153 Sarpsborg skolene U 154 Varteig skole U 155 Hafslund skole U 156 Sandbakken skole U 157 Hornnes skole U 158 Ullerøy skole U 162 Greåker vgs U 163 Kalnes vgs U 164 Borg vgs U 178 Borge barneskole U 179 Torsnes skole U 180 Nylende skole U 181 Rekustad skole U -

Thamshavnbanen Fredningsvedtak

SAKSBEHANDLER INNVALGSTELEFON TELEFAKS Ståle Arfeldt Bergås +47 22 94 04 04 Lars Erik Eibak Bru [email protected] Alexander Ytteborg www.riksantikvaren.no DERES DATO VÅR REF. DERES REF. 07/02428-13 VÅR DATO ARK. D - Infrastruktur 20.12.2013 361-362 Melhus kom. - ST Se mottakerliste THAMSHAVNBANEN, I MELDAL OG ORKANGER KOMMUNER, SØR-TRØNDELAG VEDTAK OM FREDNING MED HJEMMEL I LOV OM KULTURMINNER §§ 15 OG 19 JF. § 22 Vi viser til tidligere utsendt fredningsforslag fra Sør-Trøndelag fylkeskommune for Thamshavnbanen datert 20.4.2010 som har vært på høring hos berørte parter og instanser. På grunnlag av dette fatter Riksantikvaren følgende vedtak: VEDTAK: Med hjemmel i lov av 9. juni 1978 nr. 50 om kulturminner (kml) §§ 15 og 19 jf. § 22, freder Riksantikvaren Thamshavnbanen, i Meldal og Orkanger kommuner, Sør-Trøndelag fylke. Omfanget av fredningen Fredningen etter kml § 15 omfatter: Hele jernbanestrekningen fra Løkken Verk til Thamshavn, bestående av selve jernbanelegemet med påstående skinner, sviller og penser, samt kjøreledningsanlegg (KL-anlegg), bygningsanlegg tilhørende banen, tunnel i Klingliene og den opprinnelige traseen rundt Klinghåmmår’n fra 1908, samt bruer, bekkekulverter, overganger, underganger og fegater, jf. kart og bygningsoversikt. Total lengde for banen er 25 km, mens kjørbar lengde i dag er på 23 km. Fredningen omfatter bygningenes eksteriør og interiør og inkluderer hovedelementer som planløsning, materialbruk og overflatebehandling og detaljer som vinduer, dører, gerikter, listverk, ildsteder og fast inventar. Fredningen etter kml § 19 omfatter arealer som er tilknyttet jernbanen fra Thamshavn til Løkken Verk, avgrenset av Salvesen & Thams og Orkla sine eiendomsgrenser. I det fredete området inngår også arealer for den gamle jernbanetraséen rundt Klinghåmmår’n og deler av arealet til Elkem Thamshavn Verks grunn ved Thamshavn stasjon, til og med det gamle jernbaneverkstedet. -

National Register of Historic Places Registration Form

NFS Form 10-900 OMB No. (January 1992) Wisconsin Word Processing Format (Approved 1/92) United States Department of Interior National Park Service National Register of Historic Places Registration Form This form is for use in nominating or requesting determinations for individual properties and districts. See instructions in How to Complete the National Register of Historic Places Registration Form (National Register Bulletin 16 A). Complete each item by marking "x" in the appropriate box or by entering the information requested. If an item does not apply to the property l^r.';;; documented, enter "N/A" for "not applicable." For functions, architectural classification, materials, and areas of signiiic-^v,-, enter only categories and subcategories from the instructions. Place additional entries and narrative items on continuation sheets (NFS Form 10-900A). Use a typewriter, word processor, or computer, to complete all items. 1. Name of Property historic name Little Norway other names/site number Nissedahle 2. Location street £ number 3576 CTH JG N/A not for pubh city or town Town of Blue Mounds N/A vicinity state Wisconsin code WI county Dane code 025 zip code 5C 13, State/Federal Agency Certification As the designated authority under the National Historic Preservation Act, as amended, I hereby certify that this X nomination jf eligibility meets the documentation standards for registering properties in. the National Register o:i tfstoric Places Mnd meets |he/p?&cedural and professional requirements set forth in 36 CFR Part 60. In my opinion, the [property X meejj^^djoes. i^tjinee/ the National Register criteria. I recommend that this property be considered significant , See continuation sheet for additional comments.) —————————j———**»**———•*—————————^y?—— ^ ————^———•————— I 22 Signature of certifymg officialATitle Date Deputy State Mstorio^ Preservation Of ficer-WI State or Federal agency and bureau In my opinion, the property _ meets _ does not meet the National Register criteria. -

D4.3 2019.03 Success Factors for Future Industrial Clusters

FME HighEFF Centre for an Energy Efficient and Competitive Industry for the Future Deliverable D4.3_2019.03 Success Factors for Future Industrial Clusters Delivery date: 2020-02.16 Organisation name of lead partner for this deliverable: NTNU SR HighEFF- Centre for an Energy Efficient and Competitive Industry for the Future is one of Norway's Centre for Environment-friendly Energy Research (FME). Project co-funded by the Research Council of Norway and Industry partners. Host institution is SINTEF Energi AS. Dissemination Level PU Public X RE Restricted to a group specified by the consortium INT Internal (restricted to consortium partners only) FME HighEFF HighEFF.no Deliverable number: D4.3_2019.03 ISBN number: - Deliverable title: Success factors for Future Industrial Clusters Work package: 4.3 Industry clusters and technology integration Deliverable type: Report Lead participant: NTNU SR – Håkon Fyhn Quality Assurance, status of deliverable Action Performed by Date Verified (WP leader) Kristian Etienne Einarsrud 17.02.2020 Reviewed (RA leader) Aud Wærnes 17.02.2020 Approved (dependent on nature of deliverable)*) *) The quality assurance and approval of HighEFF deliverables and publications have to follow the established procedure. The procedure can be found in the HighEFF eRoom in the folder "Administrative > Procedures". Authors Author(s) Name Organisation E-mail adress Håkon Fyhn NTNU SR [email protected] Lucia Liste NTNU SR [email protected] Jens Petter Johansen NTNU SR [email protected] Abstract This report aims to contribute to growing body of knowledge about industrial symbiosis by portraying success factors that can facilitate the formation of future industrial clusters and symbiosis. -

Environmental Report 1998 Contents

Orkla - Environmental Report 1998 Contents Orkla's environmental policy 1 This is Orkla Focus on the environment 2, 15 Orkla is the second largest listed company in Norway in terms of market capitalisation. The Orkla Group has Environmental reports from: three core business areas: Branded Consumer Goods, Orkla Foods 4 Chemicals and Financial Investments. From the 1980s up Orkla Beverages 6 to the present the Group has been one of Norway’s Orkla Brands 8 fastest growing businesses. Operating income has in- Orkla Media 10 creased from NOK 1.2 billion in 1982 to NOK 30.8 billion Chemicals 12 in 1998. 54 % of Orkla’s operating income and 51 % of Key health and environment figures 16 employment were generated outside Norway in 1998. Glossary 17 The Branded Consumer Goods area accounts for Environmental contacts 17 close to 80 % of Group operating income and comprises food, beverages, snacks, biscuits, chocolate, confec- tionery, detergents, personal products/cosmetics, news- papers and magazines. This business area wishes to consolidate its position as the leading supplier of brand- ed consumer goods to Nordic households. Future growth will primarily be achieved through greater focus on the most successful product groups and through gradual ex- pansion outside the Nordic region, largely into selected Key group figures markets in Eastern Europe. 1998 1997 1996 The Chemicals area, which includes Borregaard’s production of specialty chemicals, fine chemicals and Operating income (NOK mill.) 30,819 30,970 25,998 ingredients, is Orkla’s most international business. The Operating profit before company has production facilities on every continent ex- OIE* (NOK mill.) 2,132 2,432 1,896 cept Australia, and holds strong global positions in its Operating profit (NOK mill.) 1,797 2,613 1,916 selected niches.