1998 Bank of America Summary Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bank of America Mortgage Securities

SECURITIES AND EXCHANGE COMMISSION FORM 8-K Current report filing Filing Date: 1999-04-30 | Period of Report: 1999-02-23 SEC Accession No. 0000914121-99-000408 (HTML Version on secdatabase.com) FILER BANK OF AMERICA MORTGAGE SECURITIES INC Mailing Address Business Address 345 MONTGOMERY ST 345 MONTGOMERY STREET CIK:1014956| IRS No.: 94324470 | State of Incorp.:DE | Fiscal Year End: 1231 LOWER LEVEL 2 UNIT 8152 LOWER LEVEL 2 UNIT 8152 Type: 8-K | Act: 34 | File No.: 333-34225 | Film No.: 99606246 SAN FRANCISCO CA 94104 SAN FRANCISCO CA SIC: 6189 Asset-backed securities 91110-7137 4154454779 Copyright © 2012 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report: February 23, 1999 (Date of earliest event reported) Commission File No. 333-67267 Bank of America Mortgage Securities, Inc. -------------------------------------------------------------------------------- Delaware 94-324470 --------------------------------- --------------------------------- (State of Incorporation) (I.R.S. Employer Identification No.) 345 Montgomery Street, Lower Level #2, Unit #8152, San Francisco, CA 94104 -------------------------------------------------------------------------------- Address of principal executive offices (Zip Code) (415) 445-4779 -------------------------------------------------------------------------------- Registrant's Telephone -

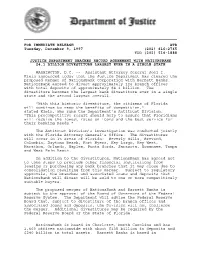

FOR IMMEDIATE RELEASE ATR Tuesday, December 9, 1997 (202

FOR IMMEDIATE RELEASE ATR Tuesday, December 9, 1997 (202) 616-2765 TDD (202) 514-1888 JUSTICE DEPARTMENT REACHES RECORD AGREEMENT WITH NATIONSBANK $4.1 BILLION DIVESTITURE LARGEST EVER IN A SINGLE STATE WASHINGTON, D.C. -- Assistant Attorney General Joel I. Klein announced today that the Justice Department has cleared the proposed merger of NationsBank Corporation with Barnett Banks. NationsBank agreed to divest approximately 124 branch offices with total deposits of approximately $4.1 billion. The divestiture becomes the largest bank divestiture ever in a single state and the second largest overall. "With this historic divestiture, the citizens of Florida will continue to reap the benefits of competition," stated Klein, who runs the Department’s Antitrust Division. "This procompetitive result should help to assure that Floridians will receive the lowest rates on loans and the best service for their banking needs." The Antitrust Division’s investigation was conducted jointly with the Florida Attorney General’s Office. The divestitures will occur in 15 areas of Florida: Beverly Hills, Brevard, Columbia, Daytona Beach, Fort Myers, Key Largo, Key West, Marathon, Orlando, Naples, Punta Gorda, Sarasota, Suwannee, Tampa and West Palm Beach. In addition to the divestitures, NationsBank has agreed not to take steps to preclude other financial institutions from leasing or purchasing any bank branches that it may close due to consolidation resulting from this merger. Subject to regulatory approvals, the branches and associated loans and deposits that NationsBank will divest will be sold to one or more competitively suitable buyers. The proposed merger of NationsBank and Barnett Banks is subject to the approval of the Board of Governors of the Federal Reserve System. -

Page 1 of 9 CEO May Be Rethinking Bofa's 'Crown Jewel'

CEO may be rethinking BofA's 'crown jewel' - Daily Report Page 1 of 9 • Law.com Home • Newswire • LawJobs • CLE Center • An incisivemedia website Welcome Megan My Account | Sign Out Get premi 3:17 P.M. EST Subscribe Thursday, February 05, 2009 Rec Home News Sections Court Opinions Court Calendars Public Notices Bench Boo Search Site: help News Articles Court Opinions Court Calendars Public Tuesday, January 13, 2009 Re CEO may be rethinking BofA's 'crown jewel' Lewis faces culture clash with retail bank's acquisition of Merrill Lynch By Edward Robinson, Bloomberg News Al When Kenneth Lewis, chief executive officer of Bank of America Corp., unveiled the acquisition of Merrill Lynch & Co. on Sept. 15, he called its 16,000-strong brokerage group the firm's “crown jewel.” Only a month later, the brokers were rebelling against their new parent. M Members of the Thundering Herd were steamed over the Bank of America • F employment contract they were asked to sign. Merrill was part of an industry • D group that let departing brokers who joined another member firm take their clients • H with them. The contract suggested that Bank of America might not join the group or honor the agreement. • L • E The advisers ridiculed their incoming retail banking bosses as “toaster salesmen” who didn't appreciate the bonds of the broker-client relationship. Some advisers AP threatened to walk, with their customers in tow, before the contract could go into effect, says a Merrill broker with 25 years of experience who requested Courtesy Bloomberg News confidentiality. Kenneth Lewis has been ridiculed by incoming Merrill Lewis, who has never displayed much affection for Wall Street, saw his $40.4 Lynch advisers as a “toaster billion acquisition devolving into a confrontation with the very people he'd praised salesman” who doesn't as Merrill's No. -

Form 10-Q Securities and Exchange

FORM 10-Q SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 (Mark One) (X) Quarterly report pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 FOR THE QUARTERLY PERIOD ENDED JUNE 30, 1997 ( ) Transition report pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 COMMISSION FILE NUMBER: 0-25464 DOLLAR TREE STORES, INC. (Exact name of registrant as specified in its charter) VIRGINIA 54-1387365 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 2555 ELLSMERE AVENUE NORFOLK COMMERCE PARK NORFOLK, VIRGINIA 23513 (Address of principal executives office) TELEPHONE NUMBER (757) 857-4600 (Registrants telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes (X) No ( ) As of August 1, 1997, there were 39,069,207 shares of the Registrant's Common Stock outstanding. DOLLAR TREE STORES, INC. and subsidiaries INDEX PART I. FINANCIAL INFORMATION Page No. ITEM 1. CONDENSED CONSOLIDATED FINANCIAL STATEMENTS: Condensed Consolidated Balance Sheets June 30, 1997 and December 31, 1996................................. 3 Condensed Consolidated Income Statements Three months and six months ended June 30, 1997 and 1996............ 4 Condensed Consolidated Statements of Cash Flows Six months ended June 30, 1997 and 1996............................. 5 Notes to Condensed Consolidated Financial Statements................ -

Case Study of the Bank of America and Merrill Lynch Merger

CASE STUDY OF THE MERGER BETWEEN BANK OF AMERICA AND MERRILL LYNCH Robert J. Rhee† The financial crisis of 2008 has posed innumerable problems in law, policy, and economics. A key event in the history of the financial crisis was Bank of America‟s acquisition of Merrill Lynch. Along with the fire sale of Bear Stearns and the bankruptcy of Lehman Brothers, the rescue of Merrill Lynch confirmed the worst fears about the financial crisis. Before this acquisition, Bank of America had long desired a top tier investment banking business, and Merrill Lynch represented a strategic opportunity to acquire a troubled but premier franchise of significant scale.1 As the financial markets continued to unravel after execution of the merger agreement, this golden opportunity turned into a highly risky gamble. Merrill Lynch was losing money at an astonishing rate, an event sufficient for Bank of America to consider seriously invoking the merger agreement‟s material adverse change clause. 2 The deal ultimately closed, but only after the government threatened to fire Bank of America‟s management and board if the company attempted to terminate the deal. The government took this coercive action to save the financial system from complete collapse. The harm to the financial system from a broken deal, officials feared, would have been unthinkable. The board‟s motivation is less clear. Like many classic corporate law cases, the factors influencing the board and management were complex. This case study examines these complexities, which raise important, unresolved issues in corporate governance and management. In 2008, three major investment banks—Bear Stearns, Lehman Brothers, and Merrill Lynch—collapsed or were acquired under distress, and these events played a large part in triggering the global financial crisis.3 In March, Bear Stearns † Associate Professor of Law, University of Maryland School of Law; J.D., The George Washington University; M.B.A., University of Pennsylvania (Wharton); B.A., University of Chicago. -

In Re: Fleetboston Financial Corporation Securities Litigation 02-CV

Case 2:02-cv-04561-GEB-MCA Document 28 Filed 04/23/2004 Page 1 of 36 NOT FOR PUBLICATION UNITED STATES DISTRICT COURT FOR THE DISTRICT OF NEW JERSEY Civ. No. 02-4561 (WGB) IN RE FLEETBOSTON FINANCIAL CORPORATION SECURITIES LITIGATION O P I N I O N APPEARANCES: Gary S. Graifman, Esq. Benjamin Benson, Esq. KANTROWITZ, GOLDHAMER & GRAIFMAN 210 Summit Avenue Montvale, New Jersey 07645 Liaison Counsel for Plaintiffs Samuel H. Rudman, Esq. CAULEY GELLER BOWMAN & COATES, LLP 200 Broadhollow Road, Suite 406 Melville, NY 11747 Co-Lead Counsel for Plaintiffs Joseph H. Weiss, Esq. WEISS & YOURMAN 551 Fifth Avenue, Suite 1600 New York, New York 10176 Co-Lead Counsel for Plaintiffs Jules Brody, Esq. Howard T. Longman, Esq. STULL, STULL & BRODY 6 East 45 th Street New York, New York 10017 Co-Lead Counsel for Plaintiffs 1 Case 2:02-cv-04561-GEB-MCA Document 28 Filed 04/23/2004 Page 2 of 36 David M. Meisels, Esq. HERRICK, FEINSTEIN LLP 2 Penn Plaza Newark, NJ 07105-2245 Mitchell Lowenthal, Esq. Jeffrey Rosenthal, Esq. CLEARY, GOTTLIEB, STEEN & HAMILTON One Liberty Plaza New York, NY 10006 Attorneys for Defendants BASSLER, DISTRICT JUDGE: This is a putative securities class action brought on behalf of all persons or entities except Defendants, who exchanged shares of Summit Bancorp (“Summit”) common stock for shares of FleetBoston Financial Corporation (“FBF”) common stock in connection with the merger between FBF and Summit. Defendants FBF and the individual Defendants 1 (collectively “Defendants”) move to dismiss Plaintiffs’ Consolidated Amended Complaint (“the Amended Complaint”) pursuant to Federal Rule of Civil Procedure Rule 12(b)(6). -

Zerohack Zer0pwn Youranonnews Yevgeniy Anikin Yes Men

Zerohack Zer0Pwn YourAnonNews Yevgeniy Anikin Yes Men YamaTough Xtreme x-Leader xenu xen0nymous www.oem.com.mx www.nytimes.com/pages/world/asia/index.html www.informador.com.mx www.futuregov.asia www.cronica.com.mx www.asiapacificsecuritymagazine.com Worm Wolfy Withdrawal* WillyFoReal Wikileaks IRC 88.80.16.13/9999 IRC Channel WikiLeaks WiiSpellWhy whitekidney Wells Fargo weed WallRoad w0rmware Vulnerability Vladislav Khorokhorin Visa Inc. Virus Virgin Islands "Viewpointe Archive Services, LLC" Versability Verizon Venezuela Vegas Vatican City USB US Trust US Bankcorp Uruguay Uran0n unusedcrayon United Kingdom UnicormCr3w unfittoprint unelected.org UndisclosedAnon Ukraine UGNazi ua_musti_1905 U.S. Bankcorp TYLER Turkey trosec113 Trojan Horse Trojan Trivette TriCk Tribalzer0 Transnistria transaction Traitor traffic court Tradecraft Trade Secrets "Total System Services, Inc." Topiary Top Secret Tom Stracener TibitXimer Thumb Drive Thomson Reuters TheWikiBoat thepeoplescause the_infecti0n The Unknowns The UnderTaker The Syrian electronic army The Jokerhack Thailand ThaCosmo th3j35t3r testeux1 TEST Telecomix TehWongZ Teddy Bigglesworth TeaMp0isoN TeamHav0k Team Ghost Shell Team Digi7al tdl4 taxes TARP tango down Tampa Tammy Shapiro Taiwan Tabu T0x1c t0wN T.A.R.P. Syrian Electronic Army syndiv Symantec Corporation Switzerland Swingers Club SWIFT Sweden Swan SwaggSec Swagg Security "SunGard Data Systems, Inc." Stuxnet Stringer Streamroller Stole* Sterlok SteelAnne st0rm SQLi Spyware Spying Spydevilz Spy Camera Sposed Spook Spoofing Splendide -

USCOURTS-Ca9-09-35307-1.Pdf

Case: 09-35307 01/18/2011 ID: 7614842 DktEntry: 67 Page: 1 of 67 FOR PUBLICATION UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT VANESSA SIMMONDS, Plaintiff-Appellant, v. CREDIT SUISSE SECURITIES (USA) LLC; JPMORGAN CHASE & CO., a Delaware corporation, successor in interest to Hambrecht & Quist and Chase Securities Inc.; BANK OF No. 09-35262 AMERICA CORPORATION, a Delaware D.C. No. 2:07-cv- corporation, successor in interest 01549-JLR to Fleetboston Robertson Stephens, Inc.; ONVIA INC., a Delaware corporation formerly known as Onvia.com Inc.; ROBERTSON STEPHENS, INC.; J.P. MORGAN SECURITIES INC., Defendants-Appellees. In Re: SECTION 16(b) LITIGATION 821 Case: 09-35307 01/18/2011 ID: 7614842 DktEntry: 67 Page: 2 of 67 822 SIMMONDS v. CREDIT SUISSE SECURITIES VANESSA SIMMONDS, Plaintiff-Appellant, v. DEUTSCHE BANK SECURITIES INC.; FOUNDRY NETWORKS INC., Nominal No. 09-35280 Defendant, a Delaware D.C. Nos. corporation; MERRILL LYNCH 2:07-cv-01566-JLR PIERCE FENNER & SMITH 2:07-cv-01549-JLR INCORPORATED; J.P. MORGAN SECURITIES INC., Defendants-Appellees. In Re: SECTION 16(b) LITIGATION VANESSA SIMMONDS, Plaintiff-Appellant, v. MERRILL LYNCH & CO. INC., Defendant, and No. 09-35282 D.C. Nos. FINISAR CORPORATION, Nominal Defendant, a Delaware 2:07-cv-01567-JLR 2:07-cv-01549-JLR corporation; MERRILL LYNCH PIERCE FENNER & SMITH INCORPORATED; J.P. MORGAN SECURITIES INC., Defendants-Appellees. In Re: SECTION 16(b) LITIGATION Case: 09-35307 01/18/2011 ID: 7614842 DktEntry: 67 Page: 3 of 67 SIMMONDS v. CREDIT SUISSE SECURITIES 823 VANESSA SIMMONDS, Plaintiff-Appellant, v. MORGAN STANLEY & CO., No. 09-35285 INCORPORATED; LEHMAN BROTHERS, D.C. -

CRA Decision #94 June 1999

Comptroller of the Currency Administrator of National Banks Washington, D.C. CRA Decision #94 June 1999 DECISION OF THE OFFICE OF THE COMPTROLLER OF THE CURRENCY ON THE APPLICATION TO MERGE BANK OF AMERICA NATIONAL TRUST AND SAVINGS ASSOCIATION, SAN FRANCISCO, CALIFORNIA, AND NATIONSBANK, NATIONAL ASSOCIATION, CHARLOTTE, NORTH CAROLINA May 20, 1999 _____________________________________________________________________________ I. INTRODUCTION On December 28, 1998, Bank of America National Trust and Savings Association (“BANTSA”), San Francisco, California, and NationsBank, National Association, Charlotte, North Carolina (“NationsBank”), applied to the Office of the Comptroller of the Currency ("OCC") for approval to merge NationsBank with and into BANTSA under BANTSA’s charter under 12 U.S.C. §§ 215a-1, 1828(c) and 1831u (the “Merger”). The resulting bank will be named “Bank of America, National Association” (“BofA-Resulting”) and will have its main office in Charlotte, North Carolina.1 Both banks are insured banks. BANTSA has its main office in California and, at the proposed consummation date for the Merger, will operate branches in California, Washington, Oregon, Idaho, Nevada, Arizona, Illinois, New York, and Florida.2 NationsBank has its main office in North Carolina and operates branches in North Carolina, South Carolina, Virginia, Maryland, the District of Columbia, Georgia, Florida, Tennessee, Illinois, 1 This application is part of the process of combining the banking operations of the subsidiary banks of the recently formed Bank of America Corporation (“New BAC”). NationsBank Corporation, Charlotte, North Carolina, merged with the former BankAmerica Corporation (“BankAmerica”), San Francisco, California. The resulting holding company is named Bank of America Corporation and is headquartered in Charlotte, North Carolina. -

Participant Bios Forum 2018 Revised

Indiaspora Leadership Forum 2018 Thinkers, Doers, Givers Bios Meenakshi Abbi joined RPA’s San Francisco office in May 2012 as a member of the Sponsored Projects & Funds team. She manages a portfolio of projects and donor collaboratives focused on a range of issues including education, diversity, improving philanthropy, impact investing, and other issues. Prior to her current role at RPA, Meenakshi worked at Tides for over four years as a program manager for fiscally sponsored 501(c)(3) and 501(c)(4) projects, and helped re-launch Tides Advocacy Fund. She was also Director of the Small Business Development Center Technology Advisory Program, a nonprofit dedicated to helping small businesses effectively utilize technology. Meenakshi holds a Bachelor’s degree in Computer Science. Her passions include civic engagement, financial inclusion, and social justice. She is on the advisory board of Fund the People, Justice Strategies and is the co-chair of Asian American Pacific Islanders in Philanthropy San Francisco’s Steering Committee. Qamar Adamjee, Malavalli Family Foundation Associate Curator of Art of the Indian Subcontinent at the Asian Art Museum in San Francisco, joined the museum in 2009. She received her PhD and MA in art history from New York University and an MBA in marketing from the Institute of Business Administration, Karachi (Pakistan). Before coming to the Asian, Adamjee worked in the Islamic department at The Metropolitan Museum of Art. Adamjee’s key interests lie in the intersections of art and culture and in connections between the past and our present. A specialist in Indian and Persian paintings, she has written, lectured, and organized exhibitions on subjects as diverse as Islamic art, Hindu and Sikh art, 19th-century photography, painting, and prints, Indian paintings, sculpture, and contemporary art. -

An Attempt to Legalize Hemp Farming in Tennessee Is Getting Pushback, Despite Its Economic Potential

TENNESSEE TITANS Deja vu all over again Neil O’Donnell explains what Fitzpatrick faces taking over at QB. ENTER Murphy’sTAINMENT law: P17 Nashville Hoops over U2 From Elvis to The Boss, the MTSU venue has seen some DaviDson • Williamson • sUmnER • ChEatham • Wilson RUthERFoRD • R great acts. But that was then. Ledger Brian Patterson Photos / shutterstock.com P16 oBERtson • maURY • DiCkson • montGomERY | October 4 – 10, 2013 www.nashvilleledger.com The power of information. Vol. 39 | Issue 40 F oR mer lY WESTVIEW sinCE 1978 An attempt to legalize hemp Page 13 farming in Tennessee is getting pushback, despite Dec.: Dec.: Keith Turner, Ratliff, Jeanan Mills Stuart, Resp.: Kimberly Dawn Wallace, Atty: Mary C Lagrone, 08/24/2010, 10P1318 its economic potential In re: Jeanan Mills Stuart, Princess Angela Gates, Jeanan Mills Stuart, Princess Angela Gates,Dec.: Resp.: Kim Prince Patrick, Angelo Terry Patrick, Gates, Atty: Monica D Edwards, 08/25/2010, 10P1326 In re: Keith Turner, TN Dept Of Correction, www.westviewonline.com TN Dept Of Correction, Resp.: Johnny Moore,Dec.: Melinda Atty: Bryce L Tomlinson, Coatney, Resp.: Pltf(s): Rodney A Hall, Pltf Atty(s): n/a, 08/27/2010, 10P1336 In re: Kim Patrick, Terry Patrick, Pltf(s): Sandra Heavilon, Resp.: Jewell Tinnon, Atty: Ronald Andre Stewart, 08/24/2010,Dec.: Seton Corp 10P1322 Insurance Company, Dec.: Regions Bank, Resp.: Leigh A Collins, In re: Melinda L Tomlinson, Def(s): Jit Steel Transport Inc, National Fire Insurance Company, Elizabeth D Hale, Atty: William Warner McNeilly, 08/24/2010, Def Atty(s): J Brent Moore, 08/26/2010, 10C3316 10P1321 Dec.: Amy In Tennessee, the idea of hemp is hot. -

09-35262.Pdf

FOR PUBLICATION UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT VANESSA SIMMONDS, Plaintiff-Appellant, v. CREDIT SUISSE SECURITIES (USA) LLC; JPMORGAN CHASE & CO., a Delaware corporation, successor in interest to Hambrecht & Quist and Chase Securities Inc.; BANK OF No. 09-35262 AMERICA CORPORATION, a Delaware D.C. No. 2:07-cv- corporation, successor in interest 01549-JLR to Fleetboston Robertson Stephens, Inc.; ONVIA INC., a Delaware corporation formerly known as Onvia.com Inc.; ROBERTSON STEPHENS, INC.; J.P. MORGAN SECURITIES INC., Defendants-Appellees. In Re: SECTION 16(b) LITIGATION 821 822 SIMMONDS v. CREDIT SUISSE SECURITIES VANESSA SIMMONDS, Plaintiff-Appellant, v. DEUTSCHE BANK SECURITIES INC.; FOUNDRY NETWORKS INC., Nominal No. 09-35280 Defendant, a Delaware D.C. Nos. corporation; MERRILL LYNCH 2:07-cv-01566-JLR PIERCE FENNER & SMITH 2:07-cv-01549-JLR INCORPORATED; J.P. MORGAN SECURITIES INC., Defendants-Appellees. In Re: SECTION 16(b) LITIGATION VANESSA SIMMONDS, Plaintiff-Appellant, v. MERRILL LYNCH & CO. INC., Defendant, and No. 09-35282 D.C. Nos. FINISAR CORPORATION, Nominal Defendant, a Delaware 2:07-cv-01567-JLR 2:07-cv-01549-JLR corporation; MERRILL LYNCH PIERCE FENNER & SMITH INCORPORATED; J.P. MORGAN SECURITIES INC., Defendants-Appellees. In Re: SECTION 16(b) LITIGATION SIMMONDS v. CREDIT SUISSE SECURITIES 823 VANESSA SIMMONDS, Plaintiff-Appellant, v. MORGAN STANLEY & CO., No. 09-35285 INCORPORATED; LEHMAN BROTHERS, D.C. Nos. INC.; BANK OF AMERICA 2:07-cv-01568-JLR CORPORATION; ROBERTSON 2:07-cv-01549-JLR STEPHENS, INC.; AVANEX CORPORATION, Defendants-Appellees. In Re: SECTION 16(b) LITIGATION VANESSA SIMMONDS, Plaintiff-Appellant, v. CREDIT SUISSE GROUP, a global bank headquartered in Zurich, Switzerland formerly known as Credit Suisse First Boston No.