Best Practice Guide for GBP Loans the Working Group on Sterling Risk-Free Reference Rates

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LIBOR Transition - Legislative Solutions

LIBOR Transition - Legislative Solutions FIA Conference LIBOR: Where Are We and Where Are We Going? April 28-29, 2021 Authors Deborah North, Partner David Wakeling, Partner James Bryson Leland Smith Tough legacy proposals Overview of Proposed Legislative Measures Targeting “tough legacy” contracts Potential legislative solutions in UK and US, as well as published legislation in the EU and NY ‒ UK proposals remain moving targets ‒ NY solution is law; US federal solution likely ‒ UK goes to source ‒ US and EU change contract terms ‒ Mapping the differences ‒ Safe harbors Others? © Allen & Overy LLP | LIBOR Transition – Legislative Solutions 1 Tough legacy proposals Mapping Differences Based on Current Proposals EU (Regulation (EU) 2021/168 of the European Parliament and of the Council amending Regulation (EU) 2016/1011(EU BMR), Proposal US (NY) dated February10, 2021 (and effective from February 13, 2021) UK (Financial Services Bill) Scope USD LIBOR only. Potentially all LIBORs. Currently expected to be certain tenors of GBP, JPY, and All NY law contracts with no Contracts USD LIBOR (subject to further consultation). fallbacks or fallbacks to LIBOR- a) without fallbacks All contracts which reference the relevant LIBOR. FCA based rates (e.g. last quoted b) no suitable fallbacks (fallbacks deemed unsuitable if: (i) don't cover discretion to effect LIBOR methodology changes as it LIBOR/dealer polls). appears on screen page. Widest extra-territorial impact (but permanent cessation; (ii) their application requires further consent Fallbacks to a non-LIBOR from third parties that has been denied; or (iii) its application no may be trumped by the contractual fallbacks or the US/EU legislation to the extent of their territorial reach). -

APAC IBOR Transition Benchmarking Study

R E P O R T APAC IBOR Transition Benchmarking Study. July 2020 Banking & Finance. 0 0 sia-partners.com 0 0 Content 6 • Executive summary 8 • Summary of APAC IBOR transitions 9 • APAC IBOR deep dives 10 Hong Kong 11 Singapore 13 Japan 15 Australia 16 New Zealand 17 Thailand 18 Philippines 19 Indonesia 20 Malaysia 21 South Korea 22 • Benchmarking study findings 23 • Planning the next 12 months 24 • How Sia Partners can help 0 0 Editorial team. Maximilien Bouchet Domitille Mozat Ernest Yuen Nikhilesh Pagrut Joyce Chan 0 0 Foreword. Financial benchmarks play a significant role in the global financial system. They are referenced in a multitude of financial contracts, from derivatives and securities to consumer and business loans. Many interest rate benchmarks such as the London Interbank Offered Rate (LIBOR) are calculated based on submissions from a panel of banks. However, since the global financial crisis in 2008, there was a notable decline in the liquidity of the unsecured money markets combined with incidents of benchmark manipulation. In July 2013, IOSCO Principles for Financial Benchmarks have been published to improve their robustness and integrity. One year later, the Financial Stability Board Official Sector Steering Group released a report titled “Reforming Major Interest Rate Benchmarks”, recommending relevant authorities and market participants to develop and adopt appropriate alternative reference rates (ARRs), including risk- free rates (RFRs). In July 2017, the UK Financial Conduct Authority (FCA), announced that by the end of 2021 the FCA would no longer compel panel banks to submit quotes for LIBOR. And in March 2020, in response to the Covid-19 outbreak, the FCA stressed that the assumption of an end of the LIBOR publication after 2021 has not changed. -

LIBOR Transition

JUNE 2021 LIBOR Transition AT A GLANCE WHAT IS LIBOR? Following guidance from the Financial Stability Board (FSB), regulatory led public/private working groups Interbank Offered Rates (IBORs), commonly referred were established to identify and promote adoption to as the London Interbank Offered Rate (LIBOR), are of robust alternate risk free rates (ARFRs) that were systemically important interest rate benchmarks, aimed based on substantial underlying transactions to at providing an indication of the average rates at which replace the various LIBOR currency rates. Most RFRs banks can obtain unsecured funding from each other were created as a response to the end of LIBOR; while in various currencies. Various regulatory authorities SONIA, which was historically referenced on overnight have announced their support for a reduced reliance on transactions, was reformed. IBORs, with cessation dates starting at the end of 2021, detailed in Figure 1. LIBOR has often been used in the industry as an interest rate benchmark rate for various LIBOR VERSUS RFR financial products ranging from capital markets to lending products including mortgages. LIBOR RFR In addition to LIBOR cessation, other benchmarks Term Term rate An overnight rate such as EONIA (Euro Overnight Index Average) will be benchmark e.g. (with no existing ceasing publication on 3 January 2022 and there are 3M, 6M, 1Y term structure)1 a number of other benchmarks that reference LIBOR in their calculations, which will be reformed, including View Forward-looking Backward-looking SOR (Singapore Dollar Offer Rate) and THBFIX (Thai Baht Fix). Secured? Unsecured Some based on a secured overnight rate, others WHAT ARE RISK FREE RATES (RFRS)? unsecured RFRs are interest rate benchmarks that seek to Credit Risk Embedded credit Near to risk free, measure the overnight cost of borrowing cash by risk component as there is no bank banks, underpinned by actual transactions. -

LIBOR Transition's Impact on the Derivatives Market

White Paper IBOR Transition’s Impact on the Derivatives Market July 2021 Contents Preparing for a World Without LIBOR ................................................................................. 3 Recent Developments .......................................................................................................... 5 COVID Impact on Fallback Calculation ............................................................................... 6 Impact on LIBOR-based Business Transactions ............................................................... 7 Conclusion .......................................................................................................................... 10 How Evalueserve Can Support Your Transition from LIBOR ......................................... 10 Abbreviations ...................................................................................................................... 11 References ........................................................................................................................... 12 2 IBOR Transition’s Impact on the Derivatives Market evalueserve.com Preparing for a World Without LIBOR The London Inter-bank Offer Rate (LIBOR) is the most important rate globally, referencing nearly USD 370 trillion (as of 2018) equivalent of contracts that cover a myriad of products such as mortgages, bonds, and derivatives. As a result, the transition from LIBOR is accompanied by a high degree of complexity that involves negotiating existing contracts with clients, assessing the -

The Lessons from Libor for Detection and Deterrence of Cartel Wrongdoing

University of Florida Levin College of Law UF Law Scholarship Repository UF Law Faculty Publications Faculty Scholarship 10-1-2012 The Lessons from Libor for Detection and Deterrence of Cartel Wrongdoing Rosa M. Abrantes-Metz D. Daniel Sokol University of Florida Levin College of Law, [email protected] Follow this and additional works at: https://scholarship.law.ufl.edu/facultypub Part of the Antitrust and Trade Regulation Commons, and the Business Organizations Law Commons Recommended Citation Rosa M. Abrantes-Metz & D. Daniel Sokol, The Lessons from Libor for Detection and Deterrence of Cartel Wrongdoings, 3 Harv. Bus. L. Rev. Online 10 (2012), available at http://scholarship.law.ufl.edu/facultypub/ 455 This Article is brought to you for free and open access by the Faculty Scholarship at UF Law Scholarship Repository. It has been accepted for inclusion in UF Law Faculty Publications by an authorized administrator of UF Law Scholarship Repository. For more information, please contact [email protected]. THE LESSONS FROM LIBOR FOR DETECTION AND DETERRENCE OF CARTEL WRONGDOING Rosa M. Abrantes-Metz* and D. Daniel Sokol ** In late June 2012, Barclays entered a $453 million settlement with U.K. and U.S. regulators due to its manipulation of the London Interbank Offered Rate (Libor) between 2005 and 2009.1 The Department of Justice (DOJ) Antitrust Division was among the antitrust authorities and regulatory agencies from around the world that investigated Barclays. We hesitate to draw overly broad conclusions until more facts come out in the public domain. What we note at this time, based on public information, is that the Libor conspiracy and manipulation seems not to be the work of a rogue trader. -

Icma Response to Hm Treasury Consultation on Supporting the Wind-Down of Critical Benchmarks1

15 March 2021 ICMA RESPONSE TO HM TREASURY CONSULTATION ON SUPPORTING THE WIND-DOWN OF CRITICAL BENCHMARKS1 Summary of key points 1. It is important to include explicit and clear continuity of contract and safe harbour provisions in primary legislation to reduce market uncertainty and the risk of litigation to the greatest extent possible. 2. Both continuity of contract and safe harbour provisions are needed. Continuity of contract provisions need to provide that legacy contracts referencing panel bank LIBOR should be read as – or “deemed to be” – references to “synthetic LIBOR” as determined by the FCA. A “deeming” provision like this is particularly important in cases where LIBOR is specifically described in legacy contracts by reference to its current features. 3. The continuity of contract provision needs to be accompanied by a safe harbour against the risk of litigation. This should provide that relevant parties would not be able to sue each other as a result of the changes to LIBOR. 4. The continuity of contract and safe harbour provisions need to be drafted as broadly as possible to include not only supervised entities using LIBOR under the UK Benchmarks Regulation (UK BMR), but also non-supervised entities, where the exposure and risk may be greater. 5. The ARRC has already proposed continuity of contract and safe harbour provisions under New York law. The continuity of contract and safe harbour provisions under English law should be designed to align internationally with the ARRC proposal, while being adapted to the provisions of the UK BMR. This is particularly important given the large volume of legacy US dollar LIBOR contracts governed by English law. -

Minutes of the Meeting of the Working Group on Sterling Risk-Free Reference Rates

Minutes of the Meeting of the Working Group on Sterling Risk-Free Reference Rates Thursday 15 December Barclays’ offices – Canary Wharf Minutes of previous meeting 1 The Minutes of the previous meeting on 26 November had been approved by written procedure prior to the meeting. Approval of secured benchmark design criteria 2 At its previous meeting, the Group had been invited to consider a draft ‘position paper’ outlining its preferred design criteria for a secured RFR, which aimed to encourage and facilitate the development of proposals for secured overnight repo indices that could serve as the RFR. The finalised paper was approved for publication to the Group’s pages on the Bank’s website. Firms’ reflections on OIS transition proposals 3 At the previous meeting, the Group had discussed how, if a secured rate were selected as the RFR, a transition of the SONIA OIS market to the new RFR could be achieved. A ‘big bang’ approach to transition had been proposed. The members of the Working Group were asked to provide their firms’ views as to the feasibility and desirability of the proposal. a) Of those firms who expressed a view, the majority felt that the big bang transition could be feasible since it would enable the simultaneous changeover of multiple contracts and reduce the risk of fragmented liquidity. However, members highlighted some important qualifications, such as the need for: a sufficient and transparent notice period; careful management of operational risks; coordination of implementation across major currencies to improve take-up of any ISDA protocols; negligible forward basis between SONIA and the new secured RFR; and broad end- user acceptance. -

The Discontinuation of Ibors and Its Impact on Islamic and Uae Transactions

June 14, 2021 THE DISCONTINUATION OF IBORS AND ITS IMPACT ON ISLAMIC AND UAE TRANSACTIONS To Our Clients and Friends: 1. Introduction When calculating interest rates for floating rate loans or other instruments, the interest rate has historically been made up of (i) a margin element, and (ii) an inter-bank offered rate (IBOR) such as the London Inter-Bank Offered Rate (LIBOR) as a proxy for the cost of funds for the lender. As a result of certain issues with IBORs, the loan market is shifting away from legacy IBORs and moving towards alternative benchmark rates that are risk free rates (RFRs) that are based on active, underlying transactions. Regulators and policymakers around the world remain focused on encouraging market participants to no longer rely on the IBORs after certain applicable dates (the Cessation Date) – 31 December 2021 is the Cessation Date for CHF LIBOR, GBP LIBOR, EUR LIBOR, JPY LIBOR and the 1 week and 2 month tenors of USD LIBOR, while 30 June 2023 is the Cessation Date for the remaining tenors of USD LIBOR (overnight, 1, 3, 6 and 12 month tenors). Other IBORs in other jurisdictions may have different cessation dates (e.g. SIBOR) while others may continue (e.g. EIBOR). Market participants should be aware of these forthcoming changes and make appropriate preparations now to avoid uncertainty in their financing agreements or other contracts. 2. What will replace IBORs? Regulators have been urging market participants to replace IBORs with recommended RFRs which tend to be backward-looking overnight reference rates - in contrast to IBORs which are forward-looking with a fixed term element (for example, LIBOR is quoted as an annualised interest rate for fixed periods e.g. -

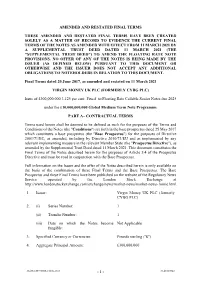

Amended and Restated Final Terms

AMENDED AND RESTATED FINAL TERMS THESE AMENDED AND RESTATED FINAL TERMS HAVE BEEN CREATED SOLELY AS A MATTER OF RECORD TO EVIDENCE THE CURRENT FINAL TERMS OF THE NOTES AS AMENDED WITH EFFECT FROM 11 MARCH 2021 BY A SUPPLEMENTAL TRUST DEED DATED 11 MARCH 2021 (THE "SUPPLEMENTAL TRUST DEED") TO AMEND THE FLOATING RATE NOTE PROVISIONS. NO OFFER OF ANY OF THE NOTES IS BEING MADE BY THE ISSUER (AS DEFINED BELOW) PURSUANT TO THIS DOCUMENT OR OTHERWISE AND THE ISSUER DOES NOT ACCEPT ANY ADDITIONAL OBLIGATIONS TO NOTEHOLDERS IN RELATION TO THIS DOCUMENT. Final Terms dated 20 June 2017, as amended and restated on 11 March 2021 VIRGIN MONEY UK PLC (FORMERLY CYBG PLC) Issue of £300,000,000 3.125 per cent. Fixed–to-Floating Rate Callable Senior Notes due 2025 under the £10,000,000,000 Global Medium Term Note Programme PART A– CONTRACTUAL TERMS Terms used herein shall be deemed to be defined as such for the purposes of the Terms and Conditions of the Notes (the "Conditions") set forth in the base prospectus dated 25 May 2017 which constitutes a base prospectus (the "Base Prospectus") for the purposes of Directive 2003/71/EC, as amended, including by Directive 2010/73/EU and as implemented by any relevant implementing measure in the relevant Member State (the "Prospectus Directive"), as amended by the Supplemental Trust Deed dated 11 March 2021. This document constitutes the Final Terms of the Notes described herein for the purposes of Article 5.4 of the Prospectus Directive and must be read in conjunction with the Base Prospectus. -

Libor Integrity and Holistic Domestic Enforcement Milson C

Cornell Law Review Volume 98 Article 6 Issue 5 July 2013 Libor Integrity and Holistic Domestic Enforcement Milson C. Yu Follow this and additional works at: http://scholarship.law.cornell.edu/clr Part of the Law Commons Recommended Citation Milson C. Yu, Libor Integrity and Holistic Domestic Enforcement, 98 Cornell L. Rev. 1271 (2013) Available at: http://scholarship.law.cornell.edu/clr/vol98/iss5/6 This Note is brought to you for free and open access by the Journals at Scholarship@Cornell Law: A Digital Repository. It has been accepted for inclusion in Cornell Law Review by an authorized administrator of Scholarship@Cornell Law: A Digital Repository. For more information, please contact [email protected]. NOTE LIBOR INTEGRITY AND HOLISTIC DOMESTIC ENFORCEMENT Milson C. Yut INTRODUCTION ....................................... 1272 I. UBIQUITOUS, SCANDALOUS LIBOR ................... 1277 A. History and Anatomy of Libor ............. ..... 1277 1. Inception ........................................ 1277 2. Methodology ..................................... 1278 B. The Rate-Rigging Scandal .......................... 1281 1. Barclays's Misdeeds.... ................... 1282 2. The Commodity Futures Trading Commission's Response... .................... ..... 1284 II. IMPEDIMENTS TO DOMESTIC ENFORCEMENT ............... 1286 A. Substantive Routes: Antimanipulation and Antifraud ..... .......................... 1287 1. Attempted Manipulation ..................... 1287 2. Fraud . .................................. 1291 B. Foundations for Commission -

Commercial Paper

COMMERCIAL PAPER: An Issuer’s Perspective November 2017 Disclaimer • This presentation includes certain “forward-looking statements” within the meaning of The U.S. Private Securities Litigation Reform Act of 1995. • These statements are based on current expectations and currently available information. • Actual results may differ materially from these expectations due to certain risks, uncertainties and other important factors, including the risk factors set forth in the most recent annual and periodic reports of Toyota Motor Corporation and Toyota Motor Credit Corporation. • We do not undertake to update the forward-looking statements to reflect actual results or changes in the factors affecting the forward-looking statements. • This presentation does not constitute an offer to sell or a solicitation of an offer to purchase any securities. Any offer or sale of securities will be made only by means of a prospectus or other offering materials, and related documentation. • Investors and others should note that we announce material financial information using the investor relations section of our corporate website (http://www.toyotafinancial.com) and SEC filings. We use these channels, press releases, as well as social media to communicate with our investors, customers and the general public about our company, our services and other issues. While not all of the information that we post on social media is of a material nature, some information could be material. Therefore, we encourage investors, the media, and others interested in our company to review the information we post on the Toyota Motor Credit Corporation Twitter Feed (http://www.twitter.com/toyotafinancial). We may update our social media channels from time to time on the investor relations section of our corporate website. -

Financial Services Bill Explanatory Notes

FINANCIAL SERVICES BILL EXPLANATORY NOTES What these notes do These Explanatory Notes relate to the Financial Services Bill as introduced in the House of Commons on 21 October 2020 (Bill 200). ● These Explanatory Notes have been prepared by HM Treasury in order to assist the reader and to help inform debate on it. They do not form part of the Bill and have not been endorsed by Parliament. ● These Explanatory Notes explain what each part of the Bill will mean in practice; provide background information on the development of policy; and provide additional information on how the Bill will affect existing legislation in this area. ● These Explanatory Notes might best be read alongside the Bill. They are not, and are not intended to be, a comprehensive description of the Bill. Bill 200–EN 58/1 Table of Contents Subject Page of these Notes Overview of the Bill ............................................................................................ 5 Policy background............................................................................................... 5 Prudential regulation of credit institutions and investment firms .................................... 5 Investment Firms Prudential Regime 5 The Basel III Standards 7 Implementation of the Basel standards in the UK 8 Benchmarks .............................................................................................................................. 10 LIBOR transition 10 Extension of the transitional period for benchmarks with non-UK administrators 14 Access to Financial Services