Chapter 3 Analysis of Current Situation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

JUBILEE LIFE INSURANCE COMPANY LIMITED List of Physical Shareholders Without CNIC As of September 30, 2019

JUBILEE LIFE INSURANCE COMPANY LIMITED List of Physical Shareholders without CNIC as of September 30, 2019 S. No. Folio No. Security Holder Name CNIC / Passport # Address 1 14 DR. FAZAL M. ABREJO C-41, I.T. OFFICER S COLONY, GARDEN, KARACHI. 2 39 MR. MASOOD AHMED 164/A, F-10/1, STREET # 36, ISLAMABAD. 3 41 MR. MOHD SIDDIQ AHMED C/O AMERICAN PRESIDENT LINES, EBRAHIM BUILDING, WEST WHARF, KARACHI. 4 42 MRS. AISHA AHMED SUITE 406-408,4TH FLOOR, AL-FALAH BUILDING, SHAHRAH-E-QUAID-E-AZAM, LAHORE. 5 48 MR. SULTAN AHMED D-42, BLOCK-IV, KEHKASHAN CLIFTON, KARACHI-75600. 6 91 MST. SARA F. AZFAR SINDH GOVERNOR S HOUSE, KARACHI. 7 99 MR. S. BARKATULLAH 190/1/B, BLOCK-2, P.E.C.H.S., KARACHI. 8 105 MR. IQBAL BENGALI 71/I, KHAYABAN-E-SHABAZ, PHASE-VI, DEFENCE HOUSING AUTHORITY, KARACHI. 9 117 MR. M. ANWAR CHAUDHARY C/O I.C.I. PAKISTAN LTD., 5, WEST WHARF ROAD, KARACHI. 10 139 SYED VIRASAT ALI DURBARI 74/1-A, LALAZAR, M.T. KHAN ROAD, KARACHI. 11 142 MR. A. HASEEB FAKIH 138/3, KOKAN MUSLIM CO-OPERATIVE HOUSING SOCIETY, NEAR ALAMGIR MOSQUE, ALAMGIR ROAD, KARACHI-74800. 12 147 MR. F.P. FERNANDES 74/1-A, LALAZAR, M.T. KHAN ROAD, KARACHI. 13 153 MRS. SHAHNAZ ARSHED GILANI C-7, STREET NO.2, BATH ISLAND, KARACHI. 14 162 MR. SALAHUDDIN HAIDER 139-E/2, KASHMIR ROAD, KARACHI-75400. 15 164 DR. SHAHID KHURSHID HAK 63/II, 24TH STREET, OFF. KHY-E-BADBAN, PH-5, D.C.H.S., KARACHI. -

Askari Bank Limited List of Shareholders (W/Out Cnic) As of December 31, 2017

ASKARI BANK LIMITED LIST OF SHAREHOLDERS (W/OUT CNIC) AS OF DECEMBER 31, 2017 S. NO. FOLIO NO. NAME OF SHAREHOLDERS ADDRESSES OF THE SHAREHOLDERS NO. OF SHARES 1 9 MR. MOHAMMAD SAEED KHAN 65, SCHOOL ROAD, F-7/4, ISLAMABAD. 336 2 10 MR. SHAHID HAFIZ AZMI 17/1 6TH GIZRI LANE, DEFENCE HOUSING AUTHORITY, PHASE-4, KARACHI. 3280 3 15 MR. SALEEM MIAN 344/7, ROSHAN MANSION, THATHAI COMPOUND, M.A. JINNAH ROAD, KARACHI. 439 4 21 MS. HINA SHEHZAD C/O MUHAMMAD ASIF THE BUREWALA TEXTILE MILLS LTD 1ST FLOOR, DAWOOD CENTRE, M.T. KHAN ROAD, P.O. 10426, KARACHI. 470 5 42 MR. M. RAFIQUE B.R.1/27, 1ST FLOOR, JAFFRY CHOWK, KHARADHAR, KARACHI. 9382 6 49 MR. JAN MOHAMMED H.NO. M.B.6-1728/733, RASHIDABAD, BILDIA TOWN, MAHAJIR CAMP, KARACHI. 557 7 55 MR. RAFIQ UR REHMAN PSIB PRIVATE LIMITED, 17-B, PAK CHAMBERS, WEST WHARF ROAD, KARACHI. 305 8 57 MR. MUHAMMAD SHUAIB AKHUNZADA 262, SHAMI ROAD, PESHAWAR CANTT. 1919 9 64 MR. TAUHEED JAN ROOM NO.435, BLOCK-A, PAK SECRETARIAT, ISLAMABAD. 8530 10 66 MS. NAUREEN FAROOQ KHAN 90, MARGALA ROAD, F-8/2, ISLAMABAD. 5945 11 67 MR. ERSHAD AHMED JAN C/O BANK OF AMERICA, BLUE AREA, ISLAMABAD. 2878 12 68 MR. WASEEM AHMED HOUSE NO.485, STREET NO.17, CHAKLALA SCHEME-III, RAWALPINDI. 5945 13 71 MS. SHAMEEM QUAVI SIDDIQUI 112/1, 13TH STREET, PHASE-VI, DEFENCE HOUSING AUTHORITY, KARACHI-75500. 2695 14 74 MS. YAZDANI BEGUM HOUSE NO.A-75, BLOCK-13, GULSHAN-E-IQBAL, KARACHI. -

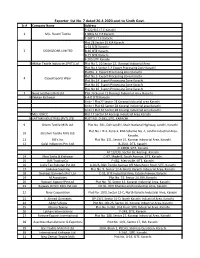

Exporter List No. 7 Dated 20-4-2020 Sent to Sindh Govt. Sr.# Company Name Address F-122/B.S.I.T.E Karachi 1 M/S

Exporter list No. 7 dated 20-4-2020 sent to Sindh Govt. Sr.# Company Name Address F-122/B.S.I.T.E Karachi 1 M/s. Roomi Textile F-98/G S.I.T.E Karachi. F-287 S.I.T.E Karachi. Plot 28 Sector 15 KIA Karachi A-33 SITE Karachi 2 SIDDIQSONS LIMITED B-26 SITE Karachi B-29 SITE Karachi F-205 SITE Karachi 3 Akhtar Textile Industries (PVT) Ltd Plot No 5, 10 Sector 23, Korangi Industrial Area Plot No.1 Sector C-4 Export Processing Zone Karachi PlotNo. 2 Export Processing Zone Karachi Plot No.3 Export Processing Zone Karachi 4 Casual Sports Wear Plot No.14 Export Processing Zone Karachi Plot No.15 Export Processing Zone Karachi Plot No.16 Export Processing Zone Karachi 5 Nova Leathers (Pvt) Ltd Plot 30 Sector 15 Korangi Industrial Area Karachi 6 Pelikan Knitwear F-4-D SITE Karachi Unit=1 Plot27 Sector 28 Korangi Industrial area Karachi Unit=1 Plot 62 Sector 28 Korangi Industrial area Karachi Unit=1 Plot 67 Sector 28 Korangi Industrial area Karachi 7 M/s. GWCC Plot 17 Sector 14 Korangi Industrial Area Karachi 8 SATTAR INDUSTRIES (PVT) LTD PLOT NO. D-281, SITE, KARACHI 9 Orient Textile Mills Ltd. Plot No. 501, Deh Landhi, Main National Highway, Landhi, Karachi. Plot No. HX-2, Zone-2, KDA Scheme No. 4, Landhi Industrial Area, 10 Ebrahim Textile Mills Ltd. Karachi. 11 Bill's Inc. Plot No. 131, Sector 15, Korangi Industrial Area, Karachi. 12 Dalal Industries Pvt. Ltd. B-25/A, SITE, Karachi. -

Karachi Mobility Project Yellow Brt Corridor

Yellow BRT Corridor – Compensation and Livelihood Rehabilitation Plan Public Disclosure Authorized KARACHI MOBILITY PROJECT YELLOW BRT CORRIDOR COMPENSATION AND LIVELIHOOD REHABILIATION PLAN Public Disclosure Authorized Public Disclosure Authorized Final Report May 09, 2019 Public Disclosure Authorized Sindh Mass Transit Authority Yellow BRT Corridor – Compensation and Livelihood Rehabilitation Plan TABLE OF CONTENTS EXECUTIVE SUMMARY .................................................................................................. 6 1 INTRODUCTION ..................................................................................................... 11 1.1 The Compensation and Livelihood Rehabilitations Plan (C&LRP) ....................... 11 1.1.1 Purpose and Scope of the C&LRP ....................................................... 11 1.1.2 Project Policy on C&LRP ...................................................................... 11 1.2 Measures to Minimize Impact ............................................................................. 12 2 PROJECT DESCRIPTION ...................................................................................... 13 2.1 Introduction ......................................................................................................... 13 2.2 Project Development Objectives and Key Results............................................... 13 2.3 Sindh Mass Transit Authority .............................................................................. 13 2.4 Project Components .......................................................................................... -

DC Valuation Table (2018-19)

VALUATION TABLE URBAN WAGHA TOWN Residential 2018-19 Commercial 2018-19 # AREA Constructed Constructed Open Plot Open Plot property per property per Per Marla Per Marla sqft sqft ATTOKI AWAN, Bismillah , Al Raheem 1 Garden , Al Ahmed Garden etc (All 275,000 880 375,000 1,430 Residential) BAGHBANPURA (ALL TOWN / 2 375,000 880 700,000 1,430 SOCITIES) BAGRIAN SYEDAN (ALL TOWN / 3 250,000 880 500,000 1,430 SOCITIES) CHAK RAMPURA (Garision Garden, 4 275,000 880 400,000 1,430 Rehmat Town etc) (All Residential) CHAK DHEERA (ALL TOWN / 5 400,000 880 1,000,000 1,430 SOCIETIES) DAROGHAWALA CHOWK TO RING 6 500,000 880 750,000 1,430 ROAD MEHMOOD BOOTI 7 DAVI PURA (ALL TOWN / SOCITIES) 275,000 880 350,000 1,430 FATEH JANG SINGH WALA (ALL TOWN 8 400,000 880 1,000,000 1,430 / SOCITIES) GOBIND PURA (ALL TOWNS / 9 400,000 880 1,000,000 1,430 SOCIEITIES) HANDU, Al Raheem, Masha Allah, 10 Gulshen Dawood,Al Ahmed Garden (ALL 250,000 880 350,000 1,430 TOWN / SOCITIES) JALLO, Al Hafeez, IBL Homes, Palm 11 250,000 880 500,000 1,430 Villas, Aziz Garden etc KHEERA, Aziz Garden, Canal Forts, Al 12 Hafeez Garden, Palm Villas (ALL TOWN 250,000 880 500,000 1,430 / SOCITIES) KOT DUNI CHAND Al Karim Garden, 13 Malik Nazir G Garden, Ghous Garden 250,000 880 400,000 1,430 (ALL TOWN / SOCITIES) KOTLI GHASI Hanif Park, Garision Garden, Gulshen e Haider, Moeez Town & 14 250,000 880 500,000 1,430 New Bilal Gung H Scheme (ALL TOWN / SOCITIES) LAKHODAIR, Al Wadood Garden (ALL 15 225,000 880 500,000 1,430 TOWN / SOCITIES) LAKHODAIR, Ring Road Par (ALL TOWN 16 75,000 880 200,000 -

Central-Karachi

Central-Karachi 475 476 477 478 479 480 Travelling Stationary Inclass Co- Library Allowance (School Sub Total Furniture S.No District Teshil Union Council School ID School Name Level Gender Material and Curricular Sport Total Budget Laboratory (School Specific (80% Other) 20% supplies Activities Specific Budget) 1 Central Karachi New Karachi Town 1-Kalyana 408130186 GBELS - Elementary Elementary Boys 20,253 4,051 16,202 4,051 4,051 16,202 64,808 16,202 81,010 2 Central Karachi New Karachi Town 4-Ghodhra 408130163 GBLSS - 11-G NEW KARACHI Middle Boys 24,147 4,829 19,318 4,829 4,829 19,318 77,271 19,318 96,589 3 Central Karachi New Karachi Town 4-Ghodhra 408130167 GBLSS - MEHDI Middle Boys 11,758 2,352 9,406 2,352 2,352 9,406 37,625 9,406 47,031 4 Central Karachi New Karachi Town 4-Ghodhra 408130176 GBELS - MATHODIST Elementary Boys 20,492 4,098 12,295 8,197 4,098 16,394 65,576 16,394 81,970 5 Central Karachi New Karachi Town 6-Hakim Ahsan 408130205 GBELS - PIXY DALE 2 Registred as a Seconda Elementary Girls 61,338 12,268 49,070 12,268 12,268 49,070 196,281 49,070 245,351 6 Central Karachi New Karachi Town 9-Khameeso Goth 408130174 GBLSS - KHAMISO GOTH Middle Mixed 6,962 1,392 5,569 1,392 1,392 5,569 22,278 5,569 27,847 7 Central Karachi New Karachi Town 10-Mustafa Colony 408130160 GBLSS - FARZANA Middle Boys 11,678 2,336 9,342 2,336 2,336 9,342 37,369 9,342 46,711 8 Central Karachi New Karachi Town 10-Mustafa Colony 408130166 GBLSS - 5/J Middle Boys 28,064 5,613 16,838 11,226 5,613 22,451 89,804 22,451 112,256 9 Central Karachi New Karachi -

Pdf (Accessed: 3 June, 2014) 17

A University of Sussex DPhil thesis Available online via Sussex Research Online: http://sro.sussex.ac.uk/ This thesis is protected by copyright which belongs to the author. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the Author The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the Author When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given Please visit Sussex Research Online for more information and further details 1 The Production and Reception of gender- based content in Pakistani Television Culture Munira Cheema DPhil Thesis University of Sussex (June 2015) 2 Statement I hereby declare that this thesis has not been submitted, either in the same or in a different form, to this or any other university for a degree. Signature:………………….. 3 Acknowledgements Special thanks to: My supervisors, Dr Kate Lacey and Dr Kate O’Riordan, for their infinite patience as they answered my endless queries in the course of this thesis. Their open-door policy and expert guidance ensured that I always stayed on track. This PhD was funded by the Arts and Humanities Research Council (AHRC), to whom I owe a debt of gratitude. My mother, for providing me with profound counselling, perpetual support and for tirelessly watching over my daughter as I scrambled to meet deadlines. This thesis could not have been completed without her. My husband Nauman, and daughter Zara, who learnt to stay out of the way during my ‘study time’. -

Ending 10 April 2016

World Health Organization – Regional Office for Eastern Mediterranean 1- AFP SURVEILLANCE 11-Apr-16 Week 14, ending 10 April 2016 Number 914 Table 1: Acute Flaccid Paralysis (AFP) cases by week of onset Reported AFP cases by week of onset - Week (14/16) / Ending on : 10/04/2016 Country 2014 2015 2016 to to date, Total Total AFP Total AFP Total AFP W03 Jan 24 16 W04 Jan 31 16 W05 Feb 07 16 W06 Feb 14 16 W07 Feb 21 16 W08 Feb 28 16 W09 Mar 06 16 W10 Mar 13 16 W11 Mar 20 16 W12 Mar 27 16 W13 Apr 03 16 W14 Apr 10 16 Afghanistan 2421 2738 713 71 47 48 67 61 50 44 53 42 47 27 5 Bahrain 16 19 10 0 0 2 1 0 0 0 2 0 1 1 1 Djibouti 3 3 1 0 1 0 0 0 0 0 0 0 0 0 Egypt 1000 1046 289 17 17 19 14 16 29 25 23 29 18 17 7 Iran 753 780 195 14 14 17 16 18 19 13 11 8 5 4 0 Iraq 590 520 197 15 12 22 12 11 15 11 10 16 13 5 Jordan **** 62 90 18 3 0 0 3 1 0 0 2 3 1 2 Kuwait 32 32 12 0 0 0 3 3 1 1 1 2 0 0 0 Lebanon **** 50 113 26 0 2 1 1 4 2 1 3 1 3 2 1 Libya 43 54 13 2 0 1 0 2 1 0 3 1 2 0 Morocco 103 78 15 2 1 2 1 0 2 2 3 0 0 Oman 34 39 12 3 1 1 1 0 1 1 0 0 0 1 0 Pakistan 5370 5811 1268 109 98 92 111 99 102 106 74 83 47 10 0 Palestine **** 21 38 19 1 1 0 4 2 1 3 1 2 0 0 0 Qatar 7 11 2 0 0 0 0 0 0 0 0 0 0 1 1 Saudi Arabia 227 254 51 7 5 6 1 7 8 6 4 1 0 0 0 Somalia 420 281 69 4 6 4 4 6 9 6 8 3 7 3 Sudan 442 436 108 5 9 7 11 10 12 7 7 17 5 2 0 Syria **** 306 235 83 4 6 8 7 7 9 13 7 4 2 3 Tunisia 44 64 20 2 0 3 1 3 2 4 1 0 0 0 U.A.E 25 31 15 2 0 0 1 1 1 3 1 1 1 0 0 Yemen 578 537 190 19 13 22 14 17 10 5 17 10 8 7 1 Total EMR 12547 13210 3326 280 233 255 273 268 274 -

East-Karachi

East-Karachi 475 476 477 478 479 480 Travelling Stationary Inclass Co- Library Allowance (School Sub Total Furniture S.No District Teshil Union Council School ID School Name Level Gender Material and Curricular Sport Total Budget Laboratory (School Specific (80% Other) 20% supplies Activities Specific Budget) 1 East Karachi Jamshed Town 1-Akhtar Colony 408070173 GBLSS - H.M.A. Middle Mixed 7,841 1,568 4,705 3,137 1,568 6,273 25,093 6,273 31,366 2 East Karachi Jamshed Town 2-Manzoor Colony 408070139 GBPS - BILAL MASJID NO.2 Primary Mixed 12,559 2,512 10,047 2,512 2,512 10,047 40,189 10,047 50,236 3 East Karachi Jamshed Town 2-Manzoor Colony 408070174 GBLSS - UNION Middle Mixed 16,613 3,323 13,290 3,323 3,323 13,290 53,161 13,290 66,451 4 East Karachi Jamshed Town 9-Central Jacob Line 408070171 GBLSS - BATOOL GOVT` BOYS`L/SEC SCHOOL Middle Mixed 12,646 2,529 10,117 2,529 2,529 10,117 40,466 10,117 50,583 5 East Karachi Jamshed Town 10-Jamshed Quarters 408070160 GBLSS - AZMAT-I-ISLAM Middle Boys 22,422 4,484 17,937 4,484 4,484 17,937 71,749 17,937 89,687 6 East Karachi Jamshed Town 10-Jamshed Quarters 408070162 GBLSS - RANA ACADEMY Middle Boys 13,431 2,686 8,059 5,372 2,686 10,745 42,980 10,745 53,724 7 East Karachi Jamshed Town 10-Jamshed Quarters 408070163 GBLSS - MAHMOODABAD Middle Boys 20,574 4,115 12,344 8,230 4,115 16,459 65,836 16,459 82,295 8 East Karachi Jamshed Town 11-Garden East 408070172 GBLSS - GULSHAN E FATIMA Middle Mixed 16,665 3,333 13,332 3,333 3,333 13,332 53,327 13,332 66,658 9 East Karachi Gulshan-e-Iqbal Town 3-PIB -

LAHORE HI Ill £1

Government of Pakistan Revenue Division Federal Board of Revenue ***** Islamabad, the 23rd July, 2019. NOTIFICATION (Income Tax) S.R.O. 9^ (I)/2019.- In exercise of the powers conferred by sub-section (4) of section 68 of the Income Tax Ordinance, 2001 (XLIX of 2001) and in supersession of its Notification No. S.R.O. 121(I)/2019 dated the Is' February, 2019, the Federal Board of Revenue is pleased to notify the value of immoveable properties in columns (3) and (4) of the Table below in respect of areas or categories of Lahore specified in column (2) thereof. (2) The value for residential and commercial superstructure shall be — (a) Rs.1500 per square foot if the superstructure is upto five years old; and (b) Rs.1000 per square foot if the superstructure is more than five years old. (3) In order to determine the value of constructed property, the value of open plot shall be added to the value worked out at sub-paragraph (2) above. (4) This notification shall come into force with effect from 24th July, 2019. LAHORE .-r* ALLAMA IQBAL TOWN S. Area Value of Residential Value of No property per maria Commercial (in Rs.) property per maria (in Rs.) HI ill £1 (41 1 ABDALIAN COOP SOCIETY 852,720 1,309,000 2 ABADI MUSALA MOUZA MUSALA 244,200 447,120 3 ABID GARDEN ABADI MUSALA 332,970 804,540 4 ADJOINING CANAL BANK ALL 564,960 1,331,000 SOCIETY MOUZA KANJARAN 5 ADJOINING CANAL BANK ALL 746,900 1,326,380 SOCIETY MOUZA IN SHAHPUR KHANPUR 6 AGRICHES COOP SOCIETY 570,900 1,039,500 7 AHBAB COLONY 392,610262,680 8 AHMAD SCHEME NIAZ BAIG 390,443 800,228 -

PAKISTAN Strives to Make Pakistan a Better Country to Live In

TRANSPARENCY INTERNATIONAL - PAKISTAN Strives to make Pakistan a better country to live in PAKISTAN PRE-PROJECT ASSESSMENT REPORT (DfID Engineering KaR I2-16) ENDING MARCH 31, 2004 PRO POOR PROGRAM “To Improve the Transparency, Quality, and Effectiveness of the delivery of Water Supply and Sewerage to the Citizens of Gulshan Town by the use of ICT’s 65 – C NATIONAL HIGHWAY Phase II Defence Housing Authority Karachi CONTENTS INTRODUCTION............................................................................................N 1 1. Background......................................................................................... 1 2. Project Justification .............................................................................. 1 3. Objectives........................................................................................... 2 4. The Bottom up Approach....................................................................... 3 5. Selection of the Sector.......................................................................... 4 6. Selection of the Site ............................................................................. 4 APPROACH TO THE PROGRAM ...................................................................... 6 1. Area of research .................................................................................. 6 2. Beneficiaries........................................................................................ 6 3. Participants ........................................................................................ -

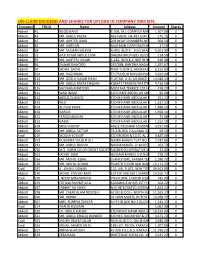

Un-Claim Dividend and Shares for Upload in Company Web Site

UN-CLAIM DIVIDEND AND SHARES FOR UPLOAD IN COMPANY WEB SITE. Company FOLIO Name Address Amount Shares Abbott 41 BILQIS BANO C-306, M.L.COMPLEX MIRZA KHALEEJ1,507.00 BEG ROAD,0 PARSI COLONY KARACHI Abbott 43 MR. ABDUL RAZAK RUFI VIEW, JM-497,FLAT NO-103175.75 JIGGAR MOORADABADI0 ROAD NEAR ALLAMA IQBAL LIBRARY KARACHI-74800 Abbott 47 MR. AKHTER JAMIL 203 INSAF CHAMBERS NEAR PICTURE600.50 HOUSE0 M.A.JINNAH ROAD KARACHI Abbott 62 MR. HAROON RAHEMAN CORPORATION 26 COCHINWALA27.50 0 MARKET KARACHI Abbott 68 MR. SALMAN SALEEM A-450, BLOCK - 3 GULSHAN-E-IQBAL6,503.00 KARACHI.0 Abbott 72 HAJI TAYUB ABDUL LATIF DHEDHI BROTHERS 20/21 GORDHANDAS714.50 MARKET0 KARACHI Abbott 95 MR. AKHTER HUSAIN C-182, BLOCK-C NORTH NAZIMABAD616.00 KARACHI0 Abbott 96 ZAINAB DAWOOD 267/268, BANTWA NAGAR LIAQUATABAD1,397.67 KARACHI-190 267/268, BANTWA NAGAR LIAQUATABAD KARACHI-19 Abbott 97 MOHD. SADIQ FIRST FLOOR 2, MADINA MANZIL6,155.83 RAMTLA ROAD0 ARAMBAG KARACHI Abbott 104 MR. RIAZUDDIN 7/173 DELHI MUSLIM HOUSING4,262.00 SOCIETY SHAHEED-E-MILLAT0 OFF SIRAJUDULLAH ROAD KARACHI. Abbott 126 MR. AZIZUL HASAN KHAN FLAT NO. A-31 ALLIANCE PARADISE14,040.44 APARTMENT0 PHASE-I, II-C/1 NAGAN CHORANGI, NORTH KARACHI KARACHI. Abbott 131 MR. ABDUL RAZAK HASSAN KISMAT TRADERS THATTAI COMPOUND4,716.50 KARACHI-74000.0 Abbott 135 SAYVARA KHATOON MUSTAFA TERRECE 1ST FLOOR BEHIND778.27 TOOSO0 SNACK BAR BAHADURABAD KARACHI. Abbott 141 WASI IMAM C/O HANIF ABDULLAH MOTIWALA95.00 MUSTUFA0 TERRECE IST FLOOR BEHIND UBL BAHUDARABAD BRANCH BAHEDURABAD KARACHI Abbott 142 ABDUL QUDDOS C/O M HANIF ABDULLAH MOTIWALA252.22 MUSTUFA0 TERRECE 1ST FLOOR BEHIND UBL BAHEDURABAD BRANCH BAHDURABAD KARACHI.