Administrative, Procedural and Miscellaneous SIMPLE IRA Plan Guidance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

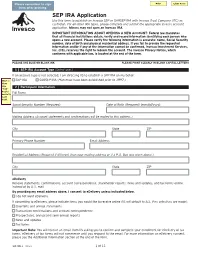

SEP IRA Application Use This Form to Establish an Invesco SEP Or SARSEP IRA with Invesco Trust Company (ITC) As Custodian

SEP IRA Application Use this form to establish an Invesco SEP or SARSEP IRA with Invesco Trust Company (ITC) as custodian. For all other IRA types, please complete and submit the appropriate Invesco account application. Minors may not open an Invesco IRA. IMPORTANT INFORMATION ABOUT OPENING A NEW ACCOUNT: Federal law mandates that all financial institutions obtain, verify and record information identifying each person who opens a new account. Please verify the following information is accurate: name, Social Security number, date of birth and physical residential address. If you fail to provide the requested information and/or if any of the information cannot be confirmed, Invesco Investment Services, Inc. (IIS), reserves the right to redeem the account. The Invesco Privacy Notice, which conforms with applicable law, is located at the end of the form. PLEASE USE BLUE OR BLACK INK PLEASE PRINT CLEARLY IN BLOCK CAPITAL LETTERS 1 | SEP IRA Account Type (Select one.) If an account type is not selected, I am directing IIS to establish a SEP IRA on my behalf. n SEP IRA n SARSEP IRA (Plan must have been established prior to 1997.) 2 | Participant Information Full Name Social Security Number (Required) Date of Birth (Required) (mm/dd/yyyy) Mailing Address (Account statements and confirmations will be mailed to this address.) City State ZIP Primary Phone Number Email Address Residential Address (Required if different than your mailing address or if a P.O. Box was given above.) City State ZIP eDelivery Receive statements, confirmations, account correspondence, shareholder reports, news and updates, and tax forms online instead of by U.S. -

Public Employee Deferred Compensation

Public Employee Deferred Compensation ILLINOIS PUBLIC PENSION FUND ASSOCIATION PUBLIC SAFETY FINANCIAL AND INVESTMENT TRAINING (IPPFA PS-FIT) NOTE: This Section is excerpted from Retirement Income for Illinois Fire and Police: Pensions, Social Security and Deferred Compensation, by Daniel W. Ryan. All rights reserved. Used with permission by the IPPFA. Chapter 1: Deferred Compensation— Introduction and Participation WHAT IS DEFERRED COMPENSATION? When a person receives wages (i.e., compensation), income taxes are withheld and the total earned is reported to the IRS at the end of the year. However, sections of the Internal Revenue Code and Illinois law allow an employee to defer receipt of some wages until after he or she retires. At the time these deferred wages are earned, they are neither received in the paycheck, subjected to tax withholding, nor reported as taxable to the IRS. They are instead deposited into an account and invested as directed by the employee. When the accumulated money is ultimately received after retirement, the withdrawal payments are then reported to the IRS as taxable distributions. This deferral of wages and taxes until after retirement is commonly referred to as deferred compensation or “deferred comp.” For most public employees, deferred compensation under IRC code Section 457 is the strongest part of the “personal savings” leg of the three-legged retirement income stool (pension, Social Security, and personal savings). Your personal savings can of course include the value of your home, brokerage 1 accounts, individual retirement accounts, investment real estate, and bank savings. But the ability to save through the paycheck on a tax-advantaged basis has made deferred compensation a large personal asset for most public employees. -

Deferred Compensation Plan of the Port of Oakland

DEFERRED COMPENSATION PLAN OF THE PORT OF OAKLAND Independent Auditor’s Report, Management’s Discussion and Analysis, and Basic Financial Statements Years Ended June 30, 2016 and 2015 DEFERRED COMPENSATION PLAN OF THE PORT OF OAKLAND Years Ended June 30, 2016 and 2015 Table of Contents Page Independent Auditor’s Report ................................................................................................................... 1 Required Supplementary Information: Management’s Discussion and Analysis ............................................................................................... 3 Basic Financial Statements: Statements of Net Position Due to Participants .................................................................................... 5 Statements of Changes in Net Position Due to Participants .................................................................... 6 Notes to the Basic Financial Statements ..................................................................................................... 7 Century City Los Angeles Newport Beach Oakland Sacramento San Diego Independent Auditor’s Report San Francisco Walnut Creek Deferred Compensation Advisory Committee Woodland Hills and Board of Port Commissioners of the City of Oakland Oakland, California Report on the Financial Statements We have audited the accompanying statements of net position due to participants of the Deferred Compensation Plan of the Port of Oakland (Plan) as of June 30, 2016 and 2015, and the related statements of changes in net position -

Alliancebernstein SEP IRA Employee Brochure

AllianceBernstein SEP IRA Employee Brochure n Overview n SEP IRA Application n SEP IRA Rollover/Transfer Form Investment Products Offered • Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed An Employee’s Guide to SEP IRA Programs The Simplified Employee Pension (SEP) IRA is one of the most popular savings plans for businesses or the self-employed. It allows your employer to make tax-deferred contributions toward your retirement. A SEP IRA is a type of Individual Retirement Distributions Account (IRA) that’s funded by your employer. It Your SEP IRA ordinarily maintains its tax-deferred allows you to design a portfolio with the help of status until you take a distribution. Distributions a financial advisor and change your investment are subject to income taxes and must commence selections without incurring a tax penalty. by April 1 of the year following the year you reach age 70½. Distributions taken before the age of 59½ Eligibility are subject to a 10% penalty in addition to federal If you’re at least 21 years old and you’ve worked income taxes. However, there are some exceptions for your employer at any time during three of the to the 10% penalty, including your permanent past five years (including part-time), you’re eligible. disability or death. Please consult your tax or Your employer may, however, exclude nonresident financial advisor for details. aliens, employees whose retirement benefits are the subject of collective bargaining and employees whose compensation for the year is less than $550 (as indexed for inflation in 2012). Getting Started Read the completed Form 5305-SEP Contribution Amounts from your employer and other Your employer may make discretionary contributions accompanying information based on a percentage of your compensation. -

Recent Change to the Stable Value Fund Plan Materials

Deferred Compensation Program KEYSTONE NEWS RECENT CHANGE TO THE STABLE WINTER 2017 VALUE FUND NEWSLETTER IN THIS ISSUE On January 2, 2018, a change took place with one of the investment options in the Pennsylvania State Employees’ Retirement System’s 457 Deferred Compensation Plan. Specifically, Invesco Advisors assumed oversight responsibility for the Stable Recent change to the Stable Value Fund. The Board of the Deferred Compensation Plan made this change as Value Fund part of its ongoing effort to provide participants with a diverse and competitive array of quality investment options. Plan materials get new look The overall investment objectives and strategy of the Stable Value Fund are The power of 1%: How saving staying the same. Invesco is currently negotiating competitive fees with the fund’s pennies can add up to more insurance providers and fixed income managers. If you invest in the Stable Value retirement income Fund, this change will not affect your account balance. Following the change, investors may see a different price per unit/share, with a corresponding change in Financial wellness the number of shares. Contribution limits in 2018 No action on your part is required. For more information about this change, refer to the letter included with your statement for additional details about the Stable Value Yearly financial checklist Fund. You can also visit www.sers457.com. If you have questions, please call 866-SERS457 (866-737-7457). PLAN MATERIALS GET NEW LOOK You may have noticed that the communications you receive from the 457 plan feature an updated look and feel and a new tagline: A new perspective on retirement. -

Publication 560, Retirement Plans for Small Business

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 8 Draft Ok to Print AH XSL/XML Fileid: … tions/P560/2020/A/XML/Cycle07/source (Init. & Date) _______ Page 1 of 31 16:18 - 1-Mar-2021 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing. Publication 560 Cat. No. 46574N Contents What's New .................. 1 Department of the Retirement Reminders ................... 2 Treasury Internal Introduction .................. 2 Revenue Plans Service Chapter 1. Definitions You Need for Small To Know ................. 4 Chapter 2. Simplified Employee Pensions (SEPs) ............ 5 Business Setting Up a SEP ............. 6 How Much Can I Contribute? ...... 6 Deducting Contributions ......... 7 (SEP, SIMPLE, and Salary Reduction Simplified Employee Pensions Qualified Plans) (SARSEPs) .............. 7 Distributions (Withdrawals) ....... 8 Additional Taxes ............. 8 Reporting and Disclosure For use in preparing Requirements ............. 8 Chapter 3. SIMPLE Plans ......... 8 2020 Returns SIMPLE IRA Plan ............. 9 SIMPLE 401(k) Plan .......... 11 Chapter 4. Qualified Plans ........ 11 Kinds of Plans ............. 12 Qualification Rules ........... 12 Setting Up a Qualified Plan ...... 14 Minimum Funding Requirement ... 14 Contributions .............. 14 Employer Deduction .......... 15 Elective Deferrals (401(k) Plans) ... 16 Qualified Roth Contribution Program ............... 18 Distributions ............... 18 Prohibited Transactions ........ 20 Reporting Requirements ....... 21 Chapter 5. Coronavirus - Related Distributions .............. 22 Qualified Individual ........... 22 Special Tax Treatment ......... 22 Repayment of Distributions and Tax Reporting Requirements ... 22 Chapter 6. Table and Worksheets for the Self-Employed ........ 24 Chapter 7. How To Get Tax Help .... 27 Index ..................... 30 Future Developments For the latest information about developments related to Pub. 560, such as legislation enacted after it was published, go to IRS.gov/Pub560. -

457 Deferred Compensation Plan and Trust

457 Governmental Deferred Compensation Plan & Trust i DEFERRED COMPENSATION PLAN AND TRUST As Amended and Restated Effective January 1, 2006 Article I. Purpose The Employer hereby establishes and maintains the Employer’s Deferred Compensation Plan and Trust, hereafter referred to as the “Plan.” The Plan consists of the provisions set forth in this document. The primary purpose of this Plan is to provide retirement income and other deferred benefits to the Employees of the Employer and the Employees’ Beneficiaries in accordance with the provisions of Section 457 of the Internal Revenue Code of 1986, as amended (the “Code”). This Plan shall be an agreement solely between the Employer and participating Employees. The Plan and Trust forming a part hereof are established and shall be maintained for the exclusive benefit of Participants and their Beneficiaries. No part of the corpus or income of the Trust shall revert to the Employer or be used for or diverted to purposes other than the exclusive benefit of Participants and their Beneficiaries. Article II. Definitions 2.01 Account. The bookkeeping account maintained for each Participant reflecting the cumulative amount of the Participant’s Deferred Compensation, including any income, gains, losses, or increases or decreases in market value attributable to the Employer’s investment of the Participant’s Deferred Compensation, and further reflecting any distributions to the Participant or the Participant’s Beneficiary and any fees or expenses charged against such Participant’s Deferred Compensation. 2.02 Accounting Date. Each business day that the New York Stock Exchange is open for trading, as provided in Section 6.06 for valuing the Trust’s assets.