The Influence of Irving Fisher on Milton Friedman's Monetary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Debt-Deflation Theory of Great Depressions by Irving Fisher

THE DEBT-DEFLATION THEORY OF GREAT DEPRESSIONS BY IRVING FISHER INTRODUCTORY IN Booms and Depressions, I have developed, theoretically and sta- tistically, what may be called a debt-deflation theory of great depres- sions. In the preface, I stated that the results "seem largely new," I spoke thus cautiously because of my unfamiliarity with the vast literature on the subject. Since the book was published its special con- clusions have been widely accepted and, so far as I know, no one has yet found them anticipated by previous writers, though several, in- cluding myself, have zealously sought to find such anticipations. Two of the best-read authorities in this field assure me that those conclu- sions are, in the words of one of them, "both new and important." Partly to specify what some of these special conclusions are which are believed to be new and partly to fit them into the conclusions of other students in this field, I am offering this paper as embodying, in brief, my present "creed" on the whole subject of so-called "cycle theory." My "creed" consists of 49 "articles" some of which are old and some new. I say "creed" because, for brevity, it is purposely ex- pressed dogmatically and without proof. But it is not a creed in the sense that my faith in it does not rest on evidence and that I am not ready to modify it on presentation of new evidence. On the contrary, it is quite tentative. It may serve as a challenge to others and as raw material to help them work out a better product. -

Front Matter

Cambridge University Press 978-1-107-10912-4 - The “Conspiracy” of Free Trade: The Anglo-American Struggle Over Empire and Economic Globalization, 1846–1896 Marc-William Palen Frontmatter More information The “Conspiracy” of Free Trade Following the Second World War, the United States would become the leading “neoliberal” proponent of international trade liberalization. Yet for nearly a century before, American foreign trade policy had been dominated by extreme economic nationalism. What brought about this pronounced ideological, political, and economic about-face? How did it affect Anglo-American imperialism? What were the repercussions for the global capitalist order? In answering these questions, The “Conspiracy” of Free Trade offers the first detailed account of the con- troversial Anglo-American struggle over empire and economic globali- zation in the mid to late nineteenth century. The book reinterprets Anglo-American imperialism through the global interplay between Victorian free-trade cosmopolitanism and economic nationalism, unco- vering how imperial expansion and economic integration were mired in political and ideological conflict. Beginning in the 1840s, this conspir- atorial struggle over political economy would rip apart the Republican party, reshape the Democratic, and redirect Anglo-American imperial expansion for decades to come. MARC-WILLIAM PALEN is Lecturer in History at the University of Exeter, and a Research Associate at the US Studies Centre, University of Sydney. © in this web service Cambridge University Press www.cambridge.org -

Deflation and the Fisher Equation

Economic SYNOPSES short essays and reports on the economic issues of the day 2010 ■ Number 27 Deflation and the Fisher Equation William T. Gavin, Vice President and Economist rving Fisher (1867-1947), one of America’s greatest federal funds rate was 2.18 percent and, in the 1980s, it I monetary economists, is famous for many reasons. was a whopping 4.61 percent. One of the most important is the Fisher equation, which states that the nominal interest rate is equal to the real interest rate plus the expected inflation rate. This is a So, according to Irving Fisher, statement about equilibrium in the market for bonds, not one reason to worry about deflation is about the factors that determine these two components. that the federal funds rate is expected Depending on which market rate is used, the expected real return will include a premium for various sources of to be held near zero as the economy risk. For most of post-WWII U.S. history, estimates of this grows out of this recession. risk premium in the federal funds market have been small relative to estimates of the risk-free real interest rate and the expected inflation rate, so they are ignored in this essay. With the federal funds rate near zero since December The chart shows the Fed’s policy rate—the federal funds 2008 and expected to remain there for the next year or two, rate—and the consumer price index (CPI) inflation trend. the Fisher equation has important implications for the The trend is measured as a 25-month centered moving expected inflation rate. -

Interest Rates and Expected Inflation: a Selective Summary of Recent Research

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Explorations in Economic Research, Volume 3, number 3 Volume Author/Editor: NBER Volume Publisher: NBER Volume URL: http://www.nber.org/books/sarg76-1 Publication Date: 1976 Chapter Title: Interest Rates and Expected Inflation: A Selective Summary of Recent Research Chapter Author: Thomas J. Sargent Chapter URL: http://www.nber.org/chapters/c9082 Chapter pages in book: (p. 1 - 23) 1 THOMAS J. SARGENT University of Minnesota Interest Rates and Expected Inflation: A Selective Summary of Recent Research ABSTRACT: This paper summarizes the macroeconomics underlying Irving Fisher's theory about tile impact of expected inflation on nomi nal interest rates. Two sets of restrictions on a standard macroeconomic model are considered, each of which is sufficient to iniplv Fisher's theory. The first is a set of restrictions on the slopes of the IS and LM curves, while the second is a restriction on the way expectations are formed. Selected recent empirical work is also reviewed, and its implications for the effect of inflation on interest rates and other macroeconomic issues are discussed. INTRODUCTION This article is designed to pull together and summarize recent work by a few others and myself on the relationship between nominal interest rates and expected inflation.' The topic has received much attention in recent years, no doubt as a consequence of the high inflation rates and high interest rates experienced by Western economies since the mid-1960s. NOTE: In this paper I Summarize the results of research 1 conducted as part of the National Bureaus study of the effects of inflation, for which financing has been provided by a grait from the American life Insurance Association Heiptul coinrnents on earlier eriiins of 'his p,irx'r serv marIe ti PhillipCagan arid l)y the mnibrirs Ut the stall reading Committee: Michael R. -

American Economic Association

American Economic Association /LIH&\FOH,QGLYLGXDO7KULIWDQGWKH:HDOWKRI1DWLRQV $XWKRU V )UDQFR0RGLJOLDQL 6RXUFH7KH$PHULFDQ(FRQRPLF5HYLHZ9RO1R -XQ SS 3XEOLVKHGE\$PHULFDQ(FRQRPLF$VVRFLDWLRQ 6WDEOH85/http://www.jstor.org/stable/1813352 $FFHVVHG Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/action/showPublisher?publisherCode=aea. Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. American Economic Association is collaborating with JSTOR to digitize, preserve and extend access to The American Economic Review. http://www.jstor.org Life Cycle, IndividualThrift, and the Wealth of Nations By FRANCO MODIGLIANI* This paper provides a review of the theory Yet, there was a brief but influential inter- of the determinants of individual and na- val in the course of which, under the impact tional thrift that has come to be known as of the Great Depression, and of the interpre- the Life Cycle Hypothesis (LCH) of saving. -

A Missing Stop on the Road from Warburton to Friedman-Meiselman

A Missing Stop on the Road from Warburton to Friedman – Meiselman and St. Louis By Michael T. Belongia Department of Economics University of Mississippi Box 1848 University, MS 38677 [email protected] and Peter N. Ireland Department of Economics Boston College 140 Commonwealth Avenue Chestnut Hill, MA 02467 [email protected] June 2021 ABSTRACT: Friedman and Meiselman (1963) typically is recognized as the original study that used a reduced-form equation to evaluate whether fiscal or monetary actions were the dominant influence on aggregate spending. It also provided the foundation for the better- known St. Louis Equation that followed. Missing from this evolution, however, are important precedents by Brunner and Balbach (1959) and Balbach (1963) that also employed a reduced form framework to offer evidence on the same fiscal versus monetary debate. Moreover, they also investigated whether the demand for money function was stable and inversely related to an interest rate, properties necessary in their reasoning before any more general model of national income determination could be developed. With this foundation, they then derived a reduced form expression for personal income from an explicit theoretical model and, in its estimation, they anticipated and addressed some of the empirical criticisms later directed at Friedman-Meiselman and the early versions of the St. Louis Equation. Taken together, the theoretical and empirical work reported in Balbach (1963) and Brunner and Balbach (1959) suggest these papers are clear antecedents of later reduced form expressions and should be recognized as such. Keywords: St. Louis Equation, monetary policy, fiscal policy, reduced form equation JEL Codes: B2, B4, E3 A Missing Stop on the Road from Warburton to Friedman – Meiselman and St. -

Monetary Policy Frameworks and Indicators for the Federal Reserve in the 1920S*

Working Paper Series This paper can be downloaded without charge from: http://www.richmondfed.org/publications/ Monetary Policy Frameworks and Indicators for the Federal Reserve in the 1920s* Thomas M. Humphrey ‡ Federal Reserve Bank of Richmond Working Paper No. 00-7 August 2000 JEL Nos. E5, B1 Keywords: quantity theory, real bills doctrine, scissors effect, policy indicators. Abstract The 1920s and 1930s saw the Fed reject a state-of-the-art empirical policy framework for a logically defective one. Consisting of a quantity theoretic analysis of the business cycle, the former framework featured the money stock, price level, and real interest rates as policy indicators. By contrast, the Fed’s procyclical needs-of-trade, or real bills, framework stressed such policy guides as market nominal interest rates, volume of member bank borrowing, and type and amount of commercial paper eligible for rediscount at the central bank. The start of the Great Depression put these rival sets of indicators to the test. The quantity theoretic set correctly signaled that money and credit were on sharply contractionary paths that would worsen the slump. By contrast, the real bills indicators incorrectly signaled that money and credit conditions were sufficiently easy and needed no correction. This experience shows that policy measures and measurement, no matter how accurate and precise, can lead policymakers astray when embodied in a theoretically flawed framework. *This paper does not necessarily represent the views of the Federal Reserve System or the Federal Reserve Bank of Richmond. The author is indebted to William Gavin, Bob Hetzel, Judy Klein, Mary Morgan, and Anna Schwartz for helpful comments. -

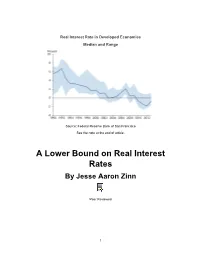

A Lower Bound on Real Interest Rates by Jesse Aaron Zinn

Real Interest Rate in Developed Economies Median and Range Source: Federal Reserve Bank of San Francisco See the note at the end of article. A Lower Bound on Real Interest Rates By Jesse Aaron Zinn Peer Reviewed 1 Jesse Aaron Zinn is an Assistant Professor of Economics in the College of Business at Clayton State University. His research interests include macroeconomics, public finance, and developmental economics. He earned his PhD in Economics at University of California, Santa Barbara. Abstract In this short article, the author demonstrates that real interest rates cannot be lower than -1 (i.e. -100%). He discusses how the textbook approximation to the Fisher equation can lead to the erroneous belief that there is no lower bound on real interest rates. He also speculates that the widespread use of the Fisher equation is why we had yet to realize that a lower bound on real rates exists. This leads him to advocate using and teaching the exact Fisher equation, rather than its approximation. Introduction Negative real interest rates have been common in the United States and other countries since the financial crisis of 2007-8. In fact, Japan has often had negative real interest rates going back to the early 1990s. In some countries, such as Denmark and Switzerland, there have been cases where nominal interest rates have also turned negative, disproving the idea that zero is an impenetrable lower bound on nominal rates. These phenomena have, no doubt, lead many to wonder how low rates can go. The objective of this short piece is to demonstrate the existence of a lower bound on real rates of interest. -

The Midway and Beyond: Recent Work on Economics at Chicago Douglas A

The Midway and Beyond: Recent Work on Economics at Chicago Douglas A. Irwin Since its founding in 1892, the University of Chicago has been home to some of the world’s leading economists.1 Many of its faculty members have been an intellectual force in the economics profession and some have played a prominent role in public policy debates over the past half-cen- tury.2 Because of their impact on the profession and inuence in policy Correspondence may be addressed to: Douglas Irwin, Department of Economics, Dartmouth College, Hanover, NH 03755; email: [email protected]. I am grateful to Dan Ham- mond, Steve Medema, David Mitch, Randy Kroszner, and Roy Weintraub for very helpful com- ments and advice; all errors, interpretations, and misinterpretations are solely my own. Disclo- sure: I was on the faculty of the then Graduate School of Business at the University of Chicago in the 1990s and a visiting professor at the Booth School of Business in the fall of 2017. 1. To take a crude measure, nearly a dozen economists who spent most of their career at Chicago have won the Nobel Prize, or, more accurately, the Sveriges Riksbank Prize in Eco- nomic Sciences in Memory of Alfred Nobel. The list includes Milton Friedman (1976), Theo- dore W. Schultz (1979), George J. Stigler (1982), Merton H. Miller (1990), Ronald H. Coase (1991), Gary S. Becker (1992), Robert W. Fogel (1993), Robert E. Lucas, Jr. (1995), James J. Heckman (2000), Eugene F. Fama and Lars Peter Hansen (2013), and Richard H. Thaler (2017). This list excludes Friedrich Hayek, who did his prize work at the London School of Economics and only spent a dozen years at Chicago. -

Real Interest Rate and Fisher Equation

6. Real interest rate, Fisher equation, Fisher effect 1. Real interest rate The real interest rate of an economy represents the purchasing power of the economy’s nominal interest rate : it is the nominal rate expressed in terms of goods. That the nominal interest rate between period and period 1 is means that, by lending 1 currency unit in , one gets 1 currency units in 1. That the real interest rate between period and period 1 is means that, by lending 1 unit of goods int , one gets 1 units of goods in 1. Thus, expresses purchasing power: the amount of goods obtained from each unit of good lent. 2. An example on the real interest rate Let “goods” be represented by the CPI basket. There are two periods, 1 and 2. The nominal interest rate between 1 and 2 is 10%. The cost of the CPI basket in 1 is 204 EUR. The cost of the CPI basket in 2 is 220 EUR; see the sketch on the right. With this information, the CPI inflation rate is 220 204 7.84%. 204 If 612 EUR are lent in 1. Then 612 1 612 1 0.10 673.2 EUR are obtained in 2. In 1, the purchasing power of 612 EUR is 612/ 612/204 3 baskets. In 2, the purchasing power of 673.2 EUR is 673.2/ 673.2/220 3.06 baskets. The real interest rate measures the change in purchasing power of the money lent. Specifically, transforms 3 baskets into 3.06 baskets. Thus, satisfies 3 1 3.06, so 0.02 2%. -

Hayek's Divorce and Move to Chicago · Econ Journal Watch

Discuss this article at Journaltalk: https://journaltalk.net/articles/5973 ECON JOURNAL WATCH 15(3) September 2018: 301–321 Hayek’s Divorce and Move to Chicago Lanny Ebenstein1 LINK TO ABSTRACT The personal life of a great intellectual is not always highly pertinent. Al- though Friedrich Hayek may have been, in his son’s words, “the great philosopher with feet of clay” (L. Hayek 1994–1997), his clay feet would not necessarily detract from his scholarly contributions. But since Hayek was a moral philosopher—his title at the University of Chicago was Professor of Social and Moral Science—his personal life may be more relevant than would be the case for intellectuals in other fields. The history of Hayek’s personal life has not always, to this point, been accurately told. The story of his divorce and move to Chicago has often been presented as one in which he discovered after World War II on a visit to Vienna to see his mother and other family members that a distant cousin of his, Helene Bitterlich, with whom he had a relationship as a young man, felt free to marry him. After Helene’s husband died, she and Hayek decided to marry, requiring Hayek to divorce his first wife, the former Hella Fritsch. At the same time, it has been suggested, he began to feel out of place in England in the immediate postwar era as a result of the policies of the first Labour Party government. He relocated to America, having first sought a post in the Economics Department at the University of Chicago and then, after being turned down by it as a result of The Road to Serfdom (1944), having been offered a position in the Committee on Social Thought. -

Register of Papers: Laughlin, James Laurence

James Laurenee L&ughlln COMMITTEE ON THE HISTORY OF THE FEDERAL RESERVE SYSTEM Register of Papers Library of Congress Ac. 4783 and add* X III-49-D, 3 5 Add. IB, 10/28/55 JAMES LAUHBNCE LIUGHLIN (1850 - 1933) The papers of Jsaes Laurence Laughlin, professor, writer, economist^ were presented to the Library of Congress in 1934 *nd 1935* by Lawrence Cramer Laughlin. Linear feet of shelf spece occupiedt 5 1/2 Approximete niasber of i terns * 2500 The papers may be used under Library Restrictions. No dedication of literary rights in the unpublished writings of James Laurence L&ughlln. Mr. Laughlin wes the author of "The Federal Reserve Act, Its Origin and Problems," 1933 an<2 many other books on economic and monetary matters. His papers contain material on the Federal Reserve System and banking reform* Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis James Laurence Laughlin LIBRARY OF CONGRESS Ac. 4.788 Ac. 4,788 ad 1 Laughlin, James LaVrence (1850-1933) Papers 1910-1932; 1912-19U includes (among 15 boxes) 1. Bundle of printed pamphlets labelled "Reports and Studies on Federal Reserve Act" hearings, papers by Aldrich etc. 2. Memoranda on banking reform Miscellaneous Correspondence 1913-1914* Glass, Warburg, etc. Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis James Laurence Laughlin Biographic 1 ote 18 £0, Apr. 2 >.rn In Deerfleld, Ohio; son of Harvey and ; apy lla Laughlin 1873 rvarc 1873^78 Taught In Ilopklnson's Classical Schoolp lies ton Io7£# Sept. larrled \lice : cGuffey I876 and HI.