Download 2019 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Softball Drills and Modified Games

SOFTBALL DRILLS AND MODIFIED GAMES This booklet has been developed as a resource guide for coaches. It has the detailed descriptions of drills and modified games listed in the National and Academy Coaches Handbook. The booklet is in two parts: 1. Softball Drills 2. Modified Games The softball drills are grouped into sections related to Offense and Defense. They are only a small selection of many drills that are used in the game of softball. No coach should feel they should only use the ones listed. You are only limited by your imagination! The modified games are designed to compliment the skills needed to play softball effectively. But most of all they are fun and add variety to any training session. The modified games can be adjusted to suit all age groups. Enjoy! CONTENTS SOFTBALL DRILLS Batting Page 3 Bunting Page 10 Fielding Page 10 Outfield Drils Page 13 Base Running Page 18 Catching Page 20 Pitching Page 22 MODIFIED GAMES Page 26 Acknowledgement This handbook was developed and put together from the collective resources and materials available to us from many different sources. We collectively acknowledge all concerned and hope this handbook will play an important role in the development of the players we have the pleasure of coaching. Wayne Durbridge Simon Roskvist Paula McGovern Chet Gray Marty Rubinoff Level 1 & 2 Softball Manuals Karen Marr VSA & VBA Games Booklets SOFTBALL DRILLS BATTING The key to successful batting is practice. Batting drills allow the batter to perform many swings in a short period of time which is important because muscle memory depends on repetition, and each drill helps the batter to focus on one particular aspect of the swing, thereby accelerating the learning. -

The Top 5G Stock to Buy in 2019 the 5G Stock We Love for 2019 Is Canada-Based Telus Corp

Contents INTRODUCTION Page i 2019 Will Bring Unprecedented Moneymaking Opportunities CHAPTER 1 Page 1 The Seven “No-Brainer” Stocks to Buy in 2019 – Plus Our “Wild Card” Pick CHAPTER 2 Page 12 The Only Stock to Own Ahead of the $1.3 Trillion 5G Revolution CHAPTER 3 Page 17 How to Turn Water Scarcity into a 40% – Plus Gain CHAPTER 4 Page 22 The Secret Way to Profit from the 11 “Unicorn” IPOs Slated for 2019 CHAPTER 5 Page 35 The Cryptocurrency with 1,000% Growth Potential CHAPTER 6 Page 40 Five Income Stocks with Double-Digit Growth Ahead CHAPTER 7 Page 47 Bank 145% Gains in the Biggest Year Yet for Cannabis Investors CHAPTER 8 Page 52 The Three Trendy Stocks to Avoid in 2019 MONEY MORNING THE ULTIMATE MONEY MAKING GUIDE FOR 2019 Introduction: 2019 Will Bring Unprecedented Moneymaking Opportunities Here at Money Morning, we have one goal: to make investing profitable. In 2018 alone, our readers had the chance to book gains of 333%, 440%, and even 478% on stock trades that came from our research. We also kept our readers at the forefront of the hottest investing trends, like cannabis legalization. After we told Money Morning subscribers about top cannabis pick Tilray Inc., the stock soared 262%. But you wouldn’t know these opportunities were out there from listening to mainstream financial news… Cable news focused on the trade war as major indexes struggled to stay in the black. And Wall Street pundits couldn’t stop talking about the evils of Facebook as it slid 24% this year. -

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

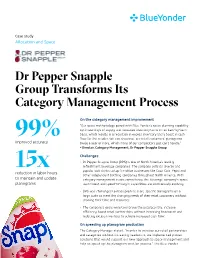

Dr Pepper Snapple Group Transforms Its Category Management Process

Case study Allocation and Space Dr Pepper Snapple Group Transforms Its Category Management Process On the category management improvement “Our space methodology paired with Blue Yonder’s space planning capability optimizes days of supply and increases inventory turns on an item-by-item basis, which results in a reduction in excess inventory and a boost in cash 99% flow for the retailer. We can also reset our retail customers’ planograms improved accuracy twice a year or more, which many of our competitors just can’t handle.” - Director, Category Management, Dr Pepper Snapple Group Challenges • Dr Pepper Snapple Group (DPS) is one of North America’s leading refreshment beverage companies. The company sells its diverse and 15x popular soft drinks to top franchise businesses like Coca-Cola, Pepsi and reduction in labor hours other independent bottling companies throughout North America. With to maintain and update category management a core competency, the beverage company’s space, planograms assortment and speed-to-insight capabilities are continuously evolving. • DPS was challenged to mass produce store-specific planograms on a large scale to meet the changing needs of their retail customers without draining their time and resources. • The company’s goals were to improve the accuracy rate, increase efficiency, boost retail partnerships without increasing headcount and reducing excess inventory to achieve increased cash flow. On speeding up planogram production The Category Manager stated, “In order to increase our retail partnerships and categories without increasing headcount, we implemented proven solutions that would support our new approach to space management and help us speed up the planogram creation process.” The Blue Yonder solution automated the large-scale production of Blue Yonder’s expertise optimized, store-specific planograms, increasing Dr Pepper Snapple Group’s accuracy rate to 99 percent. -

Fund Holdings As of 6/30/2021 Massmutual Balanced Fund Invesco Prior to 5/1/2021, the Fund Name Was Massmutual Premier Balanced Fund

Fund Holdings As of 6/30/2021 MassMutual Balanced Fund Invesco Prior to 5/1/2021, the Fund name was MassMutual Premier Balanced Fund. Fund Shares or Par Position Market Security Name Ticker CUSIP Weighting % Amount Value Apple Inc AAPL 037833100 3.91 48,433 6,633,384 Microsoft Corp MSFT 594918104 3.45 21,552 5,838,437 USTREAS T-Bill Auction Ave 3 Mon 1.69 2,862,977 JPMorgan Chase & Co JPM 46625H100 1.56 16,948 2,636,092 Verizon Communications Inc VZ 92343V104 1.45 43,768 2,452,321 The Home Depot Inc HD 437076102 1.42 7,556 2,409,533 Intel Corp INTC 458140100 1.29 38,961 2,187,271 Procter & Gamble Co PG 742718109 1.04 13,105 1,768,258 Cisco Systems Inc CSCO 17275R102 1.03 32,830 1,739,990 UnitedHealth Group Inc UNH 91324P102 1.00 4,215 1,687,855 Comcast Corp Class A CMCSA 20030N101 0.94 28,021 1,597,757 AT&T Inc T 00206R102 0.91 53,587 1,542,234 Oracle Corp ORCL 68389X105 0.83 18,031 1,403,533 Deere & Co DE 244199105 0.76 3,635 1,282,101 Accenture PLC Class A ACN G1151C101 0.74 4,237 1,249,025 Johnson Controls International PLC JCI G51502105 0.74 18,185 1,248,037 Visa Inc Class A V 92826C839 0.71 5,152 1,204,641 Texas Instruments Inc TXN 882508104 0.70 6,128 1,178,414 Costco Wholesale Corp COST 22160K105 0.67 2,850 1,127,660 Bank of America Corp BAC 060505104 0.64 26,192 1,079,896 Broadcom Inc AVGO 11135F101 0.63 2,223 1,060,015 Abbott Laboratories ABT 002824100 0.57 8,348 967,784 Target Corp TGT 87612E106 0.56 3,949 954,631 Honeywell International Inc HON 438516106 0.56 4,324 948,469 Goldman Sachs Group Inc GS 38141G104 0.53 2,374 901,004 -

OPYBS Softball Coaches' Manual

Oak Park Youth Baseball and Softball (OPYBS) Softball Coaches’ Manual Second Edition, April 2012 © 2012 Oak Park Youth Baseball and Softball OPYBS Coaches Manual, First Edition, April 2012 1 of 71 Photos and on-line video were added for the Second Edition of this manual. Thanks to the following for their work on photograph and video taping: Andrew Carlin Brian Endless Greg Meadors Brigid Sullivan Thanks also to our OPYBS players who served as “models” for these pictures and videos: Jenna Baig Eliza Endless Mireya Garcia Patti Meadors Cassie Metzger Paige Ross Mariah Scott Megan Sullivan And a special thank you to Concordia University Chicago and Fenwick High School for the use of their facilities as locations for photography and video taping. Visit www.youtube.com/opybssoftball for the “Pitching Instruction” video that accompanies this manual OPYBS Coaches Manual, First Edition, April 2012 2 of 71 Introduction -or- “Hey, you’re a coach! Now what?” ...........................................................................................4 Chapter I: Coaching 101........................................................................................................................................7 Being a coach.....................................................................................................................................................7 Positive Coaching ..............................................................................................................................................7 Competition .......................................................................................................................................................7 -

Dr Pepper Snapple Group, Inc. – Name/Symbol/Cusip Change Futures Symbol: Dps1d New Symbol: Kdp1d Date: 7/10/18

#43331 DATE: JULY 9, 2018 SUBJECT: DR PEPPER SNAPPLE GROUP, INC. – NAME/SYMBOL/CUSIP CHANGE FUTURES SYMBOL: DPS1D NEW SYMBOL: KDP1D DATE: 7/10/18 The Options Clearing Corporation (OCC) has been informed that Dr Pepper Snapple Group, Inc. (DPS) will change its name, trading symbol and CUSIP to Keurig Dr Pepper Inc. (KDP), CUSIP 49271V100. As a result, futures symbol DPS1D will also change to KDP1D effective at the opening of business on July 10, 2018. All other terms will not change. Clearing Member input to OCC must use the new futures symbol KDP1D commencing July 10, 2018. DATE: July 10, 2018 FUTURES SYMBOL: DPS1D changes to KDP1D UNDERLYING SECURITY: DPS changes to KDP MULTIPLIER: 100 (e.g. 1 equals $100) NUMBER OF CONTRACTS: Unchanged DELIVERABLE PER CONTRACT: 100 Keurig Dr Pepper Inc. (KDP) Common Shares CUSIP: (New) 49271V100 DISCLAIMER This Information Memo provides an unofficial summary of the terms of corporate events affecting listed options or futures prepared for the convenience of market participants. OCC accepts no responsibility for the accuracy or completeness of the summary, particularly for information which may be relevant to investment decisions. Option or futures investors should independently ascertain and evaluate all information concerning this corporate event(s). The determination to adjust options and the nature of any adjustment is made by a panel of The OCC Securities Committee pursuant to OCC By-Laws, Article VI, Sections 11 and 11A. The adjustment panel is comprised of representatives from OCC and each exchange which trades the affected option. The determination to adjust futures and the nature of any adjustment is made by OCC pursuant to OCC By- Laws, Article XII, Sections 3, 4, or 4A, as applicable. -

PDF Product Guide

05/24/21 To Place an Order, Call (207)947-0321 Fax: (207)947-0323 ITEM # DESCRIPTION PACK ITEM # DESCRIPTION PACK COCKTAIL MIXES COFFEE FLAVORED 14678 ROLAND OLIVE JUICE DIRTY*MARTIN 12/25.4OZ 10927 MAINE'S BEST COFFEE JAMAICAN ME CRAZY 2 24/2.25OZ 2008 OCEAN SPRAY DRINK MIX BLOODY MARY 12/32 OZ 11282 MAINE'S BEST COFFEE VACATIONLND VANILLA 24/2.25OZ 26628 MAYSON'S MARGARITA MIX ON THE ROCKS 4/1 GAL 11516 MAINE'S BEST COFFEE HARBORSIDE HAZELNUT 24/2.25OZ 26633 MAYSON'S MARGARITA MIX FOR FROZEN 4/1 GAL 83931 NewEngland COFFEE REG FRNCH VAN CRAZE 24/2.5OZ 26634 MAYSON'S MARGARITA STRAWBERRY PUREE 4/1 GAL 83933 NewEngland COFFEE REG HAZELNUT CRAZE 24/2.5OZ 26637 MAYSON'S MARGARITA RASPBERRY PUREE 4/1 GAL 83939 NewEngland COFFEE REG PUMPKIN SPICE 24/2.5OZ 26639 MAYSON'S MARGARITA PEACH PUREE 4/1 GAL 83940 NewEngland COFFEE REG CINNAMON STICKY B 24/2.5OZ 26640 MAYSON'S MARGARITA WATERMELON PUREE 4/1 GAL 26724 MAYSON'S MARGARITA MANGO PUREE 4/1 GAL 83831 Packer DRINK MIX LEMON POWDER 12/1GAL COFFEE REGULAR 83890 COCO LOPEZ DRINK MIX CREAM COCONUT 24/15oz 10444 MAXWELL HOUSE COFFEE HOTEL & REST 112/1.6OZ 84011 Rose's SYRUP GRENADINE 12/1LTR 10479 Folgers COFFEE LIQ 100% COLOMBIAN 2/1.25L 10923 MAINE'S BEST COFFEE REG ACADIA BLEND 2O 42/2OZ 10924 MAINE'S BEST COFFEE REG COUNTY BLEND 1. 42/1.5OZ CAPPUCCINO 10930 MAINE'S BEST COFFEE REG DWNEAST DARK 2. 24/2.25OZ 90343 Int Coffee CAPPUCCINO FRENCH VAN 6/2LB 1410 Maxwellhse COFFEE REGULAR MASTERBLEND 64/3.75 OZ 23529 MAINE'S BEST COFFEE SEBAGO BLEND 42/2.25OZ 23531 NEW ENGLAND COFFEE EXTREME KAFFEINE -

Keurig Dr Pepper Relocating Texas Headquarters to Frisco New Dual Headquarters Location Will Provide a Vibrant, Collaborative and Connected Workplace

FOR IMMEDIATE RELEASE February 21, 2019 MEDIA CONTACTS Keurig Dr Pepper: Frisco EDC: Dallas Cowboys Football Club: Katie Gilroy, 617-820-8971 Leigh Lyons, 972-292-5155 Joe Trahan, 972-497-4552 [email protected] [email protected] [email protected] Keurig Dr Pepper Relocating Texas Headquarters to Frisco New dual headquarters location will provide a vibrant, collaborative and connected workplace PLANO, Texas and BURLINGTON, Mass. – Keurig Dr Pepper (NYSE: KDP) today announced that the company will move its Texas headquarters from Plano to a new, 350,000 sq. ft. build-to-suit, leased facility at The Star in Frisco, Texas. The new location will be ready in 2021 and serve as one of the company’s two headquarters, with the other located in Burlington, Massachusetts. “We are excited to upgrade our Texas co-headquarters location to support the needs of our vibrant business, including enhanced technology capabilities and space to increase collaboration,” said Bob Gamgort, Chairman and CEO of Keurig Dr Pepper. “The new location at The Star in Frisco will provide a state-of the-art work environment and exciting amenities that will energize our employees and enable us to attract top talent in the area.“ The announcement follows a vote by the Frisco Economic Development Corporation Board of Directors approving an incentive package tied to certain performance criteria. Approximately 1,100 employees work in the company’s current location in Plano, which it has occupied since 1998. “This is an exciting day for the City of Frisco,” said Frisco Mayor Jeff Cheney. “Having this Fortune 500 company located in Frisco will continue to strengthen the city’s position as one of the top corporate relocation destinations in the United States. -

Product Differentiation and Mergers in the Carbonated Soft Drink Industry

Product Differentiation and Mergers in the Carbonated Soft Drink Industry JEAN-PIERRE DUBE´ University of Chicago Graduate School of Business Chicago, IL 60637 [email protected] I simulate the competitive impact of several soft drink mergers from the 1980s on equilibrium prices and quantities. An unusual feature of soft drink demand is that, at the individual purchase level, households regularly select a variety of soft drink products. Specifically, on a given trip households may select multiple soft drink products and multiple units of each. A concern is that using a standard discrete choice model that assumes single unit purchases may understate the price elasticity of demand. Tomodel the sophisticated choice behavior generating this multiple discreteness,Iuse a household-level scanner data set. Market demand is then computed by aggregating the household estimates. Combining the aggregate demand estimates with a model of static oligopoly, I then run the merger simulations. Despite moderate price increases, I find substantial welfare losses from the proposed merger between Coca-Cola and Dr. Pepper. I also find large price increases and corresponding welfare losses from the proposed merger between Pepsi and 7 UP and, more notably, between Coca-Cola and Pepsi. 1. Introduction With the advent of aggregate brand-level data collected at supermarket checkout scanners, researchers have begun to use structural econo- metric models for policy analysis. The rich content of scanner data enables the estimation of demand systems and their corresponding cross-price elasticities. The areas of merger and antitrust policy have been strong beneficiaries of these improved data. Recent advances in structural approaches to empirical merger analysis consist of combining Iamvery grateful to my thesis committee: David Besanko, Tim Conley, Sachin Gupta, and Rob Porter. -

Carbonated Soft Drinks in the US Through 2025

Carbonated Soft Drinks in the U.S. through 2025: Market Essentials 2021 Edition (To be published September 2021. Data through 2020. Market projections through 2025.) More than 120 Excel tables plus an executive summary detailing trends and comprehensive profiles of leading companies, their brands and their strategies. his comprehensive market research report on the number-two T beverage category examines trends and top companies' For A Full strategies. It provides up-to-date statistics on leading brands, Catalog of packaging, quarterly growth and channels of distribution. It also Reports and offers data on regional markets, pricing, demographics, Databases, advertising, five-year growth projections and more. Go To The report presents the data in Excel spreadsheets, which it supplements with a concise executive summary highlighting key bmcreports.com developments including the impact of the coronavirus pandemic as well as a detailed discussion of the leading carbonated soft drink (CSD) companies. INSIDE: REPORT OVERVIEW A brief discussion of key AVAILABLE FORMAT & features of this report. 2 PRICING TABLE OF CONTENTS Direct Download A detailed outline of this Excel sheets, PDF, PowerPoint & Word report’s contents and data tables. 7 $4,395 To learn more, to place an advance order or to inquire about SAMPLE TEXT AND additional user licenses call: Charlene Harvey +1 212.688.7640 INFOGRAPHICS ext. 1962 [email protected] A few examples of this report’s text, data content layout and style. 13 HAVE Contact Charlene Harvey: 212-688-7640 x 1962 QUESTIONS? [email protected] Beverage Marketing Corporation 850 Third Avenue, 13th Floor, New York, NY 10022 Tel: 212-688-7640 Fax: 212-826-1255 The answers you need Carbonated Soft Drinks in the U.S. -

Introducing Keurig Dr Pepper

Introducing Keurig Dr Pepper Investor Presentation Creating a New Challenger In the Beverage Industry Highly Confidential January 2018 Forward Looking Statements Certain statements contained herein are “forward-looking statements” within the meaning of applicable securities laws and regulations. These forward-looking statements can generally be identified by the use of words such as “anticipate,” “expect,” “believe,” “could,” “estimate,” “feel,” “forecast,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will,” “would,” and similar words, phrases or expressions and variations or negatives of these words, although not all forward-looking statements contain these identifying words. Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as statements regarding the estimated or anticipated future results of the combined company following the proposed merger, the anticipated benefits of the proposed merger, including estimated synergies, the expected timing of completion of the proposed merger and related transactions and other statements that are not historical facts. These statements are based on the current expectations of Keurig Green Mountain Parent Holdings Corp. and Dr Pepper Snapple Group, Inc. management and are not predictions of actual performance. These forward-looking statements are subject to a number of risks and uncertainties regarding the combined company’s business and the proposed merger and actual results may differ materially. These risks and uncertainties