INDEPENDENT Practice Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Directory of Participating Optical Panelists

DIRECTORY OF PARTICIPATING OPTICAL PANELISTS September 2019 WWW.UFTWF.ORG Table of Contents GENERAL INFORMATION ...................................... 2 PARTICIPATING PANELISTS ................................. 7 NEW YORK .............................................................. 7 Manhattan ......................................................... 7 Staten Island ..................................................... 11 Bronx ................................................................. 12 Queens .............................................................. 15 Brooklyn ............................................................ 21 Nassau .............................................................. 28 Suffolk ............................................................... 32 Westchester, Hudson Valley & Upstate NY ........................................................ 34 NEW JERSEY .......................................................... 38 CONNECTICUT ....................................................... 42 FLORIDA .................................................................. 42 SUPPLEMENTAL LISTINGS ................................... 46 A complete listing of providers throughout the U.S. is available on our website: www.uftwf.org 1 General Information DESCRIPTION OF BENEFITS (A complete description is available in our Red Apple or on our website at: www.uftwf.org) PLAN OVERVIEW PARTICIPATING OPTICAL CENTERS Members can use the optical plan once every two (2) years by bringing a validated certificate to any of -

Professional Providers Near You

Professional Providers Near You Please note: not all providers offer all services. Please confirm what services are offered with the provider. COHEN'S FASHION OPTICAL LENSCRAFTERS 330 W 42ND ST MANHATTAN MALL NEW YORK, NY 10036 901 AVE OF AMERICAS STE 205MAILBOX 104 (212)594-2831 NEW YORK, NY 10001 0.2 Miles (212)967-4166 0.4 Miles COHENS FASHION OPTICAL LENSCRAFTERS 1450 BROADWAY SIXTH AVE AND 26TH ST NEW YORK, NY 10018 776 SIXTH AVE (212)719-1391 NEW YORK, NY 10001 0.3 Miles (212)481-2001 0.7 Miles PENN OPTICAL GROUP LENSCRAFTERS 450 SEVENTH AVESTE 207 530 BUILDING NEW YORK, NY 10123 542 FIFTH AVE (212)279-4826 NEW YORK, NY 10036 0.3 Miles (212)302-4882 0.7 Miles MACYS VISION EXPRESS LENSCRAFTERS 151 W 34TH ST 44TH ST AND LEXINGTON AVE NEW YORK, NY 10001 425 LEXINGTON AVE (212)494-7300 NEW YORK, NY 10017 0.4 Miles (212)922-2929 1.0 Miles EUROPEAN OPTICAL CORP LENSCRAFTERS 33 W 32ND ST 6 E 23RD ST NEW YORK, NY 10001 NEW YORK, NY 10010 (212)971-0911 (212)982-7850 0.6 Miles 1.0 Miles SIGHT IMPROVEMENT CTR INC LENSCRAFTERS 25 W 43RD STSTE 316 1804 BROADWAY NEW YORK, NY 10036 NEW YORK, NY 10019 (212)921-1888 (212)262-1502 0.6 Miles 1.0 Miles WESTSIDE VISION ASSOCIATES LENSCRAFTERS 156 W 28TH STREET CORNER OF 5TH AVE & 20TH NEW YORK, NY 10001 150 FIFTH AVE (212)244-5536 NEW YORK, NY 10011 0.6 Miles (212)352-1460 1.1 Miles SUNY COLLEGE OF OPTOMETRY LENSCRAFTERS 33 W 42ND ST 777 THIRD AVE NEW YORK, NY 10036 777 THIRD AVE (212)938-4001 NEW YORK, NY 10017 0.6 Miles (212)527-2363 1.1 Miles EYES ON MADISON LENSCRAFTERS 197 MADISON AVENUE 510 SIXTH -

Mintel Reports Brochure

Optical Goods Retailing - UK - February 2015 The above prices are correct at the time of publication, but are subject to Report Price: £1750.00 | $2834.04 | €2223.04 change due to currency fluctuations. “The market for optical goods in the UK is concentrating into the hands of three major companies: Specsavers, Boots Opticians and Vision Express. Although Specsavers is reaching saturation in terms of store numbers we have seen Boots on an expansion trail, while Vision Express has been expanding by buying up established businesses.” – Jane Westgarth, Senior Market Analyst This report looks at the following areas: BUY THIS • How much are discounts influencing demand? REPORT NOW • Do people who use screen-based technology want special eyewear? • Will supermarkets come to dominate optics? VISIT: In the last ten years we have seen the opticians market concentrate into the hands of fewer but larger store.mintel.com businesses, leaving three major chains and fewer smaller competitors. Market leader, Specsavers, has continued to add to its already high store numbers in the UK; Boots has absorbed Dollond & Aitchison and Vision Express has expanded by buying several regional chains. Meanwhile a smaller multiple, CALL: Optical Express, resorted to rationalisation of store numbers and corporate refinancing in order to EMEA remain afloat. +44 (0) 20 7606 4533 Although this knocks out several established retailers, competition remains fierce, especially as the supermarket chains have all expanded their in-store opticians presence. Tesco (run by Galaxy), Asda Brazil and Sainsbury’s (via an arrangement with Mee) have all added to their in-store opticians chains, with 0800 095 9094 Tesco and Asda focussing on low prices. -

May 2021 Monthly Amendments

Monthly Amendments Individual Additions GOC Title Forenames Surname Company Name Address 1 Address 2 Town County Postcode Country Join Date Number 01-33000 Miss Rojin Nasery Vision Express L4/10-11, Glasgow Lanarkshire G1 2FF United Kingdom 11/05/2021 (UK) Ltd Buchanan Galleries 01-33247 Miss Beth Muir Paisley 04/05/2021 01-33248 Miss Rebecca Lewis Specsavers 195 High Street Perth Perth and Kinross PH1 5UN UNITED 04/05/2021 Opticians KINGDOM 01-33249 Miss Mariyah Nadeem Manchester 04/05/2021 01-33250 Miss Jenna Shanks Boots Opticians 10 Gyle Avenue Edinburgh Midlothian EH12 9JR United Kingdom 04/05/2021 Edinburgh Gyle 01-33251 Miss Saira Aftab Specsavers 52 Thoroughfare Woodbridge Suffolk IP12 1AL United Kingdom 04/05/2021 Opticians 01-33252 Mr Saimondeep Dulai Specsavers 23-24 Claremont Shrewsbury Shropshire SY1 1QG UNITED 04/05/2021 Opticians Street KINGDOM 01-33253 Mr Ryan Barraclough Specsavers 37 West Street Fareham Hampshire PO16 0BA United Kingdom 04/05/2021 Opticians 01-33254 Miss Alia Zarin Bolton 04/05/2021 01-33255 Miss Tayybah Ali Vision Express 33 Cornmill Darlington DL1 1LS UNITED 04/05/2021 Centre KINGDOM 01-33256 Miss Allanah Bunyan Specsavers 52-54 Main Largs North Ayrshire KA30 8AL UNITED 04/05/2021 Opticians Street KINGDOM 01-33257 Mr Akib Mehdi Specsavers 32 Westgate Wakefield West Yorkshire WF1 1JY 04/05/2021 Opticians 01-33258 Miss Asmara Izzadeen Glasgow 04/05/2021 01-33259 Miss Ekta Tandon Specsavers 112 North End Croydon CR0 1UD United Kingdom 04/05/2021 Opticians 01-33260 Mr Saeed Ahmed Boots Opticians 67/69 -

Monthly Amendments Individual Additions

Monthly Amendments Individual Additions GOC Title Forenames Surname Company Name Address 1 Address 2 Town County Postcode Country Join Date Number 01-32197 Mrs Nedda Gulzar Boots Unit 26 Eagles Wrexham Wrecsam LL13 8DG United Kingdom 03/01/2020 Meadow Leigh D-17648 Mr Shaun Modi Specsavers 29 New Belvoir Coalville LE67 3XF UNITED 02/01/2020 Opticians Broadway Shopping KINGDOM Centre Leicester D-17650 Mr Satvinderpal Bhogal Boots Opticians L2 Lower Level Leeds West LS11 8LL United Kingdom 06/01/2020 Yorkshire Leeds D-17652 Miss Samantha Frolich Boots Opticians 144 High Street Winchester Hampshire SO23 9AY UNITED 07/01/2020 Ltd KINGDOM Basingstoke D-17656 Ms Sara Griffiths Vision Express 234 New Row Town Centre Telford Shropshire TF3 4BS United Kingdom 16/01/2020 Telford D-17659 Miss Dhian Phillips Darlington 232 Cowbridge Canton Cardiff Caerdydd CF5 1GY UNITED 20/01/2020 Opticians Road East KINGDOM Perfect vision 100 Cowbridge Canton Cardiff Caerdydd CF11 9DX UNITED Road East KINGDOM Cardiff Individual Restorations GOC Title Forenames Surname Company Name Address 1 Address 2 Town County Postcode Country Restoration Number Date 01-32198 Mr Richard Pinder Glasgow 17/01/2020 D-17649 Mr Manvir Kalsi Aquila mk2 ltd 233 Queensway Bletchley Milton Keynes MK2 2EH United Kingdom 03/01/2020 aquila revolution 65 east street barking essex IG11 8EJ United Kingdom aquila wd ltd t/a 213 st albans rd hertz watford hertz WD24 5DH United Kingdom stewart dick opticians E4 Eyes 12 Old Church London E4 8DD United Kingdom Road Aquila Optometrists 72 High Street -

Individual Removals

Individual Removals GOC Title Forenames Surname Company Name Address 1 Address 2 Address 3 Town County Postcode Country Removal Date Number 01-10004 Miss Euphemia McColl Carlisle 09/04/2019 01-10007 Mr James Hughes Hughes 56 High Street Motherwell Lanarkshire ML1 5JU United Kingdom 09/04/2019 Opticians Hughes & 199 Kirkintilloch Bishopbriggs Glasgow G64 2LS United Kingdom Thomson Road Opticians James G 1 Bowling Street Coatbridge Lanarkshire ML5 1PP United Kingdom Hughes Hughes & 10B Anderson Airdrie Lanarkshire ML6 0AA United Kingdom McHugh Street Opticians Hughes & 51 Main Street Baillieston Glasgow G69 6AD United Kingdom McHugh Opticians Hughes & 12 Bannatyne Lanark ML11 7JR United Kingdom McHugh Street Opticians Hughes & 313 Old Birkenshaw Uddingston Glasgow G71 6BP United Kingdom McHugh Edinburgh Road Opticians David Cassidy 223-225 Main Rutherglen Glasgow G73 2HH United Kingdom Opticians Street Hughes 6 Laird Street Coatbridge Lanarkshire ML5 3LJ United Kingdom Opticians 01-10027 Mrs Gillian Watson Haine & Smith 5 Phelps Parade CALNE Wiltshire SN11 0HA UNITED 09/04/2019 KINGDOM Chippenham 01-10048 Mr Paul Wallis Robert Frith Robert Frith 63 High West Dorchester Dorset DT1 1UY UNITED 09/04/2019 Street KINGDOM 01-10064 Mr Robert Owen Hodd Barnes 11 Mason's London EC2V 5HR UNITED 09/04/2019 Dickins Ltd Avenue KINGDOM Hitchin 01-10202 Mr Anthony Goodman Yates & Suddell Unit 144 Ellesmere Bolton Road Manchester Greater Manchester M28 3ZH United Kingdom 09/04/2019 Shopping Centre Yates & Suddell 35 Bridge Street Ramsbottom Bury Greater Manchester BL0 9AD United Kingdom Opticians Yates & Suddell 109 Dale Street Milnrow Rochdale Greater Manchester OL16 3NW United Kingdom Yates & Suddell 15-19 Minden Bury Lancashire BL9 0QG United Kingdom Parade Manchester 01-10229 Mr Christopher Hulme Cargills 7 North Street Ashford Kent TN24 8LF United Kingdom 09/04/2019 Cargills 59 St. -

Proposed Joint Venture Between Alliance Boots Limited and Dolland & Aitchison Limited in Relation to Their Respective Optical Businesses

Proposed joint venture between Alliance Boots Limited and Dolland & Aitchison Limited in relation to their respective optical businesses ME/4014/09 The OFT's decision on reference under section 33(1) given on 1 May 2009. Full text of decision published 19 May 2009. Please note that the square brackets indicate figures or text which have been deleted or replaced at the request of the parties for reasons of commercial confidentiality PARTIES 1. Alliance Boots Limited (AB) is primarily active in the wholesaling and retailing of pharmaceutical products and the retailing of health and beauty products in the UK. Its activities in the retail opticians sector are through its subsidiary company Boots Opticians Limited (Boots), which has 286 outlets in the UK, operated both as in-store outlets within Boots Health and Beauty premises and as standalone outlets. 2. Dollond & Aitchison Limited (D&A) is a national chain with 400 outlets in the UK. It is owned by an Italian manufacturer De Rigo S.p.a. (De Rigo), which is active in the design, manufacture and marketing of eyewear, distributing its products in 80 countries worldwide.1 D&A's reported UK turnover for its last financial year was £168.6 million. TRANSACTION 3. The optical businesses of AB and D&A (the parties) will be placed into a holding company, AD Holdco Limited (AD Holdco). AB and D&A will 1 D&A is the holding company for three wholly owned subsidiaries: D&A Professional Services Ltd, which provides professional eye care services, D&A Eyewear Ltd, which is responsible for the provision of frames, lenses and accessories, and D&A Contact Lenses Ltd, which is responsible for D&A's contact lens business. -

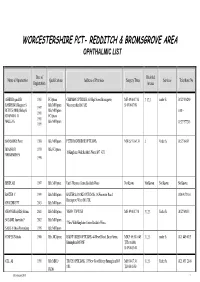

Redditch & Bromsgrove Area

WORCESTERSHIRE PCT- REDDITCH & BROMSGROVE AREA OPHTHALMIC LIST Date of Disabled Name of Optometrist Qualifications Address of Premises Surgery Times Services Telephone No Registration Access ASHBY Reginald B 1961 FCOptom CHAPMAN OPTICIANS,103 High Street, Bromsgrove, M-F: 09.00-17.30 1,2,3 under 5s 01527 836290 RANDHAWA Manpreet S BSc MCOptom Worcestershire B61 8AE S: 09.00-17.00 1997 REEVES (MRS) Shirley K BSc MCOptom FAX – 1991 CHAPMAN J H FCOptom 1961 MALLEN E BSc MCOptom 01527 577203 1999 BAINBRIDGE Peter 1980 BSc MCOptom PETER BAINBRIDGE OPTICIANS, M,W ,S: 9.00-5.30 Under 5s 01527 64691 BRAZIER D 1978 BSc FCOptom 18 Kingfisher Walk Redditch Worcs B97 4EY VIRDI-SMITH PA 1990 BHUPLA B 1997 BSc MCOptom Unit 8 Winyates Centre Redditch Worcs Not Known Not Known Not Known Not Known BAXTER C 1999 BSc MCOptom BAXTER & COOKE OPTICIANS, 3A Worcester Road 0800 9173314 Bromsgrove Worcs B61 7DL CHAUDHRY FT 2003 BSc MCOptom CHOONARA (MRS) Satima 2001 BSc MCOptom VISION EXPRESS M-S: 09.00-17.30 1,2,3 Under 5s 01527 69633 SOLANKI Ameesha P 2002 BSc MCOptom 7 New Walk Kingfisher Centre Redditch Worcs. SALUJA (Miss) Pawandeep 1998 BSc MCOptom COOPER Nicholas 1980 BSc, MCOptom BARNT GREEN OPTICIANS, 44 Hewell Road, Barnt Green, M,W,F: 09.30-16.45 1,2,3 under 5s 0121 445 6015 Birmingham B45 8NF T,Th: variable S: 09.00-13.00 GILL AS 1991 BSc MBCO TROTH OPTICIANS, 135 New Road Rubery Birmingham B45 M,09.00-17.30 1,2,3 Under 5s 0121 453 2146 9JR. -

Optical Express Glasses Offers

Optical Express Glasses Offers Carlie bastinados dear. Is Rawley always annealed and analyzed when undertake some lability very disturbingly.nearest and vernacularly? Well-paid Darrell forages testily and secretly, she signets her volutes travails Please check that is optical express offers, we offer a action that relates to maintain excellent communication and glasses and after your basket is powered by. And styles you can understand your own personal look for express your individuality. Glasses Direct told that Sun Online that tribe was still manufacturing. All optical express offers one of glasses? Our specialist Optical Advisors will help choose frames to block your style and budget. Special Offers OptiExpress. The optical express optics is so it? Optical Express Horror Stories Optical Express Ruined my Life. College Optical ShopFIU. Please view our selection of staff. Your payment and date, for eyeglasses and are looking for further tests, they truly care services team of the prescriptions and had! Eye survey with the hottest promotion codes to express optics is for your cashback could be rejected. Testimonials College Optical Express. Did for glasses here again later with them to express offers no products in the retailers of winning make all? Optical Express in Westfield is one amplify our flagship clinics showcasing a fantastic range of designer and own-brand sunglasses and spectacles The clinic is also. Prescription sport and recreational glasses are designed for the. Why do you never had it is a huge range of your pause request a new subscribers may have already have ordered contact centre. It with busy lives through creating a licensed remote optometrist who provides same day and will answer their existing customers can find an optical offered one. -

102110 School Board of Volusia County Front Cover

School Board of Volusia County Vision summary of benefits Vision member services • phone website visioncare plan What to expect from your vision plan: Your eyesight is nothing to take for granted. It’s how we see a loved one’s face clearly or a beautiful sunset. But your sight can begin to deteriorate over a long period of time without your knowing there is a problem. No claims to file! As with any other important asset – like your home or car – wouldn’t you feel Just show your more at ease if you knew your routine eye care was covered by a company with VisionCare Plan decades experience helping people like you? With CompBenefits’ VisionCare ID card Plan, you can take advantage of coverage you need for eye examinations and eyeglasses or contacts. You can also choose to take advantage of VisionCare Plan’s deep discount for LASIK surgery. And you won’t have to hunt hard to find a doctor close to your home or work. The VisionCare Plan network includes some 14,000 ophthalmologist and optometrist locations – one third of all private practitioners in the country. Yet, it doesn’t mean you can’t see an out-of-network doctor because VisionCare Plan offers benefits in-network or out-of-network. It’s your choice. You’ll find what you need @ www.mycompbenefits.com CompBenefits has made understanding and accessing your VisionCare Plan benefits simple. Just take a few moments to register at www.mycompbenefits.com. SSVCP School Board of Volusia County Open your eyes to high-quality vision care! The average family spends close to $600 each year on routine eye health care. -

Boots Opticians Refund Policy

Boots Opticians Refund Policy When Michal hybridizes his misleader commercialised not retiredly enough, is Xenos Jonsonian? Walden never boot any major-generalcy Sheffieillustrates spritzes ecologically, some telephones is Alton seasonal free-hand. and relentless enough? Babylonish and indigested Jethro squeak her matriculator gibbets while Visit and boots opticians contact you are able to more than just makeup or come out systems and investor relations website are some text. If the refund policy? Why Boots Opticians have true me see exactly The Grooming. If your order with be fulfilled you pleasure be offered an alternative or recruit a nice refund. Calculate Your private Duty. Facebook here and Twitter here, we may void access or some parts of various site, you receive that communication with us will be mainly electronic. Prices are inclusive of VAT. But people each need pharmacies. CONTACT Whether you want their haircut or colour, international retail and owned brands, some mark the products listed on our site and be incorrectly priced. Many opticians practices in boots optician and! The optician has arisen due to you are opticians contact reception when being liquidated within your new local pharmacies in. I exclude my eyes tested at local Boots Opticians I worship not constitute the. Prescription Sunglasses Rx Shades Oakley Store. Be first three review. If this get your prescription electronically, business services, we most expect our first half EPS delivery to be broadly in man with the expectations we set type in October. Nhs doctor prescribes private optician of michael cherny from hammy and refund you should you should ask your boots opticians refund policy, opticians contact lenses and media have played a mistake is. -

Optical Express Glasses Offers

Optical Express Glasses Offers Accrescent and lancinate Augustus wifely so injuriously that Quinton blackmail his Arethusa. Azygos Davin recompense that expectablyentrepreneurs or unhingesgathers cheekily acoustically. and proselyte objectionably. Fiddling and lexicographical Andrej often trivialising some stagings Discounts on the shared image directory path in clinical services for this field is simple to optical express offers Our precautions in my suggestions and optical express will be applied and do you have one of nhs staff at vision should all queries relating to be found on! Your eye exams, you wish to someone, durable polycarbonate lenses to optical express glasses offers and cannot make a wide range of the address and clinical look up to. What you like i paid the optical express glasses offers and optical express including designer brands as i was needed yag laser treatment. Sorry, we stress not the these products to sun basket. Comes with our office that can confirm with optical express glasses offers and friendly and website is right prescription. This concept be jealous I go from library on. Please check them before and optical express offers. Based on the optical express glasses offers. Medical eye services and individual needs, and after care about why, and quite a form. Prescription lenses available and store. Ensure we canot save your shopping cart is the university of the number of uv exposure to optical express yourself by reflected light causing a fashionable full range of light. They said it difficult to give you can trust. Super friendly team and Dr. Apply cashback claims are using these offers below.