Intercontinental Hotels Group PLC 2021 First Quarter Trading Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Partnering with Intercontinental Hotels Group Fiesta Resort Guam to Become First Crowne Plaza Brand in Micronesia from 2021

Partnering with Intercontinental Hotels Group Fiesta Resort Guam to become first Crowne Plaza brand in Micronesia from 2021 (15 October 2019 – HONG KONG)S.A.I. Leisure Group Company Limited (the “Company” or “S.A.I Leisure Group”) and its subsidiaries (collectively, the “Group”), is pleased to announce our Fiesta Resort Guam becomes part of the IHG system starting October 15, 2019. The Group signed a hotel management agreement with InterContinental Hotels Group (“IHG”) to manage Fiesta Resort Guam on September 10, 2019. A multi-million dollar refurbishment plan is also in place to commence and Fiesta Resort Guam will be rebranded as Crowne Plaza Resort Guam in early 2021. The Group is enthusiastic about the cooperation with IHG. IHG has extensive experience in operating hotels and resorts that cater to Japanese, Korean and Chinese guests, with more than 400 hotels across China and Korea, and 32 hotels in Japan. This experience will bring about new inspiration and marketing for Guam, and further enhance offering on the island. Management is confident that the agreement will strengthen the future prospects of Fiesta Resort Guam and bring together the best of both worlds. Dr. Henry Tan, BBS, JP, Chief Executive Officer of S.A.I. Leisure Group commented, “The partnership with IHG and the refurbishment will significantly elevate the positioning and service level of the resort and bring in a new exciting option for the visitors of Guam. Fiesta Resort Guam has enjoyed a privileged location and developed a good reputation over the years. To grow into the future, we need a global brand like Crowne Plaza to attract guests from all around the world and bring a new level of hospitality to Guam. -

Say “Hello” to the Future of Holiday Inn the Holiday Inn® Brand Is an Enduring Icon with Unmatched Recognition

Say “hello” to the future of Holiday Inn The Holiday Inn® brand is an enduring icon with unmatched recognition. That legacy shapes our present and informs our future as we continue to offer services and amenities that enable real, human connections. As we look to the future, we’ve developed a more streamlined, flexible building to meet your market needs. Questions about the new design? Experience our virtual hotel and get more information on design.holidayinn.com. Prototype Site Plan Details Acreage 2.57 acres Building Gross Building Area 73,461 sq ft Summary Number of Floors 4 stories Total Room Count 125 Gross Building Area per Key 588 sq ft Parking Spaces 127 Pool Outdoor or indoor Guest Room Public Space King 323 sq ft Lobby 2,097 sq ft Queen / Queen 323 sq ft Restaurant & Bar 1,820 sq ft Junior Suite 417 sq ft Meeting Space 1,581 sq ft Unified room bays with the fl exibility to offer King, Queen/Queen, Fitness Center & Rec. Lobby 1,337 sq ft King Comfort, King Sleeper in same size bay Open lobby with flexible space to socialize or work Multi-functional storage with integrated power and arrival moment Market 24 positioned to work with front desk or F&B concept Quality bedding and blackout shades for a great night’s sleep Flexible set of food & beverage concepts and meeting room offerings Spacious well-lit bathroom with branded shower experience to best suit your specific market needs Back of House Kitchen Catering Prep All other areas 632 sq ft 202 sq ft 3,104 sq ft ThisGet is not a anvirtual offer of atour franchise. -

Runaway Runways

RUNAWAY RUNWAYS US$1,009,008,000 Anticipated global spend on business travel by year-end 2011, UK airports have the runway capacity to be handling 540 million against US$924bn in 2010. passengers per annum (mppa) by 2050, compared with the 372m they processed in 2008, according to latest Department for Transport forecasts. All but 7m of the 168m extras passengers 5.4% per annum could be handled by regional airports – with the exception of Luton, Anticipated increase in UK spend on business travel over the next London’s gateways are full – provided additional terminal capacity is fi ve years, against 3.8% per annum in the US, 3.3% in France and made available and Plymouth and Coventry are re-opened. 2.9% in Germany. mppa mppa 11.2% per annum AIRPORT 2008 2050 Anticipated increase in China’s spend on business travel over the next fi ve years, against 10.8% per annum in India, 7.1% in Russia LONDON AIRPORTS and 7% in Brazil. Heathrow 86 86 Source: GBTA Foundation Gatwick 42 42 Stansted 35 35 Luton 10 17 London City 8 8 76,151 LONDON TOTAL 181 188 The number of car hire transactions recorded by Guild of Travel Management Companies (GTMC) members during the third quarter (to September) of 2011. This fi gure is a 16% increase on REGIONAL AIRPORTS the same quarter in 2010. Aberdeen 5 10 Source: GTMC Belfast International 10 23 Belfast City 4 4 Birmingham 18 27 ACTE/KDS STUDY 2011: IMPACT OF GLOBAL Bournemouth 26 EVENTS – HAVE YOU HAD TO RE-SCHEDULE OR Bristol 712 CANCEL A TRIP FOR THESE REASONS? Cardiff 12 12 East Midlands 25 25 Edinburgh 20 20 -

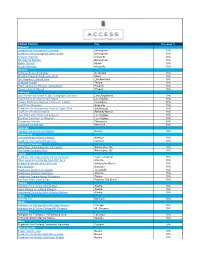

Arcis Access ALL Participating Hotels.Xlsx

UNITED STATES City Discount % Alabama Hampton Inn Birmingham-Colonnade Birmingham 10% Residence Inn Birmingham Dtwn at UAB Birmingham 10% Huntsville Marriott Huntsville 10% Birmingham Marriott Birmingham 10% Mobile Marriott Mobile 10% Westin Huntsville Huntsville 10% Arizona Embassy Suites Scottsdale Scottsdale 10% Sheraton Mesa at Wrigleyville West Mesa 10% The Wigwam Litchfield Park Litchfield Park 10% Graduate Tempe Tempe 10% Hilton Garden Inn Phoenix Airport North Phoenix 10% Phoenix Airport Marriott Phoenix 10% California Lake Arrowhead Resort & Spa, Autograph Collection Lake Arrowhead 10% Four Points Los Angeles Int'l Airport Los Angeles 10% Crowne Plaza Los Angeles Commerce Casino Commerce 10% Hyatt Place Riverside Riverside 10% Residence Inn Sacramento Dtwn at Capitol Park Sacramento 10% Doubletree Berkeley Marina Berkeley Marina 10% Luxe City Center Hotel Los Angeles Los Angeles 10% Sheraton Gateway Los Angeles Los Angeles 10% Pleasanton Marriott Pleasanton 10% Kenwoord Inn and Spa Kenwood 30% Colorado Hampton Inn Denver Int'l Airport Denver 10% Connecticut Hartford/Windsor Marriott Airport Windsor 10% Residence Inn Hartford Downtown Hartford 10% District of Columbia Hyatt Place Washington DC/US Capitol Washington, DC 10% The Fairfax Embassy Row Washington, DC 10% Florida Residence Inn Cape Canaveral Cocoa Beach Cape Canaveral 10% Hilton Garden Inn Orlando East/UCF Area Orlando 10% Newport Beachside Hotel & Resort Sunny Isles Beach 10% Aloft Sarasota Sarasota 10% Doubletree Jacksonville Airport Jacsonville 10% Doubletree Orlando Downtown Orlando 10% Doubletree Tampa Airport-Westshore Tampa 10% Bay Point Golf Resort & Spa Panama City Beach 10% Georgia Hampton Inn & Suites Atlanta-Dtwn Atlanta 10% Hilton Garden Inn Atlanta Midtown Atlanta 10% Homewood Suites by Hilton Atlanta Midtown Atlanta 10% Idaho Knob Hill Inn Ketchum 30% Illinois Hampton Inn Chicago Dtwn Michigan Avenue Chicago 10% Hampton Inn & Suites Chicago/Mt. -

Recognized at the Haute Grandeur Global Hotelawards

ANA InterContinental Beppu Resort and Spa Recognized at the Haute Grandeur Global HotelAwards 2020 WINNER Beppu, Oita - 28, September 2020 – It is with great pride, we announce that ANAInterContinental Beppu Resort and Spa was awarded in four continental categories at the recent Haute Grandeur Global Excellence Awards. After a two month rating process from June 16 to August 16, 2020, the resort received thefollowing awards: Best Hideaway Resort in Asia, Best Hot Spring Resort in Asia, Best Spa Hotel in Asia, and Most Luxurious Suite in Asia. The first of its kind in Oita Perfecture and the first onsen resort for InterContinental Hotels Group (IHG), the resort is the best of Japan’s healing culture and tradition with the IHG brand of luxury and the unique lifestyle spa concept of HARNN Global. Introducing ANA Intercontinental Beppu Resort&spa Located in the Oita Prefecture in Southwestern Japan, the world-class resort opens as the region’s first international luxury resort, offering sophisticated travellers a unique fusion of traditional hot spring culture and the InterContinental brand’s promise of modern design, award-winning dining and world-class service. roomswith bold designs. The 89 guest rooms, including 10 suites, range from a luxurious 62-212 square meters, including large onsen or hot baths, spacious design and an abundance of natural materials for a sense of relaxation. All Suites and 3Club InterContinental rooms feature private open-air baths on the terrace with views sweeping the Beppu Bay. Website: https://anaicbeppu.com/ -

HVS Asia-Pacific Hotel Operator Guide Excerpt 2016

2016 EDITION | Price US$800 SUMMARY THE ANNUAL HVS ASIA-PACIFIC HOTEL OPERATOR GUIDE (AS OF 31 DECEMBER 2015) Setthawat Hetrakul Assistant Manager Daniel J Voellm Managing Partner HVS.com HVS | Level 21, The Centre, 99 Queen’s Road Central, Hong Kong The HVS Asia-Pacific Hotel Operator Guide 2016 Foreword It is with great pleasure that I share with you our third annual Asia-Pacific Operator Guide, data as of 31 December 2015. This third edition will continue to serve owners as a reference for which operator has a strong presence in their home market and in potential future markets further ashore as well as key feeder markets across the region. With China rapidly becoming a strong outbound market, brands and operators that are well positioned there are better positioned to welcome Chinese travelers overseas. Branding, anchored by the management expertise and distribution power that operators bring to a hotel property, is becoming more and more critical. In the face of increasing competition, non-branded properties often perform at a discount to their branded peers due to lack of awareness and quality assurance. Running a hotel is no easy task and owners have a tendency to view operators’ fees as unjustified for the value they deliver. It is essential that owner and operator align their interest from very early in the process and work towards a common goal, rather than start their long-term relationship from conflicting standpoints. In this third edition, we have captured close to one million existing and more than half a million pipeline rooms spread over 6,546 properties. -

Your Wedding At

Your Wedding at DAKOTA EVENT CENTER.COM 716 LAMONT ST | ABERDEEN, SD 57401 Dear Wedding Planners, The Dakota Event Center featuring Mavericks Steak & Cocktails, the Holiday Inn Express Hotel & Suites and the Hampton Inn & Suites of Aberdeen is pleased to have the opportunity to host your special day. Lodging provided by: Catering by: Lodging Lodging Holiday Inn Express Hotel & Suites Hampton Inn Hotel & Suites www.hiexpress.com/aberdeensd www.hamptoninn.com (605) 725-4000 (605) 262-2600 For Reservations: For Reservations: 800-HOLIDAY 800-HAMPTON 3310 7th Ave SE 3216 7th Ave SE Aberdeen, SD 57401 Aberdeen, SD 57401 We are Aberdeen’s finest hotels featuring over 150 deluxe non-smoking sleeping rooms and suites between the two properties. Both hotels are connected by enclosed walkways to the event center which houses Mavericks Steak & Cocktails. All of our rooms feature comfortable pillow top king or queen beds, spacious work areas, free high-speed wireless internet, 37’’ high-definition LCD televisions, in-room coffee makers and complimentary hot breakfast. We also have rooms with whirlpool suites for those special occasions. Both hotels have fitness rooms, business centers and pool areas, with the Holiday Inn Express showcasing a 150 foot waterslide in the water park. The hotels are located on Aberdeen’s east side on Highway 12 across from the Lakewood Mall and Target, Wal-Mart and Culver’s Restaurant are all within walking distance. Storybook Land in Wylie Park, Lee Park Golf course and Rolling Hills Golf course are also just a few short minutes from the hotels. You will be able to block rooms at each of the hotels to accommodate all of your guests. -

Copy of Hotelpickuptimesupdated17 (Full)

Monterey, Carmel and the 17-Mile Drive Day Tour Depart time: 8:00am @ 478 Post Street, San Francisco FISHERMAN'S WHARF AREA HOTELS ADDRESS Estimated Time HOLIDAY INN - GOLDEN GATEWAY HOLIDAY INN GATEWAY-1500 VAN NESS AVE. NOB HILL MOTOR INN NOB HILL MOTOR INN 1630 PACIFIC AVE CASTLE INN CASTLE INN MOTEL 1565 BROADWAY/VANNESS INN AT BROADWAY INN AT BROADWAY 2201 VAN NESS AVE. 7:10-7:25 DA VINCI VILLA DA VINCI VILLA 2550 VANNESS /FILBERT AMERICAS BEST INN F.W. BEST INN &SUITES 2850 VANNESS @ CHESTNUT FAIRMONT HERITAGE PLACE FAIRMONT HERITAGE PLACE 900 NORTH POINT ST. SUITES AT FISHERMAN'S WHARF SUITES FW @ 2655 HYDE ST. COLUMBUS MOTOR INN COLUMBUS MOTOR INN 1075 COLUMBUS/CHESTNUT WASHINGTON SQUARE INN WASHINGTON SQUARE INN 1660 STOCKTON/FILBERT HOTEL BOHEME BOHEME 444 COLUMBUS AVE / STOCKTON 7:15-7:30 ROYAL PACIFIC MOTOR INN ROYAL PACIFIC 661 BROADWAY/STOCKTON "SW" HOTEL SAM WONG HOTEL 615 BROADWAY/STOCKTON CLUB QUARTERS CLUB QUARTERS 424 CLAY/SANSOME HYATT REGENCY EMBARCADERO HYATT REGENCY EMB 5 EMBARCADERO ST. (P/U ON DRUMM STREET) LE MERIDIAN SF LE MERIDIAN CLAY @ 333 BATTERY LOEWS REGENCY (AKA:MANDARIN ORIENTAL)MANDARIN 222 SANSOME/PINE OMNI HOTEL OMNI HOTEL 500 CALIFORNIA @ MONTGOMERY 7:20-7:30 HILTON FINANCIAL DISTRICT HILTON FINANCIAL DISTRICT 750 KEARNEY ST. STANFORD COURT STANFORD COURT ON CALIFORNIA ST. SAN FRANCISCO SUITES SF SUITE 710 POWELL (P/U) @ PINE ST. POWELL PLACE POWELL PLACE 730 PINE ST./POWELL ST. FAIRMONT HOTEL FAIRMONT 950 MASON/CALIFORNIA INTERCONTINENTAL MARK HOPKINS INTERCONTINENTAL MARK HOPKINS 999 CALIFORNIA ST. PACIFIC TRADEWINDS HOSTEL PACIFIC TRADEWINDS HOSTEL 680 SACRAMENTO ST. -

Holiday Inn Express® & Suites Naples Downtown 5Th Avenue Opens

FOR IMMEDIATE RELEASE Contact: Paul Sutton Holiday Inn Express & Suites Naples Downtown 5th Avenue [email protected] 1-647-567-4564 HOLIDAY INN EXPRESS® & SUITES– NAPLES DOWNTOWN 5TH AVENUE OPENS Renovated hotel located on Florida’s Paradise Coast ATLANTA (Nov. 22, 2013) — InterContinental Hotels Group (IHG) [LON:IHG, NYSE:IHG (ADRs)] today announced the opening of the 124-room Holiday Inn Express Hotel & Suites Downtown 5th Avenue. The newest Palm Holdings hotel brings quality service and familiar comfort to Naples with the completion of a $4 million re-branding and renovation to the entire interior and exterior of the former Paradise Coast Hotel and Suites. This property’s smart brand, convenient location and abundant amenities make it an ideal choice for travelers to Naples Florida, located on Florida’s Paradise Coast. "Holiday Inn Express hotels are designed to be the smart choice for value-conscious business and leisure travelers," said Heather Balsley, senior vice president, Americas Holiday Inn® Brand Family, IHG. "With more than 2,200 properties worldwide and 450 more in the pipeline, the Holiday Inn Express portfolio continues to provide our guests with an enhanced-stay experience at a great value. We are proud to welcome this hotel into the Holiday Inn brand family with the brand-new sign and everything it represents.” The hotel is within walking distance to the entertainment, shopping and business districts, trendy boutiques and art galleries and the Naples Pier. The hotel is also a convenient 30 minutes from South West Florida International Airport (RSW) in Fort Myers and 45 minutes from Everglades National Park. -

Ackerman and Greenstone Secure Financing, Sign 20‐Year Franchise Agreement with IHG for Crowne Plaza® Riverside Village Hotel in North Augusta, South Carolina

FOR IMMEDIATE RELEASE For more information, contact: Harvey Rudy 678.589.7619 hrudy@greenstone‐properties.com Ackerman and Greenstone Secure Financing, Sign 20‐Year Franchise Agreement with IHG for Crowne Plaza® Riverside Village Hotel in North Augusta, South Carolina North Augusta, S.C., January 25, 2018 – Ackerman & Co. and Greenstone Properties today announces that they have broken ground and secured financing for the development of the new‐build Crowne Plaza® Riverside Village hotel – a five‐story, 180‐key hotel located within the Riverside Village mixed‐use project in North Augusta, S.C., along the Savannah River. The partner companies have signed a 20‐year franchise agreement with InterContinental Hotels Group® (IHG®), one of the world’s leading hotel companies. Slated to open by the end of 2018, the hotel project – adjacent to the new Augusta GreenJackets’ SRP Park – will feature modern rooms and suites, the Wood Fired Grill restaurant, an outdoor pool and event space, a fitness center, a rooftop bar, and more than 7,000 square feet of conference center and meeting space with a ballroom and several meeting rooms. A 417‐space parking deck will provide hotel, ballpark and residential parking. “This is an important milestone in the development of Riverside Village, a project that will provide outstanding amenities for visitors and the local community as well as a catalyst for further economic development,” said Robert Pettit, Mayor of North Augusta. The 30‐acre, $200‐million Riverside Village live‐work‐play development combines apartment, single‐ and multi‐family living, a vibrant town center featuring high‐quality office space, premier national and local retailers, and diverse dining options, in addition to the new GreenJackets’ ballpark. -

Meeting Guide for Enhanced Care PPO (ECP) Non-Medicare UAW

Meeting guide Enhanced Care PPO (ECP) for non-Medicare UAW Trust members All states New for 2019 We want to help you get 1 great plan. familiar with your new Blue Cross Blue Shield of Michigan health care plan, Enhanced 3 ways to learn about it. Care PPO (ECP). Join us in person, by teleconference or for a webinar to get key information about your new and improved health care plan, and learn why you’ll have convenience and care like never before. Registration is required. Reserve your spot for an in-person meeting, teleconference or webinar at bcbsm.com/uawtrust or call 1-877-395-7758 Monday through Friday from 8:30 a.m. to 8 p.m. Eastern time. 2018 meeting schedule In-person meetings Join us in a city near you. Each meeting is about an hour and a half long and will start promptly at 10 a.m. and 2 p.m. local time. Alabama Florida Florence Sarasota Wednesday, September 26 Monday, November 19 Marriott Shoals Hotel & Spa Holiday Inn Sarasota – Airport 10 Hightower Place, Florence, AL 35630 8009 15th St. E., Sarasota, FL 34243 Huntsville Tampa Tuesday, September 25 Tuesday, November 20 Huntsville Marriott Space & Rocket Center Four Points Sheraton Suites Tampa Airport 5 Tranquility Base, Huntsville, AL 35805 4400 W. Cypress St., Tampa, FL 33607 Delaware Georgia Wilmington Peachtree Corners Tuesday, September 18 Thursday, September 27 DoubleTree Hotel Wilmington Atlanta Marriott Peachtree Corners 4727 Concord Pike, Wilmington, DE 19803 475 Technology Parkway NW Peachtree Corners, GA 30092 Indiana Flint Indianapolis Tuesday, October 2 Monday, October 15 Tuesday, October 23 Tuesday, October 16 Holiday Inn Gateway Centre Wyndham Indianapolis West 5353 Gateway Centre, Flint, MI 48507 2544 Executive Drive, Indianapolis, IN 46241 Grand Rapids Kokomo Thursday, October 11 Wednesday, October 17 DoubleTree Grand Rapids Hotel Rozzi’s Catering Continental Ballroom 4747 28th St. -

AWARD BRAND HOTEL NAME Torchbearer Candlewood Suites TERRE HAUTE Torchbearer Candlewood Suites CLEARWATER Torchbearer Candlewood

2019 IHG® HOTEL AWARD WINNERS AWARD BRAND HOTEL NAME TorchBearer Candlewood Suites TERRE HAUTE Torchbearer Candlewood Suites CLEARWATER TorchBearer Candlewood Suites COLUMBIA HWY 63 & I-70 TorchBearer Candlewood Suites CUT OFF - GALLIANO TorchBearer Candlewood Suites KEARNEY TorchBearer Candlewood Suites LOVELAND TorchBearer Candlewood Suites PENSACOLA - UNIVERSITY AREA TorchBearer Candlewood Suites LONGMONT TorchBearer Candlewood Suites OMAHA - MILLARD AREA TorchBearer Candlewood Suites WACO TorchBearer Candlewood Suites CHICAGO/LIBERTYVILLE TorchBearer Candlewood Suites CHICAGO-WAUKEGAN TorchBearer Candlewood Suites COLUMBUS AIRPORT TorchBearer Crowne Plaza SEATTLE-DOWNTOWN TorchBearer EVEN NEW YORK - TIMES SQUARE SOUTH TorchBearer Holiday Inn LA PIEDAD TorchBearer Holiday Inn MEXICO CITY-PLAZA UNIVERSIDAD TorchBearer Holiday Inn LONGVIEW - NORTH TorchBearer Holiday Inn DENVER TECH CENTER-CENTENNIAL TorchBearer Holiday Inn SELMA-SWANCOURT TorchBearer Holiday Inn ST. GEORGE CONV CTR TorchBearer Holiday Inn EAU CLAIRE SOUTH I-94 TorchBearer Holiday Inn INDIANAPOLIS AIRPORT TorchBearer Holiday Inn MONTERREY NORTE TorchBearer Holiday Inn MAZATLAN TorchBearer Holiday Inn OWENSBORO RIVERFRONT TorchBearer Holiday Inn CHILPANCINGO TorchBearer Holiday Inn Club Vacations SUNSET COVE RESORT TorchBearer Holiday Inn Express AUGUSTA NORTH - GA TorchBearer Holiday Inn Express SHARON-HERMITAGE TorchBearer Holiday Inn Express OAXACA-CENTRO HISTORICO TorchBearer Holiday Inn Express COLUMBUS TorchBearer Holiday Inn Express COON RAPIDS-BLAINE AREA TorchBearer