Steel-June-2020.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ecor AARTI STEELS LTD SDG ASGN Ecor BADEARAPUR BDXX Ecor GCB SIDING PARADEEP PORT, PARADEEP CBSP Ecor DAITARI DATR Ecor HIRAKUD

Annexure I (Para 1.9) List of loading points selected in sample S.no ZR Name of loading points Code 1 ECoR AARTI STEELS LTD SDG ASGN 2 ECoR BADEARAPUR BDXX 3 ECoR GCB SIDING PARADEEP PORT, PARADEEP CBSP 4 ECoR DAITARI DATR 5 ECoR HIRAKUD HKG 6 ECoR JAGDALPUR JDB 7 ECoR KIRANDUL KRDL 8 ECoR LAPANGA LPG 9 ECoR ARYAN ISPAT & POWER PVT. LTD MAIL 10 ECoR BHUSHAN STEEL LTD. SIDING MBMB 11 ECoR NMDC IRON ORE LOADING DEPOSITE NO. 5 SIDING - BACHELI NMDB 12 ECoR NMDC'S MALLINGER VALLEY SDG, KIRANDUL NMVK 13 ECoR NERGUNDI JN. NRG 14 ECoR NAYAGARH NYG 15 ECoR PORJANPUR PRNR 16 ECoR RENGALI RGL 17 ECoR SUKINDA ROAD SKND 18 ECoR VISHAKHAPATNAM-PORT VZP 19 SER BARBIL BBN 20 SER BARA JAMDA JN. BJMD 21 SER BADAMPAHAR BMPR 22 SER BANSPANI BSPX 23 SER BIMLAGARH JN. BUF 24 SER BARSUAN BXF 25 SER BOLANI FINE ORE OF M/S BSL BYFS 26 SER BOLANIKHADAN BYX 27 SER DEOJHAR DJHR 28 SER M/S ESSEL MINING & INDURSTRIES LTD'S PVT. SDG. EMIJ 29 SER NEW BUNKER SIDING OF M/S SAIL (NMDC) AT KRBU FOS 30 SER GUA GUA 31 SER GORUMAHI SANI GUMI 32 SER HINDUSTAN STEEL LTD. HLSR 33 SER M/S IRON & STEEL CO. SDG, MANOHARPUR IISM 34 SER BASPANI IRON ORE LTD. JARULI IOJB 35 SER BUNKER SIDING AT GUA FOR M/S. INDIAN IRON STEEL CO. LTD. ISCG 36 SER TISCO'S JODA EAST BIN, BANSPANI JMDT 37 SER JODA EAST IRON MINE PVT. SDG M/S TISCO JMTB 38 SER JODA EAST DIRECT ENTRY PVT. -

Iron & Steel and Scrap 2016.Pmd

IRON & STEEL AND SCRAP Indian Minerals Yearbook 2016 (Part- II : Metals & Alloys) 55th Edition IRON & STEEL AND SCRAP (FINAL RELEASE) GOVERNMENT OF INDIA MINISTRY OF MINES INDIAN BUREAU OF MINES Indira Bhavan, Civil Lines, NAGPUR – 440 001 PHONE/FAX NO. (0712) 2565471 PBX : (0712) 2562649, 2560544, 2560648 E-MAIL : [email protected] Website: www.ibm.gov.in February, 2018 9-1 IRON & STEEL AND SCRAP 9 Iron & Steel and Scrap ron & steel is decidedly the vital component of of iron & steel is sufficient to meet the domestic Ia country's economy and is considered demand, it imports mainly finished/semi-finished amongst the driving force of modernisation. steel and iron & steel (scrap) to meet specific The level of per capita consumption of steel is requirements and supply of essential grades. treated as one of the important indicators of socio-economic development and living Liberalisation of the Indian Steel Sector standards in any country. Steel continues to The Government's new economic policies be the foremost of engineering materials, which have opened up opportunities for expansion of not only is environment-friendly but also is the Steel Industry. With a view to accelerating recyclable. growth in the Steel Sector, the Government since The finished steel production in India has 1991 has been initiating and implementing a grown from a mere 1.1 million tonnes in 1951 to number of policy measures. These measures have 90.98 million tonnes in 2015-16. There, however impacted the Indian Steel Sector positively in was a decline of 1.3% in the production reported terms of modernisation and growth. -

VISA STEEL LIMITED (Our Company Was Incorporated on September 10, 1996 As VISA INDUSTRIES LIMITED Under the Companies Act, 1956, with the Registration No

RED HERRING PROSPECTUS Please read Section 60B of the Companies Act, 1956. STEEL Dated February 14 , 2006 100% Book Building Issue VISA STEEL LIMITED (Our Company was incorporated on September 10, 1996 as VISA INDUSTRIES LIMITED under the Companies Act, 1956, with the Registration No. 15-04601 of 1996-97. Our name was changed from VISA INDUSTRIES LIMITED to VISA STEEL LIMITED with effect from May 4, 2005 with new CIN No. U13209OR1996PLC004601. For details on changes of our Registered Office, please refer to the chapter titled “History and Other Corporate Matters” beginning on page 76 of this Red Herring Prospectus.) Registered Office: 11, Ekamra Kanan, Nayapalli, Bhubaneswar – 751 015, Orissa Tel: +91 674 2552479; Fax: +91 674 2554662. Corporate Office: VISA House, 8/10, Alipore Road, Kolkata – 700 027, West Bengal Tel: +91 33 24567374; Fax: +91 33 24567219. Contact Person: Mr. Manoj Kumar Digga; E-mail: [email protected]; Website: www.visasteel.com PUBLIC ISSUE OF 35,000,000 EQUITY SHARES OF RS. 10 EACH AT A PRICE OF RS. [●] PER EQUITY SHARE FOR CASH AGGREGATING RS. [●] MILLION (HEREINAFTER REFERRED TO AS THE “ISSUE”), COMPRISING OF PROMOTERS’ CONTRIBUTION OF 5,000,000 EQUITY SHARES OF RS. 10 EACH AT A PRICE OF RS. [●] FOR CASH AGGREGATING TO RS. [●] MILLION (REFERRED TO AS THE “PROMOTER’S CONTRIBUTION”). THE ISSUE LESS THE PROMOTER’S CONTRIBUTION SHALL BE HEREINAFTER REFERRED TO AS THE “NET ISSUE TO PUBLIC”. THE NET ISSUE TO PUBLIC WILL CONSTITUTE 27.27% OF THE POST ISSUE PAID-UP CAPITAL OF THE COMPANY. PRICE BAND: Rs. 52 TO Rs. -

Annual Report 2017-18

Annual Report 2017-18 01-13 COMPANY OVERVIEW 02 Vision & Values 04 Raw Material 05 Operations 06 Chairman’s Insights 08 Vice Chairman & Managing Director’s Message 10 Board of Directors 12 Corporate Social Responsibility 14-48 STATUTORY REPORTS 14 Report of the Directors 32 Management Discussion and Analysis 36 Corporate Governance 49-171 FINANCIAL STATEMENTS 49 Standalone 109 Consolidated FORWARD-LOOKING STATEMENTS In this Annual Report, we have disclosed forward-looking information to enable investors to comprehend our prospects and take investment decisions. This Report and other statements – written and oral – that we periodically make contain forward-looking statements that set out anticipated results based on the management’s plans and assumptions. We have tried wherever possible to identify such statements by using words such as ‘anticipate’, ‘estimate’, ‘expects’, ‘projects’, ‘intends’, ‘plans’, ‘believes’ and words of similar substance in connection with any discussion of future performance. We cannot guarantee that these forward-looking statements will be realised, although we believe we have been prudent in our assumptions. The achievements of results are subject Listing to risks, uncertainties and even inaccurate assumptions. Your Company has been listed on National Should known or unknown risks or uncertainties materialise, Stock Exchange of India Limited and or should underlying assumptions prove inaccurate, actual Bombay Stock Exchange Limited results could vary materially from those anticipated, estimated or projected. Readers should keep this in mind. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise. For more details, visit: http://www.visasteel.com VISA STEEL LTD. -

Thermal Power Plants in Odisha

Thermal Power Plants in Odisha Sl. Name Address & Contact Generation No. Person with E-mail-id Capacity in MW 1. M/s Aarti Steel Ltd. At-Ghantikhala, 80 Po- Mahakalabasta, Athagada, Cuttack Mr. Pritish Dash, Manager (Env.) [email protected] M-9437083942 2. M/s ACC Ltd. Bargarh Cement Works, 30 Cement Nagar, Bardol, Bargarh, Pin No. 768 038, Ph No. 91-6646-247161, Fax. 91-6646-246430 Mr. Debapratim Bhadra, Head- Energy & Env. debapratim.bhadra@accli mited.com M-9777447636 arupkumar.das@acclimite d.com 3. M/s Action Ispat & Power At: Pandripathar, 63 (P) Ltd. P.O. Marakuta, Dist-Jharsuguda, Pin No. 768202 Mr. BhabyaRanjan Nayak, Environment Dept. environment.bhabyaranja [email protected] Mr. Ranjan Sahu Asst. Env. Officer, M-7752023544 [email protected] om 4. M/s Bhushan Power & Vill-Thelkoloi, 370 Steel Ltd. P.O. Lapanga- 768232 Teh. Rengali, Dist-Sambalpur, Mr. Niranjan Parida, Dy. Manager, [email protected] M-9437150569 Sl. Name Address & Contact Generation No. Person with E-mail-id Capacity in MW 5. M/s Bhushan Steel Ltd. At- Narendrapur, 142 Meramundali, Dhenkanal Ph. No. 06762-300000 / 660002 / 660000, Fax. 91-011-66173997 Mr. Santosh Pattajoshi, Sr. Manager, santosh.pattajoshi@bhusha nsteel.com M-7077757663 ram.sharma@bhushansteel .com 6. M/s Bhushan Energy Ltd. At-Ganthigadia, 300 P.O. Nuahata, Via-Banarpal, Dist-Angul Pin No. 759128 Ph-6762-300000 Fax. 011-66173997 7. M/s Birla Tyres At/Po-Chhanpur, Kuruda, 20 Balasore-756056, Ph. No. 06782- 254621/254225, Fax.06782-254225 Mrs. Suchismita Patnaik, Team Member, suchismita_patnaik@birlaty re.com 8. -

Hon'ble National Company Law Tribunal, Kolkata

HON’BLE NATIONAL COMPANY LAW TRIBUNAL, KOLKATA BENCH (‘NCLT’) CONVENED MEETING OF THE UNSECURED CREDITORS OF VISA STEEL LIMITED Day : FRIDAY Date : 30 JUNE 2017 Time : 1.00 PM Venue : VISA House,11 Ekamra Kanan, Nayapalli, Bhubaneswar 751 015, Odisha Sl. No. Contents Page No. 1 Notice of NCLT convened meeting of the Unsecured Creditors of VISA Steel Limited 1-4 (‘Transferee Company’). 2 Explanatory Statement under Sections 102, 230 (3) and other applicable provisions of the Companies Act, 2013 read with Rules 6 and 7 of the Companies (Compromises, 5-18 Arrangements and Amalgamations) Rules, 2016 forming part of the Notice. 3 Scheme of Amalgamation of VISA BAO Limited (‘Transferor Company’) with VISA Steel Limited (‘Transferee Company’) under Sections 230 and 232 of the Companies Act, 2013 19-25 and other applicable provisions of the Companies Act, 2013 and any amendments thereto or re-enactments thereof. 4 Copy of the Audit Committee Report dated 21 August 2015 of the Transferor Company. 26 5 Copy of the Valuation Report dated 21 August 2015 issued by the Independent Chartered 27-51 Accountants, M/s Rajesh Choudhary & Associates 6 Copy of Supplementary Unaudited Financial Statements for the nine months ended on 31 52-57 December 2016 of the Transferor Company and the Transferee Company. 7 Copy of Observation Letter dated 7 April 2016 issued by BSE Limited (‘BSE’). 58 8 Copy of Observation Letter dated 6 April 2016 issued by National Stock Exchange of India 59-60 Limited (‘NSE’). 9 Copy of Fairness Opinion dated 21 august 2015 issued by Intelligent Money Managers 61-66 Private Limited SEBI Registered Category I Merchant Banker. -

Profitability Analysis of Selected Steel Companiesin India

Vol.04 issue-05, (May, 2017) ISSN: 2394-5702 International Journal in Commerce, IT & Social Sciences (Impact Factor- 4.218) PROFITABILITY ANALYSIS OF SELECTED STEEL COMPANIESIN INDIA Anandan Muthuvaithyanathana and Shanthi Rangasamyb# aResearch Scholar, Department of Management, Kaamadhenu Arts and Science College, Sathyamangalam, Erode-638401 bAssistant Professor, Department of Management, Kaamadhenu Arts and Science College, Sathyamangalam, Erode-638401 ABSTRACT India was the world’s third largest steel producer in 2016. The growth in the Indian steel sector has been driven by domestic availability of raw materials such as iron ore and cost effective labour. Consequently the steel sector has been a major contributor to India’s manufacturing output. This study tries to find out the profitability of selected steel companies in India. Five steel companieshave been selected for the study.The period of study 2011-12 to 2015-2016. Various tools like Mean, Variance, Correlation, Standard Deviation and t-test were used for analysis. It is concluded that Bhushan’s Steel and Visa Steel may give attention in the area of direct expenses to reduce it, because effective and efficiency performance of company can be measured in terms of profitability. Expenses are the major direct impact on the profitability of every enterprise. Key Words: Financial statement, Steel Companies, Profitability Analysis, Correlation, Standard Deviation INTRODUCTION Profitability (P) is the profit earning capacity which is a crucial factor contributing to the survival of the firms. The perpetual existence of the firms depends on the profit earning capacity of the firm, which is also considered to be the main factor in influencing the reputation of the firm. -

Visa Steel:There and Back Again

Vishambhar Saran, CEO, Visa Steel, at the ferrochrome tapping unit of his plant in Odisha. VISA STEEL:THERE AND BACK AGAIN How Vishambhar Saran learnt to roll with the punches. By Pavan Lall @LallPavan APRIL 5, 2015 16:12 “You didn’t go to the bathroom, did you?” That’s the punch line to what some call an apocryphal story about how Vishambhar Saran won a Chinese contract for Tata Steel. It’s all true, I’m told by Saran and some of his peers. Saran was then in charge of new business, international trading operationss, and business development, and was in China to woo one of the largest ferroalloy plants in Jilin province in Northwest China. Negotiations were preceded by a formal dinner, during which the Chinese told Saran that they had no idea about Indian ore, since they had not bought it before. A while later, Saran took a break to use the facilities, and when looking out of the window, saw a stockpile of chrome ore. His decade-plus experience in Tata’s mines, plus a childhood spent with mining families in Uttar Pradesh and Odisha, kicked in. He recognised the ore as coming from a Tata mine, which had possibly been sold through intermediaries. It meant that the Chinese officials had no idea about what ore they were using. Saran went back to the dinner table, and at an appropriate juncture, offered to sell 20,000 tonnes of ore at Rs 300 a tonne. The Tata team had earlier decided to offer the ore at between Rs 160 and Rs 180 a tonne, and allow themselves to be beaten down to Rs 140. -

Pre-Feasibility Report for Addition of Wet Screening System to Blast Furnace & DRI for Iron Ore Processing

Pre-feasibility Report for addition of Wet Screening System to Blast Furnace & DRI for Iron Ore Processing. Increase in BlastPRE Furnace- capFEASIBILITYacity from 1,75,000 to 2,50,000TPA of M/sREPORT Visa Steel Limited At- Kalinga nagar Industrial Complex, Jajpur, Odisha. Addition of Iron Ore Washing & Wet Screening System for Rainy Period 1x 50 TPH (1350 TPD Throughput-for BF feed) & 1x58.3 TPH (1600 TPD Throughput-for DRI feed) & Increase in Hot Metal production capacity from 175000 TPA to 250000 TPA without change in Size for Existing Blast Furnace At Kalinganagar Industrial Complex, Jajpur, Odisha Applicant M/s Visa Steel Limited Kalinga nagar Industrial Complex, Jajpur, Odisha. M/s VISA STEEL LIMITED Page 1 Pre-feasibility Report for addition of Wet Screening System to Blast Furnace & DRI for Iron Ore Processing. Increase in Blast Furnace capacity from 1,75,000 to 2,50,000TPA of M/s Visa Steel Limited At- Kalinga nagar Industrial Complex, Jajpur, Odisha. CHAPTER – 1 EXECUTIVE SUMMARY Presently M/s VISA Steel Limited (VSL) is operating a 0.5 MTPA integrated steel plant at Kalinganagar Industrial Complex in Odisha. The facilities include a 175000 TPA Pig Iron Plant, 300,000 TPA Sponge Iron Plant, 500,000 TPA Steel Melt Shop (with EAF, LRF and VD) & 500,000 TPA Rolling Mill (Bar & Wire Rod Mill). VISA Steel is also operating 125000 (VISA Steel-50000 & VISA Bao-75,000 TPA) Ferro Chrome Plant and a 75 MW Captive Power Plant. Previous EC was obtained for 1.5 MTPA integrated steel plant withAn CPPnexure vide– Ifile no. -

Training Example Sheet.Xlsx

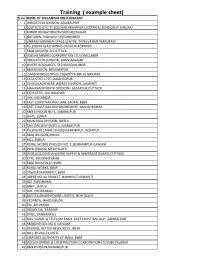

Training ( example sheet) Sl no NAME OF ORGANISATION/COMPANY 1 IRRIGATION DIVISION ,SAMBALPUR 2 SOUTHCO UTILITY SOUTHBERHAMPUR ELECTRICAL DIVISION‐III GANJAM 3 MINOR IRRIGATION DIVISION,KEONJHAR 4 NATIONAL HIGHWAY DIVISION,BBSR 5 VIKRAM SARABHAI SPACE CENTRE, THIRUVANANTHAPURAM 6 TELENGIRI HEAD WORKS DIVISION KORAPUT 7 R&B( DIVISION ‐I),CUTTACK 8 ODISHA MINING CORPORATION LTD (OMC),BBSR 9 IRRIGATION DIVISION, BHANJANAGAR 10 WATER RESOURCES, SECHASADAN,BBSR 11 R&B DIVISION, BRAHMAPUR 12 GRASIM INDUSTRIES LTD(ADITYA BIRLA) GANJAM 13 TATA STEEL LTD , JAMSHEDPUR 14 CHHELIGADA HEAD WORKS DIVISION, GAJAPATI 15 MAHANADI NORTH DIVISION‐I JAGATPUR,CUTTACK 16 TATA STEEL, KALINGANAR 17 HAL, SUNABEDA 18 EAST COAST RAILWAY, RAIL SADAN, BBSR 19 EAST COAST RAILWAY(WORKSHOP) ,MANCHESWAR 20 R&B DIVISION NO‐1, SAMBALPUR 21 OHPC, BURLA 22 MAIN DAM DIVISION, BURLA 23 DIVL.RAILWAY (MECH) ,SAMBALPUR 24 TELENGIRI CANAL DIVISION,BANIRIPUT, KORAPUT 25 R&B) DIVISION,ANGUL 26 MCL, BURLA 27 RURAL WORKS DIVISION NO ‐1 ,BERHAMPUR GANJAM 28 PWD (ROADS) MEGHALAYA 29 OISIP,JICA,ODISHA WATER SUPPLY & SEWERAGE BOARD, CUTTACK 30 CTTC, BHUBANESWAR 31 R&B) DIVISION,JEYPORE 32 RURAL WORKS, BBSR 33 CPWD,POKHARIPUT, BBSR 34 UPPER KOLAB PROJECT, BANIRIPUT,KORAPUT 35 L&T ,KANSBAHAL 36 MNIT, JAIPUR 37 ECIL, HYDERABAD 38 BSES RAJDHANI POWER LIMITED, NEW DELHI 39 VEDANTA, JHARSUGUDA 40 TRL, BELPAHAR 41 INDIAN OIL, PARADIP 42 OPGC, BANHARPALI 43 DIVL SIGNAL & TELECOM ENGR. EAST COAST RAILWAY ,SAMBALPUR 44 R&B)DIVISION NO II, GANJAM 45 DESIGNS, WATER RESOURCES , BBSR 46 MCL, IB VALLEY -

3 SAIL Augmentation of Iron Ore Production Capacity of Bolani Iron

1 Format – 1 Agenda Summary Format For IMG Meeting to be held on 31st May, 2016 at 1600 hrs. in respect of CPSEs Sl. Name of the Project Name & Location of the Sector Pending issues Pending with Central No. Project ID No. Project Privat each issues separately Ministries/State Proponents on [Brief detail to be given in e/Pub e.g. 1EC; 2 FC; 3 Land Governments/ PMG Format – 2 as Annexure 2] lic/PP acquisition; 4 Water Departments Portal P availability; 5 RoW; etc [Specify the name of the Ministry/Department or Field Office] 1 SAIL 799 Augmentation of iron ore Public Grant of Stage-II FC for MoEF & CC since (CS430 production capacity of Gua diversion of 361.295 Ha 30-09-2015 0028) Iron Ore Mine including of forest land in installation of Duargaiburu lease of Gua Beneficiation and Pellet mine is awaited. Plant facilities at Gua, Jharkhand 2 SAIL 1457 Expansion of Bhilai Steel Public Supply of EoT & HEC & MoHI (CS430 Plant Hydraulic cranes by HEC PRAGATI monitored 0057) 3 SAIL Augmentation of iron ore Publi 1. Issue related to 1. Time line provided in production capacity of c MoEFCC guideline dated the Guideline to be Bolani Iron Ore Mine along 10.03.2015 related to extended by MoEFCC. with enhancement of Sabik Kisam Forest land 2. Proposal of extension loading capacity at Bolani, 2. Extension of lease of 6.9 Sq Mile lease of Keonjhar period for 6.9 Sq Mile Bolani mines is pending lease of Bolani mine. with Secretary(Steel & 2 3. Anomaly in levy of Mines), Odisha royalty on iron ore 3. -

01 2010 Cover Story Hungry for Steel Download

metals&mining The magazine for the metals and mining industries www.siemens-vai.com Issue 1|2010 India Hungry for Steel Arvedi ESP Performance at Its Best E10001-M1-Z22-V1-7600 Dear Readers, EDITORIAL > EDITORIAL India is developing into one of the key economies in the world and is in - creasingly playing a major role in world events. Analysts expect India to become the world’s second-largest steel producer by 2016. Investments in infrastructure, housing, the energy sector and machine construction are behind the country’s hunger for steel. Current megaprojects include the construction of a 20,000 km long highway, new airports and sea- ports, irrigation networks and power plants – all part of a nationwide infra structure program that will require staggering amounts of steel in the years to come. That is why Siemens is considerably expanding its activities in India. In the next three fiscal years, the company will nearly double its investments from today’s levels. New competence centers are part of this effort; they will be responsible for the entire value-added chain – from product design Ashoke Pan and development through to production and sales in India and beyond. For Siemens’ metals business this means working further on strengthen - ing the local engineering and manufacturing network as well as con side - rably expanding the service network. In the past, Siemens VAI projects introduced state-of-the-art technologies to India for the first time. That tradition continues to today. Siemens VAI installs advanced solutions for the protection of the environment, improved operational reliability and operator safety at industrial-scale steel production sites.