West Cumbria Retail Study Final Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The List of Pharmacies Registered to Sell Ppcs on Our Behalf Is Sorted Alphabetically in Postcode Order

The list of pharmacies registered to sell PPCs on our behalf is sorted alphabetically in postcode order. 0 NAME PREMISES ADDRESS 1 PREMISES ADDRESS 2 PREMISES ADDRESS 3 PREMISES ADDRESS 4 LLOYDS PHARMACY SAINSBURYS, EVERARD CLOSE ST ALBANS HERTFORDSHIRE AL1 2QU BOOTS UK LIMITED 9 ST PETERS STREET ST.ALBANS HERTFORDSHIRE AL1 3DH FREEMAN GRIEVES LTD 111-113 ST PETERS STREET ST.ALBANS HERTFORDSHIRE AL1 3ET LLOYDS PHARMACY PARKBURY HOUSE ST PETER ST ALBANS HERTFORDSHIRE AL1 3HD IMED PHARMACY 67 HATFIELD ROAD ST ALBANS HERTFORDSHIRE AL1 4JE LLOYDS PHARMACY SAINSBURYS, BARNET ROAD LONDON COLNEY ST ALBANS HERTFORDSHIRE AL2 1AB LLOYDS PHARMACY 17 RUSSELL AVENUE ST ALBANS HERTFORDSHIRE AL3 5ES CROWN PHAMRACY 65 HIGH STREET REDBOURN ST ALBANS HERTFORDSHIRE AL3 7LW MANOR PHARMACY (WHEATHAMPSTEAD) LTD 2 HIGH STREET WHEATHAMPSTEAD HERTFORDSHIRE AL4 8AA BOOTS UK LIMITED 23-25 HIGH STREET HARPENDEN HERTFORDSHIRE AL5 2RU LLOYDS PHARMACY 40 HIGH STREET WELWYN GARDEN CITY HERTFORDSHIRE AL6 9EQ LLOYDS PHARMACY 84 HALDENS WELWYN GARDEN CITY HERTFORDSHIRE AL7 1DD BOOTS UK LIMITED 65 MOORS WALK WELWYN GARDEN CITY HERTFORDSHIRE AL7 2BQ BOOTS UK LIMITED 31 COLE GREEN LANE WELWYN GARDEN CITY HERTFORDSHIRE AL7 3PP PEARTREE PHARMACY 110 PEARTREE LANE WELWYN GARDEN CITY HERTFORDSHIRE AL7 3UJ BOOTS UK LIMITED 126 PEARTREE LANE WELWYN GARDEN CITY HERTFORDSHIRE AL7 3XY BOOTS UK LIMITED 31 THE HOWARD CENTRE WELWYN GARDEN CITY HERTFORDSHIRE AL8 6HA LLOYDS PHARMACY SAINSBURYS, CHURCH ROAD WELWYN GARDEN CITY HERTFORDSHIRE AL8 6SA LLOYDS PHARMACY 9 SHOPLANDS WELWYN GARDEN -

Registered Pharmacies 2020-12-01

The list of pharmacies registered to sell PPCs on our behalf is sorted alphabetically in postcode order. 0 NAME PREMISES ADDRESS 1 PREMISES ADDRESS 2 PREMISES ADDRESS 3 PREMISES ADDRESS 4 POSTCODE LLOYDS PHARMACY SAINSBURYS, EVERARD CLOSE ST ALBANS HERTFORDSHIRE AL1 2QU BOOTS UK LIMITED 9 ST PETERS STREET ST.ALBANS HERTFORDSHIRE AL1 3DH ST ALBANS PHARMACY 197 CELL BARNES LANE ST ALBANS HERTFORDSHIRE AL1 5PX LLOYDS PHARMACY SAINSBURYS, BARNET ROAD LONDON COLNEY ST ALBANS HERTFORDSHIRE AL2 1AB NORMANDY PHARMACY 52 WAVERLEY ROAD ST ALBANS HERTFORDSHIRE AL3 5PE QUADRANT PHARMACY 17 THE QUADRANT MARSHALSWICK LANE ST ALBANS HERTFORDSHIRE AL4 9RB BOOTS UK LIMITED 23-25 HIGH STREET HARPENDEN HERTFORDSHIRE AL5 2RU BOOTS UK LIMITED 65 MOORS WALK WELWYN GARDEN CITY HERTFORDSHIRE AL7 2BQ PEARTREE PHARMACY 110 PEARTREE LANE WELWYN GARDEN CITY HERTFORDSHIRE AL7 3UJ COHENS CHEMIST 1 ROBIN HOOD LANE HATFIELD HERTFORDSHIRE AL10 0LD BOOTS UK LIMITED 47 TOWN CENTRE HATFIELD HERTFORDSHIRE AL10 0LD BOOTS UK LIMITED 2A BRINDLEY PLACE BIRMINGHAM WEST MIDLANDS B1 2JB BOOTS UK LIMITED UNIT MSU 10A NEW BULL RING SHOP CTR BIRMINGHAM WEST MIDLANDS B2 4BE BOOTS UK LIMITED 102 NEW STREET BIRMINGHAM WEST MIDLANDS B2 4HQ BOOTS UK LIMITED 71 PERSHORE ROAD EDGBASTON BIRMINGHAM WEST MIDLANDS B5 7NX IPHARM UK LTD 4A, 11 JAMESON ROAD BIRMINGHAM WEST MIDLANDS B6 7SJ PHARMACO 2000 LTD UNIT 4 BOULTBEE BUSINESS UNITS NECHELLS PLACE BIRMINGHAM WEST MIDLANDS B7 5AR J DOCTER LTD BLOOMSBURY VILLAGE CENTRE 67 RUPERT STREET NECHELLS BIRMINGHAM B7 5DT MASTERS UK LTD 55 NECHELLS PARK -

New Additions to CASCAT from Carlisle Archives

Cumbria Archive Service CATALOGUE: new additions August 2021 Carlisle Archive Centre The list below comprises additions to CASCAT from Carlisle Archives from 1 January - 31 July 2021. Ref_No Title Description Date BRA British Records Association Nicholas Whitfield of Alston Moor, yeoman to Ranald Whitfield the son and heir of John Conveyance of messuage and Whitfield of Standerholm, Alston BRA/1/2/1 tenement at Clargill, Alston 7 Feb 1579 Moor, gent. Consideration £21 for Moor a messuage and tenement at Clargill currently in the holding of Thomas Archer Thomas Archer of Alston Moor, yeoman to Nicholas Whitfield of Clargill, Alston Moor, consideration £36 13s 4d for a 20 June BRA/1/2/2 Conveyance of a lease messuage and tenement at 1580 Clargill, rent 10s, which Thomas Archer lately had of the grant of Cuthbert Baynbrigg by a deed dated 22 May 1556 Ranold Whitfield son and heir of John Whitfield of Ranaldholme, Cumberland to William Moore of Heshewell, Northumberland, yeoman. Recites obligation Conveyance of messuage and between John Whitfield and one 16 June BRA/1/2/3 tenement at Clargill, customary William Whitfield of the City of 1587 rent 10s Durham, draper unto the said William Moore dated 13 Feb 1579 for his messuage and tenement, yearly rent 10s at Clargill late in the occupation of Nicholas Whitfield Thomas Moore of Clargill, Alston Moor, yeoman to Thomas Stevenson and John Stevenson of Corby Gates, yeoman. Recites Feb 1578 Nicholas Whitfield of Alston Conveyance of messuage and BRA/1/2/4 Moor, yeoman bargained and sold 1 Jun 1616 tenement at Clargill to Raynold Whitfield son of John Whitfield of Randelholme, gent. -

Copeland Unclassified Roads - Published January 2021

Copeland Unclassified Roads - Published January 2021 • The list has been prepared using the available information from records compiled by the County Council and is correct to the best of our knowledge. It does not, however, constitute a definitive statement as to the status of any particular highway. • This is not a comprehensive list of the entire highway network in Cumbria although the majority of streets are included for information purposes. • The extent of the highway maintainable at public expense is not available on the list and can only be determined through the search process. • The List of Streets is a live record and is constantly being amended and updated. We update and republish it every 3 months. • Like many rural authorities, where some highways have no name at all, we usually record our information using a road numbering reference system. Street descriptors will be added to the list during the updating process along with any other missing information. • The list does not contain Recorded Public Rights of Way as shown on Cumbria County Council’s 1976 Definitive Map, nor does it contain streets that are privately maintained. • The list is property of Cumbria County Council and is only available to the public for viewing purposes and must not be copied or distributed. -

Postal Locality Name Phone Public Address Postcode Christmas Day

Cumbria CCG Christmas Boxing Day New Years Day Postal Locality Name Phone Public Address Postcode Day 25th 26th 1st January December December PARKHOUSE Asda Pharmacy - Carlisle 01228 554119 Chandler Way, Parkhouse, Carlisle, CA3 0JQ Closed 09:00-18:00 10:00-17:00 Cumbria Workington Asda Pharmacy - Workington 01900 607730 Dunmail Park Shopping Centre, Siddick CA14 1NQ Closed 09:00-18:00 10:00-17:00 Road, Workington, Cumbria Carlisle Boots The Chemist - English 01228 542944 43-49 English Street, Carlisle, Cumbria CA3 8JU Closed 08:30-17:30 Closed Street - Carlisle Cockermouth Boots UK Limited - Cockermouth 01900 823160 56-58 Main Street, Cockermouth, CA13 9LU Closed 09:00-19:30 Closed Cumbria Keswick Boots UK Limited - Keswick 017687 72383 31 Main Street, Keswick, Cumbria CA12 5BL Closed 09:30-17:00 09:30-17:00 Penrith Boots UK Limited - Penrith 01768 862735 Unit 3, Angel Square, Penrith, Cumbria CA11 7BT Closed 10:00-16:00 Closed Whitehaven Boots UK Limited - Whitehaven 01946 692042 26 King Street, Whitehaven, Cumbria CA28 7JN Closed 10:00-17:30 Closed Workington Boots UK Limited - Workington 01900 602405 27-31 Murray Road, Workington, CA14 2AB Closed 09:00-16:00 Closed Cumbria Cockermouth Castlegate Pharmacy - 017687 72383 Cockermouth Community Hospital and CA13 9HT 10:00-12:00 Closed Closed Cockermouth - Cumbria Health Centre, Isel Road, Cockermouth, Cumbria Cleator Moor Cohens Chemist - Cleator Moor 01946 810373 Cleator Moor Health Centre, Birks CA25 5HP Closed Closed 18:00-20:00 Road, Cleator Moor, Cumbria Keswick Cohens Chemist - -

Store List For

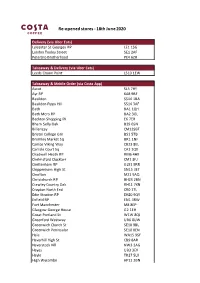

Re-opened stores - 18th June 2020 Delivery (via Uber Eats) Leicester St Georges RP LE1 1SG London Tooley Street SE1 2AF Peterbro Brotherhood PE4 6ZR Takeaway & Delivery (via Uber Eats) Leeds Crown Point LS10 1EW Takeaway & Mobile Order (via Costa App) Ascot SL5 7HY Ayr RP KA8 9BF Basildon SS14 1BA Basildon Pipps Hill SS14 3AF Bath BA1 1QH Bath Mero RP BA2 3GL Beckton Shopping Pk E6 7ER Bham Selly Oak B29 6SN Billericay CM129BT Bristol College Grn BS1 5TB Bromley Market Sq BR1 1NF Cambs Viking Way CB23 8EL Carlisle CoUrt Sq CA1 1QX Chadwell Heath RP RM6 4HX Chelmsford Clocktwr CM1 3FJ Cheltenham RP GL51 9RR Chippenham High St SN15 3ET Chorlton M21 9AQ ChristchUrch RP BH23 2BN Crawley CoUntry Oak RH11 7XN Croydon North End CR0 1TL Edin Straiton RP EH20 9QY Enfield RP EN1 3RW Fort Manchester M8 8EP Glasgow George HoUse G2 1EH Great Portland St W1W 8QJ Greenford Westway UB6 0UW Greenwich ChUrch St SE10 9BL Greenwich PeninsUlar SE10 0EN Hale WA15 9SF Haverhill High St CB9 8AR Haverstock Hill NW3 2AG Hayes UB3 3EX Hayle TR27 5LX High Wycombe HP11 2BN Holloway Road N7 6PN Kingston KT1 1JH Leeds Merrion LS2 8BT Leicester Haymarket LE1 3YR Leigh on Sea SS9 1PA Lon Brent Cross Sth NW2 1LS Lon Charlton SE7 7AJ Lon Friern Bridge RP N11 3PW Lon Leyton Mills RP E10 5NH Lon SoUthampton St WC2E 7HG Lon SoUthwark SE1 8LP Lon Staples CornerRP NW2 6LW Lon Wembley Central HA9 7AJ LoUghton IG10 1EZ Manchester Market St M1 1WA Manchester Portland M60 1HR Milton Keynes Kingst MK10 0BA NewqUay TR7 1DH Northampton NN1 2AJ Orpington BR5 3RP Perth Inveralmond RP -

Stop Smoking Providers

Stop Smoking Service The information below is correct as of the 23rd Jan 2018 Community Pharmcy Cumbria would recommend that patients contact the pharmacy for an appointment. Locality Name Address Telephone Allerdale AF Norman Chemists Ltd 55 Senhouse Street, Maryport CA15 6BL 01900 812615 Allerdale Alneburgh Pharmacy Ltd Alneburgh House, Ewanrigg Road, Maryport CA15 8EL 01900 819111 Allerdale Asda Pharmacy Dunmail Park Shopping Centre, Maryport Road, Workington CA14 1NQ 01900 607730 Allerdale Boots UK Ltd 31 Main Street, Keswick CA12 5BL 01768 772383 Allerdale Boots UK Ltd West Street Health Centre, West Street, Aspatria CA7 3HH 016973 20236 Allerdale Boots UK Ltd 29 Murray Road, Workington CA14 2AB 01900 602405 Allerdale Castlegate Pharmacy Cockermouth Cottage Hospital, Isel Road, Cockermouth CA13 9HT 01900 826018 Allerdale Harrington Pharmacy 25 Church Road, Harrington, Workington CA14 5QA 01946 833565 Allerdale HS Dobie Chemist 29 Curzon Street, Maryport CA15 6LN 01900 812662 Allerdale JWW Allison and Sons Ltd 31 Main Street, Cockermouth CA13 9LE 01900 822292 Allerdale Moorclose Pharmacy Unit 6,Moorclose Rd/About, Moorclose, Workington, CA14 3RW 01900 62618 Allerdale Seaton Pharmacy 91 Main Road, Seaton, Workington CA14 1JE 01900 67679 Allerdale Tuschem Ltd Workington Community Hospital, Park Lane, Workington CA14 2RW 01900 705130 Allerdale Well 1-3 Station Road, Silloth CA7 4AE 016973 31394 Allerdale Well 14 King Street, Wigton, Carlisle CA7 9DT 01697 342445 Carlisle Asda Pharmacy Chandler Way, Parkhouse Kingstown Ind Est, Carlisle -

Registered Pharmacies 2021-02-04

The list of pharmacies registered to sell PPCs on our behalf is sorted alphabetically in postcode order. 0 NAME PREMISES ADDRESS 1 PREMISES ADDRESS 2 PREMISES ADDRESS 3 PREMISES ADDRESS 4 POSTCODE LLOYDS PHARMACY SAINSBURYS, EVERARD CLOSE ST ALBANS HERTFORDSHIRE AL1 2QU BOOTS UK LIMITED 9 ST PETERS STREET ST.ALBANS HERTFORDSHIRE AL1 3DH ST ALBANS PHARMACY 197 CELL BARNES LANE ST ALBANS HERTFORDSHIRE AL1 5PX LLOYDS PHARMACY SAINSBURYS, BARNET ROAD LONDON COLNEY ST ALBANS HERTFORDSHIRE AL2 1AB NORMANDY PHARMACY 52 WAVERLEY ROAD ST ALBANS HERTFORDSHIRE AL3 5PE QUADRANT PHARMACY 17 THE QUADRANT MARSHALSWICK LANE ST ALBANS HERTFORDSHIRE AL4 9RB BOOTS UK LIMITED 23-25 HIGH STREET HARPENDEN HERTFORDSHIRE AL5 2RU BOOTS UK LIMITED 65 MOORS WALK WELWYN GARDEN CITY HERTFORDSHIRE AL7 2BQ PEARTREE PHARMACY 110 PEARTREE LANE WELWYN GARDEN CITY HERTFORDSHIRE AL7 3UJ COHENS CHEMIST 1 ROBIN HOOD LANE HATFIELD HERTFORDSHIRE AL10 0LD BOOTS UK LIMITED 47 TOWN CENTRE HATFIELD HERTFORDSHIRE AL10 0LD BOOTS UK LIMITED 2A BRINDLEY PLACE BIRMINGHAM WEST MIDLANDS B1 2JB BOOTS UK LIMITED UNIT MSU 10A NEW BULL RING SHOP CTR BIRMINGHAM WEST MIDLANDS B2 4BE BOOTS UK LIMITED 102 NEW STREET BIRMINGHAM WEST MIDLANDS B2 4HQ BOOTS UK LIMITED 71 PERSHORE ROAD EDGBASTON BIRMINGHAM WEST MIDLANDS B5 7NX IPHARM UK LTD 4A, 11 JAMESON ROAD BIRMINGHAM WEST MIDLANDS B6 7SJ PHARMACO 2000 LTD UNIT 4 BOULTBEE BUSINESS UNITS NECHELLS PLACE BIRMINGHAM WEST MIDLANDS B7 5AR J DOCTER LTD BLOOMSBURY VILLAGE CENTRE 67 RUPERT STREET NECHELLS BIRMINGHAM B7 5DT MASTERS UK LTD 55 NECHELLS PARK -

Applications Received by Copeland Borough Council for Period

Applications Received by Copeland Borough Council for period Week ending 17 June 2011 App No. 4/11/2272/0F1 Date 13/06/2011 Received Proposal CONVERSION OF EXISTING BUILDING INTO 2 NO. SELF CONTAINED THREE Case Officer Nick Hayhurst BEDROOMED DWELLINGS Site 14 ENNERDALE ROAD, CLEATOR MOOR Parish Cleator Moor Applicant Mrs G Roberts Map Ref: 302157 515003 Address Startoes Farm, Pica, DISTINGTON, Cumbria, Agent Edwin Thompson Address 28 St John Street, KESWICK, Cumbria CA12 5AF, FAO Christopher Reeve App No. 4/11/2275/0F1 Date 15/06/2011 Received Proposal CONSTRUCTION OF ADDITIONAL STOREY ABOVE EXISTING GROUND FLOOR Case Officer Rachel Carrol EXTENSION Site 4 BECKSIDE, THE GREEN, MILLOM Parish Millom Without Applicant Mr M Huddleston Map Ref: 317889 484684 Address 3 Willowside Park, Haverigg, MILLOM, Cumbria LA18 4PT Agent Address App No. 4/11/2282/0O1 Date 15/06/2011 Received Proposal OUTLINE APPLICATION FOR 5 NO. THREE BEDROOMED TERRACED HOUSES Case Officer Simon Blacker Site LAND ADJACENT TO FRIZINGTON VETERANS CLUB, LINDOW STREET, Parish Arlecdon & Frizington FRIZINGTON Applicant Minotaur Construction Ltd Map Ref: 303565 517361 Address Speedwell Mill, Old Coach Road, Tansley, MATLOCK, Derbyshire DE4 5FY, FAO Michael Foster Agent IDIR Address c/o McDowell + Benedetti, Karen House, 1-11 Baches Street, LONDON N1 6DL, FAO Jane Clossick Applications Received by Copeland Borough Council for period Week ending 17 June 2011 App No. 4/11/2284/0A1 Date 13/06/2011 Received Proposal ERECTION OF THREE SALES BOARD ADVERTISEMENTS Case Officer Nick Hayhurst Site WASTWATER ROAD, WOODHOUSE ROAD & JUNCTION OF WOODHOUSE ROAD & Parish Whitehaven LOW ROAD, WOODHOUSE, WHITEHAVEN Applicant Story Homes Map Ref: 297413 516112 Address Burgh Road Industrial Estate, CARLISLE, Cumbria CA2 7NA, FAO Rachel Lightfoot Agent Address App No. -

Appendix F Dunmail Park Consultation

Appendix F Dunmail Park Consultation Consultation letter Map of Dunmail Park (site 4/WOR/106/M) Deposit locations for consultation information List of those notified of the consultation either by letter or email Website screenshots GDPR consent form Consultation Statement Our Ref: SA Local Plan update/05/2018 This matter is being dealt by: Planning Policy Direct Line: 01900 878703 E-Mail: [email protected] 31 May 2018 Dear Sir/Madam ALLERDALE LOCAL PLAN (PART 2): SITE ALLOCATIONS LOCAL PLAN UPDATE & CONSULTATION ON LAND AT DUNMAIL PARK Dunmail Park. Further to our focussed consultation earlier this year, an error was made regarding the site area for the proposed retail/mixed use site submitted at Dunmail Park, Workington, reference 4/WOR/106/M (page 23 of the Focused Consultation document 2017). The correct site plan is now available for inspection on the Council’s website: (https://www.allerdale.gov.uk/en/planning-building-control/planning-policy/local-plan-part-2/site-allocation- process/). A hard copy of the correct plan is available at the Council’s offices at Allerdale House, Workington between 9:00 am and 5:00 pm Monday to Thursday and 9:00 am and 4:30 pm on Fridays (0303 123 1702). Copies are also available for inspection at the following locations during their normal opening hours: • Aspatria Library: Local Link, The Brandraw, Aspatria, CA7 3EZ (016973 20515) • Cockermouth Library Link: Main Street, Cockermouth, CA13 9LU (01900 7067170) • Maryport Library: Lawson Street, Maryport CA15 6ND (01900 812384) • Maryport Customer Services Centre: Town Hall, Senhouse Street, Maryport CA15 6BH (0303 123 1702) • Silloth Library: The Discovery Centre, Liddell Street, Silloth CA7 4DD (016973 32195) • Wigton Library: High Street, Wigton (016973 66150) • Wigton Local Link: Community Office, Market Hall, Wigton CA7 9AA (0303 123 1702) • Workington Library: Vulcans Lane, Workington, CA14 2ND (01900 706170) If you have any comments to make on this site please submit them in writing either by email or post, no later than 4pm 29 June 2018. -

CLEATOR MOOR Spatial Framework: a Vision for Cleator Moor

CLEATOR MOOR Spatial Framework: A vision for Cleator Moor August 2018 CLEATOR MOOR Spatial Framework: A vision for Cleator Moor CONTENTS Preface 4 01 Introduction 6 Contact: 02 Emerging Vision Objectives 11 Copeland Borough Council, The Copeland Centre, Catherine Street, Whitehaven, 03 Spatial Framework 17 Cumbria, CA28 7SJ. tel: 01946 598300 email: [email protected] Appendices: web: www.copeland.gov.uk twitter: @copelandbc A Consultation Summary 31 Please note, this report is intended to be viewed and printed as an A3 double-sided document with cover page. All Ordnance Survey imagery © Crown copyright & database rights (2018 Ordnance Survey (100019619) © Copeland Borough Council 2018 Prepared by Arup on behalf of Copeland Borough Council. August 2018 PREFACE Cleator Moor: Spatial Framework 3 PREFACE Copeland Borough Council is leading the preparation The Spatial Framework is intended to: of Spatial Frameworks covering the four main towns in the Borough: Whitehaven, Cleator Moor, Millom 1. Provide clarity on the nature, scale and location of and Egremont. potential growth within Cleator Moor; The Council’s key objective is to produce a 2. Give confidence to key partners, investors and the comprehensive vision for Cleator Moor that: community in the future of Cleator Moor through leadership and direction and engagement in the - Identifies the opportunity sites for commercial, reshaping of key areas; and leisure, tourism or residential uses; 3. Deliver greater certainty for potential investors - Supports healthy spaces placemaking and improves and developers by ensuring that the Spatial social wellbeing and cohesion; Framework is integrated within the Council’s planning framework. - Enables better access and movement through rethinking highways, cycle paths, pedestrian routes and parking. -

Ken Bradford

Ken Bradford In August 2018, Ken Bradford died following a short illness. He was aged 69. Ken was a founding member of the Whitehaven Harbour Youth Project and part of the team who created this mission statement: - “Giving young people opportunities to develop their potential, to understand themselves and others, to enjoy life, and to contribute positively to the world” He volunteered his time as a Trustee for over 20 years and was committed to ensuring that the project stayed true to its guiding principles. His wisdom, compassion, expertise and humour have helped to shape the project as it is today. He is sorely missed by all those who were fortunate enough to know him. In our Annual Report 2015-2016 we published a ‘Close Up With Ken’ interview. We have included it again in this report. Enjoy. First Published November 2016 Contents Pg 5-6 2017-2018 Highlights Pg 7-8 Programme Design and Partnerships Pg 9-10 Comments and Feedback Pg 11-12 Sea Bins Project and Whitehaven Marina Pg 13-18 Activities and Events in Pictures Pg 19-20 Funders and Supporters Pg 21 Staff, Volunteers & Trustees Pg 22 Trustees Report Pg 23 Financial Summary Pg 24 What’s On Every Week 2017-2018 Highlights 1104 young people have taken We took over the delivery of part in our activities this year. Post code FUSION Youth Group for analysis shows us that 32% of these live in young people aged 16-25 with wards that rank within the 20% most Special Educational Needs. deprived areas in England.