The French Automotive Industry Analysis And

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Air Dryer Cartridge 5001004902 New

AIR DRYER CARTRIDGE 5001004902 NEW Product Images PARTS THAT ARE NOT INCLUDED, CAN BE OFFERED ON REQUEST This is general information. Depending on the engine model, deviations are possible WWW.HAMOFA.COM PARTS THAT ARE NOT INCLUDED, CAN BE OFFERED ON REQUEST This is general information. Depending on the engine model, deviations are possible WWW.HAMOFA.COM Additional Information MARKE RENAULT Replaces Ref. No. Agrale 6008099011006 Askam 25242T Astra 0010 7163 Astra 0017 4767 Astra 0819 0948 Astra 5 0313 7484 Astra 5 0313 7742 Bluebird 5008414 BMC 9P917828 DAF 1504900 DAF 1505970 DAF 1518683 DAF 1527756 DAF 6993878 DAF BBU8146 DAF BBU9424 Demag 76117673 Dennis 4324102227 Dennis 4324102227WHITE Dennis 6528852 ERF 1368731 Faun 99707305720 Fendt F 931 882 140 010 Fiat 0017 4767 Fiat 0190 0812 Fiat 0190 7612 Fiat 0299 2261 Fiat 0812 3564 Fiat 0819 0948 Fiat 1990 7612 Fiat 21 3091 2136 Fiat 5 0313 7484 Fiat 5 0313 7742 Fiat 58 0138 2289 Fiat 80 1011 2016 Fiat 8512 7004 Fiat 9844 6957 Fruehauf CF352490 Heuliez 0299 2261 Heuliez 5 0344 6090 Iveco 0017 4767 Iveco 0190 0812 Iveco 0190 7612 Iveco 0299 2261 Iveco 0812 3564 Iveco 0819 0948 Iveco 0819 0984 Iveco 17 4767 Iveco 190 7612 Iveco 1990 7612 Iveco 21 3091 2136 Iveco 299 2261 Iveco 5 0005 0616 Iveco 5 0313 5256 Iveco 5 0313 7484 Iveco 5 0313 7742 Iveco 50 0183 0112 Iveco 50 0186 5037 Iveco 50 0601 6342 Iveco 80 1000 2016 Iveco 80 1011 2016 Iveco 812 3564 Iveco 819 0948 JCB 15/920105 John Deere AL204884 Kamaz 00100000 King Long 35G4211501 Kögel 326549 Liebherr 571352308 Mack 950011 MAN 04.32410.2227 MAN 08.15210.2008 MAN 79.20036.1087 MAN 79.20036.1090 MAN 81.52102.0008 MAN 81.52102.0009 MAN 81.52102.0010 MAN 81.52102.0013 Ersetzt Ref. -

Final Frm Map.Qxd

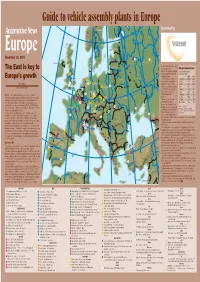

Guide to vehicle assembly plants in Europe NORWAY SWEDEN Sponsored by 33 16 ESTONIA 12 9 November 29, 2004 11 9 LATVIA 18 1 RUSSIA IRELAND DENMARK 21 greater worker flexibility and local U. K. LITHUANIA The East is key to sales growth, says Europe’s top producers 4 35 Felix Kuhnert, an auto consultant Vehicle assembly capacity, 12 for PricewaterhouseCoopers in 7 10 in thousands of units 12 14 7 29 southern Germany. 2004 2009 Europe’s growth “But being present in these 1. Germany 6,190 6,398 9 16 12 1 BELARUS 8 1 markets and the possibility to 2. France 4,356 4,500 7 6 2 7 JESSE SNYDER 5 10 4 export from there is another 3. Spain 3,329 3,318 14 4 NETH. 15 1 14 5 driver,” he said. “However, if you 4. UK 2,632 2,613 AUTOMOTIVE NEWS EUROPE 3 POLAND 6 19 look at the EU capacity trends 5. Russia 1,874 2,113 9 13 13 4 GERMANY through 2007 you also see 6. Italy 1,803 1,802 5 1 11 2 25 significant expansion in 7. Belgium 1,133 1,222 MUNICH – The manufacturing movement to the East continues. 2 5 BELGIUM 5 3 18 8 Germany.” 8. Turkey 1,003 1,105 New and expanded plants in eastern Europe have driven total vehicle 6 3 3 3 17 8 UKRAINE assembly capacity in greater Europe above 26 million units a year. 2 5 LUX. 19 Helped by the 2005 opening of 9. Poland 847 654 6 4 In central and eastern Europe, manufacturers are rapidly adding 31 1 7 CZECH a BMW plant in Leipzig, 10.Czech Rep. -

France Axa Private Equity Cède Sa Participation

BRÈVES DE 10H30 2013/04/12 FRANCE AXA PRIVATE EQUITY CÈDE SA PARTICIPATION MAJORITAIRE DANS AIXAM MEGA Axa Private Equity a cédé sa participation majoritaire dans Aixam Mega, groupe français spécialisé dans la production de voitures sans permis, à l’américain Polaris Industries. Aixam Mega gère deux usines de production en France et a généré en 2012 un chiffre d’affaires de 90 millions d’euros (5 000 voitures écoulées dans l’Hexagone). (Echos) Par Alexandra Frutos HEULIEZ A SIX MOIS POUR SURMONTER SES DIFFICULTÉS Heuliez a été placé en redressement judiciaire le 11 avril par le tribunal de commerce de Niort, qui lui a laissé six mois pour surmonter ses difficultés. Dans son jugement, le tribunal décrète le redressement judiciaire et accorde une période d’observation de six mois, laissant à l’administrateur du temps pour trouver un éventuel repreneur, alors que le carrossier de Cerizay (Deux-Sèvres) est en lice pour gagner un important contrat avec Volkswagen.(Figaro) Par Alexandra Frutos LA MORTALITÉ ROUTIÈRE A DIMINUÉ DE 26,8 % EN MARS ET DE 11,1 % AU PREMIER TRIMESTRE Le nombre de personnes décédées dans des accidents de la route a diminué de 26,8 % en mars (203 victimes) et de 11,1 % au premier trimestre (692 victimes). (Largus.fr) Par Alexandra Frutos LANCEMENT DES NOUVELLES SÉRIES SPÉCIALES PEUGEOT ROLAND GARROS Comme chaque année depuis 29 ans, le Tournoi de tennis de Roland Garros s’accompagne de la commercialisation de la série spéciale éponyme chez Peugeot. Trois modèles richement dotés sont concernés : la 207 CC, la 308 CC et le 3008. -

Transports ; Direction Des Transports Terrestres (1923-1989)

Transports ; Direction des transports terrestres (1923-1989) Répertoire (19920581/1-19920581/69) Archives nationales (France) Pierrefitte-sur-Seine 1992 1 https://www.siv.archives-nationales.culture.gouv.fr/siv/IR/FRAN_IR_018269 Cet instrument de recherche a été encodé en 2011 par l'entreprise diadeis dans le cadre du chantier de dématérialisation des instruments de recherche des Archives Nationales sur la base d'une DTD conforme à la DTD EAD (encoded archival description) et créée par le service de dématérialisation des instruments de recherche des Archives Nationales 2 Archives nationales (France) INTRODUCTION Référence 19920581/1-19920581/69 Niveau de description fonds Intitulé Transports ; Direction des transports terrestres Date(s) extrême(s) 1923-1989 Nom du producteur • Direction des transports terrestres Localisation physique Pierrefitte DESCRIPTION Présentation du contenu Sommaire Art 1-14 : Rapports d’inspection générale des directions départementales et régionales de l’équipement, fonctionnement de l’association des inspecteurs des transports, 1961-1984. Art 15-32 : Coopération internationale et accords en matière de transports :. PV de réunions des conseils des ministres de la CEE, 1961-1975. Travaux de la CEE consacrée à la mise en place de la Tarification d’Usage des Infrastructures (TUI), 1961-1981. PV de réunions de la Conférence Européenne des Ministres des Transports (CEMT), 1953-1988. Accords multilatéraux et bilatéraux, 1960-1989. Art 33-39 : Tutelle de la Caisse Autonome Mutuelle de Retraite (CAMR) et la Caisse Autonome de Retraites Complémentaires et de Prévoyance des Transports (CARCEPT) : Législation, réglementation, législation de la sécurité sociale, 1923-1986. Art 40-42 : Participation du Fonds de Développement Economique et Social (FDES) concernant la RATP et la SNCF : Projets d’investissements, compte rendus de réunions, 1981-1986. -

CNH Industrial Bus Brand, Heuliez Bus, Wins a Major Tender from the Paris Public Transport Operator, RATP, Thanks to Its Leadership in Hybrid Technologies

Corporate Communications CNH Industrial bus brand, Heuliez Bus, wins a major tender from the Paris public transport operator, RATP, thanks to its leadership in hybrid technologies The Paris, France transport operator, RATP (Régie Autonome des Transports Parisiens) recently launched a major European multi-year tender (2014-2017) for a contract for some 1,000 standard 12-metre hybrid and gas citybuses. Basildon, May 6, 2014 RATP, the Parisian public transport operator, has just awarded one of four tender lots to supply hybrid electric buses to Heuliez Bus, a French premium citybus specialist brand and hybrid bus pioneer, a brand of CNH Industrial. This is the first time in its history that Heuliez Bus has won a major tender from RATP with its GX 337 HYB model. This rewards the efforts of the company, which has pioneered the development of the hybrid bus market in France and continental Europe. These buses will be equipped with the ‘Arrive & Go’ function, which allows for arrivals and departures to be made in 100% electric mode from bus stops, offering a 5% reduction in fuel consumption. This is an innovative technology which represents a major evolution, from hybrid bus to full electric. Constant and smooth acceleration has significantly improved passenger and driver comfort and reduced noise levels benefit both passengers and local residents. To date, Heuliez Bus has delivered more than 165 hybrid buses, including 16 articulated buses for RATP, which have covered over nine million kilometres. The largest hybrid fleet in Europe operates in Dijon, France, with 102 standard 12m GX 327 HYB and articulated 18m GX 427 HYB buses. -

For Potential Foreign Investors & Business Partners

925<'1/'-;/*+ For Potential Foreign Investors & Business Partners 2009 ISBN 978-80-970068-6-0 Sponsored by The American Chamber of Commerce in the Slovak Republic © 2009, Published by ECENTER The American Chamber of Commerce in the Slovak Republic Founded in 1993, the American Chamber of Commerce (AmCham) in Bratislava is an indepen- dent and self-supported organization, relying entirely on contributions from its member compa- nies. Fifteen years after, this membership has grown to more than 300 international and Slovak companies, including a majority of the largest and most important ¿ rms in Slovakia. IMPORTANT ECONOMIC FIGURES 15 Years in Slovakia 20 Percentage of Slovakia´s GDP represented by AmCham members 320 Number of AmCham members* 130,000 Number of employees in AmCham membership 13,000,000,000 Total annual turnover in EUR represented by AmCham members * From the total of AmCham members, approximately 1/3 are subsidiaries of US companies, 1/3 are Slovak com- panies and 1/3 are multinational companies The American Chamber of Commerce in Slovakia Come join us! Crowne Plaza, Hodžovo nám. 2, 811 06 Bratislava Tel: (421-2) 5464 0534, Fax: (421-2) 5464 0535 We´re making E-mail: of¿ [email protected], Web: www.amcham.sk KOŠICE OFFICE: Hlavná 6, 040 01 Košice things happen! Tel./Fax: (421-55) 720 5218, E-mail: [email protected] amchamA52008.indd 1 26.9.2008 10:47:30 We provide help with research, consulting, coaching, management, implementation, and operations. ECENTER – helps its clients to excel Think, Work & Excel with us! ECENTER HELPS your business enter the Slovak market. -

Guide to Assembly Plants in Europe

AN_071112_16_17.qxd 3/13/08 4:11 PM Page 16 PAGE 16 · www.autonew seurope.com November 12, 2007 Guide to assembly plants in Europe BMW GROUP A San Benedetto Val di Sangro, Italy (Sevel Sud: Fiat 50%, (2008). Note: GM has temporary plant on site until 4 Flins, France – Renault Clio III, Clio II (See also 3 , 25 ) PSA 50%) – Citroen Jumper/Relay; Fiat Ducato; permanent plant opens in 2008. 5 Maubeuge, France – Passenger cars: Kangoo, new 1 Dingolfing, Germany – BMW 5-series sedan, station Peugeot Boxer 11 Asaka, Uzbekistan (UzDaewoo: joint venture of GM, Kangoo; LCV: new Kangoo Express, new Kangoo Express wagon, 6-series coupe, convertible, 7-series sedan, B Lieu Saint-Amand, France (Sevel Nord: Fiat 50%, PSA GM Daewoo and Uzautosanoat) – Daewoo Tico, Matiz, Compact; Nissan Kubistar M5 sedan, station wagon, M6 coupe, convertible 50%) – Citroen Atlante/C8, Dispatch/Jumpy; Fiat Scudo, Damas, Nexia, Lacetti; (from kits** starting in 2008) 6 Sandouville, France – Renault Laguna III Sport Tourer and 2 Leipzig, Germany – BMW 1-series 3 door, coupe, Scudo Panorama, Ulysse; Lancia Phedra; Peugeot 807, Chevrolet Epica, Tacuma, Captiva hatchback, Espace IV, Vel Satis convertible, 3-series sedan Expert, TePee A Togliatti, Russia (joint venture of GM and AvtoVAZ) – 7 Palencia, Spain – Renault Megane II hatchback, sport 3 Munich, Germany – BMW 3-series sedan, station wagon Chevrolet Niva, Viva; Opel car (2008) hatch, sport station wagon 4 Regensburg, Germany – BMW 1-series 5 door, 3-series FORD B Warsaw, Poland (FSO: UkrAvto 60%, GM Daewoo 40%) – 8 Valladolid, -

Acronimos Automotriz

ACRONIMOS AUTOMOTRIZ 0LEV 1AX 1BBL 1BC 1DOF 1HP 1MR 1OHC 1SR 1STR 1TT 1WD 1ZYL 12HOS 2AT 2AV 2AX 2BBL 2BC 2CAM 2CE 2CEO 2CO 2CT 2CV 2CVC 2CW 2DFB 2DH 2DOF 2DP 2DR 2DS 2DV 2DW 2F2F 2GR 2K1 2LH 2LR 2MH 2MHEV 2NH 2OHC 2OHV 2RA 2RM 2RV 2SE 2SF 2SLB 2SO 2SPD 2SR 2SRB 2STR 2TBO 2TP 2TT 2VPC 2WB 2WD 2WLTL 2WS 2WTL 2WV 2ZYL 24HLM 24HN 24HOD 24HRS 3AV 3AX 3BL 3CC 3CE 3CV 3DCC 3DD 3DHB 3DOF 3DR 3DS 3DV 3DW 3GR 3GT 3LH 3LR 3MA 3PB 3PH 3PSB 3PT 3SK 3ST 3STR 3TBO 3VPC 3WC 3WCC 3WD 3WEV 3WH 3WP 3WS 3WT 3WV 3ZYL 4ABS 4ADT 4AT 4AV 4AX 4BBL 4CE 4CL 4CLT 4CV 4DC 4DH 4DR 4DS 4DSC 4DV 4DW 4EAT 4ECT 4ETC 4ETS 4EW 4FV 4GA 4GR 4HLC 4LF 4LH 4LLC 4LR 4LS 4MT 4RA 4RD 4RM 4RT 4SE 4SLB 4SPD 4SRB 4SS 4ST 4STR 4TB 4VPC 4WA 4WABS 4WAL 4WAS 4WB 4WC 4WD 4WDA 4WDB 4WDC 4WDO 4WDR 4WIS 4WOTY 4WS 4WV 4WW 4X2 4X4 4ZYL 5AT 5DHB 5DR 5DS 5DSB 5DV 5DW 5GA 5GR 5MAN 5MT 5SS 5ST 5STR 5VPC 5WC 5WD 5WH 5ZYL 6AT 6CE 6CL 6CM 6DOF 6DR 6GA 6HSP 6MAN 6MT 6RDS 6SS 6ST 6STR 6WD 6WH 6WV 6X6 6ZYL 7SS 7STR 8CL 8CLT 8CM 8CTF 8WD 8X8 8ZYL 9STR A&E A&F A&J A1GP A4K A4WD A5K A7C AAA AAAA AAAFTS AAAM AAAS AAB AABC AABS AAC AACA AACC AACET AACF AACN AAD AADA AADF AADT AADTT AAE AAF AAFEA AAFLS AAFRSR AAG AAGT AAHF AAI AAIA AAITF AAIW AAK AAL AALA AALM AAM AAMA AAMVA AAN AAOL AAP AAPAC AAPC AAPEC AAPEX AAPS AAPTS AAR AARA AARDA AARN AARS AAS AASA AASHTO AASP AASRV AAT AATA AATC AAV AAV8 AAW AAWDC AAWF AAWT AAZ ABA ABAG ABAN ABARS ABB ABC ABCA ABCV ABD ABDC ABE ABEIVA ABFD ABG ABH ABHP ABI ABIAUTO ABK ABL ABLS ABM ABN ABO ABOT ABP ABPV ABR ABRAVE ABRN ABRS ABS ABSA ABSBSC ABSL ABSS ABSSL ABSV ABT ABTT -

A Second Automobile Revolution? Firms Strategies and Public Policies

« The Greening of the Global Auto Industry in a Period of Crisis », 18th International GERPISA colloquium 9-11 June 2010, Berlin A Second Automobile Revolution? Firms strategies and public policies Michel Freyssenet CNRS Paris GERPISA international network The hypothesis of a Second Automobile Revolution • It was proposed in the last GERPISA book published in spring 2009 • To consolidate this assertion, we undertook for the last GERPISA colloquium in Paris (june 2009) to compare the present situation to the first automobile revolution period • One year later, how far have we got? Declining oil and gas stocks by world resident May 2010 oil prices… at the level of May 2007 The hypothesis of a Second Automobile Revolution • It was proposed in the last GERPISA book published in spring 2009 • To consolidate this assertion, we undertook for the last GERPISA colloquium in Paris (june 2009) to compare the present situation to the first automobile revolution period • One year later, how far have we with it? Four conditions and stages for a revolution in transport system The analisis of the First Automobile Revolution period came into sight four main conditions and stages for an automobile revolution • The crisis of the previous transport system • The emergence of various solutions, combining and adaptating innovations often coming from other sectors • The formation of a coalition of forces for one of the solutions, despite its great uncertainties and its disavantages, through a societal battle • Macroeconomic decisions and public policies allowing the diffusion and the generalization of adopted solution Today, the first and the second conditions and stages are probably fulfiling • The crisis of the petrol automobile system: - fast rise of the use costs, - growing gap of productivity with the other activities, - profitability drop of auto industry, - fall of use value of the automobile because of congestion, pollution, growing costs of the externalities, accidents, - etc. -

IP Auto TP TL Final.Indd

Intellectual property in the automotive industry Transfer pricing aspects Intellectual property in the automotive industry Transfer pricing aspects Introduction 1 What types of intellectual property are there? 2 Why is this such an important issue in the automotive industry? 4 Implications for measuring intellectual property in the automotive industry 5 • A typical analysis 5 • An alternative view 6 Summary 9 Introduction Transfer pricing taxation rules place a huge burden on multinational taxpayers. These rules exist to ensure that companies adhere to the “arm’s-length principle” (where economic conditions between two unconnected enterprises refl ect those that would exist between independent enterprises1) when pricing transactions between their affi liates. These rules apply to intangible and tangible product fl ows, and it becomes a diffi cult yet important analysis when different parts of a global organisation contribute or exploit intellectual property (IP). It has been calculated that such knowledge assets now comprise a greater share of public companies’ market values than their hard assets,2 so such intangibles are vital to shareholders, too. Most importantly, from a transfer pricing perspective, the way intellectual property is created, used and shared drives the way profi ts are recognised for tax purposes. This is an increasingly signifi cant focus for tax authorities, which perceive substantial profi ts made at a (consolidated) group level are not necessarily replicated at a local level. This area involves a great deal of judgment, and much reliance is placed on the principles presented in the Organisation of Economic Co-operation Development (OECD) guidelines.3 The intention of the guidelines is to promote the arm’s-length principle, but the guidelines acknowledge that this principle can be diffi cult to apply to intangible property because such property may have a special character. -

7/3689-Couverture Ccfa Gb

2000 EDITION ANALYSIS AND STATISTICS THE FRENCH AUTOMOTIVE INDUSTRY THE FRENCH AUTOMOTIVE INDUSTRY - 2000 EDITION INDUSTRY THE FRENCH AUTOMOTIVE Comité des Constructeurs Français d’Automobiles Comité des Constructeurs Français d’Automobiles 2, rue de Presbourg – 75008 Paris – Tél. : 01 49 52 51 00 – Télécopie : 01 47 20 02 46 – www.ccfa.fr CHAIRMAN’S MESSAGE The French automobile market enjoyed a firm, solid upswing in 1999, impelled by renewed confidence as the economy improved, the steady introduction of new models, declining prices and lower more consumer-friendly interest rates. All in all, 1999 was an excellent year, and 2000 may turn out to be the best of the decade. Demand was also strong in Western Europe, where 15 million new vehicles were sold, and French automakers reported faster growth than other marques. Global production of French automakers reached a record level of more than 4,800,000 units. While underpinning the market, confidence is also crucial to the special relation- ships that link customers and their dealer networks. The automobile, which is both a source of pleasure and a means of transportation, is not an ordinary product. Maintaining selective and exclusive distribution channels safeguards the interests of consumers, dealer networks and manufacturers. In this way, it guarantees balance and consistency for all parties, while enabling the develop- ment of sales practices and structures based on future-oriented approaches and methods. The Comité des Constructeurs Français d’Automobiles has expanded its commu- nications strategy to include topics addressing the relationship between the auto- mobile and society, in particular the environment, transport modes and safety. -

Modèles De Voitures Électriques

Modèles de voitures électriques Electric cars Catalog This page has been updated 30 sept 2010 The TESLA ROADSTER (first photo), is a 2-seater electric sports car, 0 to 100 km/h in less than 4 secondes. The price tag starts at 100 000 dollars. Leonardo di Caprio was one of the first clients. The same company, TESLA MOTORS, prepares the TESLA MODEL S (second photo below), a real family-car which will be the most performing electric family vehicle. It should be available in 2012 (450 km range, enough space for 5 adults and 2 children, a real trunk, a real car. It is expected to cost 42 300 Euros. The MIA by HEULIEZ, a nice little car, available in 2012 in France 1 of 5 20/10/10 5:31 Modèles de voitures électriques The pionneers, first cars that made it to the market (below) : the REVA (left) and the MEGA-CITY (right) The first electric car to be mass-produced will be the NISSAN LEAF by Renault-Nissan . The LEAF is available since december 2010 in California, Ireland, Israel, Denmark, Japan... and will be available in other regions of the world in 2012. Here is a photo of the Nissan Leaf : Below is a catalog of the vehicles that are on the market or in fabrication. Small cars (less than 3 meters long or maximum speed < 90 km/h or range <100 km) Weight of Long Name of Type of Type of Fabricant Availability Max speed Range Number empty car x Web car car battery (country) of seats (max charge) large (m) Small MEGA-Aixam Available : 60 à 100 750 kg 2,959 Mega-City car lead (France) delivery in 65 km/h km 2 or 4 (1025) x http://www.nicecarcompany.co.uk/m