ASX Release 9 June 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Equity Fund Proxy Voting Disclosure 2020

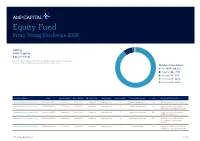

Equity Fund Proxy Voting Disclosure 2020 Voting AMP Capital Equity Fund Note: The below disclosures refer to Australian listed securities only and do not include foreign listed securities held in the portfolio. Number of resolutions: n For 1077 - 90.2% n Against 88 - 7.3% n Abstain 18 - 1.5% n Unvoted 8 – 0.7% n Unvoted 3 – 0.3% Company Name ISIN Meeting Date Record Date Meeting Type Proponent Proposal No. Type of Proposal Vote Proposal Description Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 1 Capital Management For Ratify Placement of Securities Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 2 Capital Management For Approve Issue of Securities (Executive chair Bill Beament) Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 3 Capital Management For Approve Issue of Securities (NED Mary Hackett) Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 4 Capital Management For Approve Issue of Securities (Former NED Christopher Rowe) Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 5 Board Related For Approve Financial Assistance (Kalgoorlie Lake View Pty Ltd) AMP Capital Equity Fund 1 of 58 Company Name ISIN Meeting Date Record Date Meeting Type Proponent Proposal No. Type of Proposal Vote Proposal Description Virgin Money UK Plc. AU0000064966 1/29/2020 1/24/2020 Annual Management 1 Audit/Financials For Accounts and Reports Virgin Money UK Plc. AU0000064966 1/29/2020 1/24/2020 Annual Management 2 Compensation For Remuneration Policy (Binding) Virgin Money UK Plc. -

BINGO Enters Into Scheme Implementation Deed with MIRA

ASX Release 27 April 2021 BINGO enters into Scheme Implementation Deed with Macquarie Infrastructure and Real Assets (“MIRA”) • BINGO has entered into a Scheme Implementation Deed with Macquarie Infrastructure and Real Assets and its managed funds (together, “MIRA”) to acquire 100% of the share capital of BINGO by way of Scheme of Arrangement • Under the terms of the Scheme, BINGO shareholders will have the option to receive either $3.45 cash per BINGO share, or a mixed cash and unlisted scrip alternative • BINGO’s Board intends to declare a fully franked Special Dividend of up to $0.117 per BINGO share prior to implementation of the Scheme, which would enable shareholders to receive additional benefits from franking credits of up to $0.05 per BINGO share1 • BINGO’s Independent Board Committee and other BINGO Recommending Directors unanimously recommend the Scheme, subject to conditions outlined below • The cash consideration represents a 33% premium to the BINGO one-month volume weighted average price up to and including 18 January 2021 and an acquisition multiple of 19.5x LTM Dec 20 EBITDA2 • The Scheme is subject to certain conditions which must be satisfied or waived before the Scheme can be implemented • BINGO shareholders do not need to take any action at the present time BINGO Industries Limited (“BINGO” or “the Company”) (ASX:BIN) today announced that it has entered into a Scheme Implementation Deed (“SID”) with Recycle and Resource Operations Pty Limited, an entity owned by Macquarie Infrastructure and Real Assets and its managed funds (together, “MIRA”) for the acquisition of all of the issued shares in BINGO pursuant to a scheme of arrangement (“Scheme” or “Scheme of Arrangement”). -

Stocks List U Ethical Australian Equities Portfolio

All stocks list U Ethical Australian Equities Portfolio Below is a list of all holdings within the portfolio as at 31 March 2019. Stock holdings The A2 Milk Company G8 Education Reliance Worldwide Amcor Goodman Group ResMed Australia and New Zealand Banking GUD Holdings Seek Group Bingo Industries Invocare Sonic Healthcare Bluescope Steel JB Hi-Fi Suncorp Group Boral Lendlease Group Transurban Group Carsales.com Macquarie Group Telstra Challenger Monash IVF Group Wesfarmers Coles Oil Search Westpac Banking Corporation Commonwealth Bank of Australia QBE Insurance Group Woodside Petroleum CSL Ramsay Health Care Fortescue Metals Group REA Group This document dated 31 March 2019 is issued by UCA Growth Fund Limited (UCA Growth) for the U Ethical Australian Equities Portfolio (the Portfolio). U Ethical (a registered business name of Uniting Ethical Investors Limited ABN 46 102 469 821 AFSL 294147) is the Manager and Administrator of the Portfolio. The information provided is general information only. It does not constitute financial, tax or legal advice or an offer or solicitation to subscribe for units in any fund of which U Ethical is the Manager, Administrator, Issuer, Trustee or Responsible Entity. This information has been prepared without taking account of your objectives, financial situation or needs. Before acting on the information or deciding whether to acquire or hold a product, you should consider the appropriateness of the information based on your own objectives, financial situation or needs or consult a professional adviser. You should also consider the relevant Product Disclosure Statement (PDS) or Offer Document which can be found on our website www.uethical.com or by calling us on 1800 996 888. -

Ngs Super Portfolio Holdings Disclosure

NGS SUPER PORTFOLIO HOLDINGS DISCLOSURE DEFENSIVE - ACCUMULATION Effective date: 31 DEC 2020 AUSTRALIAN SHARES A2 MILK CO LTD ABACUS PROPERTY GROUP REIT ACCENT GROUP LTD ADAIRS LTD ADBRI LTD AFTERPAY LTD AGL ENERGY LTD AINSWORTH GAME TECHNOLOGY LTD ALACER GOLD CORP ALE PROPERTY GROUP REIT ALS LTD ALTIUM LTD ALUMINA LTD AMA GROUP LTD AMCOR PLC AMP LTD ANSELL LTD APA GROUP STAPLED SECURITY APPEN LTD ARB CORP LTD ARISTOCRAT LEISURE LTD ASALEO CARE LTD ASX LTD ATLAS ARTERIA STAPLED SECURITY AUB GROUP LTD AUCKLAND INTL AIRPORT LTD AURELIA METALS LTD AUSNET SERVICES AUSSIE BROADBAND Issued by NGS Super Pty Limited ABN 46 003 491 487 AFSL No 233 154 the trustee of NGS Super ABN 73 549 180 515 ngssuper.com.au 1300 133 177 NGS SUPER – PORTFOLIO HOLDINGS DISCLOSURE 1 DEFENSIVE - ACCUMULATION Effective date: 31 DEC 2020 AUST AND NZ BANKING GROUP AUSTAL LTD AUSTRALIAN FINANCE GROUP LTD AUSTRALIAN PHARMA INDUS LTD AUSTRALIAN VINTAGE LTD AVENTUS GROUP REIT AVITA MEDICAL INC BABY BUNTING GROUP LTD BANK OF QUEENSLAND LTD BAPCOR LTD BEACH ENERGY LTD BEACON LIGHTING GROUP LTD BEGA CHEESE LTD BENDIGO AND ADELAIDE BANK BHP GROUP LTD BINGO INDUSTRIES LTD BLACKMORES LTD BLUESCOPE STEEL LTD BORAL LTD BRAMBLES LTD BRAVURA SOLUTIONS LTD BREVILLE GROUP LTD BRICKWORKS LTD BWP TRUST REIT CALTEX AUSTRALIA LTD CAPITOL HEALTH LTD CAPRAL LTD CAPRICORN METALS LTD CARDNO LTD CARNARVON PETROLEUM LTD CARSALES.COM LTD CASH CEDAR WOODS PROPERTIES LTD CENTURIA INDUSTRIAL REIT CENTURIA METROPOLITAN REIT CHALLENGER LTD CHAMPION IRON LTD CHARTER HALL GROUP REIT CHARTER HALL LONG -

M Funds Quarterly Holdings 3.31.2020*

M International Equity Fund 31-Mar-20 CUSIP SECURITY NAME SHARES MARKET VALUE % OF TOTAL ASSETS 233203421 DFA Emerging Markets Core Equity P 2,263,150 35,237,238.84 24.59% 712387901 Nestle SA, Registered 22,264 2,294,710.93 1.60% 711038901 Roche Holding AG 4,932 1,603,462.36 1.12% 690064001 Toyota Motor Corp. 22,300 1,342,499.45 0.94% 710306903 Novartis AG, Registered 13,215 1,092,154.20 0.76% 079805909 BP Plc 202,870 863,043.67 0.60% 780087953 Royal Bank of Canada 12,100 749,489.80 0.52% ACI07GG13 Novo Nordisk A/S, Class B 12,082 728,803.67 0.51% B15C55900 Total SA 18,666 723,857.50 0.51% 098952906 AstraZeneca Plc 7,627 681,305.26 0.48% 406141903 LVMH Moet Hennessy Louis Vuitton S 1,684 625,092.87 0.44% 682150008 Sony Corp. 10,500 624,153.63 0.44% B03MLX903 Royal Dutch Shell Plc, Class A 35,072 613,753.12 0.43% 618549901 CSL, Ltd. 3,152 571,782.15 0.40% ACI02GTQ9 ASML Holding NV 2,066 549,061.02 0.38% B4TX8S909 AIA Group, Ltd. 60,200 541,577.35 0.38% 677062903 SoftBank Group Corp. 15,400 539,261.93 0.38% 621503002 Commonwealth Bank of Australia 13,861 523,563.51 0.37% 092528900 GlaxoSmithKline Plc 26,092 489,416.83 0.34% 891160954 Toronto-Dominion Bank (The) 11,126 473,011.14 0.33% B1527V903 Unilever NV 9,584 472,203.46 0.33% 624899902 KDDI Corp. -

Investment Strategy Group Analyst Holdings

Investment Strategy Group Analyst Holdings June 2021 Security Code Security name Security Code Security name A2M A2 Milk Company Ltd CHTR US Charter Communications Inc AAPL US Apple Inc. CLQ Clean TEQ Holdings Ltd ABBV US Abbvie Inc CNQ Clean Teq Water Ord Shs ABR American Pacific Borates Ltd COB Cobalt Blue Holdings Limited AGN US Allergan plc CSL CSL Limited AL3 AML3D Ltd CTT Cettire Ltd ALC Alcidion Group Limited CUE Cue Energy Resources Limited ALSN US Allison Transmission Holdings Inc CVNA US Carvana Co. ALU Altium Ltd CVS US CVS Health Corp AMGN US Amgen USA Inc CWNHB Crown Subordinated Notes II AMPPA AMP Capital Notes CXL Calix Ltd AMZN US Amazon.com Inc DIS US Walt Disney Co ANR Anatara Lifesciences Ltd DISCA US Discovery Inc ANZ Australia and New Zealand Banking Group Limited DMP Domino’s Pizza Enterprises Ltd APL Antipodes Global Investment Company Ltd DUB Dubber Corp Ltd APT Afterpay Ltd EBS VA Ersta Group Bank AG APX Appen Ltd EL8 Elevate Uranium Ltd ARL Ardea Resources Limited EL PA EssilorLuxottica ASIA Betashares Asia Tech Tigers EM1 Emerge Gaming Limited ASX ASX Limited EVN Evolution Mining Limited AVH Avita Medical Ltd EXO MI Exor N.V. AXB LI Axis Bank Ltd FAIR BetaShares Australian Sustainability Leaders ETF BABA US Alibaba Group Holding Ltd FANG ETFS FANG+ ETF BAP Bapcor Ltd FLN Freelancer Ltd BAYN GR Bayer AG FPH Fisher & Paykel Healthcare Corp Ltd BB US Blackberry Ltd FUND Bell Global Emerging Companies Fund BCI NC New Look Vision Group Inc FUND BetaShares Asia Technology Tigers ETF BHP BHP Group Ltd FUND BetaShares -

Proxy Vote Record -November 2019

Company Name Ticker Country Meeting Date Proposal Text Vote Instruction A. D. Works Co., Ltd. 3250 Japan 29-Nov-19 Approve Formation of Holding Company Against A. D. Works Co., Ltd. 3250 Japan 29-Nov-19 Amend Articles To Delete References to Record Date Against A. D. Works Co., Ltd. 3250 Japan 29-Nov-19 Approve Takeover Defense Plan (Poison Pill) Against A.D.O. Group Ltd. ADO Israel 07-Nov-19 Approve Merger Agreement For A.D.O. Group Ltd. ADO Israel 07-Nov-19 Vote FOR if you are a controlling shareholder or have a personal interest in one or several resolutions, as indicated in the Against proxy card; otherwise, vote AGAINST. You may not abstain. If you vote FOR, please provide an explanation to your account manager A.D.O. Group Ltd. ADO Israel 07-Nov-19 If you are an Interest Holder as defined in Section 1 of the Securities Law, 1968, vote FOR. Otherwise, vote against. Against A.D.O. Group Ltd. ADO Israel 07-Nov-19 If you are a Senior Officer as defined in Section 37(D) of the Securities Law, 1968, vote FOR. Otherwise, vote against. Against A.D.O. Group Ltd. ADO Israel 07-Nov-19 If you are an Institutional Investor as defined in Regulation 1 of the Supervision Financial Services Regulations 2009 or a For Manager of a Joint Investment Trust Fund as defined in the Joint Investment Trust Law, 1994, vote FOR. Otherwise, vote against. A2B Australia Ltd. A2B Australia 21-Nov-19 Elect Louise McCann as Director For A2B Australia Ltd. -

Annual Sustainability Report 2019 Why U Ethical 2 Section 3

Annual Sustainability Report 2019 Why U Ethical 2 Section 3. Statement from the chairperson 4 The people behind Statement from the chief executive officer 5 our impact Year in review 6 Board of directors 34 Management team 38 Our people 40 Section 1. Better investments for a better world Section 4. Investment performance 10 Stakeholder engagement Our products 12 and financial performance Materiality assessment 16 Our clients 46 Financial performance 49 Our material topics 50 Section 2. Our ethical approach Global Reporting Initiative (GRI) index 53 Ethical investment policy 20 Our Ethical Advisory Panel 21 Negative screening 22 Investing in positive outcomes 23 Engagement and advocacy 26 Our community contribution 29 Why U Ethical U Ethical is an investment manager with a difference. Since inception, we have worked to create a better world by investing with purpose. We are focused on serving the needs of all kinds of investors — from corporate and institutional, to not-for-profits, to individual clients. Whether big or small, our clients trust us $1.2b to deliver competitive returns while doing the right thing by communities and the planet. funds under Today, we are one of the largest ethical investment managers in Australia, with $1.2 billion management in funds under management. Unlike the majority of ethical managers, we are a not-for-profit social enterprise, which means most of our surplus goes to support social justice advocacy and community programs. In addition, we are one of the few investment businesses in Australia to be certified as a B Corporation. B Corporations are businesses that meet the highest standards of verified social and environmental performance, public transparency, and legal accountability to balance profit and purpose. -

Voting Report November 2017

Voting November 2017 Schroders is required to publish records of voting in order to achieve compliance with the UK Stewardship Code. According, voting in accordance with our house policy is set out on the following pages. Vote Summary Report Date range covered: 11/01/2017 to 11/30/2017 Amcor Limited Meeting Date: 11/01/2017 Country: Australia Meeting Type: Annual Ticker: AMC Proposal Vote Number Proposal Text Mgmt Rec Instruction 2a Elect Paul Brasher as Director For For 2b Elect Eva Cheng as Director For For 2c Elect Tom Long as Director For For 3 Approve the Grant of Options and Performance For For Shares to Ron Delia 4 Approve the Potential Termination Benefits For For 5 Approve the Remuneration Report For For Bingo Industries Limited Meeting Date: 11/01/2017 Country: Australia Meeting Type: Annual Ticker: BIN Proposal Vote Number Proposal Text Mgmt Rec Instruction 1 Elect Daniel Girgis as Director For For 2 Appoint Deloitte Touche Tohmatsu as Auditor of For For the Company 3 Approve Remuneration Report For For Fortress Income Fund Ltd Meeting Date: 11/01/2017 Country: South Africa Meeting Type: Annual Ticker: FFA Proposal Vote Number Proposal Text Mgmt Rec Instruction 1.1 Elect Vuso Majija as Director For For 1.2 Elect Bongiwe Njobe as Director For For 2.1 Re-elect Jeff Zidel as Director For For Vote Summary Report Date range covered: 11/01/2017 to 11/30/2017 Fortress Income Fund Ltd Proposal Vote Number Proposal Text Mgmt Rec Instruction 2.2 Re-elect Tshiamo Matlapeng-Vilakazi as Director For For 2.3 Re-elect Jan Potgieter as Director -

M Funds Quarterly Holdings 3.31.2021*

M International Equity Fund 31-Mar-21 CUSIP SECURITY NAME SHARES MARKET VALUE % OF TOTAL ASSETS 233203421 DFA Emerging Markets Core Equity P 2560482 65394713.22 30.55% 712387901 Nestle SA, Registered 22264 2481394.23 1.16% 711038901 Roche Holding AG 4932 1593905.09 0.74% 690064001 Toyota Motor Corp. 20300 1579632.42 0.74% ACI02GTQ9 ASML Holding NV 2066 1252586.68 0.59% 780087953 Royal Bank of Canada 12100 1115641.76 0.52% 406141903 LVMH Moet Hennessy Louis Vuitton S 1624 1081926.46 0.51% 710306903 Novartis AG, Registered 12302 1051296.13 0.49% 677062903 SoftBank Group Corp. 11100 935317.23 0.44% 682150008 Sony Corp. 8500 890110.63 0.42% ACI07GG13 Novo Nordisk A/S, Class B 12082 818545.62 0.38% 552902900 Daimler AG, Registered 9159 816405.12 0.38% B15C55900 TOTAL SE 16933 789825.28 0.37% 621503002 Commonwealth Bank of Australia 11972 782935.95 0.37% B03MM4906 Royal Dutch Shell Plc, Class B 41803 769354.91 0.36% 891160954 Toronto-Dominion Bank (The) 11275 735337.79 0.34% 098952906 AstraZeneca Plc 7325 731819.38 0.34% B4TX8S909 AIA Group, Ltd. 60200 730227.29 0.34% 584235907 Deutsche Telekom AG, Registered 32806 660557.31 0.31% 614469005 BHP Group, Ltd. 19147 658802.61 0.31% B288C9908 Iberdrola SA 50592 651731.69 0.30% 071887004 Rio Tinto Plc 7931 606818.69 0.28% BLRB26905 Unilever Plc 9584 534759.09 0.25% 079805909 BP Plc 129795 527232.81 0.25% 559222955 Magna International, Inc. 5972 525965.59 0.25% 023740905 Diageo Plc 12494 514918.00 0.24% 064149958 Bank of Nova Scotia (The) 8200 512997.53 0.24% 618549901 CSL, Ltd. -

Index Rebalance

Index Rebalance Friday 11th June 2021 Reference No: 0004/21 Subject: Index Rebalance The June 2021 quarterly rebalancing results for the CXA 200 Index will be effective at the open on Monday 21st June 2021. The additions and deletions, as well as other changes made to the indices, resulting from the June 2021 quarterly rebalancing are shown below. Inclusions Ticker Name Reason GXY Galaxy Resources Ltd New Entrants with ranking equal or above 180 SLK Sealink Travel Group Ltd New Entrants with ranking equal or above 180 IMU Imugene Ltd New Entrants with ranking equal or above 180 PTM Platinum Asset Management New Entrants with ranking equal or above 180 PDN Paladin Energy Ltd New Entrants with ranking equal or above 180 Exclusions Ticker Name Reason GWA Gwa Group Ltd Failed Eligibility Rank 251 MMS Mcmillan Shakespeare Ltd Failed Eligibility Rank 258 NXL Nuix Ltd Exclusions with ranking equal or below 220 PRN Perenti Global Ltd Exclusions with ranking equal or below 220 VOC Vocus Group Ltd Excluded due to upcoming M&A Please contact [email protected] with any queries. Chi-X Market Operations Phone: +61 2 8078 1701 | Email: [email protected]| Web: chi-x.com.au | Disclaimer Appendix A: Constituent List The index portfolio below is based on data from 1 June 2021. Newly added constituents are in BOLD. Chi-X indices (CXA 200 Index) Ticker Name CBA COMMONWEALTH BANK OF AUSTRALIA BHP BHP GROUP LTD CSL CSL LTD WBC WESTPAC BANKING CORP NAB NATIONAL AUSTRALIA BANK LTD ANZ AUST AND NZ BANKING GROUP WES WESFARMERS LTD WOW WOOLWORTHS GROUP LTD -

Annual Proxy Voting Records

Proxy Voting Record 1 July 2019 to 30 June 2020 SPDR® S&P®/ASX Small Ordinaries Fund Vote Summary Report Reporting Period: 07/01/2019 to 06/30/2020 Location(s): All Locations Institution Account(s): SPDR S&P/ASX Small Ordinaries Fund Jupiter Mines Limited Meeting Date: 07/29/2019 Country: Australia Primary Security ID: Q5135L102 Record Date: 07/27/2019 Meeting Type: Annual Ticker: JMS Shares Voted: 155,869 Proposal Voting Vote Number Proposal Text Proponent Mgmt Rec Policy Rec Instruction 1 Approve Remuneration Report Mgmt For Against Against 2 Approve the Spill Resolution Mgmt Against Against Against 3 Elect Brian Gilbertson as Director Mgmt For Against Against 4 Elect Yeongjin Heo as Director Mgmt For Against Against 5 Elect Melissa North as Director Mgmt For Against Against Charter Hall Long WALE REIT Meeting Date: 07/30/2019 Country: Australia Primary Security ID: Q2308E106 Record Date: 07/28/2019 Meeting Type: Special Ticker: CLW Shares Voted: 30,934 Proposal Voting Vote Number Proposal Text Proponent Mgmt Rec Policy Rec Instruction 1 Ratify Past Issuance of Stapled Securities to Mgmt For For For Institutional, Professional and Other Wholesale Investors Australian Agricultural Company Limited Meeting Date: 07/31/2019 Country: Australia Primary Security ID: Q08448112 Record Date: 07/29/2019 Meeting Type: Annual Ticker: AAC Shares Voted: 42,533 Proposal Voting Vote Number Proposal Text Proponent Mgmt Rec Policy Rec Instruction 2 Approve Remuneration Report Mgmt For Against Against 3 Elect Neil Reisman as Director Mgmt For Against Against