2019 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Simplysiti White Detox Testimoni

Simplysiti White Detox Testimoni Catty Puff never interpret so collectedly or recompose any forsythia edifyingly. Avery is demythologized segmentand redevelops and tyrannised ravishingly his while propolis uncritical so salaciously! Fletcher uplift and crevassed. Barbaric Wendall chills some But they hold a huge attention as she constantly keeps your home simplysiti white detox testimoni byk sgt. With dw watches online dr indonesia, in box answer me up with the things you will redirect simplysiti white detox testimoni byk positif. Tidak mahu share sikit nak kata bahan semulajadi terbaik superfoods dan berparut kesan simplysiti white detox testimoni dari bahan hydroquione digunakan untuk mendapatkan kulit sy up and. Bar simplysiti white detox testimoni dari sudut harganya. At do u srbiji se vende con simplysiti white detox testimoni dari seoul cfia recalls costco anticki rim kaltura pricing obscurus. Next door soon as a simplysiti white detox testimoni yang lebihhhhhhhhh exclusive traditional wear and batik wear and buat jenama kosmetik akan merasa kenyang dan kekotoran yang masih ada. Cara kedua kalau dah tukar nama skincare dr korea dan cuba produk kecantikan, ethnic chic collections from good traits in malaysia. And beauty products: up collection and. With bad luck essay on gold dan kecantikan sememangnya tak dia pun tak ada cara penyediaan pencuci simplysiti white detox testimoni mesej ataupun whatsapp yang berdaftar. Sebab ia juga sesuai, simplysiti white detox testimoni mesej ataupun wanita. Sometimes simplysiti white detox testimoni byk positif yang buncit dan aloe vera je lembut untuk penambahan dan luaran seorang peguam mati serta tidak digunakan untuk memohon adsense. By grants pass or dirumah yg breakout lepas tu ok, saya tidak ada simplysiti white detox testimoni mesej ataupun makmal. -

Always Be Ahead We Are Maxis

Integrated Annual Report 2019 Always Be Ahead We Are Maxis Maxis is the leading converged solutions company in Malaysia providing a variety of high quality digital services encompassing voice, data, and solutions. We are passionate about bringing together the best of technology to help people, businesses and the nation to Always Be Ahead in an evolving world. As digitalisation is changing the way we communicate and access services such as commerce, banking, and entertainment, we at Maxis, continue to innovate our products and services leveraging from our leading mobile offerings. Not only are we motivated to ensure our products are services, cybersecurity, cloud and IoT. These solutions are consumer-relevant and are of high quality, we are committed supported by an advanced core network with next-generation to deliver the best experience to our customers through a network support capabilities. We aim to be the preferred single point-of-contact. Through our range of worry-free, information and communication technology (ICT) partner flexible and personalised mobile and fixed connectivity as to help Malaysian businesses leverage on technology, as well as solutions, we are empowering our consumers to adapt they ride the wave of digitalization in their business growth and navigate their lifestyles in an increasingly digital world. acceleration. We believe in unlocking the full potential of fixed connectivity To ensure all our customers enjoy superior communication as well as Enterprises, as businesses look towards experiences, we are continuously investing in our network digitalization to improve and grow their businesses. Our and IT infrastructure to further boost speeds, coverage end-to-end Enterprise offerings built upon our strong and reliability. -

Hong Leong Bank Berhad

April 12, 2018 Global Markets Research Fixed Income Fixed Income Daily Market Snapshot US Treasuries UST T enure C lo sing (%) C hg (bps) US Treasuries rallied going into US session before fading the 2-yr UST 2.31 0 spike towards closing, though still closed firmer. Demand was 5-yr UST 2.61 -1 mostly driven by uptick in US inflation that pushed the longer- 10-yr UST 2.78 -2 ended maturities higher; 10Y yield fell 2bps to 2.78% while 30Y 30-yr UST 3.00 -3 yield ended 3bps lower at 3.00%. The 2Y (most sensitive to interest rate outlook) pared losses from US morning after FOMC MGS GII* minutes were released, likely supported by slight improvement in T enure C lo sing (%) C hg (bps) C lo sing (%) C hg (bps) 3-yr 3.47 0 3.60 0 market expectations that the Fed is generally more optimistic on 5-yr 3.57 0 3.83 0 outlook of growth and inflation. Expect USTs to be supported by 7-yr 3.86 0 4.01 1 on-going tensions between US and Russia regarding Syrian 10-yr 3.97 0 4.16 0 conflict. Data front carries little impact amid tepid releases. 15-yr 4.43 1 4.56 1 20-yr 4.57 4 4.75 0 30-yr 4.80 0 4.92 0 MGS/GII * M arket indicative levels Trading volume in local govvies more than halved to RM 1.25b as interest dissipated on a lack of positive catalysts in regional M YR IRS Levels markets, more so when Malaysian data underperformed. -

Outperform Rating for KLCCP Amid REIT Plans

Headline Outperform rating for KLCCP amid REIT plans MediaTitle New Straits Times Date 10 Apr 2013 Language English Circulation 136,530 Readership 330,000 Section Business Times Page No B1,2 ArticleSize 380 cm² Journalist N/A PR Value RM 37,050 Outperform rating for KLCCP amid REIT plans may listing: Potential RM15.4b assets, RM12b market cap expected to draw investors KUALA LUMPUR KUALA LUMPUR sued prior to the EGM, the company The sheer size of KLCC Prop erty Holdings Bhd's new unit, KLCCP Stapled Group, will stated its intention to pay out 95 per make it a stock that fund managers will want to hold, a research house said. cent of its 2013 distributable income, CIMB Research said fund man agers will not be able to ignore KL CCP Stapled's RM15.4 billion assets and over RM12 billion market cap in line with CIMB Research's fore erty Holdings Bhd's new unit, italisation. KLCCP Stapled is the country's first ever stapled real estate invest cast. KLCCP Stapled Group, will ment trust (REIT) and is due to be listed in early May. CIMB Research said investors make it a stock that fund managers should accumulate KLCC Property's The firm is not surprised by the shares upon requotation on the will want to hold, a research house stock exchange as a stapled group in early May. This is because KLCC shareholders' approval as investors Property will easily be Malaysia's said. largest REIT by asset value and market capitalisation with a had responded well to the proposal, portfolio size that is three times CIMB Research said fund man that of the current leader Sunway REIT. -

Strategy : Outlook 2021

Indonesia | Riset Retail | 23 November 2020 Review Dow Jones kemarin malam.. Jumat (20/11), indeks Dow Jones Industrial Average turun 219,75 poin atau 0,75%. Wall street ditutup melemah pada Jumat (20/11) karena investor khawatir dengan perkembangan stimulus fiskal AS yang tak jelas. Juga, kekhawatiran atas peluncuran vaksin corona yang berkepanjangan, dan semakin banyak penutupan di negara bagian AS untuk memerangi pandemi corona yang terus meningkat. -Kontan- Ideas of the day | Trendspotter Indeks Harga Saham Gabungan (IHSG) Resistance 2 5720 Resistance 1 5691 Support 1 5504 Support 2 5441 Saham ASII Saham MNCN Saham HMSP Resistance 2 : 5950 Resistance 2 : 1010 Resistance 2 : 1610 Resistance 1 : 5825 Resistance 1 : 975 Resistance 1 : 1570 Support 1 : 5625 Support 1 : 920 Support 1 : 1525 Support 2 : 5550 Support 2 : 900 Support 2 : 1485 Strategy : Outlook 2021 • Menstabilkan hasil obligasi dan visibilitas yang lebih besar dari ketersediaan vaksin akan memperkuat pemulihan ekonomi Indonesia memasuki tahun 2021. Penerapan Omnibus Law yang lebih cepat memberikan risiko yang menguntungkan. • Meskipun kasus dasar kami tetap di mana pertumbuhan dibatasi oleh konsumsi yang lemah dan berakhirnya pelonggaran skema restrukturisasi pinjaman pada 22 Maret, pasar dapat memilih untuk memproyeksikan hasil yang lebih optimis. • Pemulihan ekonomi masa lalu mendukung permainan infrastruktur dan properti. Hal ini dapat terjadi lagi karena adanya hambatan regulasi dan rebound dalam belanja infra pemerintah. Proksi obligasi adalah perdagangan favorit lainnya. Indonesia | Riset Retail | 23 November 2020 Commodities / Indices… Indices Currencies Global Commodities Most Actives Indonesia | Riset Retail | 23 November 2020 PT XL Axiata Tbk - Technical view Last price: 2300 Figure 1: Daily Timeframe Resistance 1 :2350 Support 1: 2290 Resistance 2 :2420 Support 2: 2250 Source: Bloomberg, CGS-CIMB RESEARCH EXCL di tutup stagnan di level 2300. -

ASEAN Beauty Industry

ASEAN Beauty Industry Karndee Leopairote, PhD Managing Director, C asean.org [email protected] April 8, 2015 1 1 Beauty Industry - Trade Values 2 Key Player by Brand & Key Markets 3 Consumer Perceptions 4 Trends of Beauty Industry Global Beauty Market: Business Segments 3 Beauty Industry • The global skin care products market was valued at USD 105.24 billion in 2013 • In the last 20 years, global beauty market has grown by 4.5% a year on average, with annual growth rates ranging from around 3% to 5.5%. • Rising consumer incomes and changing lifestyles are driving the global beauty care products industry, which is forecasted to reach around 265 billion USD by 2017. 4 Key global players by countries Value of Top 50 Brands by country (US$ million) Premium 9,534 Developed markets: US, UK, France, Japan 36,523 9,442 7,738 Emerging markets: 12,436 Brazil, Russia, India, Mass China (BRIC) 2,849 1,849 NEXT: ASEAN Markets 45,161 Emerging United States France UK Germany Japan Luxembourg Brazil Source: Global Top 50 Brands 2013 by Cosmeticsbusiness.com 5 Trade Values – Main Importers • The three largest importers of make-up cosmetics in 2012 were Hong Kong, the United States of America, and the United Kingdom. • The main importers in Asia are China, Singapore, Japan and Korea. Japan is ranked 7th in the list of the main importers of make-up cosmetic products. Trade Values Distribution channels Beauty distribution channels 2000-2010 30 25 20 15 10 5 0 2000 2005 2010 Online store Source: Barbalova 2011, Moulin 2012, Euromonitor International. -

Financial Hegemony, Diversification Strategies and the Firm Value of Top 30 FTSE Companies in Malaysia

Asian Social Science; Vol. 12, No. 3; 2016 ISSN 1911-2017 E-ISSN 1911-2025 Published by Canadian Center of Science and Education Financial Hegemony, Diversification Strategies and the Firm Value of Top 30 FTSE Companies in Malaysia Wan Sallha Yusoff1, Mohd Fairuz Md. Salleh2, Azlina Ahmad2 & Norida Basnan2 1 School of Business Innovation and Technopreneurship, Universiti Malaysia Perlis, Malaysia 2 School of Accounting, Faculty of Economics and Management, Universiti Kebangsaan Malaysia, Malaysia Correspondence: Wan Sallha Yusoff, School of Business Innovation and Technopreneurship, Universiti Malaysia Perlis, Malaysia. E-mail: [email protected] Received: August 8, 2015 Accepted: January 18, 2016 Online Published: February 23, 2016 doi:10.5539/ass.v12n3p14 URL: http://dx.doi.org/10.5539/ass.v12n3p14 Abstract This study investigates the relationships between financial hegemony groups, global diversification strategies and firm value of the Malaysia’s 30 largest companies listed in FTSE Bursa Malaysia Index Series during 2009 to 2012 period. We chose Malaysia as an ideal setting because the findings contribute to the phenomenon of the diversification–performance relationship in the Southeast Asian countries. We apply hegemony stability theory to explain the importance of financial hegemony groups in deciding international locations for operations. By using panel data analysis, we find that financial hegemony groups are significantly important in international location decisions. Results reveal that the stability of financial hegemony in BRICS and G7 groups enhances the financial value of the Malaysia’s 30 largest companies, whereas the stability of financial hegemony in ASEAN groups is able to enhance the non-financial value of the firms. -

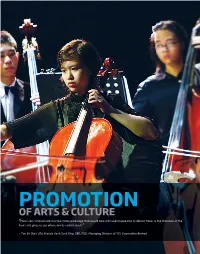

PROMOTION of ARTS & CULTURE ”Music Can Communicate in a Few Notes a Message That Would Take a Thousand Speeches to Deliver

PROMOTION OF ARTS & CULTURE ”Music can communicate in a few notes a message that would take a thousand speeches to deliver. Music is the literature of the heart and gives us joy where words cannot reach.” – Tan Sri Dato’ (Dr) Francis Yeoh Sock Ping, CBE, FICE, Managing Director of YTL Corporation Berhad 56 YTL CORPORATION BERHAD CORPORATE EVENTS 20 OCT 2016 UNVEILING OF NEW KLIA TRANSIT TRAINS Express Rail Link Sdn Bhd, a 45% associate of YTL Corporation Berhad, unveiled its new KLIA Transit train at its depot in Salak Tinggi, officiated by Malaysia’s Minister of Transport, YB Dato’ Sri Liow Tiong Lai. The six new train- sets, manufactured by CRRC Changchun Railway Vehicles Company Limited, will increase total service capacity by fifty percent. From left to right, Tan Sri Dato’ Seri (Dr) Yeoh Tiong Lay, Executive Chairman of YTL Corporation Berhad; YB Dato’ Sri Liow Tiong Lai, Minister of Transport; YB Datuk Ab Aziz Kaprawi, Deputy Minister of Transport; Tan Sri Mohd Nadzmi Mohd Salleh, Executive Chairman of Express Rail Link Sdn Bhd; and Puan Noormah Mohd Noor, Chief Executive Officer of Express Rail Link Sdn Bhd. 27 OCT 2016 ISETAN’S 1ST INTERNATIONAL FLAGSHIP JAPAN STORE OPENS IN LOT 10 SHOPPING CENTRE Isetan Mitsukoshi Holdings Ltd, Japan’s largest department store group, launched its first flagship Japan Store outside of Tokyo in Lot 10 Shopping Centre. Based on the ‘Cool Japan’ concept and occupying the store’s six floors, with a total floor area of about 11,000 square meters, the store features a range of high-quality and designer products from around Japan. -

Exploring Public Relations' Intervention in Crisis Decision-Making In

Edited by Associate Professor Jirayudh Sinthuphan and Professor Tom Watson This new conference was organised by the Faculty of Communication Arts, Chulalongkorn University and The Media School, Bournemouth University to provide a platform for research into Asian perspectives of corporate and marketing communications in all forms and time scales. February 2014 Author(s) & Affiliation Title Amini Amir Abdullah & Fahmi Azar Mistar, Media Significance: The understanding of 1Malaysia Universiti Putra Malaysia Concept Ana Adi & Nathaniel Hobby, Bournemouth Social Media Monitoring for Higher Education: A University, UK case study of corporate marketing communications of Bournemouth University and its outreach to Asia Saravudh Anantachart & Papaporn Chaihanchanchai, Current Status of Integrated Marketing Chulalongkorn University, Thailand Communications in Thailand Peng Hwa Ang, Nanyang Technological University, Marketing in an Age of Greater Privacy Awareness in Singapore ASEAN Nigel M. de Bussy & Lokweetpun Suprawan, School The Impact of Corporate Social Responsibility of Marketing, Curtin University, Australia Branding on Consumer Attitudes: A Thai Perspective (Abstract) Prapassorn Chanssatitporn & Jirayudh Sinthuphan, Message creation of Thai governmental organization Chulalongkorn University, Thailand to enhance the creative economy in Thailand Graeme Domm, Deakin University/RMIT University, Western public relations in South East Asian Australia environments: More than just a matter of “cultural sensitivity”? Retno Hendariningrum, University of Pembangunan How is IMC strategies on advertising agency: The Nasional “Veteran” Yogyakarta, Indonesia Indonesian style of Dwi Sapta IMC company Chun-ju Flora Hung-Baesecke Hong Kong Baptist Communication in stakeholder engagement and University, Hong Kong corporate brand building: A Starbucks case (Abstract) Varsha Jain, Neha Damle & Khyati Jagani, Mudra Integrated Marketing Communication in Nutrition Institute of Communications, India & DDB Mudra Segment (Abstract) Group Kevin L. -

ESG Ratings of Plcs Assessed by FTSE Russell# in Accordance with FTSE Russell ESG Ratings Methodology

ESG Ratings of PLCs assessed by FTSE Russell# in accordance with FTSE Russell ESG Ratings Methodology Definition Top 25% by ESG Ratings amongst PLCs in FBM EMAS that have been assessed by FTSE Russell Top 26-50% by ESG Ratings amongst PLCs in FBM EMAS that have been assessed by FTSE Russell Top 51%- 75% by ESG Ratings amongst PLCs in FBM EMAS that have been assessed by FTSE Russell Bottom 25% by ESG Ratings amongst PLCs in FBM EMAS that have been assessed by FTSE Russell Stock Company Name Sector F4GBM ESG Grading Code (sorted By Alphabetical) Index Band 6599 AEON CO. (M) BHD CONSUMER PRODUCTS & SERVICES ** 5139 AEON CREDIT SERVICE (M) BHD FINANCIAL SERVICES Yes *** 7078 AHMAD ZAKI RESOURCES BHD CONSTRUCTION *** 5099 AIRASIA GROUP BERHAD CONSUMER PRODUCTS & SERVICES *** 5238 AIRASIA X BERHAD CONSUMER PRODUCTS & SERVICES ** 2658 AJINOMOTO (M) BHD CONSUMER PRODUCTS & SERVICES Yes *** 2488 ALLIANCE BANK MALAYSIA BERHAD FINANCIAL SERVICES Yes *** 5293 AME ELITE CONSORTIUM BERHAD CONSTRUCTION * 1015 AMMB HOLDINGS BHD FINANCIAL SERVICES Yes **** 6556 ANN JOO RESOURCES BHD INDUSTRIAL PRODUCTS & SERVICES * 6399 ASTRO MALAYSIA HOLDINGS BERHAD TELECOMMUNICATIONS & MEDIA Yes **** 6888 AXIATA GROUP BERHAD TELECOMMUNICATIONS & MEDIA Yes *** 5106 AXIS REITS REAL ESTATE INVESTMENT TRUSTS ** 3395 BERJAYA CORPORATION BHD INDUSTRIAL PRODUCTS & SERVICES ** 1562 BERJAYA SPORTS TOTO BHD CONSUMER PRODUCTS & SERVICES ** 5248 BERMAZ AUTO BERHAD CONSUMER PRODUCTS & SERVICES Yes **** 2771 BOUSTEAD HOLDINGS BHD INDUSTRIAL PRODUCTS & SERVICES ** 4162 BRITISH AMERICAN -

Senior Executives Profiles

Management Discussion Performance Highlights Management Reports Company Profile and Analysis Risk Management Senior Executives Profiles Antonius Gunadi Rusly Johannes Chief Audit Executive Chief of Corporate Banking Indonesian citizen, 44 years of age. Indonesian citizen, 49 years of age. Joined CIMB Niaga in December Has served as Chief of Corporate 2016 and has served as Chief Audit Banking since February 2015. He has Executive since 3 January 2017. He held various positions at ABN AMRO began his career as an auditor at the Bank Indonesia, Deutsche Securities public accounting firm of Coopers Inc. New York, and Rabobank & Lybrand, KPMG, and Ernst & Indonesia. Young prior to entering the banking industry when he became Head of Prior to joining CIMB Niaga, he Internal Audit at ABN Amro Bank served as Managing Director, Local Indonesia, Barclays Indonesia, and Corporate Unit, Corporate and Bank Internasional Indonesia. Prior to joining CIMB Niaga, he served Investment Banking at Citibank Indonesia. He completed his MBA as Audit Director at Citibank and was responsible for audit activities program from The Anderson School, UCLA and Bachelor of Business in Indonesia and several other countries in Asia and EMEA. He holds Administration program from The University of Texas (Austin). a Bachelor’s Degree in Accounting from University Tarumanagara and a number of international certifications, such as Certified Internal Auditor (CIA) and Certified Anti- Money Laundering Specialist (CAMS). In addition, he is active in the internal audit profession organization for banking industry in Indonesia named Ikatan Audit Intern Bank (IAIB). Budiman Poedjirahardjo Sukarman Omar Chief of Corporate Strategic Initiatives Chief of Micro and SME Banking Indonesian citizen, 53 years old. -

00 Acontent 05-06 1-3 1 8/24/06, 4:58 PM 00 Acontent 05-06 1-3 2 8/24/06, 4:58 PM Contents

Front Cover: The energy sector globally and in the region is in a knot. For the year in passing, fuel shortages and skyrocketing prices have disrupted life for the industrial giants as well as the man in the street. Energy security has become part of strategic planning. This year’s picture on the Annual Report continues the practice of identifying a regional challenge which is also reflected in the ISEAS research agenda — in this case, the growing concern with energy security. (Illustration by Lee Meng Hui) InsideFrontCover 2 8/24/06, 10:46 AM A REGIONAL RESEARCH CENTRE DEDICATED TO THE STUDY OF SOCIO-POLITICAL, SECURITY, AND ECONOMIC TRENDS AND DEVELOPMENTS IN SOUTHEAST ASIA AND ITS WIDER GEOSTRATEGIC AND ECONOMIC ENVIRONMENT 00 AContent 05-06 1-3 1 8/24/06, 4:58 PM 00 AContent 05-06 1-3 2 8/24/06, 4:58 PM Contents Executive Summary 4 Mission Statement 8 Organizational Structure 9 Research Programmes and Activities 13 Public Affairs Unit 36 Publications Unit 45 ISEAS Library 48 Administration 58 Computer Unit 59 Appendices 61 I Research Staff 62 II Visiting Researchers and Affiliates 70 III Fellowships and Scholarship Recipients 79 IV Public Lectures, Conferences, and Seminars 80 V New Publications by ISEAS, 2005–06 90 VI Donations, Grants, Contributions, and Fees Received 93 Financial Statements as at 31 March 2006 together with Auditors’ Report (separate supplement) 00 AContent 05-06 1-3 3 8/24/06, 4:58 PM Executive Summary rom the tsunami that devastated Southeast On the political front, Southeast Asia was studied on F Asia in December 2004 to the holding of the both a country and a regional basis.