Audit Report on the Accounts of Union Committees / Councils of Sindh Audit Year 2017-18

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CIVIL TRANSPORTERS - BAHRIA COLLEGE KARSAZ Transport Incharge : Javed Amjad Kayani: 0343-2432072 - 0302-5723178

CIVIL TRANSPORTERS - BAHRIA COLLEGE KARSAZ Transport Incharge : Javed Amjad Kayani: 0343-2432072 - 0302-5723178 S# Name Contact # Vehicle Route Morning & Evening 1 Abdul Salam 3002185124 Hiace Saddar, Garden, Jamshed Road 2 Abid Sheikh 3002454876 Hiroof University, Gulistan-e-Johar, Kiran Hospital 3 Amin Ud Din 3002519301 Hiace PIB Colony, Jamshed Raod, Chandni Chok, Bahadurabad 4 Shahbaz 3139030400 Hiroof Dalmian NHS Phase I & II 5 Asif 3432468290 Hiroof Shah Faisal, Rafay e Ama, Jumma Goth, Green Town 6 Atta Ullah 3332224684 Hiroof Majeed SRE, Dalmia 7 Bilal 3320337639 Hiace Manzor Colony DHA Phase II Qayumabad 8 Faisal Abbas 3462593009 Mazda Nagan Chorangi, Disco Bakery, Maskan 9 Farhat Abbas 3002327290 Coaster Gulshan-e-Jamal, Gulistan-e-Jouhar, Rabia City 10 Fiaz 3101288299 Hiace Azizabad, Karimabad, Gol Market 11 Haseeb 3162594642 Hiace 4K, Bufferzone, Shafi Mor, Sohrab Goth 12 Imran 3338999790 Hiroof Baloch Colony, Manzoor Colony 13 Imran Burfat 3213380750 Hiroof Dalmia 14 Islam ud Din 3332294481 Coaster Gulistan-e-Johar 15 Jamil ud Din 3003645880 Coaster Shah Faisal Colony 16 Jaseem Ahmed Khan 3002484125 Hiroof saudi Town, Safora, Malir Cantt, Karachi Universty falcon 17 K M Yaqoob 3002170136 Mazda Gulshan-e-Iqbal, Mochi Mor, Expo Centre 18 Kaleem 3462695707 Coaster Essa Nagri, Azizabad, Tahir Villa, 4K Chorangi 19 Khan Baba 3332294959 Hiace Bhadurabad, Sharfabad, Guru Mander, Soldier Bazar 20 M Aqil 3161605887 Hi-Roof Shah Faisal 1 , 2 , 3 and 5 Golden Town 21 M Yamin 3012721186 Hiace Nursery, NORE-I, Lucky Star 22 M. Akbar 3002157893 Hiroof Clifton,Seaview,Teen Talwar,NORE II Sharahefaisal 23 M. Farooq Patel 3073516561 Hiace Landhi, Quaidabad 24 M. -

Askari Bank Limited List of Shareholders (W/Out Cnic) As of December 31, 2017

ASKARI BANK LIMITED LIST OF SHAREHOLDERS (W/OUT CNIC) AS OF DECEMBER 31, 2017 S. NO. FOLIO NO. NAME OF SHAREHOLDERS ADDRESSES OF THE SHAREHOLDERS NO. OF SHARES 1 9 MR. MOHAMMAD SAEED KHAN 65, SCHOOL ROAD, F-7/4, ISLAMABAD. 336 2 10 MR. SHAHID HAFIZ AZMI 17/1 6TH GIZRI LANE, DEFENCE HOUSING AUTHORITY, PHASE-4, KARACHI. 3280 3 15 MR. SALEEM MIAN 344/7, ROSHAN MANSION, THATHAI COMPOUND, M.A. JINNAH ROAD, KARACHI. 439 4 21 MS. HINA SHEHZAD C/O MUHAMMAD ASIF THE BUREWALA TEXTILE MILLS LTD 1ST FLOOR, DAWOOD CENTRE, M.T. KHAN ROAD, P.O. 10426, KARACHI. 470 5 42 MR. M. RAFIQUE B.R.1/27, 1ST FLOOR, JAFFRY CHOWK, KHARADHAR, KARACHI. 9382 6 49 MR. JAN MOHAMMED H.NO. M.B.6-1728/733, RASHIDABAD, BILDIA TOWN, MAHAJIR CAMP, KARACHI. 557 7 55 MR. RAFIQ UR REHMAN PSIB PRIVATE LIMITED, 17-B, PAK CHAMBERS, WEST WHARF ROAD, KARACHI. 305 8 57 MR. MUHAMMAD SHUAIB AKHUNZADA 262, SHAMI ROAD, PESHAWAR CANTT. 1919 9 64 MR. TAUHEED JAN ROOM NO.435, BLOCK-A, PAK SECRETARIAT, ISLAMABAD. 8530 10 66 MS. NAUREEN FAROOQ KHAN 90, MARGALA ROAD, F-8/2, ISLAMABAD. 5945 11 67 MR. ERSHAD AHMED JAN C/O BANK OF AMERICA, BLUE AREA, ISLAMABAD. 2878 12 68 MR. WASEEM AHMED HOUSE NO.485, STREET NO.17, CHAKLALA SCHEME-III, RAWALPINDI. 5945 13 71 MS. SHAMEEM QUAVI SIDDIQUI 112/1, 13TH STREET, PHASE-VI, DEFENCE HOUSING AUTHORITY, KARACHI-75500. 2695 14 74 MS. YAZDANI BEGUM HOUSE NO.A-75, BLOCK-13, GULSHAN-E-IQBAL, KARACHI. -

DC Valuation Table (2018-19)

VALUATION TABLE URBAN WAGHA TOWN Residential 2018-19 Commercial 2018-19 # AREA Constructed Constructed Open Plot Open Plot property per property per Per Marla Per Marla sqft sqft ATTOKI AWAN, Bismillah , Al Raheem 1 Garden , Al Ahmed Garden etc (All 275,000 880 375,000 1,430 Residential) BAGHBANPURA (ALL TOWN / 2 375,000 880 700,000 1,430 SOCITIES) BAGRIAN SYEDAN (ALL TOWN / 3 250,000 880 500,000 1,430 SOCITIES) CHAK RAMPURA (Garision Garden, 4 275,000 880 400,000 1,430 Rehmat Town etc) (All Residential) CHAK DHEERA (ALL TOWN / 5 400,000 880 1,000,000 1,430 SOCIETIES) DAROGHAWALA CHOWK TO RING 6 500,000 880 750,000 1,430 ROAD MEHMOOD BOOTI 7 DAVI PURA (ALL TOWN / SOCITIES) 275,000 880 350,000 1,430 FATEH JANG SINGH WALA (ALL TOWN 8 400,000 880 1,000,000 1,430 / SOCITIES) GOBIND PURA (ALL TOWNS / 9 400,000 880 1,000,000 1,430 SOCIEITIES) HANDU, Al Raheem, Masha Allah, 10 Gulshen Dawood,Al Ahmed Garden (ALL 250,000 880 350,000 1,430 TOWN / SOCITIES) JALLO, Al Hafeez, IBL Homes, Palm 11 250,000 880 500,000 1,430 Villas, Aziz Garden etc KHEERA, Aziz Garden, Canal Forts, Al 12 Hafeez Garden, Palm Villas (ALL TOWN 250,000 880 500,000 1,430 / SOCITIES) KOT DUNI CHAND Al Karim Garden, 13 Malik Nazir G Garden, Ghous Garden 250,000 880 400,000 1,430 (ALL TOWN / SOCITIES) KOTLI GHASI Hanif Park, Garision Garden, Gulshen e Haider, Moeez Town & 14 250,000 880 500,000 1,430 New Bilal Gung H Scheme (ALL TOWN / SOCITIES) LAKHODAIR, Al Wadood Garden (ALL 15 225,000 880 500,000 1,430 TOWN / SOCITIES) LAKHODAIR, Ring Road Par (ALL TOWN 16 75,000 880 200,000 -

Central-Karachi

Central-Karachi 475 476 477 478 479 480 Travelling Stationary Inclass Co- Library Allowance (School Sub Total Furniture S.No District Teshil Union Council School ID School Name Level Gender Material and Curricular Sport Total Budget Laboratory (School Specific (80% Other) 20% supplies Activities Specific Budget) 1 Central Karachi New Karachi Town 1-Kalyana 408130186 GBELS - Elementary Elementary Boys 20,253 4,051 16,202 4,051 4,051 16,202 64,808 16,202 81,010 2 Central Karachi New Karachi Town 4-Ghodhra 408130163 GBLSS - 11-G NEW KARACHI Middle Boys 24,147 4,829 19,318 4,829 4,829 19,318 77,271 19,318 96,589 3 Central Karachi New Karachi Town 4-Ghodhra 408130167 GBLSS - MEHDI Middle Boys 11,758 2,352 9,406 2,352 2,352 9,406 37,625 9,406 47,031 4 Central Karachi New Karachi Town 4-Ghodhra 408130176 GBELS - MATHODIST Elementary Boys 20,492 4,098 12,295 8,197 4,098 16,394 65,576 16,394 81,970 5 Central Karachi New Karachi Town 6-Hakim Ahsan 408130205 GBELS - PIXY DALE 2 Registred as a Seconda Elementary Girls 61,338 12,268 49,070 12,268 12,268 49,070 196,281 49,070 245,351 6 Central Karachi New Karachi Town 9-Khameeso Goth 408130174 GBLSS - KHAMISO GOTH Middle Mixed 6,962 1,392 5,569 1,392 1,392 5,569 22,278 5,569 27,847 7 Central Karachi New Karachi Town 10-Mustafa Colony 408130160 GBLSS - FARZANA Middle Boys 11,678 2,336 9,342 2,336 2,336 9,342 37,369 9,342 46,711 8 Central Karachi New Karachi Town 10-Mustafa Colony 408130166 GBLSS - 5/J Middle Boys 28,064 5,613 16,838 11,226 5,613 22,451 89,804 22,451 112,256 9 Central Karachi New Karachi -

Public Notice Auction of Gold Ornament & Valuables

PUBLIC NOTICE AUCTION OF GOLD ORNAMENT & VALUABLES Finance facilities were extended by JS Bank Limited to its customers mentioned below against the security of deposit and pledge of Gold ornaments/valuables. The customers have neglected and failed to repay the finances extended to them by JS Bank Limited along with the mark-up thereon. The current outstanding liability of such customers is mentioned below. Notice is hereby given to the under mentioned customers that if payment of the entire outstanding amount of finance along with mark-up is not made by them to JS Bank Limited within 15 days of the publication of this notice, JS Bank Limited shall auction the Gold ornaments/valuables after issuing public notice regarding the date and time of the public auction and the proceeds realized from such auction shall be applied towards the outstanding amount due and payable by the customers to JS Bank Limited. No further public notice shall be issued to call upon the customers to make payment of the outstanding amounts due and payable to JS Bank as mentioned hereunder: Customer ID Customer Name Address Amount as of 8th April 1038553 ZAHID HUSSAIN MUHALLA MASANDPURSHI KARPUR SHIKARPUR 343283.35 1012051 ZEESHAN ALI HYDERI MUHALLA SHIKA RPUR SHIKARPUR PK SHIKARPUR 409988.71 1008854 NANIK RAM VILLAGE JARWAR PSOT OFFICE JARWAR GHOTKI 65110 PAK SITAN GHOTKI 608446.89 999474 DARYA KHAN THENDA PO HABIB KOT TALUKA LAKHI DISTRICT SHIKARPU R 781000 SHIKARPUR PAKISTAN SHIKARPUR 361156.69 352105 ABDUL JABBAR FAZALEELAHI ESTATE S HOP NO C12 BLOCK 3 SAADI TOWN -

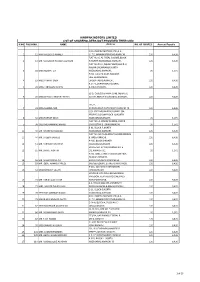

Hinopak Motors Limited List of Shareholders Not Provided Their Cnic S.No Folio No

HINOPAK MOTORS LIMITED LIST OF SHAREHOLDERS NOT PROVIDED THEIR CNIC S.NO FOLIO NO. NAME Address NO. OF SHARES Amount Payable C/O HINOPAK MOTORS LTD.,D-2, 1 12 MIR MAQSOOD AHMED S.I.T.E.,MANGHOPIR ROAD,KARACHI., 120 6,426 FLAT NO. 6, AL-FAZAL SQUARE,BLOCK- 2 13 MR. MANZOOR HUSSAIN QURESHI H,NORTH NAZIMABAD,KARACHI., 120 6,426 FLAT NO.19-O, IQBAL PLAZA,BLOCK-O, NAGAN CHOWRANGI,NORTH 3 18 MISS NUSRAT ZIA NAZIMABAD,KARACHI., 20 1,071 H.NO. E-13/40,NEAR RAILWAY LINE,GHARIBABAD, 4 19 MISS FARHAT SABA LIAQUATABAD,KARACHI., 120 6,426 R.177-1,SHARIFABADFEDERAL 5 24 MISS TABASSUM NISHAT B.AREA,KARACHI., 120 6,426 52-D, Q-BLOCK,PAHAR GANJ, NEAR LAL 6 28 MISS SHAKILA ANWAR FATIMA KOTTHI,NORTH NAZIMABAD,KARACHI., 120 6,426 171/2, 7 31 MISS SAMINA NAZ AURANGABAD,NAZIMABAD,KARACHI-18. 120 6,426 C/O. SYED MUJAHID HUSSAINP-394, PEOPLES COLONYBLOCK-N, NORTH 8 32 MISS FARHAT ABIDI NAZIMABADKARACHI, 20 1,071 FLAT NO. A-3FARAZ AVENUE, BLOCK- 9 38 SYED MOHAMMAD HAMID 20GULISTAN-E-JOHARKARACHI, 20 1,071 B-91, BLOCK-P,NORTH 10 40 MR. KHURSHID MAJEED NAZIMABAD,KARACHI. 120 6,426 FLAT NO. M-45,AL-AZAM SQUARE,FEDRAL 11 44 MR. SALEEM JAWEED B. AREA,KARACHI., 120 6,426 A-485, BLOCK-DNORTH 12 51 MR. FARRUKH GHAFFAR NAZIMABADKARACHI. 120 6,426 HOUSE NO. D/401,KORANGI NO. 5 13 55 MR. SHAKIL AKHTAR 1/2,KARACHI-31. 20 1,071 H.NO. 3281, STREET NO.10,NEW FIDA HUSSAIN SHAIKHA 14 56 MR. -

Folio No. Title Address Unclaimed Amount of Dividend Warrant No Year

Unclaimed Warrant Folio No. Title Address Amount of Year No Dividend 13 MST. BADAR BEGUM N/A 4,500 29 1989 273 MR. FAYYAZ AHMED MALIK 318 - R.A BAZAR RAWALPINDI 1,225 180 1990 1466 MRS. SAFINA SALIM GODIL 55-K.M.C.H SOCIETY OFF ALAMGIR ROAD, KARACHI 245 891 1990 447 MR. MOHAMMED JAVED N/A 2,450 281 1990 454 MR. YAHYA N/A 245 286 1990 529 MR. WASEEM HAMEED N/A 245 339 1990 744 MISS FARIDA N/A 1,960 469 1990 933 MR. MOHAMMED SIDDIQUE N/A 490 585 1990 258 MR. IQBAL PIRANI A-72 Block-5, Gulshan e Iqbal, KDA Scheme No.24, Karachi 1,800 127 1991 1483 SHEIKH MOHAMMED AHSAN S/O. SH. ALLAH DITTA SAIDPURI GATE Q-287 RAWALPINDI 1,675 492 1991 528 MR. ARIF SAEED N/A 335 203 1991 755 MISS FARIDA N/A 1,005 265 1991 857 MR. ABID HUSSAIN N/A 335 300 1991 1639 MR. MAHBOOB HUSSAIN N/A 335 589 1991 156 MR. MOHAMMED AMIN FAZLANI N/A 335 68 1992 236 MUFTI JAVAID AZIZ 119- Gulbahar Colony No.1, Peshawar City 1,675 96 1992 W/O. MOHAMMAD YOUSAF 3RD FLOOR, JANNAT SITARA MANSION, 1340 MST. KULSUM 335 306 1992 ASLAM ROAD, EIDGAH, KARACHI 1466 MRS. SAFINA SALIM GODIL 55-K.M.C.H SOCIETY OFF ALAMGIR ROAD, KARACHI 335 1466 1992 1483 SHEIKH MOHAMMED AHSAN S/O. SH. ALLAH DITTA SAIDPURI GATE Q-287 RAWALPINDI 1,675 1483 1992 1652 MRS. ZUBEDA BEGUM N/A 335 1652 1992 Page 1 of 32 Unclaimed Warrant Folio No. -

(Rfp) for Front End Collection and Disposal of Municipal Solid Waste for Zone Korangi (Dmc Korangi Area) Karachi, Sindh, Pakistan

REQUEST FOR PROPOSAL (RFP) FOR FRONT END COLLECTION AND DISPOSAL OF MUNICIPAL SOLID WASTE FOR ZONE KORANGI (DMC KORANGI AREA) KARACHI, SINDH, PAKISTAN. Executive Director (Operation-I) Sindh Solid Waste Management Board (SSWMB) Govt. of Sindh SSWMB – NIT-16 Table of Content Sindh Solid Waste Management Board Section-I Preamble Clause# Page# 1.1 Purpose of Request for Proposal 8 1.2 Scope of Work/Assignment 8 1.3 Brief Description of DMC Korangi 8 1.4 MAP of DMC Korangi 9 1.5 Definition & Interpretation 9 1.6 Abbreviation 10 1.7 Section of RFP/Bidding Documents 11 1.8 Procuring Agency Right to cancel any or all proposals/tenders 11 Section-II Instructions to Contractors/Bidders. Clause# Page# 2.1 Information related to procuring agency 13 2.2 Language of proposal and correspondence 13 2.3 Method of Procurement 13 2.4 Period of Contract 13 2.5 Pre-proposal Meeting 13 2.6 Clarification and modifications of Bidding Document 14 2.7 Visit of the area of Service 14 2.8 Utilization of Existing Work Force on SWM of DMC Korangi 14 2.9 Utilization of Existing Solid Waste Collection & Transportation Vehicle of 16 DMC Korangi. 2.10 Utilization of Existing Facilities i.e. Workshop, Offices of DMC Korangi 17 2.11 Amendment through Addendums 17 2.12 Cancelation of Tender before Tender Time 17 2.13 Proposal Preparation Cost/Cost of bidding 17 2.14 Bid submitted by a Joint Venture/Consortium 18 2.15 Place, date, time and manner of submission of Tender/Bid Document 19 2.16 Currency Unit of Offers and Payments 21 2.17 Conditional and Partial Offers 22 2.18 -

East-Karachi

East-Karachi 475 476 477 478 479 480 Travelling Stationary Inclass Co- Library Allowance (School Sub Total Furniture S.No District Teshil Union Council School ID School Name Level Gender Material and Curricular Sport Total Budget Laboratory (School Specific (80% Other) 20% supplies Activities Specific Budget) 1 East Karachi Jamshed Town 1-Akhtar Colony 408070173 GBLSS - H.M.A. Middle Mixed 7,841 1,568 4,705 3,137 1,568 6,273 25,093 6,273 31,366 2 East Karachi Jamshed Town 2-Manzoor Colony 408070139 GBPS - BILAL MASJID NO.2 Primary Mixed 12,559 2,512 10,047 2,512 2,512 10,047 40,189 10,047 50,236 3 East Karachi Jamshed Town 2-Manzoor Colony 408070174 GBLSS - UNION Middle Mixed 16,613 3,323 13,290 3,323 3,323 13,290 53,161 13,290 66,451 4 East Karachi Jamshed Town 9-Central Jacob Line 408070171 GBLSS - BATOOL GOVT` BOYS`L/SEC SCHOOL Middle Mixed 12,646 2,529 10,117 2,529 2,529 10,117 40,466 10,117 50,583 5 East Karachi Jamshed Town 10-Jamshed Quarters 408070160 GBLSS - AZMAT-I-ISLAM Middle Boys 22,422 4,484 17,937 4,484 4,484 17,937 71,749 17,937 89,687 6 East Karachi Jamshed Town 10-Jamshed Quarters 408070162 GBLSS - RANA ACADEMY Middle Boys 13,431 2,686 8,059 5,372 2,686 10,745 42,980 10,745 53,724 7 East Karachi Jamshed Town 10-Jamshed Quarters 408070163 GBLSS - MAHMOODABAD Middle Boys 20,574 4,115 12,344 8,230 4,115 16,459 65,836 16,459 82,295 8 East Karachi Jamshed Town 11-Garden East 408070172 GBLSS - GULSHAN E FATIMA Middle Mixed 16,665 3,333 13,332 3,333 3,333 13,332 53,327 13,332 66,658 9 East Karachi Gulshan-e-Iqbal Town 3-PIB -

January 2018 NEWS COVERAGE PERIOD from JANUARY 29TH to FEBRUARY 4TH 2017

The Globalization Bulletin Environment January 2018 NEWS COVERAGE PERIOD FROM JANUARY 29TH TO FEBRUARY 4TH 2017 DENSE FOG DISRUPTS LIFE IN PUNJAB Business Recorder, January 29, 2018 Lahore: Dense fog and poor visibility during the night and morning hours continue to disrupt life as the Highway Police has warned the commuters against unnecessary travelling to avoid fatal accidents. The Met office has said that weather remained cold and dry in most parts of the country on Sunday. Dense fog prevailed over plain areas of Punjab and Sukkur division. Dense fog is likely to occur in plain areas of Punjab and upper Sindh during the night and morning hours on Monday. As the blanket of fog disrupted normal traffic on motorways and national highways in Punjab and Sukkur division it also disrupted flight and train schedule due to poor visibility. With regard to synoptic situation the Met office said that a westerly wave is likely to enter western parts of the country tonight and likely to grip upper parts on Monday. It may persist over northern areas till Tuesday. Predicting rain/snowfall on Monday and Tuesday, it said rain/thunderstorm is expected at scattered places in Malakand, Hazara, Mardan, Quetta, and Zhob divisions, Fata, Gilgit Baltistan and Kashmir while at isolated places in Bannu, Peshawar, Kohat, Kalat, Rawalpindi, Gujranwala, Sargodha divisions and Islamabad on Monday/Tuesday. Snowfall is also expected in Malakand division, Gallyat, Naran, Kaghan, Murree, Kashmir and Gilgit-Baltistan during the period. https://epaper.brecorder.com/2018/01/29/5-page/696776-news.htl SOME 20,000 PREMATURE DEATHS LINKED TO AIR POLLUTION The Express Tribune, January 29th, 2018. -

Government of Sindh Finance Department

2021-22 Finance Department Government of Sindh 1 SC12102(102) GOVERNOR'S SECRETARIAT/ HOUSE Rs Charged: ______________ Voted: 51,652,000 ______________ Total: 51,652,000 ______________ ____________________________________________________________________________________________ GOVERNOR'S SECRETARIAT ____________________________________________________________________________________________ BUILDINGS ____________________________________________________________________________________________ P./ADP DDO Functional-Cum-Object Classification & Budget NO. NO. Particular Of Scheme Estimates 2021 - 2022 ____________________________________________________________________________________________ Rs 01 GENERAL PUBLIC SERVICE 011 EXECUTIVE & LEGISLATIVE ORGANS, FINANCAL 0111 EXECUTIVE AND LEGISLATIVE ORGANS 011103 PROVINCIAL EXECUTIVE KQ5003 SECRETARY (GOVERNOR'S SECRETARIAT/ HOUSE) ADP No : 0733 KQ21221562 Constt. of Multi-storeyed Flats Phase-II at Sindh Governor's 51,652,000 House, Karachi (48 Nos.) including MT-s A12470 Others 51,652,000 _____________________________________________________________________________ Total Sub Sector BUILDINGS 51,652,000 _____________________________________________________________________________ TOTAL SECTOR GOVERNOR'S SECRETARIAT 51,652,000 _____________________________________________________________________________ 2 SC12104(104) SERVICES GENERAL ADMIN & COORDINATION Rs Charged: ______________ Voted: 1,432,976,000 ______________ Total: 1,432,976,000 ______________ _____________________________________________________________________________ -

LIST of POLLING STATIONS for a CONSTITUENCY of Election to the Provincial Assembly of the Sindh PS-116 KARACHI WEST-V

ELECTION COMMISSION OF PAKISTAN FORM-28 [see rule 50] LIST OF POLLING STATIONS FOR A CONSTITUENCY OF Election to the Provincial Assembly of the Sindh PS-116 KARACHI WEST-V Number of voters as igned to In Case of Rural Areas In Case of Urban Areas Number of polling booths S. No. of voters polling station on the electoral No. and Name of Polling Sr. No. roll in case Station Census Block Census Block Name of Electoral Areas Name of Electoral Areas electoral area is Male Female Total Male Female Total Code Code bifurcated 1 2 3 4 5 6 7 8 9 10 11 12 13 Islam Nagar 408010101 - 0 423 207 630 1 Babul Ilam Sec School Islam Nagar 408010102 - - 0 356 0 356 2 1 3 Islam Nagar 408010108 -- 0 302 0 302 1 Total - -- 1081 207 1288 2 1 3 Islam Nagar 408010103 - 0 284 0 284 Islam Nagar 408010104 - - 0 234 0 234 Islam Nagar 408010105 0 117 0 117 2 Babul Ilam Sec School 3 0 3 Islam Nagar 408010106 0 211 0 211 Islam Nagar 408010107 -- 0 461 0 461 Islam Nagar 408010109 -- 0 201 0 201 2 Total - - 1508 0 1508 3 0 3 Islam Nagar 408010102 - - 0 0 243 243 Islam Nagar 408010103 - 0 0 170 170 Islam Nagar 408010104 - 0 0 152 152 Islam Nagar 408010105 - - 0 0 72 72 3 Babul Ilam Sec School 0 - 3 3 Islam Nagar 408010106 - 0 0 126 126 Islam Nagar 408010107 - 0 0 281 281 Islam Nagar 408010108 -- 0 0 116 116 Islam Nagar 408010109 - - 0 0 156 156 3 Total - - - 0 1316 1316 0 3 3 Abidabad BI-A Islam 408010201 - - 0 330 197 527 Nagar Abidabad BI-A Islam 4 GBPS Siddiqui, Abidabad 408010202 - 0 401 207 608 2 1 3 Nagar Abidabad BI-A Islam 408010203 - 0 101 68 169 Nagar 4 Total - - - 832 472 1304 2 1 3 Number of voters assigned to Number of polling booths In Case of Rural Areas In Case of Urban Areas 5.