Community Reinvestment Act Performance Evaluation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Toolkit for Working with the Media

Utilizing the Media to Facilitate Social Change A Toolkit for Working with the Media WEST VIRGINIA FOUNDATION for RAPE INFORMATION and SERVICES www.fris.org 2011 Media Toolkit | 2 TABLE OF CONTENTS Media Advocacy……………………………….. ……….. 3 Building a Relationship with the Media……... ……….. 3 West Virginia Media…………………………………….. 4 Tips for Working with the Media……………... ……….. 10 Letter to the Editor…………………………….. ……….. 13 Opinion Editorial (Op-Ed)…………………….. ……….. 15 Media Advisory………………………………… ……….. 17 Press/News Release………………………….. ……….. 19 Public Service Announcements……………………….. 21 Media Interviews………………………………. ……….. 22 Survivors’ Stories and the Media………………………. 23 Media Packets…………………………………. ……….. 25 Media Toolkit | 3 Media Advocacy Media advocacy can promote social change by influencing decision-makers and swaying public opinion. Organizations can use mass media outlets to change social conditions and encourage political and social intervention. When working with the media, advocates should ‘shape’ their story to incorporate social themes rather than solely focusing on individual accountability. “Develop a story that personalizes the injustice and then provide a clear picture of who is benefiting from the condition.” (Wallack et al., 1999) Merely stating that there is a problem provides no ‘call to action’ for the public. Therefore, advocates should identify a specific solution that would allow communities to take control of the issue. Sexual violence is a public health concern of social injustices. Effective Media Campaigns Local, regional or statewide campaigns can provide a forum for prevention, outreach and raising awareness to create social change. This toolkit will enhance advocates’ abilities to utilize the media for campaigns and other events. Campaigns can include: public service announcements (PSAs), awareness events (Take Back the Night; The Clothesline Project), media interviews, coordinated events at area schools or college campuses, position papers, etc. -

NRC AM Radio Log, 30Th Edition the NRC AM Radio Log Is Unbound and Three- Hole Punched for Standard Binders

• Serving DX’ers since 933 • Volume 77, No. 2 • DecemberNews 2, 2009 • (ISSN 0737-659) Inside … 2 ...Radio Collection in Oak Forest DX 2 ...AM Switch 22 ...Geomagnetic Indices 4 ...DDXD 10 ...IDXD 11 ...Finding Online Parallels 12 ...Using the NRC Pattern Book as a DX Tool 16 ...College Sports Networks 20 ...NRC Contests CPC Test Calendar DXN Publishing Schedule, Volume 77 WGGH IL 1150 Feb. 6 0100-0200 Deadline Publ Date Deadline Publ Date 13. Dec. 26 Jan. 4 22. Feb. 26 Mar. 8 From the Publisher … Don’t worry about not 14. Jan. 2 Jan. 23. Mar. 5 Mar. 5 receiving a copy of DX News in your mailbox next 15. Jan. 8 Jan. 8 24. Mar. 9 Mar. 29 week, once you’ve come up for air from your stock- 16. Jan. 5 Jan. 25 25. Apr. 9 Apr. 9 ing over your fireplace. We are now in our annual 17. Jan. 22 Feb. 26. May 7 May 7 skip week, when we give editors and publishers 18. Jan. 29 Feb. 8 27. June 4 June 4 and everyone who is connected with the pub- 19. Feb. 5 Feb. 5 28. July 9 July 9 lication of DXN a week off to enjoy the holiday 20. Feb. 2 Feb. 22 29. Aug. 6 Aug. 6 season with their families. Merry Christmas and 2. Feb. 9 Mar. 30. Sept. 7 Sept. 27 happy holidays, everyone! (And if you do run into DX Time Machine subscription problems, contact the membership From the pages of DX News chairman, not the publisher … his address is on 25 years ago … from the December 3, 984 the back cover.) DXN: J. -

Issue 209 Music & Mornings Many Factors Determine the Amount of Music a Country Station Plays in Morning Drive

September 13, 2010 Issue 209 Music & Mornings Many factors determine the amount of music a Country station plays in morning drive. The competitive situation, spot load, caliber of air talent and even a change in morning shows are among them. Most recently, PPM ratings have led a number of programmers to increase the amount of music heard between 6-10am. For purposes of this week’s study, we looked at a variety of market situations to see how many songs were played in morning drive on a Wednesday for the last 12 months (excluding December 2009). As always, all airplay information comes from our friends at Mediabase 24/7. Stand Alone PPM Markets KKGO/Los Angeles has added a couple of songs per hour in the Medal Heads: “Not bad for an old radio guy!” says WGH-FM/AM/Norfolk last three months. It averaged about 12 songs between 6-9am up Dir. of Programming and Operations John Shomby. He and his niece Sara until about three months ago when it bumped to 14-15 songs in that (left) cheese for the camera after running the Virginia Beach Rock & Roll Half Marathon. At right (l-r), WWFG/Salisbury-Ocean City morning host time frame. Its 9am hour has stayed steady at 14 tunes throughout John Trout (5k), MM Jefferson Ward and Clear Channel’s Diane Walsh the last year. (both half-marathon) celebrate completing the local Hidden Treasures WUSN/Chicago has been stable in its morning airplay. It routinely runs. Each earned a podium finish in their age groups. has aired six-seven songs in the first hour of morning drive, seven- eight songs in the second hour, eight-nine songs in the third hour and McGraw’s Super In Dallas 10-11 songs in the final drive-time hour. -

Original, PATRICIA M·CHUH

PEPPER & CORAZZINI VINCENT A PEPPER GREGG P.SKALL L. L. P. ROBERT F. CORAlllNI E. THEODORE MALLYCK PETER GUTMANN ATTORNEYS AT LAW OF COUNSEL JOHN F. GARllGLIA 1776 K STREET, NORTHWEST, SUITE 200 FREDERICK W. FORO NEAl. J.FRIEOMAN 1909·1986 ELLEN S. MANDELL WASHINGTON, D. C.20006 HOWARD J. BARR TELECOPIER (202) 296-5572 (202) 296-0600 MICHAEL J. LEHMKUHL)II; INTERN ET [email protected] SUZANNE C.SPINK * WEB SITE HTTP·i../WWW.COMMLAW.COM MICHAEL H. SHACTER KEVIN l.SIEBERT '* ORIGINAl, PATRICIA M·CHUH III NOT ADMITTED IN O. C. JUly 2, 1997 RECEIVED Mr. William F. Caton Acting Secretary JUL - 2 1997 Federal Communications Commission FEDEIW. COMIINCATXlNS COMMISSION Washington, D.C. 20554 OffICE OF THE SECRETARY Re: Amendment of section 73.202(b), FM Table of Allotments (Elkhorn city, Kentucky and Clinchco, virginia) Dear Mr. Caton: Transmitted herewith on behalf of East Kentucky Broadcasting Company is an original and four copies of a Petition for Rule Making seeking the commencement of a proceeding to amend the FM Table of Allotments to SUbstitute Channel 22lA for Channel 276A at Elkhorn City, and modify the license of WPKE-FM, Elkhorn city, Kentucky to specify operation on Channel 221A; and to SUbstitute Channel 276A for Channel 22lA at Clinchco, Virginia, and modify the license of WDIC-FM, Clinchco, Virginia to specify operation on Channel 276A. Should any questions arise concerning this matter, please contact this office directly. Sincerely, &f'~. ~:-F~ Garziglia Enclosure Nc ;'j' t· Li~:' :0 .~---_._-------'_._.__ . Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. -

LWTW Artist / Song Title / Label Spins

L T Wks On Spins + Stations Adds W W - Chart Artist / Song Title / Label 2 1 LUKE COMBS/Forever After All/River House / Columbia Nashville 3770 239 130 1 11 1 2 JAKE OWEN/Made For You/Big Loud Records 3674 -141 127 0 55 3 3 SAM HUNT/Breaking Up Was Easy In The 90's/MCA Nashville 3564 99 120 1 31 4 4 ERIC CHURCH/Hell Of A View/EMI Records Nashville (UMGN) 3493 184 128 0 27 7 5 DIERKS BENTLEY/Gone/Capitol Records Nashville 3047 236 129 0 29 6 6 BLAKE SHELTON/Minimum Wage/Warner Music Nashville 2915 -14 131 0 17 8 7 CHRIS YOUNG & KANE BROWN/Famous Friends/RCA Nashville (SMN) 2875 190 131 0 20 9 8 JASON ALDEAN/Blame It On You/Broken Bow Records (BBRMG) 2800 147 129 0 27 11 9 MIRANDA LAMBERT/Settling Down/Vanner Records / RCA Nashville (SMN) 2595 144 134 0 35 13 10 DYLAN SCOTT/Nobody/Curb Records 2493 103 125 0 64 15 11 JORDAN DAVIS/Almost Maybes/MCA Nashville 2327 2 123 0 50 14 12 KEITH URBAN AND P!NK/One Too Many/Capitol Records Nashville 2306 -60 121 0 33 17 13 COLE SWINDELL/Single Saturday Night/Warner Music Nashville/WEA 2198 183 124 0 46 16 14 JUSTIN MOORE/We Didn't Have Much/Valory Music Co. (BMLG) 2136 -1 133 1 29 18 15 CARLY PEARCE/Next Girl/Big Machine Records 2031 101 129 0 34 20 16 THOMAS RHETT/Country Again/Valory Music Co. (BMLG) 1953 267 122 7 3 19 17 TIM MCGRAW & TYLER HUBBARD/Undivided/Big Machine Records 1892 -26 125 0 17 21 18 LUKE BRYAN/Waves/Capitol Records (UMG) 1835 205 123 3 4 10 19 RASCAL FLATTS/How They Remember You/Big Machine Records (BMLG) 1724 -751 125 0 46 24 20 ELVIE SHANE/My Boy/Wheelhouse (BBRMG) 1707 180 116 5 30 22 21 LAINEY WILSON/Things A Man Oughta Know/Broken Bow Records (BBRMG) 1618 39 119 2 23 23 22 DAN + SHAY/Glad You Exist/Warner Bros. -

Attachment a DA 19-526 Renewal of License Applications Accepted for Filing

Attachment A DA 19-526 Renewal of License Applications Accepted for Filing File Number Service Callsign Facility ID Frequency City State Licensee 0000072254 FL WMVK-LP 124828 107.3 MHz PERRYVILLE MD STATE OF MARYLAND, MDOT, MARYLAND TRANSIT ADMN. 0000072255 FL WTTZ-LP 193908 93.5 MHz BALTIMORE MD STATE OF MARYLAND, MDOT, MARYLAND TRANSIT ADMINISTRATION 0000072258 FX W253BH 53096 98.5 MHz BLACKSBURG VA POSITIVE ALTERNATIVE RADIO, INC. 0000072259 FX W247CQ 79178 97.3 MHz LYNCHBURG VA POSITIVE ALTERNATIVE RADIO, INC. 0000072260 FX W264CM 93126 100.7 MHz MARTINSVILLE VA POSITIVE ALTERNATIVE RADIO, INC. 0000072261 FX W279AC 70360 103.7 MHz ROANOKE VA POSITIVE ALTERNATIVE RADIO, INC. 0000072262 FX W243BT 86730 96.5 MHz WAYNESBORO VA POSITIVE ALTERNATIVE RADIO, INC. 0000072263 FX W241AL 142568 96.1 MHz MARION VA POSITIVE ALTERNATIVE RADIO, INC. 0000072265 FM WVRW 170948 107.7 MHz GLENVILLE WV DELLA JANE WOOFTER 0000072267 AM WESR 18385 1330 kHz ONLEY-ONANCOCK VA EASTERN SHORE RADIO, INC. 0000072268 FM WESR-FM 18386 103.3 MHz ONLEY-ONANCOCK VA EASTERN SHORE RADIO, INC. 0000072270 FX W289CE 157774 105.7 MHz ONLEY-ONANCOCK VA EASTERN SHORE RADIO, INC. 0000072271 FM WOTR 1103 96.3 MHz WESTON WV DELLA JANE WOOFTER 0000072274 AM WHAW 63489 980 kHz LOST CREEK WV DELLA JANE WOOFTER 0000072285 FX W206AY 91849 89.1 MHz FRUITLAND MD CALVARY CHAPEL OF TWIN FALLS, INC. 0000072287 FX W284BB 141155 104.7 MHz WISE VA POSITIVE ALTERNATIVE RADIO, INC. 0000072288 FX W295AI 142575 106.9 MHz MARION VA POSITIVE ALTERNATIVE RADIO, INC. 0000072293 FM WXAF 39869 90.9 MHz CHARLESTON WV SHOFAR BROADCASTING CORPORATION 0000072294 FX W204BH 92374 88.7 MHz BOONES MILL VA CALVARY CHAPEL OF TWIN FALLS, INC. -

Academic Catalog 2016 - 2017

Academic Catalog 2016 - 2017 2016 – 2017 Catalog Southern West Virginia Community and Technical College 1-866-SWVCTC1 www.southernwv.edu This catalog is for informational purposes only and is not considered a binding contract between Southern West Virginia Community and Technical College and its students. The College reserves the right to change any statement in this publication concerning, but not limited to, rules, policies, tuition, fees, refunds, curricula, and courses without advance notice or obligation. Failure to read this catalog does not excuse students from the regulations and requirements described herein. Institutional Accreditation Southern West Virginia Community and Technical College is accredited by the: Higher Learning Commission Radiologic Technology 230 South LaSalle Street, Suite 7-500 Joint Review Committee on Education in Radiologic Chicago, Illinois 60604-1413 Technology Phone: 312.263.0456 or 800.621.7440 20 N. Wacker Drive, Suite 2850 Fax: 312.263.7462 Chicago, IL 60606-3182 http://www.hlcommission.org Phone: 312.704.5300 Fax: 312.704.5304 Programmatic Accreditation http://www.jrcert.org Agencies accrediting specific program offerings at Southern West Virginia Community and Technical College include: Respiratory Care Technology Commission on Accreditation for Respiratory Care Medical Laboratory Technology 1248 Harwood Road National Accrediting Agency for Clinical Laboratory Bedford, TX 76021-4244 Sciences Phone: 817.283.2835 5600 River Road, Suite 720 Fax: 817.354.8519 Rosemont, IL 60018 http://www.coarc.com Phone: -

List of Radio Stations in West Virginia

Not logged in Talk Contributions Create account Log in Article Talk Read Edit View history Search Wikipedia List of radio stations in West Virginia From Wikipedia, the free encyclopedia Main page The following is a list of FCC-licensed radio stations in the U.S. state of West Virginia, which can Contents be sorted by their call signs, frequencies, cities of license, licensees, and programming formats. Featured content Current events Contents [hide] Random article 1 List of radio stations Donate to Wikipedia 2 Defunct Wikipedia store 3 See also 4 References Interaction 5 Bibliography Help 6 External links About Wikipedia 7 Images Community portal Recent changes Contact page List of radio stations [edit] Tools This list is complete and up to date as of December 17, 2018. What links here Related changes Call City of [2][3] [4] Upload file Frequency Licensee Format sign License [1][2] Special pages open in browser PRO version Are you a developer? Try out the HTML to PDF API pdfcrowd.com Permanent link Princeton Broadcasting, WAEY 1490 AM Princeton Southern gospel Page information Inc. Wikidata item Webster Cite this page WAFD 100.3 FM Summit Media, Inc. Hot adult contemporary Springs Print/export WAGE- Southern Appalachian 106.5 FM Oak Hill Variety Create a book LP Labor School Download as PDF West Virginia Radio Printable version WAJR 1440 AM Morgantown News/Talk/Sports Corporation In other projects WAJR- West Virginia Radio 103.3 FM Salem News/Talk/Sports Wikimedia Commons FM Corporation of Salem Languages West Virginia – Virginia WAMN 1050 AM Green Valley Classic country Add links Media, LLC WAMX 106.3 FM Milton Capstar TX LLC Classic rock WASP- Spring Valley High 104.5 FM Huntington Variety LP School (Students) WAXE- Coal Mountain 106.9 FM St. -

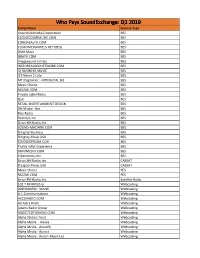

Licensee Count Q1 2019.Xlsx

Who Pays SoundExchange: Q1 2019 Entity Name License Type Aura Multimedia Corporation BES CLOUDCOVERMUSIC.COM BES COROHEALTH.COM BES CUSTOMCHANNELS.NET (BES) BES DMX Music BES GRAYV.COM BES Imagesound Limited BES INSTOREAUDIONETWORK.COM BES IO BUSINESS MUSIC BES It'S Never 2 Late BES MTI Digital Inc - MTIDIGITAL.BIZ BES Music Choice BES MUZAK.COM BES Private Label Radio BES Qsic BES RETAIL ENTERTAINMENT DESIGN BES Rfc Media - Bes BES Rise Radio BES Rockbot, Inc. BES Sirius XM Radio, Inc BES SOUND-MACHINE.COM BES Stingray Business BES Stingray Music USA BES STUDIOSTREAM.COM BES Thales Inflyt Experience BES UMIXMEDIA.COM BES Vibenomics, Inc. BES Sirius XM Radio, Inc CABSAT Stingray Music USA CABSAT Music Choice PES MUZAK.COM PES Sirius XM Radio, Inc Satellite Radio 102.7 FM KPGZ-lp Webcasting 999HANKFM - WANK Webcasting A-1 Communications Webcasting ACCURADIO.COM Webcasting Ad Astra Radio Webcasting Adams Radio Group Webcasting ADDICTEDTORADIO.COM Webcasting Aloha Station Trust Webcasting Alpha Media - Alaska Webcasting Alpha Media - Amarillo Webcasting Alpha Media - Aurora Webcasting Alpha Media - Austin-Albert Lea Webcasting Alpha Media - Bakersfield Webcasting Alpha Media - Biloxi - Gulfport, MS Webcasting Alpha Media - Brookings Webcasting Alpha Media - Cameron - Bethany Webcasting Alpha Media - Canton Webcasting Alpha Media - Columbia, SC Webcasting Alpha Media - Columbus Webcasting Alpha Media - Dayton, Oh Webcasting Alpha Media - East Texas Webcasting Alpha Media - Fairfield Webcasting Alpha Media - Far East Bay Webcasting Alpha Media -

2014–2015 Catalog

2014–2015 Catalog Southern West Virginia Community and Technical College 1-866-SWVCTC1 www.southernwv.edu This catalog is for informational purposes only and is not considered a binding contract between Southern West Virginia Community and Technical College and its students. The College reserves the right to change any statement in this publication concerning, but not limited to, rules, policies, tuition, fees, refunds, curricula, and courses without advance notice or obligation. Failure to read this catalog does not excuse students from the regulations and requirements described herein. Institutional Accreditation Southern West Virginia Community and Technical College is accredited by the: Higher Learning Commission of the North Central Radiologic Technology Association of Schools and Colleges Joint Review Committee on Education in Radiologic 230 South LaSalle Street, Suite 7-500 Technology Chicago, Illinois 60604-1413 20 N. Wacker Drive, Suite 2850 Phone: 312.263.0456 or 800.621.7440 Chicago, IL 60606-3182 Fax: 312.263.7462 Phone: 312.704.5300 http://www.ncahlc.org Fax: 312.704.5304 http://www.jrcert.org Programmatic Accreditation Agencies accrediting specific program offerings at Southern Respiratory Care Technology West Virginia Community and Technical College include: Commission on Accreditation for Respiratory Care 1248 Harwood Road Medical Laboratory Technology Bedford, TX 76021-4244 National Accrediting Agency for Clinical Laboratory Sciences Phone: 817.283.2835 5600 River Road, Suite 720 Fax: 817.354.8519 Rosemont, IL 60018 http://www.coarc.com -

Broadcast Applications 4/2/2019

Federal Communications Commission 445 Twelfth Street SW PUBLIC NOTICE Washington, D.C. 20554 News media information 202 / 418-0500 Recorded listing of releases and texts 202 / 418-2222 REPORT NO. 29456 Broadcast Applications 4/2/2019 STATE FILE NUMBER E/P CALL LETTERS APPLICANT AND LOCATION N A T U R E O F A P P L I C A T I O N AM STATION APPLICATIONS FOR ASSIGNMENT OF LICENSE ACCEPTED FOR FILING KY BAL-20190327ABN WPKE 18225 EAST KENTUCKY Voluntary Assignment of License BROADCASTING CORPORATION E 1240 KHZ From: EAST KENTUCKY BROADCASTING CORPORATION KY , PIKEVILLE To: MOUNTAIN TOP MEDIA LLC Form 314 KY BAL-20190327ABQ WEKB 32972 EAST KENTUCKY Voluntary Assignment of License BROADCASTING CORPORATION E 1460 KHZ From: EAST KENTUCKY BROADCASTING CORPORATION KY , ELKHORN CITY To: MOUNTAIN TOP MEDIA LLC Form 314 KY BAL-20190327ABR WLSI 38388 EAST KENTUCKY Voluntary Assignment of License BROADCASTING CORPORATION E 900 KHZ From: EAST KENTUCKY BROADCASTING CORPORATION KY , PIKEVILLE To: MOUNTAIN TOP MEDIA LLC Form 314 WV BAL-20190327ABW WBTH 26392 EAST KENTUCKY RADIO Voluntary Assignment of License NETWORK, INC. E 1400 KHZ From: EAST KENTUCKY RADIO NETWORK, INC. WV , WILLIAMSON To: MOUNTAIN TOP MEDIA LLC Form 314 KY BAL-20190327ABY WPRT 18548 EAST KENTUCKY RADIO Voluntary Assignment of License NETWORK, INC. E 960 KHZ From: EAST KENTUCKY RADIO NETWORK, INC. KY , PRESTONSBURG To: MOUNTAIN TOP MEDIA LLC Form 314 Page 1 of 14 Federal Communications Commission 445 Twelfth Street SW PUBLIC NOTICE Washington, D.C. 20554 News media information 202 / 418-0500 Recorded listing of releases and texts 202 / 418-2222 REPORT NO. -

Press Television and Radio Postal

Section 7:Section 7 6/21/13 2:19 PM Page 523 Section Seven ✩ PRESS News Organizations and Newspapers ✩ TELEVISION AND RADIO ✩ POSTAL ✩ Section 7:Section 7 6/21/13 2:19 PM Page 524 THE PRESS WEST VIRGINIA PRESS ASSOCIATION 3422 Pennsylvania Avenue, Charleston 25302 Phone: 1-800-235-6881 Website: www.wvpress.org Board of Directors: Nanya Friend, President, Charleston; Pam Pritt, Marlinton; David Corcoran, Glenville; Perry Nardo, Wheeling; Butch Antolini, Beckley; James Heishman, Moorefield; Matthew Yeager, Summersville; Ed Dawson, Huntington; David Hedges, Spencer; Jim Spanner, Parkersburg; Jim McGoldrick, St. Marys; Sandra Buzzerd, Berkeley Springs; Alan Waters, Morgantown; Darryl Hudson, Bluefield. Executive Director: Gloria Flowers. ________ WEST VIRGINIA BROADCASTERS ASSOCIATION 149 Seventh Avenue, South Charleston 25303 Phone: (304)744-2143 Website: www.wvba.com Board of Directors: Frank Brady, President, Bluefield; Bob Spencer, Pineville; Roger Spencer, Park- ersburg; Mike Buxser, Charleston; Don Ray, Huntington; Dale Miller, Morgantown; Tim DeFazio, Clarksburg; Mike Kirtner, Huntington; Larry Bevins, Logan; Jay Phillppone, Weirton; Jeri Math- eney, Charleston. Executive Director: Michele Crist. ________ DAILY NEWSPAPERS Beckley: The Register-Herald Bluefield: Bluefield Daily Telegraph Charleston: Gazette-Mail (Saturday and Sunday) Charleston Daily Mail (Monday through Friday) The Charleston Gazette (Monday through Friday) Clarksburg: The Exponent-Telegram (Monday through Saturday) Elkins: The Inter-Mountain (Monday through Saturday)